Get our free Debt vs Invest Calculator — click here to access it

Registered Disability Savings Plan (RDSP): Complete Guide for 2025

Complete Registered Disability Savings Plan Canada guide: eligibility requirements, government grants and bonds, tax benefits, investment options, and withdrawal rules.

REGISTERED DISABILITY SAVINGS PLANRDSP

9/15/202533 min read

Introduction

The Registered Disability Savings Plan (RDSP) is one of the most powerful, yet often overlooked, financial tools available to Canadians with disabilities and their families. Designed to provide long-term security, the RDSP combines personal contributions with generous government grants and bonds, all while allowing investments to grow tax-deferred. Despite its benefits, many people either don’t know it exists, or assume it’s too complex to set up.

In this guide, we’ll walk you through everything you need to know about the RDSP in 2025 from eligibility criteria and contributions, to government support, investment strategies, and withdrawal rules. Our hope is that this will help you make the most of this unique opportunity.

What is an RDSP?

The RDSP was introduced in 2008 by the Government of Canada. It was designed to provide support for Canadians with disabilities and their families. The program was directed towards enabling families of those with disabilities to save for their future, and ensure financial security.

As we will discuss, this account has a complex start-up process. However, once it is set-up, it provides the most significant benefits of all of the Registered Accounts.

Who is Eligible for an RDSP?

In order to set-up an RDSP with a financial institution, you have to meet certain criteria, which includes:

1. Must qualify for the Disability Tax Credit (DTC).

The Disability Tax Credit (DTC) is a key requirement for opening an RDSP. Many people are surprised by how broad the eligibility criteria can be. Qualifying doesn’t always mean you have a severe or visible disability. Instead, the DTC covers a wide range of conditions that affect daily living, such as difficulties with walking, hearing, vision, mental functions, or even life-sustaining therapies. Because of this, individuals who might not see themselves as “disabled” could still be eligible. It’s always worth reviewing the criteria or speaking with a professional before assuming you don’t qualify.

In order to apply for the DTC you are required to complete Form T2201 – Disability Tax Credit Certificate. This is a 16 page document that has two distinct sections:

Part A - Filled out by the Applicant

Personal Information (Name, Address, SIN Number) of the applicant.

Section asking if you want prior tax years adjusted from the date of DTC approval.

Authorization for the medical practitioner to release medical information.

Part B- Filled out by a Medical Professional

A medical doctor or nurse practitioner can fill out all disability sections on the form.

If the impairment is specific (ie. vision, speech, etc) there is an option of having a specialist fill out the forms.

Ex. Optometrists can fill out the vision impairment section of the form

Once the form is complete, it will need to be sent to the Canada Revenue Agency (CRA) for review. They may request more medical information, and supporting documents prior to making a decision.

2. Must meet the age requirements, or be a guardian of the recipient.

Once qualified for the DTC, an RDSP can be opened through a financial institution as long as the beneficiary is age 18 or older and has a Social Insurance Number (SIN).

If the beneficiary is under age 18, a parent, guardian, or legal representative can open the account on their behalf. The parent or guardian will be the account holder until the beneficiary turns 18. At which point the account can be transferred to the beneficiary. If the beneficiary lacks the mental capacity to manage the account, the parent or guardian can continue to control it after age 18.

An RDSP must be opened before the beneficiary is age 60. However, the eligibility for benefits (ie. grants, and bonds) stops after age 49.

Contributions and Limits

The RDSP has a lifetime contribution limit of $200,000. However, there is no annual limit.

An RDSP is limited to one account per beneficiary. However, contributions can be made by many people (more just the account holder(. While only the account holder can open and manage an RDSP, friends and family can contribute to it as well. They’ll need written permission, which usually takes the form of a signed authorization or letter handled through the financial institution that manages the RDSP.

Government Support: Grants and Bonds

The feature that makes the RDSP stand out amongst other registered accounts is the access to government support via grants and bonds. These include the Canada Disability Savings Grant (CDSG), and Canada Disability Savings Bond (CDSB). These government supports can significantly enhance the long term returns of the account by increasing your contributions.

1.Canadian Disability Savings Grant (CDSG)

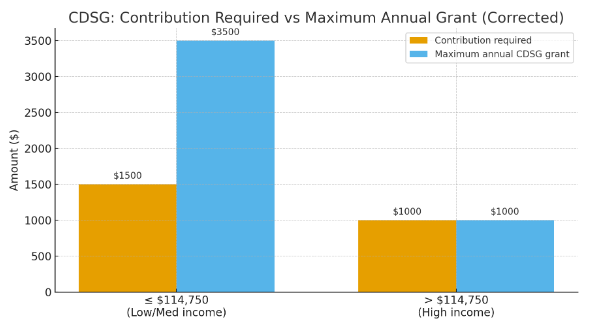

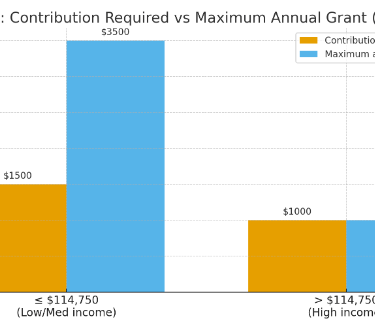

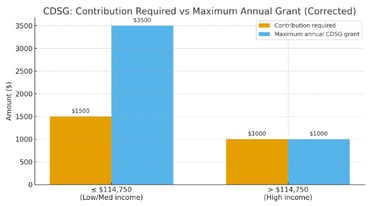

The Canadian government will match any contributions to an RDSP up to an annual maximum of $3,500 and a lifetime maximum of $70,000.

The rate of matching depends on the beneficiaries net family income:

<$114,750 of net family income

3:1 on the first $500 of yearly contributions

2:1 on the next $1,000

>$114,750 of net family income

1:1 on the first $1,000 of yearly contributions

In the case that the individual is under age 18, qualification will be calculated based on the net income of the parents/guardians. After this point, it will be based on the net income of the account beneficiary.

