Get our free Debt vs Invest Calculator — click here to access it

RESP Basics: A Complete Guide for Parents

A complete guide to RESPs for Canadian parents. Learn how to open, contribute, invest, and optimize RESP accounts to fund your child's education.

RESPREGISTERED EDUCATION SAVING'S PLAN

8/11/202529 min read

What is the RESP?

In previous blogs we discussed a variety of registered account types including the TFSA, RRSP, & FHSA. Each of which was created for a unique purpose.

The account we are going to discuss today is perfect for parents, or grandparents. This account is referred to as the RESP which stands for the Registered Education Savings Plan. The RESP is a tax deferred account that was set up by the government in 1974 in order to help parents save for their child’s post-secondary education.

This account acts like a piggy bank for your child's education. However, what makes this account unique is that the government assists you in contributing to it over time.

Key Terms

The terminology used to describe this account can often provide confusion. In order to avoid this the following is a list of what those terms are, and what they refer to:

Subscriber (The person who opens the account)

Beneficiary (The Child)

Promoter (The Financial Institution)

EAP (Education Assistance Payment)

Opening an RESP

You can open, and start contributing to an RESP as soon as your child is born. This can be done through most financial institutions.

All you will need to set-up the account is:

Legal name of the beneficiary

Social insurance number of the beneficiary

And a date of birth of the beneficiary

The maximum contribution limit to the RESP is $50,000 per beneficiary.

Multiple accounts can be set-up for each beneficiary. So if the grandparents of the child also want to set up an RESP, they can too. However, is important that you monitor the total contribution amount if you do decide to set-up multiple accounts in order to avoid over-contributing. The fee for over-contribution is the same as other tax-advantaged accounts charged at 1% of the over-contributed balance per month.

All of the contributions must be made prior to the beneficiaries 31st Birthday.

Types of RESP's

The two types of RESP’s are:

Individual RESP

Family RESP

Regardless of which option that you choose the maximum contribution limit remains at $50,000 per beneficiary. For example: If you had 3 children you could contribute up to $150,000 to a family RESP (ie. $50,000 per beneficiary)

The primary benefit of a family RESP is that the funds can be split between children. This is helpful in cases whereby one child's education is more costly than others.

Now that you know the types of RESP accounts available, let’s dive into what makes them particularly powerful.

What Makes the RESP Unique?

The RESP is unique for two specific reasons:

The Grants/Bonds

& Tax Advantages

Grants and Bond

Canada Education Savings Grant (CESG)

The primary benefit of the RESP is the ability to receive the Canada Education Savings Grant (CESG). This is a government grant that will match 20% of your contribution room up to a yearly maximum of $500. In order to receive the maximum annual grant you will need to contribute $2,500/year.

The maximum amount of grant that a beneficiary can receive over the life of the account is $7,200. This would require you to contribute a total of $36,000 (ie. 14.5 years x $2,500).

You will receive no additional grant money by contributing more than $2,500 in a single year, or $36,000 over the life of the account. However, in the case that a year is missed you are able to engage in a one year catch-up by contributing an additional $2,500 in that year.

For Example: Imagine you start contributing to your Child's RESP in 2025, when they reached 3 years of age. In this case you would be able to contribute $5,000 in the first year of the account, and receive $1,000 worth of CESG.

$2,500 (Grant Eligible Contribution for 2025) + $2,500 (Catch-Up Grant Eligible Contribution from 2024)= $5,000 Grant Eligible Contribution in 2025

Every subsequent year you are limited to $2,500 of grant eligible contributions.

Income Thresholds (Bonds)

If your household income is $50,197 or less, and you have between 1-3 children you qualify for what is called the Child Learning Bond (CLB). With the CLB the Government of Canada will contribute $500 in your first year, and $100 for each subsequent year up to a lifetime maximum of $2,000 to the beneficiaries RESP.

What makes this program so powerful is that you, as the subscriber, don’t even have to contribute any money to the account in order to qualify and receive the CLB. All you have to do is open an RESP for the beneficiary. In other words, this is $2,000 of free money.

Quebec Education Savings Incentive

If you live in Quebec there is an additional grant called the Quebec Education Savings Incentive (QESI).

This grant will match 10% of your RESP contributions, up to a maximum of $3,600. This means that for Quebec citizens that contribute $2,500 per year to a beneficiaries RESP, could potentially receive up to a 30% matching on every dollar up to the $36,000 lifetime maximum.

20% from CESG

10% from QESI

That is potentially $10,800 of free money on $36,000 of contributions. Seems like a pretty good trade if you ask me…

Tax Advantages

The next important characteristic of the RESP is the tax advantages provided by the account. The name of the account creates confusion for many people as it sounds like the RRSP. However, the tax implications of the account are actually more like the TFSA. The subscriber (ie. parent or grandparent) does not get a tax deduction in the year of contribution. Sorry Grandpa… no tax breaks on this one. Instead you are contributing with after tax dollars, like a TFSA.

