Get our free Debt vs Invest Calculator — click here to access it

What Is a GIC and How Does It Work in Canada? (2025 Guide)

What is a GIC and how does it work in Canada? Learn about GIC types, interest rates, tax implications, and how they compare to bonds.

INVESTING FOR BEGINNERSGUARANTEED INTEREST CERTIFICATES

3/1/202514 min read

Introduction

As you continue learning the basics of personal finance, you will quickly find there are a plethora of different avenues you can use to invest your hard earned case. These include things such as stocks and bonds, which we have discussed in past posts here & here. There are a variety of other options to choose from including things such as real estate, REITS, private equity, private credit, and much more. But what if you have a reasonable amount of cash that you don’t want to invest in risky assets? One good options for Canadian’s is the topic of today’s article, and it is GIC’s.

What are GICs?

A GIC stands for a Guaranteed Interest Certificate. A GIC is a loan contract similar to a bond. In a GIC you are lending your money to a bank, over a defined time period, for an agreed upon interest return.

Like bonds, there are two key features to a GIC which are the term length, and the yield.

Term Length & Yield

The term length is the duration of the holding period. It generally can range anywhere between 3 months and 10 years.

The yield is the rate of interest return that you will receive in exchange for lending your money to the bank. It is generally quoted yearly, and expressed as an annual percentage (ie. 1%, 3%, 7%). Depending on the type of GIC the interest can be paid out monthly, quarterly, annually, or at the end of the term.

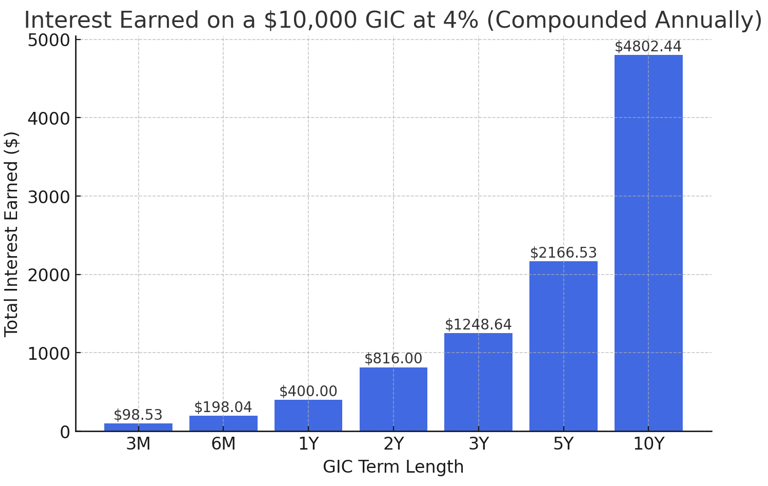

For Example: If I go to my bank and purchase a 1-year GIC for $10,000 that yields a 4% return. I agree to loan $10,000 to the bank for the next year in exchange for a 4% interest payment (ie. $400). After the 1-year I will receive $10,400, which includes my principle investment of $10,000 combined with the interest payment of $400.

Understanding Annualized & Compounded Rates

The important thing I want to touch on here is that interest rates are quoted yearly. So even if you see your bank is offering a 3- month GIC at 4%, this does not mean you will receive 4% on your money. Because 3 months is only ~¼ of a year you would actually only receive the total 4% if you renewed the same terms 4 times throughout the year.

For Example: If I purchased a 3- Month GIC for $10,000 that yields a 4% annualized return. I will only receive ~$100 in interest at the end of the term.

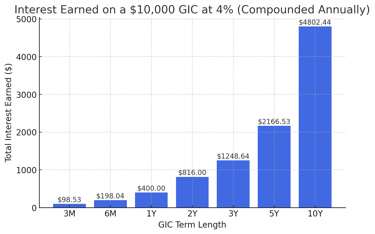

The same confusion could happen with longer terms as well because the rate of return is quoted annually, and the interest earned compounds.

Example: If I buy a 2-year GIC for $10,000 at 4%, I will actually receive $816 in interest at the end of the two year term. If you go back to our previous example we said that a 1- year term at the same rate would provide you with $10,400. Since the interest compounds, then the interest earned in year 2 has to be calculated based on the balance at the end of year 1.

