Get our free Debt vs Invest Calculator — click here to access it

Canadian Personal Finance Terms You Need to Know Before Your First 100k

Canadian personal finance terms explained in plain language with real examples to help beginners understand investing, taxes, and portfolio building on the path to their first 100k.

FINANCIAL BASICS

1/2/202611 min read

Introduction

Have you ever been in a room where no one speaks the same language as you? It feels uncomfortable and confusing. Unfortunately, many young Canadians feel this exact way when it comes to money conversations. Everything sounds like jargon, and it’s easy to feel overwhelmed.

This isn’t because you lack the ability to understand personal finance. It’s because most people were never taught the language of money.

Search the word “investing” on YouTube and you’ll quickly hear terms like bull and bear markets, asset allocation, dividend yield, capital gains, and volatility. When something feels confusing, the natural reaction is to disengage and avoid it altogether.

Our goal at NextGenFinance Canada is to change that. If your objective is to build your first $100,000 then understanding the core vocabulary of Canadian personal finance is a non-negotiable first step.

When you understand the words, you understand the decisions. When you understand the decisions, you start making choices that move your net worth forward.

Investing Terms

Asset

An asset is anything you own that has economic value, either today or in the future. Assets can generate income, appreciate in value, or both.

Example: If you have $4,000 invested in a TFSA and a car worth $8,000, your total assets equal $12,000.

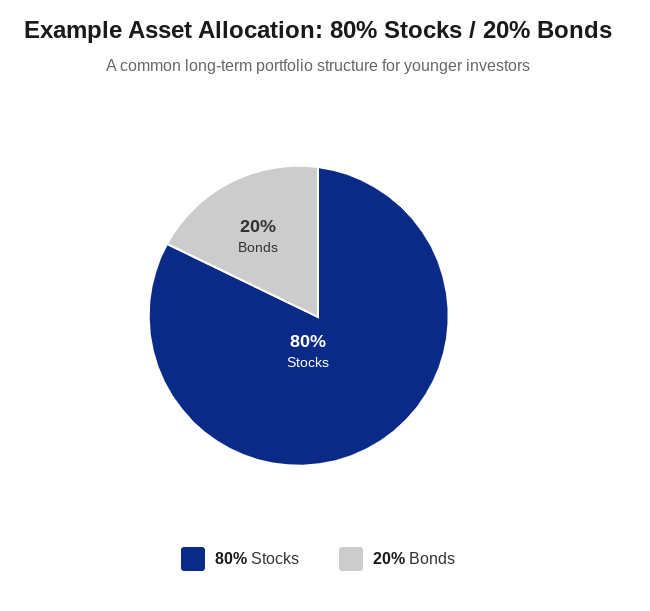

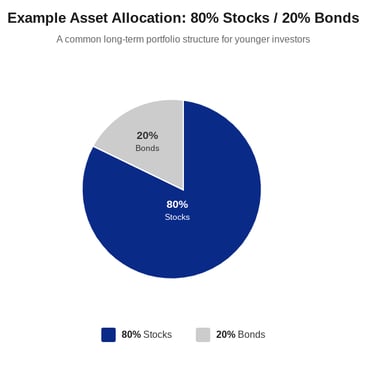

Asset Allocation

Asset allocation refers to how your investments are divided across asset classes such as stocks, bonds, cash, and real estate. It is one of the biggest drivers of long-term investment returns and risk.

Example: An 80/20 portfolio means 80% of your investments are in stocks and 20% are in bonds, a common recommendation for younger investors with longer time horizons.

Balanced Portfolio

A balanced portfolio generally refers to a mix of stocks and bonds designed to balance growth and stability. There is no single definition, but the term often implies moderate risk.

Example: A 60/40 portfolio (60% stocks, 40% bonds) is commonly described as balanced.

Balanced Stock Portfolio

A balanced stock portfolio spreads investments across different sectors and geographic regions to reduce reliance on any single company, industry, or country.

Balanced Bond Portfolio

A balanced bond portfolio holds bonds with varying maturities, issuers, and credit qualities to manage interest-rate and credit risk.

