Get our free Debt vs Invest Calculator — click here to access it

Why the TFSA Is the Best Registered Account in Canada (2025)

Learn how the TFSA helps you grow wealth tax-free, maximize savings, and make flexible withdrawals—making it one of the best investment accounts in Canada.

TFSATAX FREE SAVINGS ACCOUNT

3/15/202510 min read

Introduction

In the Olympics, there is an event called the decathlon, which is a combined ten-discipline event which includes the 100-meter, 400-meter, 1500-meter runs, the 110-meter high hurdles, the javelin and discus throws, shot put, pole vault, high jump, and long jump. The winner of this event is called the “World’s Greatest Athlete” and wins a gold medal.

Unfortunately, there is no Olympic tournament for the “World's Greatest Registered Account”, but if there were, the tax free savings account (TFSA) would hands down win the gold medal against the other accounts. We will be discussing some of the TFSA basics for you to make sure you understand what this account is and why we love it so much.

Account Types vs Asset Classes

In previous blogs we discussed various types of investment products including stocks, bonds, GIC’s, and REITS. Once you have learned enough about each of the above asset classes, the next inevitable question you’re going to ask yourself is, where should I invest in these asset classes?

There are several different account types in Canada including a TFSA, RRSP, RESP, FHSA, non-registered account and so on.

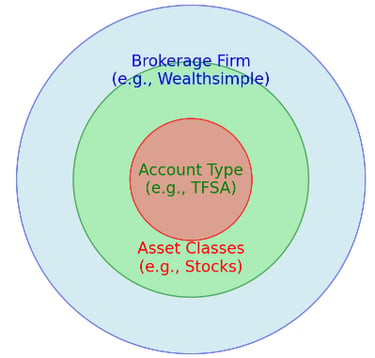

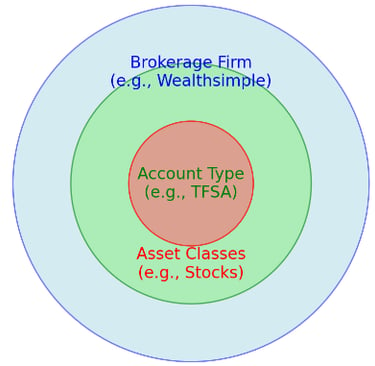

The best way to understand the relationship between asset classes, and account is through a three circle diagram. The largest circle is your brokerage (ie. Wealthsimple, Questrade, etc). You need to select a brokerage before opening up an account of any form. The next circle is the specific type of account you choose to open at your brokerage (ie. TFSA, RRSP, etc). Lastly, the smallest circle is the asset classes you decide to invest in within that specific account (ie. Stocks, Bonds, REITS, etc).

A common mistake people make is that they think a TFSA is an investment. A TFSA is not an investment itself but rather a container for investments. Whether you hold stocks, bonds, REITs, or cash in it, the tax benefits remain the same. However, due to this misconception Canadians often deposit their hard earned money into a TFSA with their brokerage firm of choice. However, they fail to take the second step of investing the funds into assets that can grow their wealth and take full advantage of the benefits provided by a TFSA.

Overview of a TFSA

The TFSA is a registered account that you can open at any Canadian financial institution. It is a Canadian specific account that started in 2009. Anyone who is 18 years of age or older, a Canadian citizen, and has a social insurance number (SIN) can open a TFSA.

Any contributions you make to a TFSA are not deductible for income tax purposes. That means that you have to pay taxes on any income first, and then put it into the account later.

For example: If you live in Ontario and make $60,000 a year in gross income. Your net income after taxes, and EI premiums would be $46,559. Unfortunately, regardless of how much you contribute to your TFSA you will not receive a tax deduction. You will pay $13,441 in taxes before deductions.

The Magic of the TFSA Account

Although you’re using after-tax money, The magic of the TFSA is that any income earned in or withdrawn from the account is tax- free. Possible income sources could be:

Interest from high interest savings account, bonds, or GIC’s

Distributions from REITs

Dividends from stocks

Or capital gains from the sale of stocks

For example: Imagine I deposit $1,000 into a TFSA with my local financial institution. I then invest that money in a 1-year GIC that is paying 5% interest per year. Next year at this time, I should have $1,050 in my account. In other words, I earned a $50 profit. This $50 of profit will not be taxed, and I do not have to claim it on my tax return.

What makes the TFSA even more powerful is that the earning's can compound over time, increasing your wealth without ever being taxed.

On the contrary, let’s imagine I used the same strategy as the example above. However, instead I invested the money within a non-registered (also known as a taxable account) high interest saving’s account. In this case I would have to claim the $50 of earned interest as income on my tax return using a T5 provided by my institution.