Year 1: $10,000 (Principle) x 1.04% (4% interest) = $10,400

Year 2: $10,400 (Principe) x 1.04% (4% interest) = $10,816

Why does the bank offer GICs? Interest spreads

You’ve probably heard the term “everything that glitters is not gold”, so the key question is, why do banks offer this to their customers? and what do they get in return?

The bank earns the majority of its profits from lending other people's money for a gain. With GICs, the bank has found a way to attract and lock in your deposits for a specified time period (ie. 3 months, 6 months, 1 year). They will then use that money to lend to others at a higher rate than that annual interest that is owed to you. They will lend the money to others for things such as mortgages, auto loans, lines of credit, etc.

Interest Spread = The difference between the interest rate of lending products vs borrowing products.

For example, let's continue with the previous example from above where you gave the bank $10,000 for a 1-Year GIC with a 4% yield. You receive $400 in interest at the end of the term. The bank decides to take your $10,000, and loan it to someone for the same year for 6%. In this scenario, the banks benefit from this transaction because they borrowed your money, invested it to make $600 and only gave you $400. They capture $200 profit after these transactions are complete. The interest rate spread between what the interest the bank charges someone for your money (6%) vs what they give you (4%), is where banks benefit.

GIC vs Bonds

As we noted above GICs and bonds are very similar in that they are a loan contract whereby you are the lender. Bonds can be between you and multiple different types of agencies including the Government and Corporations. Meanwhile, GICs are generally just offered by banks.

However, another key difference between GICs and bonds is the degree of liquidity. Liquidity is just a fancy word for how quickly something can be converted into cash.

For example: A house would be very illiquid because you would have to list it on the real estate market, and then sell it (likely over the course of a few months) before you can get access to the cash. Money in a checking account on the other hand would be very liquid because you can go to my ATM and convert it to cash right now.

Bonds are more liquid than standard GICs because with GICs you have to lock your money in for an agreed upon term. That is you can’t get access to your principal (ie. the money you initially deposited) until the end of the term. A bond on the other hand can be sold on the secondary market throughout the term. So you don’t have to hold a bond to maturity (ie. end of term)

Why does this matter?

This is important because interest rates change. If you lock your money in at a lower interest rate and the rates go up you don’t have the ability to capitalize on the new rates.

For example: In January 2019 the 5-Year GIC rate at EQ Bank was 3.5%. If you purchased this GIC, you would have agreed to lend them your money until January 2024. This was a very good decision until May 2022 when interest rates were gradually increased and the 1 Year GIC rate started to rise above 3.5%. Worse yet, throughout 2023 the 1 year GIC remained at 5% or higher. In other words if you decided to buy the 5 year GIC at 3.5% in 2019, you would still be earning 3.5% on my money, while people who held shorter term GICs would now be getting a 5% return.

Now imagine you instead purchased a 5- Year Treasury Bond. You could potentially have sold your 5-Year bond, and regained the principle. This would have allowed you to purchase a shorter term bond like a 1-Year to take advantage of rising interest rates.

Redeemable GICs and GIC Laddering

There are two ways that GIC holders can reduce this liquidity risk as discussed above:

Redeemable GICs

Sometimes banks offer Redeemable GICs whereby you can cash them before the end of the agreed upon term. The major downside with these is they offer a lower interest return than standard GICs.

For example: Scotiabank currently offers a 2 year redeemable GIC at 2.75%. Meanwhile, the standard non-redeemable 2 year GIC is at 3.45%. So you are losing 0.7% just to keep easy access to your money.

GIC Laddering

This is a strategy people can use to increase the liquidity of their total invested capital in GICs. What it involves is purchasing multiple GICs with varying term lengths. The idea is that at a fairly regular interval some of your invested cash will be available to be reinvested into new GICs. This will allow you to capitalize on changing interest rates.

For example: Imagine I have $10,000 to invest in GICs. I could divide that money into equal portions (3 months- $1500, 6 months- $1500, 9 months - $1500, 1 year- $1500, 2- year $1500, etc). That way every few months I have another $1500 plus an interest earned available to reinvest into a new GIC.