Example: Imagine your net family income is $95,000 and you contribute $1,500 per year to your son’s RDSP. The government will provide you with an additional $3,500 in CDSG, up to a lifetime maximum of $70,000. This is a 233% return on investment from contributing to the account alone.

Carry-forward rule

The carry-forward rule allows you to receive unused grants for up to 10 prior years. In order to be eligible to receive these grants, you would need to have had DTC status during all of the catch up years. Also, you will need to make the necessary contributions from all of those prior years.

There are a two common scenarios where this may occur:

You had DTC status, but didn’t know about the RDSP, or didn’t take advantage of the account benefits.

You just received DTC status for the current year, and previous years were recognized.

Ex. Imagine you had DTC status from 2015-2025. During which time your net family income was below the $114,750 threshold (adjusted for inflation). However, you didn’t open an RDSP until 2025. You are now eligible to receive all of the grants from that 10 year period. If you were able to do so, you could make $15,000 of contributions ($1,500 x 10 years). In return, you should receive $35,000 ($3,500 x 10 years) in CDSG. In 2026, you would be eligible to contribute an additional $1,500, and receive $3,500 in CDSG.

Investment Power of the CESG

The personal finance industry spends most of their energy discussing the subjects of savings, and cost-cutting. This is important because you can’t start to improve your financial position until you remove the proverbial 400lbs weight that looms over your head (ie. debt). However, savings and cost cutting are also important because we realize the impact that maximizing early contributions makes on your long term investment returns.

Early on, the impact of compound interest is minimal. But as your account grows, the power of compound interest is unbelievable. The CESG is such a powerful tool because it boosts your contributions. It provides fuel to the fire. A combination of your own contributions, and CESG raises the RDSP account balance closer to the point that compound interest starts to do its magic.

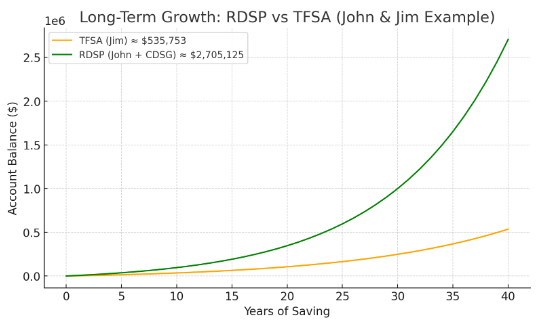

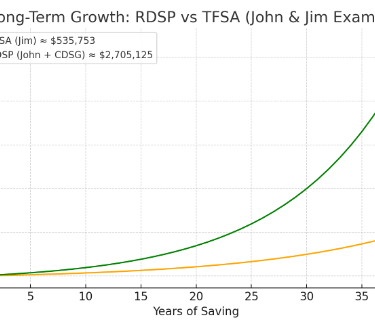

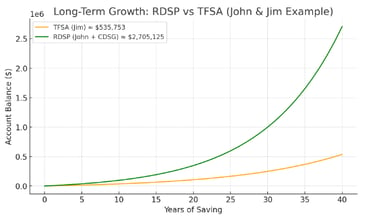

Ex. Jennifer has twin sons John and Jim that are both 10 years old.

John has a speech impediment and is eligible for the DTC, and RDSP.

Jim doesn’t have any disabilities.

Jennifer makes <$114,750. However, she is a good saver, and has $5,000/year to save for both of her son’s futures. She decides she will allocate $2,500/year for each son. She opens two accounts a TFSA for Jim (*), and an RDSP for John. In both accounts she decides to invest in a low cost index ETF which produces a long term average return of 7% /year. By age 50 the account balances should be the following:

Jim (TFSA, No CESG)- $535,753

John (RDSP, CESG)- $2,705,125

The CESG isn’t looking too bad now is it…

(*) Note that Jennifer will have to open a personal TFSA until Jim is age 18. Then he can open a TFSA of his own. The TFSA was used in this example to minimize the tax complexity of a taxable account.

2.Canadian Disability Savings Bond (CDSB)

In conjunction with the CDSG, there is also another benefit known as the Canadian Disability Savings Bond (CDSB). Like the CDSG, this bond is provided to individuals that have qualified for, and opened an RDSP. However, in order to be eligible for the CDSB you must have an individual or family net income <$57,375/year.

In the case that the individual is under age 18, qualification will be calculated based on the net income of the parents/guardians. After this point, it will be based on the net income of the account beneficiary.

Provided you meet this criteria, you may be eligible to receive up to $1,000 of CDSB annually, up to a lifetime maximum of $20,000. What’s even more enticing about this program is that you do not even need to make any contributions in order to receive these funds. This is free money.

However, the program unfortunately has additional income thresholds that impact how much of the $1,000 you are eligible for:

Annual income below $34,487 = Full $1,000 of CDSB

Annual income between $34,487 - $57,375 = <100% of CDSB

Carry-forward rule

Like the CDSG, RDSP holders are eligible to carry forward up to 10 years of CDSB entitlements. The maximum CDSB you can receive in a single year is $11,000. This consists of $1,000 of current year CDSB, and up to $10,000 of prior years CDSB.

In order to qualify, you must have had DTC status, and would have been a Canadian resident throughout this time period. You will not be required to fill out any form. Instead, the system automatically calculates and applies the prior years CDSB when you open an RDSP or make contributions, as long as eligibility requirements are met.

Ex. Imagine you received DTC status in 2015. Throughout this period your net family income has been below the $34,487 threshold. However, you didn’t open a RDSP until 2024. You would be eligible to receive all of the bonds over that 10 year period. In other words, you could theoretically contribute $0, and get $10,000 in CDSB deposited in your RDSP in year 1.