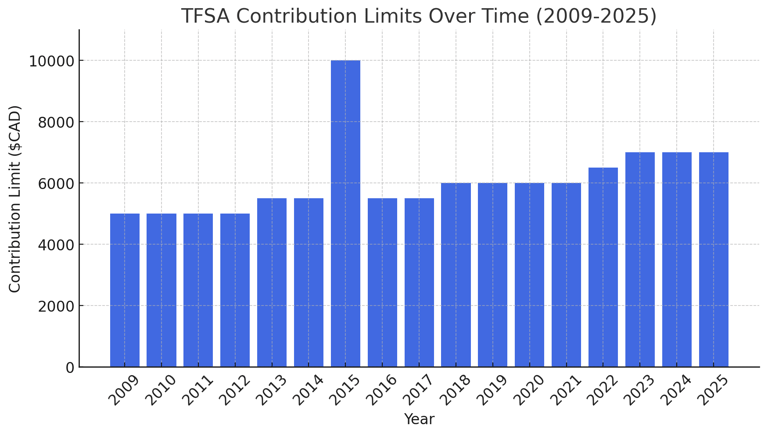

How much can I deposit into a TFSA?

Each person has what is referred to as a contribution limit that starts to accumulate from the age of 18. Provided that you turned 18 in 2009, or afterwards and are a Canadian citizen.

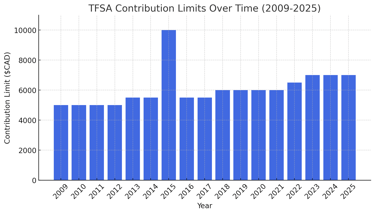

The annual limit is decided each year by the government. The decision is influenced by a variety of factors but is mostly tied to inflation. The annual limit has ranged anywhere between $5,000 to upwards of $10,000 from its inception. The annual limit for 2025 is $7,000.

The annual limits are cumulative. This means that even if you have never contributed to a TFSA you continue to accumulate more room each year.

For example: If you were 18 years of age or older in 2009, you would have accumulated a total of $102,000 of contribution room in 2025.

In order to calculate how much you can contribute there are several TFSA Contribution Limit calculators online. However, we created one you can use here. Using these calculators will require you to input the year you were born, how much you previously contributed, and if you have previously withdrawn money from a TFSA. It will then provide you with your total contribution limit.

It is important to input the data accurately, and monitor your contribution limit as there are consequences for over contributing. The CRA charges a fee of 1% per month on excess contribution.

For example, if I over contribute $10,000 and don’t withdraw it for 6 months, I could be hit with a $600 fee.

Conclusion

As you can see the TFSA is a very effective tool to grow your wealth, hence why we love it so much. Understanding this account is critical on your path to long term wealth accumulation. This weeks instalment was meant as a brief overview. Next week we will dive into some common misconceptions of the TFSA, before we move on to our second favourite account type.

Related Posts:

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

World Athletics. (n.d.). Decathlon. World Athletics. Retrieved February 5, 2025, from https://worldathletics.org/disciplines/combined-events/decathlon#:~:text=The%20decathlon%20is%20a%20combined,range%20of%20skills%20and%20techniques.

Government of Canada. Tax-Free Savings Account (TFSA), guide for individuals. Government of Canada. Retrieved February 5, 2025, from https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4466/tax-free-savings-account-tfsa-guide-individuals.html

OpenAI. (2025). Three Circle Chart describing the relationship between brokerage firms, account types, and asset classes [AI-generated graph]. ChatGPT. https://chat.openai.com/

OpenAI. (2025). Bar Chart showing the annual TFSA Contribution Limits since inception in 2009 [AI-generated graph]. ChatGPT. https://chat.openai.com/

Introduction

In the Olympics, there is an event called the decathlon, which is a combined ten-discipline event which includes the 100-meter, 400-meter, 1500-meter runs, the 110-meter high hurdles, the javelin and discus throws, shot put, pole vault, high jump, and long jump. The winner of this event is called the “World’s Greatest Athlete” and wins a gold medal.

Unfortunately, there is no Olympic tournament for the “World's Greatest Registered Account”, but if there were, the tax free savings account (TFSA) would hands down win the gold medal against the other accounts. We will be discussing some of the TFSA basics for you to make sure you understand what this account is and why we love it so much.

Account Types vs Asset Classes

In previous blogs we discussed various types of investment products including stocks, bonds, GIC’s, and REITS. Once you have learned enough about each of the above asset classes, the next inevitable question you’re going to ask yourself is, where should I invest in these asset classes?

There are several different account types in Canada including a TFSA, RRSP, RESP, FHSA, non-registered account and so on.