However, the tax advantages occur while the account is open, and at the time of withdrawal.

Tax Free Growth

Any money made while the account is open in the form of interest, dividends, or capital gains are not subjected to taxation in the year they are earned. This is what we call tax-free growth.

Withdrawal

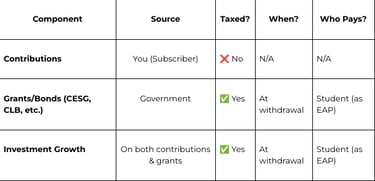

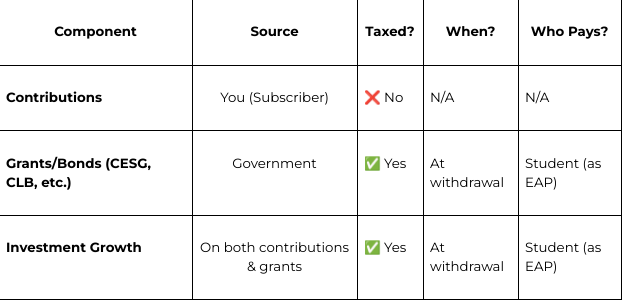

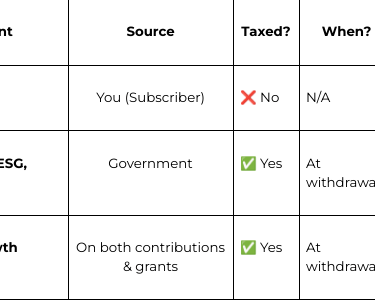

The funds from the RESP are withdrawn in the name of the beneficiary (ie. child). Provided this information, the child or grandchild will be taxed on the money withdrawn during their post-secondary education. This initially sound very bad right? … no parent wants to increase their child's tax obligations. However, before you give up on this account please consider the following:

The Child will be attending post-secondary education which means they will have a low taxable income. Add to this they will be eligible for tax write-offs, and deductions. This often results in minimal to no taxation on the funds withdrawn from a RESP.

The beneficiary is only taxed on the EAP (Education Assistance Payment) which is made up of:

Any money you receive as part of the Canada Education Savings Grant (CESG), or Canada Learning Bond (CLB)

Any investment growth accumulated in the account.

They are not taxed on any of the funds made by contributions to the account.

Why?

Because remember the RESP contributions are after tax dollars, they had to be reported as income in the year you received them. If they were taxed upon withdrawal from the RESP that would be double taxation, and would negate the benefits of this account.

To reduce the complexity let’s us an example:

Imagine your son Joey is 18 years of age, and attending post-secondary education. You as a financially savvy adult have maximized their RRSP up until the grant limit every year.

Contributions of $36,000.

CESG Grants of $7,200.

Not only were you a forward thinking individual but also an avid reader of NextGenFinance Canada. You used the smart investing strategies taught here to grow the account to $100,000.

Investment Growth Earned of $66,800 (ie. $100,000 - $36,000 - $7,200)

If you remember the EAP is made up of all grants/bonds received and any interest earned in the account. This portion will be subjected to taxation upon withdrawal.

EAP of $74,000 (ie. $66,800 + $7,200)

What Can You Invest the Money In?

Similar to your other tax-advantaged accounts the money in an RESP can be invested in a variety of financial products including ETFs, Stocks, Bonds, REITS, GIC's, Mutual Funds, etc. You can use a direct investment account and manage the money on your own, or you can outsource to a financial advisor.

All investment gains over the life of the account (ie. interest, capital gains, or dividends) will not be subjected to income taxes at the time they are received. As we stated above you will be taxed at the time of withdrawal on the EAP. However, these taxes aren't applied while the money remains in the account like they would be in a taxable account.

As per usual, we recommend that you take the time to understand the fee structure if you do hire a financial advisor to manage your investment accounts. Although there are many good people in the financial services industry there are equally as many bad actors. Our primary goal with this website is to help you be more informed with your financial decisions so that you can identify these bad actors when they arrive.

How to Withdraw the Funds?

In order to withdraw the funds from an RESP the beneficiary will need proof of enrollment in a educational institution. This is a document that you can often get on your university portal, or at the student centre.

The standards of what programs qualify for RESP withdrawals are quite vast including a undergraduate degree, college, and trade programs. Even some shorter programs may qualify.

Also, the funds can be used for education outside of Canada. For more information regarding if the program qualifies though we suggest you consult the Government of Canada website.

Withdrawal-First Year Rule

One additional layer of complexity is how much can be withdrawn from this account in the first 13 weeks of the program. If you remember from earlier we divided the total balance of the account into two categories:

The contributions made by the subscriber

The EAP which consists of grants/bonds provided by the government, and any investment growth.