Bear Market

A bear market occurs when markets experience prolonged declines, typically defined as a drop of 20% or more from recent highs. Bear markets are often associated with fear and negative investor sentiment.

Example: When media says “the bears are out for Apple,” it means selling pressure is outweighing buying, pushing prices lower.

Bull Market

A bull market is a sustained period of rising prices and positive investor sentiment. Bull markets often coincide with economic growth and strong corporate earnings.

Blue Chip Stock

A blue chip stock represents a large, established company with a long history of financial stability and reliable operations.

Example: Major Canadian banks such as the Bank of Montreal, which has operated for over 200 years, are classic blue-chip stocks.

Buy and Hold

Buy and hold is an investment strategy where assets are purchased and held for long periods, regardless of short-term market fluctuations. This approach focuses on long-term growth rather than frequent trading.

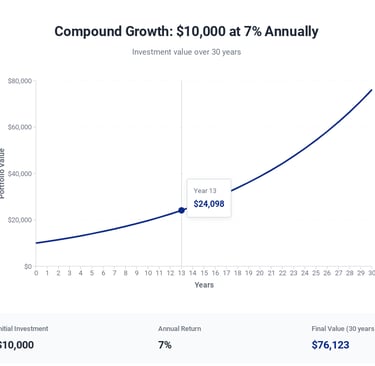

Compound Interest

Compound interest is the process where investment growth earns additional growth over time. Returns are generated not only on your original contributions but also on previously earned returns.

Example: Investing $100 at a 7% annual return grows to $107 after one year and $114.49 after two years because prior gains also earn returns.

Capital Gain

A capital gain occurs when you sell an investment for more than its purchase price. In Canada, capital gains earned outside registered accounts are taxable.

Realized vs. Unrealized Capital Gains

Unrealized gains exist on investments you still own, while realized gains occur only after you sell. Only realized capital gains are taxable in Canada.

Capital Loss

A capital loss happens when you sell an investment for less than you paid. Realized capital losses can be used to offset realized capital gains for tax purposes.

Cash Equivalent

Cash equivalents are low-risk investments that can quickly be converted into cash with minimal loss in value.

Examples: High-interest savings accounts, money market funds, cash ETFs, and short-term GICs.

Diversification

Diversification means spreading investments across different assets, industries, and regions to reduce overall portfolio risk.

Dividend

A dividend is a portion of company profits paid to shareholders. Dividends provide income without requiring the sale of the investment. Not all companies pay dividends.

Exchange Traded Fund (ETF)

An ETF is a pooled investment that trades like a stock and provides instant diversification across many securities.

Index ETF

An index ETF tracks a market index, such as the S&P/TSX Composite or S&P 500, by holding all (or most) of the securities in that index.

Liquidity

Liquidity describes how easily an investment can be converted into cash without significant loss in value.

Ex. A money market fund is very liquid as it can be sold today. On the other hand, a house is very illiquid as you will have to hire a real estate agent, find a buyer, and complete the sale before you receive your investment back.

Mutual Fund

A mutual fund pools money from investors and is actively or passively managed to achieve specific investment objectives.

Portfolio

A portfolio is the collection of all your investments across accounts and asset types.

Return on Investment (ROI)

ROI measures the percentage gain or loss on an investment relative to its initial cost.

Ex. If you buy a stock for $20, and it goes to $30 then you had a ROI of 50%.

Volatility

Volatility refers to how much an investment’s price fluctuates over time. Higher volatility means larger price swings.

Discount Broker

A discount broker is a low-cost platform that allows investors to buy and sell investments with minimal fees.

Example: Wealthsimple Trade or Questrade

Stock

A stock represents partial ownership in a company and entitles shareholders to a claim on earnings and assets.

Management Expense Ratio (MER)

MER is the annual fee charged by funds to cover operating and management costs.

Dollar Cost Averaging (DCA)

DCA involves investing a fixed amount regularly, reducing the risk of investing a lump sum at an unfavourable time.

Withholding Tax

Withholding tax is a tax deducted by foreign governments on dividends paid to Canadian investors, depending on the account type.