Tax Implications

Like stocks, bonds, exchange traded funds (ETF’s), real estate investment trusts (REITS), etc the tax implications of GICs highly depends on the account the asset is held in. Like many other asset classes you can purchase your GICs via tax sheltered or deferred accounts such as the TFSA, FHSA, RRSP, RESP and so on. In which case there are no direct tax implications for the interest earned on these accounts.

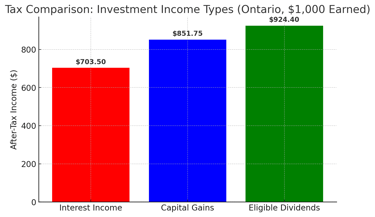

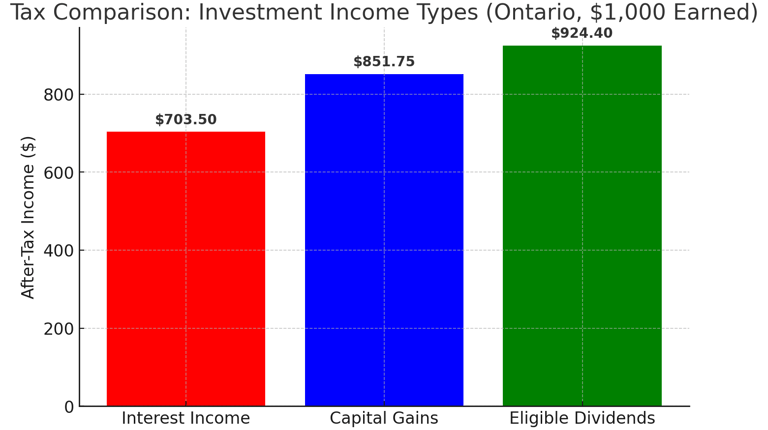

However, if you purchase GICs within a taxable account, you will be taxed on any interest earned. In Canada interest income is the least tax-efficient investment income. This is because it is taxed at your marginal tax rate (ie. highest tax rate), which is based on your income.

Example: Imagine you make $60,000/year in 2025 and live in Ontario, your combined marginal tax rate is 29.65% (20.5%- Federal, 9.15%-Ontario). This means that for every additional $100 you make, $29.65 cents will go to the government. If you make an additional $1,000 of interest income via GICs, you will have to pay an additional $296.50, so a little under ⅓ of your profits go to taxes.

This is why it is generally advised that any assets you own earning interest income remain within your tax advantaged accounts.

Related Posts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Scotiabank. (n.d.). GIC rates. Scotiabank. Retrieved February 7, 2025, from https://www.scotiabank.com/ca/en/personal/rates-prices/gic-rates.html

Royal Bank of Canada. (n.d.). Understanding taxes and your investments. RBC Global Asset Management. Retrieved February 7, 2025, from https://www.rbcgam.com/en/ca/learn-plan/investment-basics/understanding-taxes-and-your-investments/detail

HighInterestSavings.ca. (n.d.). EQ Bank GIC rate history. Retrieved February 7, 2025, from https://www.highinterestsavings.ca/profile/eq-bank/gic-rate-history/

Bates, L. (2018). Beat the bank: The Canadian guide to simply successful investing. Dundurn.

Beyond MD. (2023, April 20). GICs 101 with Mahima Poddar from EQ Bank [Podcast]. Beyond MD Podcast.

OpenAI. (2025). Graph comparing bond term lengths [AI-generated graph]. ChatGPT. https://chat.openai.com/

OpenAI. (2025). Graph comparing bond yeild vs credit rating [AI-generated graph]. ChatGPT. https://chat.openai.com/

Introduction

As you continue learning the basics of personal finance, you will quickly find there are a plethora of different avenues you can use to invest your hard earned case. These include things such as stocks and bonds, which we have discussed in past posts here & here. There are a variety of other options to choose from including things such as real estate, REITS, private equity, private credit, and much more. But what if you have a reasonable amount of cash that you don’t want to invest in risky assets? One good options for Canadian’s is the topic of today’s article, and it is GIC’s.