The beneficiary can withdraw some or all of the initial contributions at any time throughout the educational program. However, during the first 13 weeks of the program the maximum amount of EAP that can be withdrawn is limited to $8,000 for a full time education, and $4,000 for part time education. This is measure used in order to limit individuals from enrolling in post-secondary education to get access to the funds, and then dropping out of school.

In certain circumstances you do have the ability to submit a request via your promoter (ie. the financial institution) for increased funds during this period. However, you will be required to provide receipts to support the request.

What Can the Funds be Withdrawn For?

The funds can be withdrawn from the account for a variety of education related expenses. This could be the obvious expenses such tuition, rent, books, transportation, and school related equipment (ie. pencils, laptop, notebooks, agenda's).

It can also expand to things such as the purchase of a car, or other non-obvious expenses. However, similar to a business you should keep a good record of receipts and have a appropriate rationale for the purchase as the account can be subjected to an audit.

According to the Government of Canada website the RESP "promoter" determines what is a "reasonable" expense. So there is a lot of subjectivity in the wording.

What if the Funds Do Not Get Used?

Before we explain what will happen if your child/grandchild decides to not attend post-secondary education we must note that you can use the funds up until your child's 35th birthday. There is no harm in keeping the account open in case the child decides later that they would like to go to University or College.

If you are certain they will not be attending post-secondary education you have three options:

1. Replace the Beneficiary

If you don't already have a family RESP the funds can be transferred to another beneficiary.

However, the maximum remains $50,000 per beneficiary.

2. Transfer to the RRSP of the Subscriber/Beneficiary

The money can be transferred to the RRSP of the Subscriber or Beneficiary provided they have the available contribution limit.

There is a limit of $50,000 of investment gains though.

3. Transfer to RDSP of Beneficiary

If the child has a disability that would prevent them from attending post-secondary education you have the option of transferring the funds to an RDSP.

However, there is one major caveat with this. If the funds are not used for the purpose of education you will be required to pay back both the CESG, and 20% of investment returns (ie. the amount equivalent of the CESG portion).

How to Maximize This Account

Firstly, let’s recap prior sections:

If you have a low family income (ie. $50,197 or <), and do not have available funds to contribute to the RESP it is still worth opening the account for a beneficiary. In doing so they will get access to the CLB which is $2,000 of free money.

If you do have funds to contribute to this account for a beneficiary. You will receive 20% matching on the first $2,500/year of contributions. This is $500 of free money per year from the CESG.

The maximum lifetime CESG grants is $7,200 which would require you to make $36,000 of contributions.

The total contribution limit for the RESP is $50,000 per beneficiary. This means that the last $14,000 will not be matched at 20%.

Even with these restrictions the account is a very powerful tool to assist in saving for the post-secondary education of a loved one. However, some people like to optimize, and this section is for them. The following are a list of strategies that can be utilized to get full use of this account:

1. Investment Strategy

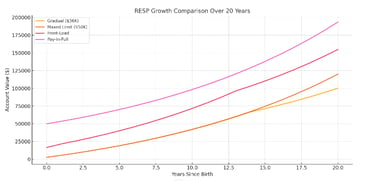

Historically, stocks have outperformed all other assets, on timeframes > than 10 years. Provided you start investing around the time your child is born, or even within the first 5 years of their lifespan a portfolio of 100% stocks should ensure the best returns when the money is withdrawn.

Ex. Assuming you start contributing in the year the child is born, maximize the grants, and invest in stocks yielding 7% per year. The expected return by the time the child is 18 years of age should be ~90,213.

Note: Similar to retirement there is a drawdown period that occurs during the beneficiaries post-secondary education. During this time stability becomes more important relative to investment returns. Consequently, it may be better to shift to more stable assets (ie. bonds, GIC's) to minimize the volatility of your portfolio as they approach their post-secondary education.

2. Maximize Account Limit

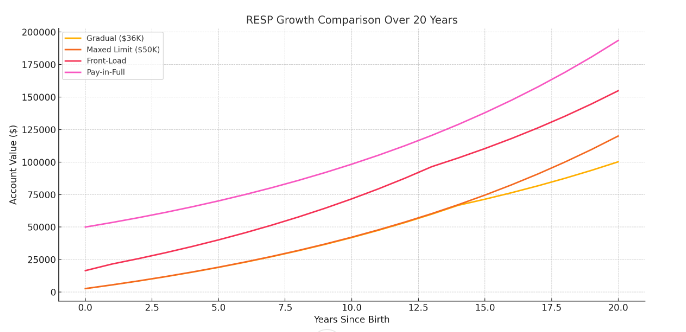

As we stated earlier the contribution limit of the RESP is $50,000. However, you maximize the grants when you contribute $36,000. One way of optimizing this account would be to just continue contributing after you have maxed out the grants.

Utilizing a similar investment strategy as above yielding 7%/year, the beneficiary should have:

~$100,032 at 18 years of age

or ~$119,701 at 20 years of age (which is when the full $50,000 will have been contributed).