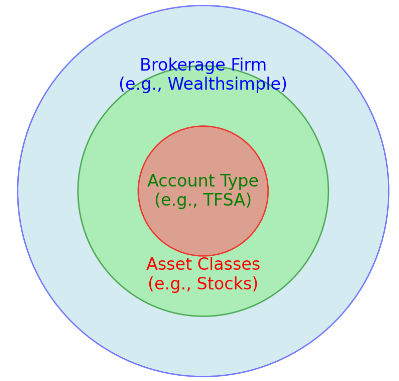

The best way to understand the relationship between asset classes, and account is through a three circle diagram. The largest circle is your brokerage (ie. Wealthsimple, Questrade, etc). You need to select a brokerage before opening up an account of any form. The next circle is the specific type of account you choose to open at your brokerage (ie. TFSA, RRSP, etc). Lastly, the smallest circle is the asset classes you decide to invest in within that specific account (ie. Stocks, Bonds, REITS, etc).

A common mistake people make is that they think a TFSA is an investment. A TFSA is not an investment itself but rather a container for investments. Whether you hold stocks, bonds, REITs, or cash in it, the tax benefits remain the same. However, due to this misconception Canadians often deposit their hard earned money into a TFSA with their brokerage firm of choice. However, they fail to take the second step of investing the funds into assets that can grow their wealth and take full advantage of the benefits provided by a TFSA.

Overview of a TFSA

The TFSA is a registered account that you can open at any Canadian financial institution. It is a Canadian specific account that started in 2009. Anyone who is 18 years of age or older, a Canadian citizen, and has a social insurance number (SIN) can open a TFSA.

Any contributions you make to a TFSA are not deductible for income tax purposes. That means that you have to pay taxes on any income first, and then put it into the account later.

For example: If you live in Ontario and make $60,000 a year in gross income. Your net income after taxes, and EI premiums would be $46,559. Unfortunately, regardless of how much you contribute to your TFSA you will not receive a tax deduction. You will pay $13,441 in taxes before deductions.

The Magic of the TFSA Account

Although you’re using after-tax money, The magic of the TFSA is that any income earned in or withdrawn from the account is tax- free. Possible income sources could be:

Interest from high interest savings account, bonds, or GIC’s

Distributions from REITs

Dividends from stocks

Or capital gains from the sale of stocks

For example: Imagine I deposit $1,000 into a TFSA with my local financial institution. I then invest that money in a 1-year GIC that is paying 5% interest per year. Next year at this time, I should have $1,050 in my account. In other words, I earned a $50 profit. This $50 of profit will not be taxed, and I do not have to claim it on my tax return.

What makes the TFSA even more powerful is that the earning's can compound over time, increasing your wealth without ever being taxed.

On the contrary, let’s imagine I used the same strategy as the example above. However, instead I invested the money within a non-registered (also known as a taxable account) high interest saving’s account. In this case I would have to claim the $50 of earned interest as income on my tax return using a T5 provided by my institution.

How much can I deposit into a TFSA?

Each person has what is referred to as a contribution limit that starts to accumulate from the age of 18. Provided that you turned 18 in 2009, or afterwards and are a Canadian citizen.

The annual limit is decided each year by the government. The decision is influenced by a variety of factors but is mostly tied to inflation. The annual limit has ranged anywhere between $5,000 to upwards of $10,000 from its inception. The annual limit for 2025 is $7,000.

The annual limits are cumulative. This means that even if you have never contributed to a TFSA you continue to accumulate more room each year.

For example: If you were 18 years of age or older in 2009, you would have accumulated a total of $102,000 of contribution room in 2025.

In order to calculate how much you can contribute there are several TFSA Contribution Limit calculators online. You can check out our favourite TFSA calculator here. Using these calculators will require you to input the year you were born, how much you previously contributed, and if you have previously withdrawn money from a TFSA. It will then provide you with your total contribution limit.

It is important to input the data accurately, and monitor your contribution limit as there are consequences for over contributing. The CRA charges a fee of 1% per month on excess contribution.

For example, if I over contribute $10,000 and don’t withdraw it for 6 months, I could be hit with a $600 fee.

Conclusion

As you can see the TFSA is a very effective tool to grow your wealth, hence why we love it so much. Understanding this account is critical on your path to long term wealth accumulation. This weeks installment was meant as a brief overview. Next week we will dive into some common misconceptions of the TFSA, before we move on to our second favourite account type.

Related Posts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

World Athletics. (n.d.). Decathlon. World Athletics. Retrieved February 5, 2025, from https://worldathletics.org/disciplines/combined-events/decathlon#:~:text=The%20decathlon%20is%20a%20combined,range%20of%20skills%20and%20techniques.

Government of Canada. Tax-Free Savings Account (TFSA), guide for individuals. Government of Canada. Retrieved February 5, 2025, from https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4466/tax-free-savings-account-tfsa-guide-individuals.html

OpenAI. (2025). Three Circle Chart describing the relationship between brokerage firms, account types, and asset classes [AI-generated graph]. ChatGPT. https://chat.openai.com/

OpenAI. (2025). Bar Chart showing the annual TFSA Contribution Limits since inception in 2009 [AI-generated graph]. ChatGPT. https://chat.openai.com/