Age Limit

The beneficiary is eligible to receive grants and bonds until December 31st of the year they turn age 49. They can continue to make further contributions to the account until age 59. However, those contributions will not be eligible for government top-ups.

Please note that you could still be eligible to receive carry forward grants and bonds from prior years though, provided you meet the eligibility requirements.

The RDSP is intended as a long term savings tool in order to ensure retirement security for those with disabilities, not a short term assistance vehicle. By reducing the eligibility to age 49, it directs the focus on building savings earlier in life, giving funds more time to grow through compounding.

Investing Inside an RDSP

Like other tax-advantaged accounts (RRSP, TFSA, RESP) the RDSP funds (ie. contributions & grants/bonds) can be invested in a variety of financial products. These include:

Stocks, Bonds, GICs

ETFs, Mutual funds, REITs

High-interest savings accounts

Many financial institutions offer RDSPs, but the ability to self-manage investments may vary.

Investment Strategy

The investment approach utilized for this account will significantly depend on your personal situation. However, you should consider your risk tolerance and investment timeline.

Historically, during most rolling 10-year time periods, stocks have outperformed fixed income assets (ie. bonds and GIC’s). The mandatory withdrawal age for the RDSP is 60. This suggests that if you are 50 years old or younger, historically, stocks should provide you with a larger nest egg in retirement. On shorter timeframes, the risk adjusted return for stocks decreases. This suggests a move towards more fixed income assets may prove “safer”.

As with all investment decisions, there’s inherent risk. As the classic disclaimer goes…past results are not indicative of future returns.

Tax Treatment of RDSPs

All account types have different forms of taxation that you should consider. The RDSP is no different. The following is a break down of how the account is taxed at each stage of the process:

Contributions

Any contributions to an RDSP are not tax-deductible. Instead they act like a TFSA whereby you contribute after tax dollars.

Holding Period

Any investment growth within the RDSP (e.g., interest, dividends, capital gains) is not taxable in the year they are earned. Instead it is a tax-deferred account which means no taxes are paid on growth until withdrawal.

Withdrawal

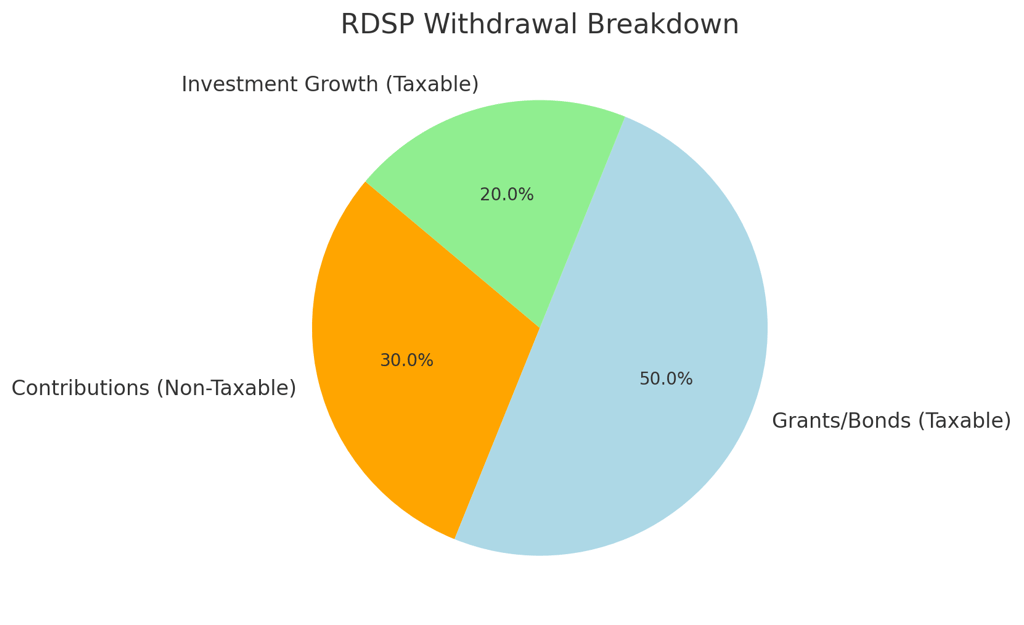

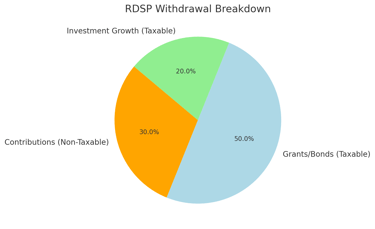

At withdrawal the funds are broken down into two distinct parts:

Contributions

Not taxable upon withdrawal.

Remember these funds were contributed using after tax dollars (see above).

Government Bonds, Grants, and Investment Gains

Subjected to taxation at the time of withdrawal.

All withdrawals from this portion will be added to an individuals earned income, and taxed at their marginal tax rate.

Withdrawal Options

RDSP withdrawals can occur at any time. However, there are specific rules depending on the beneficiary's age, and the account balance at the time of withdrawal. Generally, withdrawals are categorized into two types:

Lifetime Disability Assistance Payments (LDAP)

Disability Assistance Payments (DAP)

Lifetime Disability Assistance Payments (LDAP)

Lifetime Disability Assistance Payments (LDAP) are recurring payments to the beneficiary, using funds from their RDSP. This is similar to a RRIF for the RRSP. These payments are made up of a portion of all three components of the account: personal contributions, government contributions (CDSG or CDSB), and investment growth.

LDAPs must begin by the end of the year, when the beneficiary turns 60 years old. Once they start, they continue for the beneficiary’s lifetime. There is a complex calculation to identify the amount of those payments. However, they are calculated according to two factors:

Your account balance at the time of initiating the LDAP

Your projected life expectancy.