3. Front Load Method

The front load method is when you contribute the non-grant eligible portion in the first year of the account. In this case you would contribute $16,500 in your first year which includes:

$14,000 (Non-Grant Eligible Funds)

and $2,500 in order to qualify for the first $500 of CESG.

Why?

This allows you to start compounding the money as early as possible. The more money you have to compound early, the greater the account balance will be when the child goes to post-secondary education.

Using this strategy, investing 100% stocks, and earning 7%/year the child should have a RESP balance of $137,532.

Note: In theory, this could also be done in the subscribers TFSA. However, this depends on them having the available contribution limit.

4. Pay in Full

Another strategy people may utilize is the paid in full method. This involves depositing $50,000 directly into the account when your child is born. In which case you would only receive the first $500 of CESG. The purpose is that the full $50,000 could start to compound today, and would have a full 18 years or more depending on when your child/grandchild starts post-secondary education.

Although this strategy will produce a higher account balance we are not the biggest fan for a few reasons.

Firstly, very few people actually have $50,000 to deposit into the account.

Secondly, you don't take advantage of the CESG after year 1.

Lastly, if you aren't capitalizing on the CESG, then contributing to a TFSA may be a better use of the funds.

However, despite the drawbacks to this method it appears to perform the best with an account balance at 18 years of age of ~$170,686.

5. Using a Bare Trust

The next strategy we have to give credit where credit is due. We got this strategy from Ed Rempel at the Unconventional Wisdom Podcast.

There are two methods in this one:

The first would involve putting all $36,000 into a Bare Trust when the beneficiary is born, and investing it.

You would then deposit $2,500 each year into an RESP for the beneficiary each year in order to receive the $500 of CESG.

You would repeat this until the grants are maximized.

The second would be the same process except you would invest the full $50,000 into the bare trust when the beneficiary is born.

Both of these will produce significantly higher returns then the other two methods. However, due to the complexities of setting up a bare trust we recommend that you consult with a tax professional before engaging in either option.

6. Withdraw Strategically

The last way to optimize this account has to do with when the funds are withdrawn. The goal should be to strategically withdraw the taxable portion of the funds (ie. EAP) during the beneficiaries lowest income years.

Many people will decide to work part-time during their post-secondary education, or they may qualify for a paid co-op/internship. These decisions often occur during the 3rd or 4th year of an undergraduate degree. If you believe the beneficiary has a high likelihood of getting an internship, or working later in their education it may be worth increasing the withdrawal of the EAP portion during years 1 and 2.

Similar to the use of the Bare Trust though we recommend you consult with a tax professional to set-up a plan in order to minimize the tax burden upon withdrawal.

Drawbacks to the RESP

We believe that the RESP is very powerful tool that could be very helpful for parents looking to save for their child's education. However, like any account type their are drawbacks. The key drawbacks of the RESP include:

1. Limited Benefits for Lower-Income Families

Although low income individuals have access to the Canada Learning Bond (CLB) the program is limited. You need a low family income, and the amount received is very small relative to rising tuition costs.

In order to maximize this account the subscriber would need to have an extra $2,500 per year of disposable income. Provided rising cost of living there are fewer people who are able to come up with the $2,500 each year in order to maximize the grant. This is especially true when considering that fewer jobs offer pensions so families have the added stress of saving for retirement.

2. No Recent Adjustments

The RESP contribution limit and grant amount has remained the same since 2007. In 2007, the annual tuition for an average Canadian undergraduate program was $4,558 according to StatsCan. Since this time it has increased to $7,360. Now factor in rising costs of housing, food, transportation, and equipment and the cost is significant.

In order for this program to maintain its effectiveness it should increase with the rate of inflation.

3. Potential Impact on Scholarships

In order to qualify for certain scholarships you have to provide financial information. One of those pieces of information is whether, or not you have an RESP. The RESP balance in this case can be calculated into the determination of whether or not you are eligible for certain scholarships.

This is my biggest pet peeve with the RESP. In this case the student is actually being punished for their parent/guardians financial due diligence. In reality, there are many people who don't have a high income per se but are good savers, and financially intelligent. This should be rewarded, not restricted.

4. Limited Flexibility

A child may choose to pursue Entrepreneurship instead of post-secondary education. Based on the information we found, you are unable to use the EAP funds towards starting a business. So if you do decide to withdraw the money for anything outside of attending post-secondary education you will have to return the CESG, and 20% of the investment gains.

In this case the child is being punished for possibly having a viable business idea instead of attending post-secondary school like their friends. This in our opinion is a net negative for the growth of the Canadian economy.

Conclusion

The Registered Education Savings Plan (RESP) remains one of the most powerful tools available to Canadian parents and guardians looking to invest in their child’s post-secondary future. By taking advantage of the government grants, tax-sheltered growth, and flexibility in investment choices, families can substantially ease the financial burden of higher education. While there are limitations—especially for low-income families or those whose children pursue non-traditional paths—the RESP still provides unmatched value when used strategically. Whether you're just beginning to plan or looking to optimize your approach, understanding the RESP in detail allows you to make informed decisions that can significantly benefit the next generation.