Guaranteed Investment Certificate (GIC)

A GIC is a low-risk investment that pays a fixed return over a set period, with limited or no access to funds before maturity.

Registered Accounts

Tax-Free Savings Account (TFSA)

A TFSA allows investments to grow and be withdrawn tax-free for life, making it one of the most flexible accounts available to Canadians. Contributions are not tax-deductible, but withdrawals are tax-free and can be used at any time for any purpose.

Registered Retirement Savings Plan (RRSP)

An RRSP is a retirement savings account that lets you reduce your taxable income today by contributing now, with the trade-off that withdrawals are taxed later. This works best when you expect to be in a lower tax bracket in retirement than you are today.

First Home Savings Account (FHSA)

The FHSA is a registered account designed for first-time home buyers that combines the tax deduction of an RRSP with the tax-free withdrawals of a TFSA (only if used for first home purchase). It allows you to save for a first home more efficiently than using either account on its own.

Registered Education Savings Plan (RESP)

An RESP is an education savings account that allows parents to invest money for a child’s post-secondary education while receiving government grants. The key benefit is that the government helps boost your savings, not just your own contributions.

Registered Disability Savings Plan (RDSP)

An RDSP is a long-term savings account for Canadians with disabilities that includes generous government grants and bonds. It is designed to support long-term financial security rather than short-term spending.

Contribution Room

Contribution room is the maximum amount you are allowed to deposit into a registered account.

Carry Forward

Unused contribution room carries forward indefinitely until used.

Tax Deduction

A tax deduction reduces your taxable income, lowering the amount of tax owed.

Tax-Free Growth

Growth inside certain accounts, such as a TFSA, is never taxed.

Home Buyers’ Plan (HBP)

The HBP allows first-time buyers to withdraw funds from their RRSP to purchase a home, provided the amount is repaid over time.

Lifelong Learning Plan (LLP)

The LLP allows RRSP withdrawals for education or training, with required repayments.

Budgeting Terms

Net Income

Net income is the amount you take home after taxes and payroll deductions. For the individual it's the number that your actually receive from your employer after removing CPP, EI, pension payments and taxes.

Gross Income

Gross income is your total earnings before any deductions. For the individual it's the number that appears at the top of your paycheck before deducting CPP, EI, pension payments, and taxes.

Fixed Expenses

Fixed expenses are those that remain relatively constant each month, such as rent or insurance.

Variable Expenses

Variable expenses fluctuate month to month, including groceries and entertainment.

Emergency Fund

An emergency fund is money set aside for unexpected events such as car repairs, medical costs, or job loss. It exists to prevent these situations from forcing you into high-interest debt.

Savings Rate

Your savings rate is the percentage of your income that you consistently save instead of spend. Over time, a higher savings rate matters more than earning a slightly higher return, provided the additional amount is invested.

Cash Flow

Cash flow refers to the movement of money into and out of your accounts.

Pay Yourself First

Paying yourself first means saving money immediately when you get paid, before covering discretionary expenses. This approach makes saving automatic instead of relying on willpower. Most banks offer automatic deposits now to save you the time of actually completing the action on your own.

Sinking Fund

A sinking fund is money you set aside gradually for a known future expense, such as a vacation or annual insurance bill. It helps avoid financial stress by spreading costs over time. It's purpose is to deal with expected future expenses, unlike the emergency fund which is meant for unexpected future expenses.

Debt and Credit Terms

Credit Score

A credit score is a number lenders use to judge how reliably you’ve handled debt in the past. A higher score generally leads to lower interest rates and better borrowing terms.

Credit Utilization

Credit utilization is how much of your available credit you are using at any given time. Even if you pay your bills on time, consistently using a high percentage of your limit can negatively affect your credit score.

Interest Rate

The interest rate represents the cost of borrowing money.

APR

APR reflects the total annual cost of credit, including fees.

Principal

Principal is the original amount borrowed or invested.

Minimum Payment

The minimum payment is the smallest amount required to keep a credit account in good standing. Paying only the minimum slows debt repayment and significantly increases total interest costs.