The following online calculator here can help you estimate your expected LDAP payments according to your planned withdrawal age.

Disability Assistance Payments (DAP)

A Disability Assistance Payment (DAP) is a one-time withdrawal that can be made at any time throughout the beneficiaries lifetime. There is no maximum for the amount that can be withdrawn during a DAP.

A DAP is intended for scenarios whereby the funds are needed to deal with financial burdens (ex. medical bills). However, there are consequences to early withdrawal…most notably what is known as The 10-Year Rule.

The 10-Year Rule: Understanding the Catch

The 10-Year Rules states that if you withdraw from the RDSP within 10 years of receiving any Canada Disability Savings Grant (CDSG) or Canada Disability Savings Bond (CDSB), you will have to repay a portion of those grants and bonds to the government. This rule is in place to encourage long-term saving, and avoid short term profiting of grants/bonds.

For every $1 withdrawn, the beneficiary will have to payback $3 of CESG and/or CESB received in the last 10 years. This is referred to as the assistance holdback amount. You personally will not have to repay the amount. Instead the RDSP provider (ie. your bank) will withhold the funds by sending them directly back to the government.

For example, imagine Sarah opened an RDSP in 2015. She contributed the maximum of $1,500 annually, and received $3,500 in CESG for the last 10 years (ie. 2015-2024). Sarah wasn’t an avid reader of the nextgenfinance Canada blog, and she didn’t invest the funds. Instead, they sat in an account collecting no interest. Now in 2025, she has an account balance of $50,000. Of which $35,000 is grants ($3,500 x 10 years). The additional $15,000 is personal contributions. However, she decides to make a withdrawal of $5,000 from the account to pay for a treatment. The 10-year rule states that she will now be required to repay $15,000 in CESG ($5,000 x 3). However, if she waited until 2035 (10 years later) to withdraw the same $5,000 she would not be obligated to repay any of the CESG.

Key takeaway: In practice, withdrawing funds so soon after receiving grants is very costly, since it triggers a much larger clawback. That’s why the RDSP is usually most beneficial if left untouched until grants have “aged out” (10 years after deposit).

Special Rules for Shortened Life Expectancy

There are special rules that apply in circumstances where the beneficiary is deemed to have a short life expectancy. A short life expectancy is considered five years or less. This exception allows the beneficiary to be able to access their funds without being subjected to the typical penalties of early withdrawal. For this to occur, the RDSP has to first be designated as a Specified Disability Savings Plan (SDSP).

In order for the RDSP to be designated as a SDSP the following steps will need to occur:

Obtain written medical documentation from a physician stating the individual has a life expectancy of five years or less.

The account holder (beneficiary or parent/guardian) will submit the document to their financial institution.

They will concurrently request for the account to be switched from an RDSP to a SDSP.

Once the RDSP becomes an SDSP:

No new contributions can be made to the account.

The beneficiary will not receive any additional grants or bonds.

Withdrawals are still taxed. However, like an RDSP, this only applies to the portion that comes from government contributions and investment growth.

While the RDSP is designated as an SDSP, there are limits on how much can be withdrawn annually:

The beneficiary can withdraw up to $10,000 per year without requiring the repayment of any Canada Disability Savings Grants (CDSG) or Bonds (CDSB).

If the beneficiary needs to withdraw more than $10,000, the 10-year repayment rule will apply, and government contributions from the last 10 years must be repaid.

In other words, by switching from the RDSP to the SDSP the beneficiary can make $10,000 of taxable withdrawals annually without the penalties they would typically be subjected to if the account remained an RDSP.

If the beneficiary’s condition improves and they are no longer considered to have a shortened life expectancy, the SDSP status can be revoked, and the RDSP will revert to its original form. This allows the plan to continue receiving contributions and government grants or bonds.

Transferring Other Accounts Into an RDSP

Converting an RESP to an RDSP

If there is an existing RESP (Registered Education Savings Plan) for the beneficiary, and they have developed a disability that reduces their ability to attend higher education, you can convert the RESP to an RDSP. This ensures that the funds continue to support the individual.

In order to transfer the funds the individual must first meet the eligibility criteria for the RDSP and be receiving the Disability Tax Credit (DTC). Once this is confirmed the following steps must occur:

Open an RDSP Account for the beneficiary

Fill out Form RC435 with your financial institution. This allows the funds to be rolled over from the RESP to an RDSP.

Close the RESP (Must be completed by the following February)

Once this is completed:

No more contributions can be made to the RESP

All government grants and bonds must be repaid to the government. This includes the CESG (Canadian Education Savings Grant) and CESB (Canadian Education Savings Bond).

All contributions to the RESP, and investment returns on those contributions (AIP) will be transferred to the RDSP and count towards your $200,000 lifetime contribution limit.

All funds transferred will not be eligible for matching grants or bonds. Also, they will be considered part of the taxable portion upon withdrawal.

Transferring Funds from a Parent/Grandparent's (RRSP, RRIF, RPP, or PRPP to an RDSP)

There are special rules for cases whereby a parent or grandparent, that financially supported the beneficiary, is deceased. In these instances, funds from their retirement accounts (RRSP, RRIF, RPP, or SPP) can be transferred to the beneficiaries RDSP. This option provides a unique way to ensure financial security for a child with a disability, while also taking advantage of the tax benefits provided by the RDSP.

Below is an overview of how this process works:

Beneficiary must qualify for the RDSP (ie. DTC status, be under the age of 59 years old.), and will have opened an account with a financial institution.

Fill out Form RC4625 with your financial institution which allows the funds to be rolled over from a variety of different pension and retirement savings plans to an RDSP.

The transfer typically happens as part of the estate settlement process upon the death of the account holder.

Close the RRSP, RRIF, RPP, or SPP

The funds are rolled over without any tax consequences in the year the rollover occurs.