If you liked this post you may also like:

[FHSA Canada Guide: How It Works for First-Time Home Buyers]

[RRSP Guide 2025: Canada's Powerful Retirement Savings Tool]

[Registered Disability Savings Plan (RDSP): Complete Guide for 2025]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Government of Canada. “Registered Education Savings Plan (RESP).”

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/registered-education-savings-plans-resps.htmlGovernment of Canada. “Canada Education Savings Grant (CESG).”

https://www.canada.ca/en/employment-social-development/services/education-savings/education-savings-grant.htmlGovernment of Canada. “Canada Learning Bond (CLB).”

https://www.canada.ca/en/employment-social-development/services/learning-bond.htmlGovernment of Canada. “Promoters’ Guide to RESP.”

https://www.canada.ca/en/employment-social-development/services/student-financial-aid/resp/promoters-guide.htmlStatistics Canada. “Table 37-10-0045-01 – Canadian undergraduate tuition fees by field of study.”

https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3710004501Quebec Government. “Quebec Education Savings Incentive (QESI).”

https://www.revenuquebec.ca/en/citizens/tax-credits/quebec-education-savings-incentive/

What is the RESP?

In previous blogs we discussed a variety of registered account types including the TFSA, RRSP, & FHSA. Each of which was created for a unique purpose.

The account we are going to discuss today is perfect for parents, or grandparents. This account is referred to as the RESP which stands for the Registered Education Savings Plan. The RESP is a tax deferred account that was set up by the government in 1974 in order to help parents save for their child’s post-secondary education.

This account acts like a piggy bank for your child's education. However, what makes this account unique is that the government assists you in contributing to it over time.

Key Terms

The terminology used to describe this account can often provide confusion. In order to avoid this the following is a list of what those terms are, and what they refer to:

Subscriber (The person who opens the account)

Beneficiary (The Child)

Promoter (The Financial Institution)

EAP (Education Assistance Payment)

Opening an RESP

You can open, and start contributing to an RESP as soon as your child is born. This can be done through most financial institutions.

All you will need to set-up the account is:

Legal name of the beneficiary

Social insurance number of the beneficiary

And a date of birth of the beneficiary

The maximum contribution limit to the RESP is $50,000 per beneficiary.

Multiple accounts can be set-up for each beneficiary. So if the grandparents of the child also want to set up an RESP, they can too. However, is important that you monitor the total contribution amount if you do decide to set-up multiple accounts in order to avoid over-contributing. The fee for over-contribution is the same as other tax-advantaged accounts charged at 1% of the over-contributed balance per month.

All of the contributions must be made prior to the beneficiaries 31st Birthday.

Types of RESP's

The two types of RESP’s are:

Individual RESP

Family RESP

Regardless of which option that you choose the maximum contribution limit remains at $50,000 per beneficiary. For example: If you had 3 children you could contribute up to $150,000 to a family RESP (ie. $50,000 per beneficiary)

The primary benefit of a family RESP is that the funds can be split between children. This is helpful in cases whereby one child's education is more costly than others.

Now that you know the types of RESP accounts available, let’s dive into what makes them particularly powerful.

What Makes the RESP Unique?

The RESP is unique for two specific reasons:

The Grants/Bonds

& Tax Advantages

Grants and Bond

Canada Education Savings Grant (CESG)

The primary benefit of the RESP is the ability to receive the Canada Education Savings Grant (CESG). This is a government grant that will match 20% of your contribution room up to a yearly maximum of $500. In order to receive the maximum annual grant you will need to contribute $2,500/year.

The maximum amount of grant that a beneficiary can receive over the life of the account is $7,200. This would require you to contribute a total of $36,000 (ie. 14.5 years x $2,500).

You will receive no additional grant money by contributing more than $2,500 in a single year, or $36,000 over the life of the account. However, in the case that a year is missed you are able to engage in a one year catch-up by contributing an additional $2,500 in that year.

For Example: Imagine you start contributing to your Child's RESP in 2025, when they reached 3 years of age. In this case you would be able to contribute $5,000 in the first year of the account, and receive $1,000 worth of CESG.

$2,500 (Grant Eligible Contribution for 2025) + $2,500 (Catch-Up Grant Eligible Contribution from 2024)= $5,000 Grant Eligible Contribution in 2025

Every subsequent year you are limited to $2,500 of grant eligible contributions.

Income Thresholds (Bonds)

If your household income is $50,197 or less, and you have between 1-3 children you qualify for what is called the Child Learning Bond (CLB). With the CLB the Government of Canada will contribute $500 in your first year, and $100 for each subsequent year up to a lifetime maximum of $2,000 to the beneficiaries RESP.