Debt Consolidation

Debt consolidation combines multiple debts into a single loan.

Home Equity Line of Credit (HELOC)

A HELOC is a line of credit secured by your home’s equity.

Good Debt vs. Bad Debt

Good debt is generally used to build long-term value or increase earning potential, while bad debt typically funds short-term consumption. The difference often comes down to whether the debt improves your future financial position.

Ex. Borrowing $20,000 for an RRSP loan to invest in the S&P500 vs Borrowing $20,000 to upgrade your car even though your current one works fine.

Tax Terms

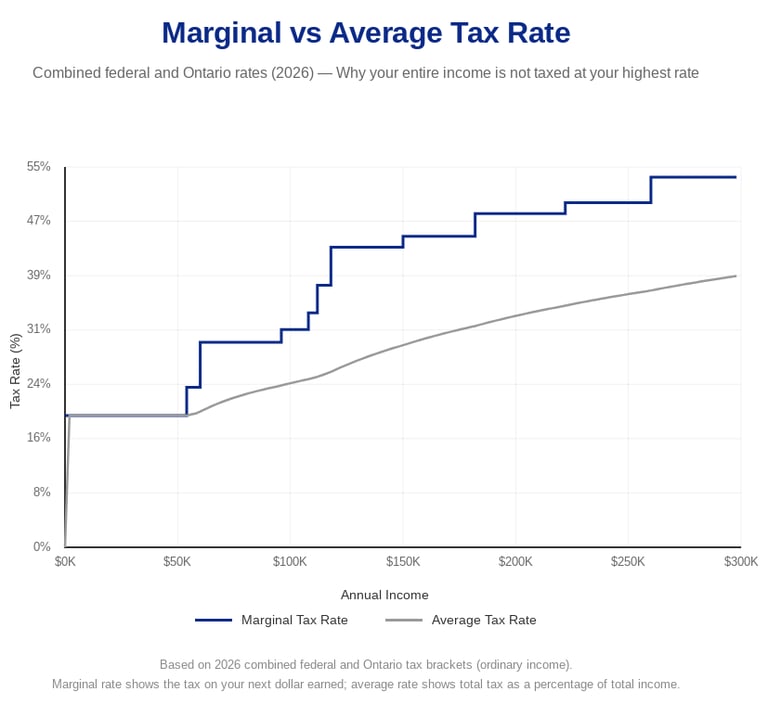

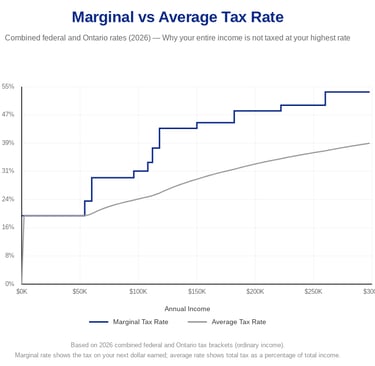

Marginal Tax Rate

Your marginal tax rate is the tax applied to your next dollar of income, not your entire income. This is why earning more money does not suddenly mean all of your income is taxed at a higher rate.

Average Tax Rate

Your average tax rate represents the overall percentage of your income paid in tax. It is usually much lower than your marginal tax rate.

Tax Brackets

Tax brackets are income ranges that determine what rate you will be taxed at. Canada uses a progressive tax system where higher income is taxed at higher rates.

Taxable Income

Taxable income is income remaining after deductions.

Non-Refundable Tax Credit

These credits reduce tax owed but do not create refunds.

Capital Gains Tax

In Canada, only 50% of a capital gain earned outside registered accounts is taxable. This means half of your profit is added to your taxable income, not the full amount.

Ex. You buy $100,000 of Apple stock and it increases to $200,000. The resulting capital gain is the difference between the two amounts at $100,000. You will only be taxed on 50% of the capital gain which is $50,000. This amount will be added to your taxable income.

CRA MyAccount

The CRA MyAccount portal allows Canadians to manage tax information online.

Notice of Assessment

A Notice of Assessment summarizes your tax return and confirms account balances.