What are GICs?

A GIC stands for a Guaranteed Interest Certificate. A GIC is a loan contract similar to a bond. In a GIC you are lending your money to a bank, over a defined time period, for an agreed upon interest return.

Like bonds, there are two key features to a GIC which are the term length, and the yield.

Term Length & Yield

The term length is the duration of the holding period. It generally can range anywhere between 3 months and 10 years.

The yield is the rate of interest return that you will receive in exchange for lending your money to the bank. It is generally quoted yearly, and expressed as an annual percentage (ie. 1%, 3%, 7%). Depending on the type of GIC the interest can be paid out monthly, quarterly, annually, or at the end of the term.

For Example: If I go to my bank and purchase a 1-year GIC for $10,000 that yields a 4% return. I agree to loan $10,000 to the bank for the next year in exchange for a 4% interest payment (ie. $400). After the 1-year I will receive $10,400, which includes my principle investment of $10,000 combined with the interest payment of $400.

Understanding Annualized & Compounded Rates

The important thing I want to touch on here is that interest rates are quoted yearly. So even if you see your bank is offering a 3- month GIC at 4%, this does not mean you will receive 4% on your money. Because 3 months is only ~¼ of a year you would actually only receive the total 4% if you renewed the same terms 4 times throughout the year.

For Example: If I purchased a 3- Month GIC for $10,000 that yields a 4% annualized return. I will only receive ~$100 in interest at the end of the term.

The same confusion could happen with longer terms as well because the rate of return is quoted annually, and the interest earned compounds.

Example: If I buy a 2-year GIC for $10,000 at 4%, I will actually receive $816 in interest at the end of the two year term. If you go back to our previous example we said that a 1- year term at the same rate would provide you with $10,400. Since the interest compounds, then the interest earned in year 2 has to be calculated based on the balance at the end of year 1.

Year 1: $10,000 (Principle) x 1.04% (4% interest) = $10,400

Year 2: $10,400 (Principe) x 1.04% (4% interest) = $10,816

Why does the bank offer GICs? Interest spreads

You’ve probably heard the term “everything that glitters is not gold”, so the key question is, why do banks offer this to their customers? and what do they get in return?

The bank earns the majority of its profits from lending other people's money for a gain. With GICs, the bank has found a way to attract and lock in your deposits for a specified time period (ie. 3 months, 6 months, 1 year). They will then use that money to lend to others at a higher rate than that annual interest that is owed to you. They will lend the money to others for things such as mortgages, auto loans, lines of credit, etc.

Interest Spread = The difference between the interest rate of lending products vs borrowing products.

For example, let's continue with the previous example from above where you gave the bank $10,000 for a 1-Year GIC with a 4% yield. You receive $400 in interest at the end of the term. The bank decides to take your $10,000, and loan it to someone for the same year for 6%. In this scenario, the banks benefit from this transaction because they borrowed your money, invested it to make $600 and only gave you $400. They capture $200 profit after these transactions are complete. The interest rate spread between what the interest the bank charges someone for your money (6%) vs what they give you (4%), is where banks benefit.

GIC vs Bonds

As we noted above GICs and bonds are very similar in that they are a loan contract whereby you are the lender. Bonds can be between you and multiple different types of agencies including the Government and Corporations. Meanwhile, GICs are generally just offered by banks.

However, another key difference between GICs and bonds is the degree of liquidity. Liquidity is just a fancy word for how quickly something can be converted into cash.

For example: A house would be very illiquid because you would have to list it on the real estate market, and then sell it (likely over the course of a few months) before you can get access to the cash. Money in a checking account on the other hand would be very liquid because you can go to my ATM and convert it to cash right now.

Bonds are more liquid than standard GICs because with GICs you have to lock your money in for an agreed upon term. That is you can’t get access to your principal (ie. the money you initially deposited) until the end of the term. A bond on the other hand can be sold on the secondary market throughout the term. So you don’t have to hold a bond to maturity (ie. end of term)

Why does this matter?