The maximum transferable funds is $200,000 - Any previous contributions.

All funds transferred will not be eligible for matching grants or bonds.

They will be considered part of the taxable portion upon withdrawal.

Ex. Imagine you have already contributed $50,000 to an RDSP. Your grandfather passes away, and he would like $250,000 from his RRSP to be willed to you. In this case only $150,000 can be transferred to your RDSP. The additional $100,000 will have to be added to his final tax return, while settling the estate. The net remaining amount will then be distributed to you. At which point you can invest it in a variety of different accounts (RRSP, TFSA, Taxable Account). However, it can not be contributed to the RDSP, because the account contributions are already maximized.

What Happens If You Lose DTC Status?

A criteria for the DTC is that the individual may be required to undergo periodic re-evaluations. The frequency of these evaluations depends on the medical condition.

Permanent conditions (ex. Blindness)

May involve the CRA approving the DTC with no expiry date.

In which case no re-evaluation will occur.

Conditions that are expected to improve (ex. Physical Injuries)

CRA may grant approval for a shorter period of time, often 2-5 years.

Re-evaluation of eligibility will occur, and they may need a new T2201 Disability Tax Credit Certificate from a doctor.

In some cases, upon re-evaluation you may lose your DTC status. When this occurs you will not be able to make any further contributions to the RDSP, and you will not receive any further grants or bonds.

Changes to Loss of DTC

Prior to 2014, if you lost DTC status you were required to close your RDSP and repay all government grants/bonds obtained within the last 10 years. However, these rules were relaxed.

Now, even if you lose DTC eligibility, you are no longer required to close your RDSP immediately. Instead you have a five year “grace period” whereby the account can remain open. This is intended for circumstances whereby you expect to re-qualify again in the future. During this time, you will not be able to make further contributions or receive additional grants/bonds. However, your investments can continue to grow tax-deferred, and you will not be required to repay any grants/bonds that you have previously received.

Conclusion

The RDSP stands out as an unmatched tool for building financial security for Canadians with disabilities. With up to $90,000 available in government grants and bonds, plus the power of tax-deferred growth, it provides opportunities that no other registered account can match. While the application process may seem daunting at first, the long-term benefits far outweigh the initial complexity. If you or a loved one qualifies for the Disability Tax Credit, don’t wait. The earlier you open an RDSP, the greater the impact compounding and government support can have.

If you like this post you may also like:

[Old Age Security (OAS) in Canada 2025: Eligibility, Payments, and Clawback Explained]

[Complete Guide to Canada Pension Plan (CPP) 2025: Maximize Your Benefits & Contributions]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Canada Revenue Agency. (2023). Disability Tax Credit (DTC). Government of Canada. https://www.canada.ca/en/revenue-agency/services/tax/individuals/segments/tax-credits-deductions-persons-disabilities/disability-tax-credit.html

Canada Revenue Agency. (2023). Form RC435: Rollover from a Registered Education Savings Plan to a Registered Disability Savings Plan. Government of Canada. https://www.canada.ca/en/revenue-agency/services/forms-publications/forms/rc435.html

Canada Revenue Agency. (2023). Form RC4625: Rollover to a Registered Disability Savings Plan (RDSP) under Paragraph 60(l). Government of Canada. https://www.canada.ca/en/revenue-agency/services/forms-publications/forms/rc4625.html

Canada Revenue Agency. (2023d). Registered Disability Savings Plan (RDSP). Government of Canada. https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/registered-disability-savings-plan-rdsp.html

Employment and Social Development Canada. (2022). Canada Disability Savings Grant and Canada Disability Savings Bond. Government of Canada. https://www.canada.ca/en/employment-social-development/programs/disability/savings/eligibility.html

RBC Wealth Management. (2023). An In-Depth Look at RDSPs. https://ca.rbcwealthmanagement.com/documents/266841/1274778/An+In-Depth+Look+at+RDSPs.pdf/5d31aa7f-4e5c-4909-99e6-7134abc38c6b

Scotiabank. (2023). A Guide to the Registered Disability Savings Plan (RDSP). Scotiabank. https://www.scotiabank.com/ca/en/personal/investing/registered-disability-savings-plan.html

TD Wealth. (2023). Registered Disability Savings Plan (RDSP) Explained. TD Bank. https://www.td.com/ca/en/investing/registered-disability-savings-plan/

The Team Ability No Excuses Podcast. (2020). Episode 31: What the heck is an RDSP? [Audio podcast]. https://teamabilitypodcast.libsyn.com/episode-31-what-the-heck-is-an-rdsp

Watt, J. (Host). (2021). RDSP specialist [Audio podcast episode]. CE Drive with Jason Watt. Buzzsprout. https://www.buzzsprout.com/1593283/episodes/7978919-rdsp-specialist

Plan Institute. (n.d.). RDSP calculator. Retrieved September 13, 2025, from https://www.rdsp.com/calculator/

Introduction

The Registered Disability Savings Plan (RDSP) is one of the most powerful, yet often overlooked, financial tools available to Canadians with disabilities and their families. Designed to provide long-term security, the RDSP combines personal contributions with generous government grants and bonds, all while allowing investments to grow tax-deferred. Despite its benefits, many people either don’t know it exists, or assume it’s too complex to set up.

In this guide, we’ll walk you through everything you need to know about the RDSP in 2025 from eligibility criteria and contributions, to government support, investment strategies, and withdrawal rules. Our hope is that this will help you make the most of this unique opportunity.

What is an RDSP?

The RDSP was introduced in 2008 by the Government of Canada. It was designed to provide support for Canadians with disabilities and their families. The program was directed towards enabling families of those with disabilities to save for their future, and ensure financial security.

As we will discuss, this account has a complex start-up process. However, once it is set-up, it provides the most significant benefits of all of the Registered Accounts.

Who is Eligible for an RDSP?