What makes this program so powerful is that you, as the subscriber, don’t even have to contribute any money to the account in order to qualify and receive the CLB. All you have to do is open an RESP for the beneficiary. In other words, this is $2,000 of free money.

Quebec Education Savings Incentive

If you live in Quebec there is an additional grant called the Quebec Education Savings Incentive (QESI).

This grant will match 10% of your RESP contributions, up to a maximum of $3,600. This means that for Quebec citizens that contribute $2,500 per year to a beneficiaries RESP, could potentially receive up to a 30% matching on every dollar up to the $36,000 lifetime maximum.

20% from CESG

10% from QESI

That is potentially $10,800 of free money on $36,000 of contributions. Seems like a pretty good trade if you ask me…

Tax Advantages

The next important characteristic of the RESP is the tax advantages provided by the account. The name of the account creates confusion for many people as it sounds like the RRSP. However, the tax implications of the account are actually more like the TFSA. The subscriber (ie. parent or grandparent) does not get a tax deduction in the year of contribution. Sorry Grandpa… no tax breaks on this one. Instead you are contributing with after tax dollars, like a TFSA.

However, the tax advantages occur while the account is open, and at the time of withdrawal.

Tax Free Growth

Any money made while the account is open in the form of interest, dividends, or capital gains are not subjected to taxation in the year they are earned. This is what we call tax-free growth.

Withdrawal

The funds from the RESP are withdrawn in the name of the beneficiary (ie. child). Provided this information, the child or grandchild will be taxed on the money withdrawn during their post-secondary education. This initially sound very bad right? … no parent wants to increase their child's tax obligations. However, before you give up on this account please consider the following:

The Child will be attending post-secondary education which means they will have a low taxable income. Add to this they will be eligible for tax write-offs, and deductions. This often results in minimal to no taxation on the funds withdrawn from a RESP.

The beneficiary is only taxed on the EAP (Education Assistance Payment) which is made up of:

Any money you receive as part of the Canada Education Savings Grant (CESG), or Canada Learning Bond (CLB)

Any investment growth accumulated in the account.

They are not taxed on any of the funds made by contributions to the account.

Why?

Because remember the RESP contributions are after tax dollars, they had to be reported as income in the year you received them. If they were taxed upon withdrawal from the RESP that would be double taxation, and would negate the benefits of this account.

To reduce the complexity let’s us an example:

Imagine your son Joey is 18 years of age, and attending post-secondary education. You as a financially savvy adult have maximized their RRSP up until the grant limit every year.

Contributions of $36,000.

CESG Grants of $7,200.

Not only were you a forward thinking individual but also an avid reader of NextGenFinance Canada. You used the smart investing strategies taught here to grow the account to $100,000.

Investment Growth Earned of $66,800 (ie. $100,000 - $36,000 - $7,200)

If you remember the EAP is made up of all grants/bonds received and any interest earned in the account. This portion will be subjected to taxation upon withdrawal.

EAP of $74,000 (ie. $66,800 + $7,200)

What Can You Invest the Money In?

Similar to your other tax-advantaged accounts the money in an RESP can be invested in a variety of financial products including ETFs, Stocks, Bonds, REITS, GIC's, Mutual Funds, etc. You can use a direct investment account and manage the money on your own, or you can outsource to a financial advisor.

All investment gains over the life of the account (ie. interest, capital gains, or dividends) will not be subjected to income taxes at the time they are received. As we stated above you will be taxed at the time of withdrawal on the EAP. However, these taxes aren't applied while the money remains in the account like they would be in a taxable account.

As per usual, we recommend that you take the time to understand the fee structure if you do hire a financial advisor to manage your investment accounts. Although there are many good people in the financial services industry there are equally as many bad actors. Our primary goal with this website is to help you be more informed with your financial decisions so that you can identify these bad actors when they arrive.

How to Withdraw the Funds?

In order to withdraw the funds from an RESP the beneficiary will need proof of enrollment in a educational institution. This is a document that you can often get on your university portal, or at the student centre.

The standards of what programs qualify for RESP withdrawals are quite vast including a undergraduate degree, college, and trade programs. Even some shorter programs may qualify.

Also, the funds can be used for education outside of Canada. For more information regarding if the program qualifies though we suggest you consult the Government of Canada website.

Withdrawal-First Year Rule

One additional layer of complexity is how much can be withdrawn from this account in the first 13 weeks of the program. If you remember from earlier we divided the total balance of the account into two categories:

The contributions made by the subscriber

The EAP which consists of grants/bonds provided by the government, and any investment growth.

The beneficiary can withdraw some or all of the initial contributions at any time throughout the educational program. However, during the first 13 weeks of the program the maximum amount of EAP that can be withdrawn is limited to $8,000 for a full time education, and $4,000 for part time education. This is measure used in order to limit individuals from enrolling in post-secondary education to get access to the funds, and then dropping out of school.

In certain circumstances you do have the ability to submit a request via your promoter (ie. the financial institution) for increased funds during this period. However, you will be required to provide receipts to support the request.