This is important because interest rates change. If you lock your money in at a lower interest rate and the rates go up you don’t have the ability to capitalize on the new rates.

For example: In January 2019 the 5-Year GIC rate at EQ Bank was 3.5%. If you purchased this GIC, you would have agreed to lend them your money until January 2024. This was a very good decision until May 2022 when interest rates were gradually increased and the 1 Year GIC rate started to rise above 3.5%. Worse yet, throughout 2023 the 1 year GIC remained at 5% or higher. In other words if you decided to buy the 5 year GIC at 3.5% in 2019, you would still be earning 3.5% on my money, while people who held shorter term GICs would now be getting a 5% return.

Now imagine you instead purchased a 5- Year Treasury Bond. You could potentially have sold your 5-Year bond, and regained the principle. This would have allowed you to purchase a shorter term bond like a 1-Year to take advantage of rising interest rates.

Redeemable GICs and GIC Laddering

There are two ways that GIC holders can reduce this liquidity risk as discussed above:

Redeemable GICs

Sometimes banks offer Redeemable GICs whereby you can cash them before the end of the agreed upon term. The major downside with these is they offer a lower interest return than standard GICs.

For example: Scotiabank currently offers a 2 year redeemable GIC at 2.75%. Meanwhile, the standard non-redeemable 2 year GIC is at 3.45%. So you are losing 0.7% just to keep easy access to your money.

GIC Laddering

This is a strategy people can use to increase the liquidity of their total invested capital in GICs. What it involves is purchasing multiple GICs with varying term lengths. The idea is that at a fairly regular interval some of your invested cash will be available to be reinvested into new GICs. This will allow you to capitalize on changing interest rates.

For example: Imagine I have $10,000 to invest in GICs. I could divide that money into equal portions (3 months- $1500, 6 months- $1500, 9 months - $1500, 1 year- $1500, 2- year $1500, etc). That way every few months I have another $1500 plus an interest earned available to reinvest into a new GIC.

Tax Implications

Like stocks, bonds, exchange traded funds (ETF’s), real estate investment trusts (REITS), etc the tax implications of GICs highly depends on the account the asset is held in. Like many other asset classes you can purchase your GICs via tax sheltered or deferred accounts such as the TFSA, FHSA, RRSP, RESP and so on. In which case there are no direct tax implications for the interest earned on these accounts.

However, if you purchase GICs within a taxable account, you will be taxed on any interest earned. In Canada interest income is the least tax-efficient investment income. This is because it is taxed at your marginal tax rate (ie. highest tax rate), which is based on your income.

Example: Imagine you make $60,000/year in 2025 and live in Ontario, your combined marginal tax rate is 29.65% (20.5%- Federal, 9.15%-Ontario). This means that for every additional $100 you make, $29.65 cents will go to the government. If you make an additional $1,000 of interest income via GICs, you will have to pay an additional $296.50, so a little under ⅓ of your profits go to taxes.

This is why it is generally advised that any assets you own earning interest income remain within your tax advantaged accounts.

Related Posts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Scotiabank. (n.d.). GIC rates. Scotiabank. Retrieved February 7, 2025, from https://www.scotiabank.com/ca/en/personal/rates-prices/gic-rates.html

Royal Bank of Canada. (n.d.). Understanding taxes and your investments. RBC Global Asset Management. Retrieved February 7, 2025, from https://www.rbcgam.com/en/ca/learn-plan/investment-basics/understanding-taxes-and-your-investments/detail

HighInterestSavings.ca. (n.d.). EQ Bank GIC rate history. Retrieved February 7, 2025, from https://www.highinterestsavings.ca/profile/eq-bank/gic-rate-history/

Bates, L. (2018). Beat the bank: The Canadian guide to simply successful investing. Dundurn.

Beyond MD. (2023, April 20). GICs 101 with Mahima Poddar from EQ Bank [Podcast]. Beyond MD Podcast.

OpenAI. (2025). Graph comparing bond term lengths [AI-generated graph]. ChatGPT. https://chat.openai.com/

OpenAI. (2025). Graph comparing bond yeild vs credit rating [AI-generated graph]. ChatGPT. https://chat.openai.com/