In order to set-up an RDSP with a financial institution, you have to meet certain criteria, which includes:

1. Must qualify for the Disability Tax Credit (DTC).

The Disability Tax Credit (DTC) is a key requirement for opening an RDSP. Many people are surprised by how broad the eligibility criteria can be. Qualifying doesn’t always mean you have a severe or visible disability. Instead, the DTC covers a wide range of conditions that affect daily living, such as difficulties with walking, hearing, vision, mental functions, or even life-sustaining therapies. Because of this, individuals who might not see themselves as “disabled” could still be eligible. It’s always worth reviewing the criteria or speaking with a professional before assuming you don’t qualify.

In order to apply for the DTC you are required to complete Form T2201 – Disability Tax Credit Certificate. This is a 16 page document that has two distinct sections:

Part A - Filled out by the Applicant

Personal Information (Name, Address, SIN Number) of the applicant.

Section asking if you want prior tax years adjusted from the date of DTC approval.

Authorization for the medical practitioner to release medical information.

Part B- Filled out by a Medical Professional

A medical doctor or nurse practitioner can fill out all disability sections on the form.

If the impairment is specific (ie. vision, speech, etc) there is an option of having a specialist fill out the forms.

Ex. Optometrists can fill out the vision impairment section of the form

Once the form is complete, it will need to be sent to the Canada Revenue Agency (CRA) for review. They may request more medical information, and supporting documents prior to making a decision.

2. Must meet the age requirements, or be a guardian of the recipient.

Once qualified for the DTC, an RDSP can be opened through a financial institution as long as the beneficiary is age 18 or older and has a Social Insurance Number (SIN).

If the beneficiary is under age 18, a parent, guardian, or legal representative can open the account on their behalf. The parent or guardian will be the account holder until the beneficiary turns 18. At which point the account can be transferred to the beneficiary. If the beneficiary lacks the mental capacity to manage the account, the parent or guardian can continue to control it after age 18.

An RDSP must be opened before the beneficiary is age 60. However, the eligibility for benefits (ie. grants, and bonds) stops after age 49.

Contributions and Limits

The RDSP has a lifetime contribution limit of $200,000. However, there is no annual limit.

An RDSP is limited to one account per beneficiary. However, contributions can be made by many people (more just the account holder(. While only the account holder can open and manage an RDSP, friends and family can contribute to it as well. They’ll need written permission, which usually takes the form of a signed authorization or letter handled through the financial institution that manages the RDSP.

Government Support: Grants and Bonds

The feature that makes the RDSP stand out amongst other registered accounts is the access to government support via grants and bonds. These include the Canada Disability Savings Grant (CDSG), and Canada Disability Savings Bond (CDSB). These government supports can significantly enhance the long term returns of the account by increasing your contributions.

1.Canadian Disability Savings Grant (CDSG)

The Canadian government will match any contributions to an RDSP up to an annual maximum of $3,500 and a lifetime maximum of $70,000.

The rate of matching depends on the beneficiaries net family income:

<$114,750 of net family income

3:1 on the first $500 of yearly contributions

2:1 on the next $1,000

>$114,750 of net family income

1:1 on the first $1,000 of yearly contributions

In the case that the individual is under age 18, qualification will be calculated based on the net income of the parents/guardians. After this point, it will be based on the net income of the account beneficiary.

Example: Imagine your net family income is $95,000 and you contribute $1,500 per year to your son’s RDSP. The government will provide you with an additional $3,500 in CDSG, up to a lifetime maximum of $70,000. This is a 233% return on investment from contributing to the account alone.

Carry-forward rule

The carry-forward rule allows you to receive unused grants for up to 10 prior years. In order to be eligible to receive these grants, you would need to have had DTC status during all of the catch up years. Also, you will need to make the necessary contributions from all of those prior years.

There are a two common scenarios where this may occur:

You had DTC status, but didn’t know about the RDSP, or didn’t take advantage of the account benefits.

You just received DTC status for the current year, and previous years were recognized.

Ex. Imagine you had DTC status from 2015-2025. During which time your net family income was below the $114,750 threshold (adjusted for inflation). However, you didn’t open an RDSP until 2025. You are now eligible to receive all of the grants from that 10 year period. If you were able to do so, you could make $15,000 of contributions ($1,500 x 10 years). In return, you should receive $35,000 ($3,500 x 10 years) in CDSG. In 2026, you would be eligible to contribute an additional $1,500, and receive $3,500 in CDSG.

Investment Power of the CESG

The personal finance industry spends most of their energy discussing the subjects of savings, and cost-cutting. This is important because you can’t start to improve your financial position until you remove the proverbial 400lbs weight that looms over your head (ie. debt). However, savings and cost cutting are also important because we realize the impact that maximizing early contributions makes on your long term investment returns.

Early on, the impact of compound interest is minimal. But as your account grows, the power of compound interest is unbelievable. The CESG is such a powerful tool because it boosts your contributions. It provides fuel to the fire. A combination of your own contributions, and CESG raises the RDSP account balance closer to the point that compound interest starts to do its magic.

Ex. Jennifer has twin sons John and Jim that are both 10 years old.

John has a speech impediment and is eligible for the DTC, and RDSP.

Jim doesn’t have any disabilities.

Jennifer makes <$114,750. However, she is a good saver, and has $5,000/year to save for both of her son’s futures. She decides she will allocate $2,500/year for each son. She opens two accounts a TFSA for Jim (*), and an RDSP for John. In both accounts she decides to invest in a low cost index ETF which produces a long term average return of 7% /year. By age 50 the account balances should be the following:

Jim (TFSA, No CESG)- $535,753

John (RDSP, CESG)- $2,705,125

The CESG isn’t looking too bad now is it…

(*) Note that Jennifer will have to open a personal TFSA until Jim is age 18. Then he can open a TFSA of his own. The TFSA was used in this example to minimize the tax complexity of a taxable account.