What Can the Funds be Withdrawn For?

The funds can be withdrawn from the account for a variety of education related expenses. This could be the obvious expenses such tuition, rent, books, transportation, and school related equipment (ie. pencils, laptop, notebooks, agenda's).

It can also expand to things such as the purchase of a car, or other non-obvious expenses. However, similar to a business you should keep a good record of receipts and have a appropriate rationale for the purchase as the account can be subjected to an audit.

According to the Government of Canada website the RESP "promoter" determines what is a "reasonable" expense. So there is a lot of subjectivity in the wording.

What if the Funds Do Not Get Used?

Before we explain what will happen if your child/grandchild decides to not attend post-secondary education we must note that you can use the funds up until your child's 35th birthday. There is no harm in keeping the account open in case the child decides later that they would like to go to University or College.

If you are certain they will not be attending post-secondary education you have three options:

1. Replace the Beneficiary

If you don't already have a family RESP the funds can be transferred to another beneficiary.

However, the maximum remains $50,000 per beneficiary.

2. Transfer to the RRSP of the Subscriber/Beneficiary

The money can be transferred to the RRSP of the Subscriber or Beneficiary provided they have the available contribution limit.

There is a limit of $50,000 of investment gains though.

3. Transfer to RDSP of Beneficiary

If the child has a disability that would prevent them from attending post-secondary education you have the option of transferring the funds to an RDSP.

However, there is one major caveat with this. If the funds are not used for the purpose of education you will be required to pay back both the CESG, and 20% of investment returns (ie. the amount equivalent of the CESG portion).

How to Maximize This Account

Firstly, let’s recap prior sections:

If you have a low family income (ie. $50,197 or <), and do not have available funds to contribute to the RESP it is still worth opening the account for a beneficiary. In doing so they will get access to the CLB which is $2,000 of free money.

If you do have funds to contribute to this account for a beneficiary. You will receive 20% matching on the first $2,500/year of contributions. This is $500 of free money per year from the CESG.

The maximum lifetime CESG grants is $7,200 which would require you to make $36,000 of contributions.

The total contribution limit for the RESP is $50,000 per beneficiary. This means that the last $14,000 will not be matched at 20%.

Even with these restrictions the account is a very powerful tool to assist in saving for the post-secondary education of a loved one. However, some people like to optimize, and this section is for them. The following are a list of strategies that can be utilized to get full use of this account:

1. Investment Strategy

Historically, stocks have outperformed all other assets, on timeframes > than 10 years. Provided you start investing around the time your child is born, or even within the first 5 years of their lifespan a portfolio of 100% stocks should ensure the best returns when the money is withdrawn.

Ex. Assuming you start contributing in the year the child is born, maximize the grants, and invest in stocks yielding 7% per year. The expected return by the time the child is 18 years of age should be ~90,213.

Note: Similar to retirement there is a drawdown period that occurs during the beneficiaries post-secondary education. During this time stability becomes more important relative to investment returns. Consequently, it may be better to shift to more stable assets (ie. bonds, GIC's) to minimize the volatility of your portfolio as they approach their post-secondary education.

2. Maximize Account Limit

As we stated earlier the contribution limit of the RESP is $50,000. However, you maximize the grants when you contribute $36,000. One way of optimizing this account would be to just continue contributing after you have maxed out the grants.

Utilizing a similar investment strategy as above yielding 7%/year, the beneficiary should have:

~$100,032 at 18 years of age

or ~$119,701 at 20 years of age (which is when the full $50,000 will have been contributed).

3. Front Load Method

The front load method is when you contribute the non-grant eligible portion in the first year of the account. In this case you would contribute $16,500 in your first year which includes:

$14,000 (Non-Grant Eligible Funds)

and $2,500 in order to qualify for the first $500 of CESG.

Why?

This allows you to start compounding the money as early as possible. The more money you have to compound early, the greater the account balance will be when the child goes to post-secondary education.

Using this strategy, investing 100% stocks, and earning 7%/year the child should have a RESP balance of $137,532.

Note: In theory, this could also be done in the subscribers TFSA. However, this depends on them having the available contribution limit.

4. Pay in Full

Another strategy people may utilize is the paid in full method. This involves depositing $50,000 directly into the account when your child is born. In which case you would only receive the first $500 of CESG. The purpose is that the full $50,000 could start to compound today, and would have a full 18 years or more depending on when your child/grandchild starts post-secondary education.

Although this strategy will produce a higher account balance we are not the biggest fan for a few reasons.

Firstly, very few people actually have $50,000 to deposit into the account.

Secondly, you don't take advantage of the CESG after year 1.

Lastly, if you aren't capitalizing on the CESG, then contributing to a TFSA may be a better use of the funds.

However, despite the drawbacks to this method it appears to perform the best with an account balance at 18 years of age of ~$170,686.