Housing Terms

Amortization

Amortization is the total length of time it takes to fully repay a mortgage. Longer amortizations reduce monthly payments but increase the total interest paid over the life of the loan.

Mortgage Term

The mortgage term is the length of time your mortgage contract conditions apply. In Canada, the typical mortgage is 5 years but could be anywhere from 1-10 years.

Fixed Mortgage

A fixed mortgage has a constant interest rate for the duration of the term.

Variable Mortgage

A variable mortgage has an interest rate that changes with the prime rate set by the bank. The prime rate is influenced by the overnight rate set by the Bank of Canada, and a variety of other economic factors.

High-Ratio Mortgage

A mortgage with less than 20% down payment. Due to high house prices in Canada, most lenders, especially first time home buyers would fall into this category.

CMHC Insurance

Mortgage default insurance required for high-ratio mortgages. This protects the lender (bank) from your defaulting on your mortgage loan. However, it also allows people to get access to a mortgage with a relatively low down payment. It will significantly increase the cost of home ownership though.

Ex. An $800,000 home purchased in Ottawa, Ontario at a minimum down-payment of $55,000 (or 6.88%) would require CMHC payments adding up to a total of $29,800.

Loan-to-Value (LTV)

Loan-to-value compares the size of your mortgage to the value of your home. A higher LTV generally means higher borrowing risk and may require mortgage insurance.

Equity

Equity is the difference between a home’s value and the mortgage balance (amount owing).

Closing Costs

Closing costs are fees paid when completing a real estate transaction.

Retirement Terms

Canada Pension Plan (CPP)

CPP is a government pension that provides retirement income based on how much you contributed during your working years. It is meant to supplement your own savings, not replace them.

Old Age Security (OAS)

OAS is a government benefit available to most Canadians aged 65 and older, regardless of work history. High-income retirees may see part of this benefit clawed back. The amount you receive is calculated based on the numbers of years you have been a Canadian citizen.

Guaranteed Income Supplement (GIS)

GIS supports low-income seniors receiving OAS.

Registered Retirement Income Fund (RRIF)

A RRIF provides structured withdrawals from an RRSP in retirement.

Defined Benefit Pension

Pays a guaranteed income based on salary and years of service. The best example would be the pensions offered to civil servants in the federal government, or law enforcement agencies.

Defined Contribution Pension

Retirement income depends on contributions and investment performance. A common variation of this is an RRSP matching program offered by employers.

Annuity

An annuity provides guaranteed income for life or a set period.

Longevity Risk

The risk of outliving your retirement savings.

Four Percent Rule

The four percent rule is a guideline suggesting that retirees may be able to withdraw 4% of their portfolio annually without running out of money. Most calculations are based on a portfolio that is high in equities, atleast a typical 80/20 portfolio. It is a rule of thumb, not a guarantee.

Mindset Terms

Financial Literacy

The ability to understand and apply money concepts effectively.

Lifestyle Creep

Lifestyle creep happens when spending rises alongside income, leaving little progress toward savings or investing goals. Many people earn more over time but feel no wealthier because their expenses grow just as quickly.

FOMO

Fear of missing out can drive emotional financial decisions such as buying a stock when it is already overbought.

Emotional Spending

Emotional spending occurs when purchases are driven by stress, excitement, or boredom rather than necessity. This often leads to regret and slows long-term financial progress.

Sunk Cost Fallacy

The sunk cost fallacy is the tendency to continue a decision because of money or time already invested, even when changing course would be the better option. In investing, this often shows up as holding losing investments for the wrong reasons.

Anchoring Bias

Anchoring bias occurs when you rely too heavily on the first number or idea you encounter, even if it’s no longer relevant. In personal finance, this often shows up when someone refuses to sell an investment because they are anchored to the price they originally paid.

Money Scripts

Money scripts are the beliefs you formed about money growing up, often without realizing it. These beliefs quietly influence how you save, spend, invest, and take financial risks.

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Canada Revenue Agency. (n.d.). Registered plans and savings. Government of Canada.

Government of Canada. (n.d.). Personal finance basics

Bank of Canada. (n.d.). Inflation and interest rates.