2.Canadian Disability Savings Bond (CDSB)

In conjunction with the CDSG, there is also another benefit known as the Canadian Disability Savings Bond (CDSB). Like the CDSG, this bond is provided to individuals that have qualified for, and opened an RDSP. However, in order to be eligible for the CDSB you must have an individual or family net income <$57,375/year.

In the case that the individual is under age 18, qualification will be calculated based on the net income of the parents/guardians. After this point, it will be based on the net income of the account beneficiary.

Provided you meet this criteria, you may be eligible to receive up to $1,000 of CDSB annually, up to a lifetime maximum of $20,000. What’s even more enticing about this program is that you do not even need to make any contributions in order to receive these funds. This is free money.

However, the program unfortunately has additional income thresholds that impact how much of the $1,000 you are eligible for:

Annual income below $34,487 = Full $1,000 of CDSB

Annual income between $34,487 - $57,375 = <100% of CDSB

Carry-forward rule

Like the CDSG, RDSP holders are eligible to carry forward up to 10 years of CDSB entitlements. The maximum CDSB you can receive in a single year is $11,000. This consists of $1,000 of current year CDSB, and up to $10,000 of prior years CDSB.

In order to qualify, you must have had DTC status, and would have been a Canadian resident throughout this time period. You will not be required to fill out any form. Instead, the system automatically calculates and applies the prior years CDSB when you open an RDSP or make contributions, as long as eligibility requirements are met.

Ex. Imagine you received DTC status in 2015. Throughout this period your net family income has been below the $34,487 threshold. However, you didn’t open a RDSP until 2024. You would be eligible to receive all of the bonds over that 10 year period. In other words, you could theoretically contribute $0, and get $10,000 in CDSB deposited in your RDSP in year 1.

Age Limit

The beneficiary is eligible to receive grants and bonds until December 31st of the year they turn age 49. They can continue to make further contributions to the account until age 59. However, those contributions will not be eligible for government top-ups.

Please note that you could still be eligible to receive carry forward grants and bonds from prior years though, provided you meet the eligibility requirements.

The RDSP is intended as a long term savings tool in order to ensure retirement security for those with disabilities, not a short term assistance vehicle. By reducing the eligibility to age 49, it directs the focus on building savings earlier in life, giving funds more time to grow through compounding.

Investing Inside an RDSP

Like other tax-advantaged accounts (RRSP, TFSA, RESP) the RDSP funds (ie. contributions & grants/bonds) can be invested in a variety of financial products. These include:

Stocks, Bonds, GICs

ETFs, Mutual funds, REITs

High-interest savings accounts

Many financial institutions offer RDSPs, but the ability to self-manage investments may vary.

Investment Strategy

The investment approach utilized for this account will significantly depend on your personal situation. However, you should consider your risk tolerance and investment timeline.

Historically, during most rolling 10-year time periods, stocks have outperformed fixed income assets (ie. bonds and GIC’s). The mandatory withdrawal age for the RDSP is 60. This suggests that if you are 50 years old or younger, historically, stocks should provide you with a larger nest egg in retirement. On shorter timeframes, the risk adjusted return for stocks decreases. This suggests a move towards more fixed income assets may prove “safer”.

As with all investment decisions, there’s inherent risk. As the classic disclaimer goes…past results are not indicative of future returns.

Tax Treatment of RDSPs

All account types have different forms of taxation that you should consider. The RDSP is no different. The following is a break down of how the account is taxed at each stage of the process:

Contributions

Any contributions to an RDSP are not tax-deductible. Instead they act like a TFSA whereby you contribute after tax dollars.

Holding Period

Any investment growth within the RDSP (e.g., interest, dividends, capital gains) is not taxable in the year they are earned. Instead it is a tax-deferred account which means no taxes are paid on growth until withdrawal.

Withdrawal

At withdrawal the funds are broken down into two distinct parts:

Contributions

Not taxable upon withdrawal.

Remember these funds were contributed using after tax dollars (see above).

Government Bonds, Grants, and Investment Gains

Subjected to taxation at the time of withdrawal.

All withdrawals from this portion will be added to an individuals earned income, and taxed at their marginal tax rate.

Withdrawal Options

RDSP withdrawals can occur at any time. However, there are specific rules depending on the beneficiary's age, and the account balance at the time of withdrawal. Generally, withdrawals are categorized into two types:

Lifetime Disability Assistance Payments (LDAP)

Disability Assistance Payments (DAP)

Lifetime Disability Assistance Payments (LDAP)

Lifetime Disability Assistance Payments (LDAP) are recurring payments to the beneficiary, using funds from their RDSP. This is similar to a RRIF for the RRSP. These payments are made up of a portion of all three components of the account: personal contributions, government contributions (CDSG or CDSB), and investment growth.

LDAPs must begin by the end of the year, when the beneficiary turns 60 years old. Once they start, they continue for the beneficiary’s lifetime. There is a complex calculation to identify the amount of those payments. However, they are calculated according to two factors:

Your account balance at the time of initiating the LDAP

Your projected life expectancy.

The following online calculator here can help you estimate your expected LDAP payments according to your planned withdrawal age.

Disability Assistance Payments (DAP)

A Disability Assistance Payment (DAP) is a one-time withdrawal that can be made at any time throughout the beneficiaries lifetime. There is no maximum for the amount that can be withdrawn during a DAP.

A DAP is intended for scenarios whereby the funds are needed to deal with financial burdens (ex. medical bills). However, there are consequences to early withdrawal…most notably what is known as The 10-Year Rule.

The 10-Year Rule: Understanding the Catch

The 10-Year Rules states that if you withdraw from the RDSP within 10 years of receiving any Canada Disability Savings Grant (CDSG) or Canada Disability Savings Bond (CDSB), you will have to repay a portion of those grants and bonds to the government. This rule is in place to encourage long-term saving, and avoid short term profiting of grants/bonds.