5. Using a Bare Trust

The next strategy we have to give credit where credit is due. We got this strategy from Ed Rempel at the Unconventional Wisdom Podcast.

There are two methods in this one:

The first would involve putting all $36,000 into a Bare Trust when the beneficiary is born, and investing it.

You would then deposit $2,500 each year into an RESP for the beneficiary each year in order to receive the $500 of CESG.

You would repeat this until the grants are maximized.

The second would be the same process except you would invest the full $50,000 into the bare trust when the beneficiary is born.

Both of these will produce significantly higher returns then the other two methods. However, due to the complexities of setting up a bare trust we recommend that you consult with a tax professional before engaging in either option.

6. Withdraw Strategically

The last way to optimize this account has to do with when the funds are withdrawn. The goal should be to strategically withdraw the taxable portion of the funds (ie. EAP) during the beneficiaries lowest income years.

Many people will decide to work part-time during their post-secondary education, or they may qualify for a paid co-op/internship. These decisions often occur during the 3rd or 4th year of an undergraduate degree. If you believe the beneficiary has a high likelihood of getting an internship, or working later in their education it may be worth increasing the withdrawal of the EAP portion during years 1 and 2.

Similar to the use of the Bare Trust though we recommend you consult with a tax professional to set-up a plan in order to minimize the tax burden upon withdrawal.

Drawbacks to the RESP

We believe that the RESP is very powerful tool that could be very helpful for parents looking to save for their child's education. However, like any account type their are drawbacks. The key drawbacks of the RESP include:

1. Limited Benefits for Lower-Income Families

Although low income individuals have access to the Canada Learning Bond (CLB) the program is limited. You need a low family income, and the amount received is very small relative to rising tuition costs.

In order to maximize this account the subscriber would need to have an extra $2,500 per year of disposable income. Provided rising cost of living there are fewer people who are able to come up with the $2,500 each year in order to maximize the grant. This is especially true when considering that fewer jobs offer pensions so families have the added stress of saving for retirement.

2. No Recent Adjustments

The RESP contribution limit and grant amount has remained the same since 2007. In 2007, the annual tuition for an average Canadian undergraduate program was $4,558 according to StatsCan. Since this time it has increased to $7,360. Now factor in rising costs of housing, food, transportation, and equipment and the cost is significant.

In order for this program to maintain its effectiveness it should increase with the rate of inflation.

3. Potential Impact on Scholarships

In order to qualify for certain scholarships you have to provide financial information. One of those pieces of information is whether, or not you have an RESP. The RESP balance in this case can be calculated into the determination of whether or not you are eligible for certain scholarships.

This is my biggest pet peeve with the RESP. In this case the student is actually being punished for their parent/guardians financial due diligence. In reality, there are many people who don't have a high income per se but are good savers, and financially intelligent. This should be rewarded, not restricted.

4. Limited Flexibility

A child may choose to pursue Entrepreneurship instead of post-secondary education. Based on the information we found, you are unable to use the EAP funds towards starting a business. So if you do decide to withdraw the money for anything outside of attending post-secondary education you will have to return the CESG, and 20% of the investment gains.

In this case the child is being punished for possibly having a viable business idea instead of attending post-secondary school like their friends. This in our opinion is a net negative for the growth of the Canadian economy.

Conclusion

The Registered Education Savings Plan (RESP) remains one of the most powerful tools available to Canadian parents and guardians looking to invest in their child’s post-secondary future. By taking advantage of the government grants, tax-sheltered growth, and flexibility in investment choices, families can substantially ease the financial burden of higher education. While there are limitations—especially for low-income families or those whose children pursue non-traditional paths—the RESP still provides unmatched value when used strategically. Whether you're just beginning to plan or looking to optimize your approach, understanding the RESP in detail allows you to make informed decisions that can significantly benefit the next generation.

If you liked this post you may also like:

[FHSA Canada Guide: How It Works for First-Time Home Buyers]

[RRSP Guide 2025: Canada's Powerful Retirement Savings Tool]

[Why the TFSA Is the Best Registered Account in Canada (2025)]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Government of Canada. “Registered Education Savings Plan (RESP).”

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/registered-education-savings-plans-resps.htmlGovernment of Canada. “Canada Education Savings Grant (CESG).”

https://www.canada.ca/en/employment-social-development/services/education-savings/education-savings-grant.htmlGovernment of Canada. “Canada Learning Bond (CLB).”

https://www.canada.ca/en/employment-social-development/services/learning-bond.htmlGovernment of Canada. “Promoters’ Guide to RESP.”

https://www.canada.ca/en/employment-social-development/services/student-financial-aid/resp/promoters-guide.htmlStatistics Canada. “Table 37-10-0045-01 – Canadian undergraduate tuition fees by field of study.”

https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3710004501Quebec Government. “Quebec Education Savings Incentive (QESI).”

https://www.revenuquebec.ca/en/citizens/tax-credits/quebec-education-savings-incentive/