For every $1 withdrawn, the beneficiary will have to payback $3 of CESG and/or CESB received in the last 10 years. This is referred to as the assistance holdback amount. You personally will not have to repay the amount. Instead the RDSP provider (ie. your bank) will withhold the funds by sending them directly back to the government.

For example, imagine Sarah opened an RDSP in 2015. She contributed the maximum of $1,500 annually, and received $3,500 in CESG for the last 10 years (ie. 2015-2024). Sarah wasn’t an avid reader of the nextgenfinance Canada blog, and she didn’t invest the funds. Instead, they sat in an account collecting no interest. Now in 2025, she has an account balance of $50,000. Of which $35,000 is grants ($3,500 x 10 years). The additional $15,000 is personal contributions. However, she decides to make a withdrawal of $5,000 from the account to pay for a treatment. The 10-year rule states that she will now be required to repay $15,000 in CESG ($5,000 x 3). However, if she waited until 2035 (10 years later) to withdraw the same $5,000 she would not be obligated to repay any of the CESG.

Key takeaway: In practice, withdrawing funds so soon after receiving grants is very costly, since it triggers a much larger clawback. That’s why the RDSP is usually most beneficial if left untouched until grants have “aged out” (10 years after deposit).

Special Rules for Shortened Life Expectancy

There are special rules that apply in circumstances where the beneficiary is deemed to have a short life expectancy. A short life expectancy is considered five years or less. This exception allows the beneficiary to be able to access their funds without being subjected to the typical penalties of early withdrawal. For this to occur, the RDSP has to first be designated as a Specified Disability Savings Plan (SDSP).

In order for the RDSP to be designated as a SDSP the following steps will need to occur:

Obtain written medical documentation from a physician stating the individual has a life expectancy of five years or less.

The account holder (beneficiary or parent/guardian) will submit the document to their financial institution.

They will concurrently request for the account to be switched from an RDSP to a SDSP.

Once the RDSP becomes an SDSP:

No new contributions can be made to the account.

The beneficiary will not receive any additional grants or bonds.

Withdrawals are still taxed. However, like an RDSP, this only applies to the portion that comes from government contributions and investment growth.

While the RDSP is designated as an SDSP, there are limits on how much can be withdrawn annually:

The beneficiary can withdraw up to $10,000 per year without requiring the repayment of any Canada Disability Savings Grants (CDSG) or Bonds (CDSB).

If the beneficiary needs to withdraw more than $10,000, the 10-year repayment rule will apply, and government contributions from the last 10 years must be repaid.

In other words, by switching from the RDSP to the SDSP the beneficiary can make $10,000 of taxable withdrawals annually without the penalties they would typically be subjected to if the account remained an RDSP.

If the beneficiary’s condition improves and they are no longer considered to have a shortened life expectancy, the SDSP status can be revoked, and the RDSP will revert to its original form. This allows the plan to continue receiving contributions and government grants or bonds.

Transferring Other Accounts Into an RDSP

Converting an RESP to an RDSP

If there is an existing RESP (Registered Education Savings Plan) for the beneficiary, and they have developed a disability that reduces their ability to attend higher education, you can convert the RESP to an RDSP. This ensures that the funds continue to support the individual.

In order to transfer the funds the individual must first meet the eligibility criteria for the RDSP and be receiving the Disability Tax Credit (DTC). Once this is confirmed the following steps must occur:

Open an RDSP Account for the beneficiary

Fill out Form RC435 with your financial institution. This allows the funds to be rolled over from the RESP to an RDSP.

Close the RESP (Must be completed by the following February)

Once this is completed:

No more contributions can be made to the RESP

All government grants and bonds must be repaid to the government. This includes the CESG (Canadian Education Savings Grant) and CESB (Canadian Education Savings Bond).

All contributions to the RESP, and investment returns on those contributions (AIP) will be transferred to the RDSP and count towards your $200,000 lifetime contribution limit.

All funds transferred will not be eligible for matching grants or bonds. Also, they will be considered part of the taxable portion upon withdrawal.

Transferring Funds from a Parent/Grandparent's (RRSP, RRIF, RPP, or PRPP to an RDSP)

There are special rules for cases whereby a parent or grandparent, that financially supported the beneficiary, is deceased. In these instances, funds from their retirement accounts (RRSP, RRIF, RPP, or SPP) can be transferred to the beneficiaries RDSP. This option provides a unique way to ensure financial security for a child with a disability, while also taking advantage of the tax benefits provided by the RDSP.

Below is an overview of how this process works:

Beneficiary must qualify for the RDSP (ie. DTC status, be under the age of 59 years old.), and will have opened an account with a financial institution.

Fill out Form RC4625 with your financial institution which allows the funds to be rolled over from a variety of different pension and retirement savings plans to an RDSP.

The transfer typically happens as part of the estate settlement process upon the death of the account holder.

Close the RRSP, RRIF, RPP, or SPP

The funds are rolled over without any tax consequences in the year the rollover occurs.

The maximum transferable funds is $200,000 - Any previous contributions.

All funds transferred will not be eligible for matching grants or bonds.

They will be considered part of the taxable portion upon withdrawal.

Ex. Imagine you have already contributed $50,000 to an RDSP. Your grandfather passes away, and he would like $250,000 from his RRSP to be willed to you. In this case only $150,000 can be transferred to your RDSP. The additional $100,000 will have to be added to his final tax return, while settling the estate. The net remaining amount will then be distributed to you. At which point you can invest it in a variety of different accounts (RRSP, TFSA, Taxable Account). However, it can not be contributed to the RDSP, because the account contributions are already maximized.

What Happens If You Lose DTC Status?

A criteria for the DTC is that the individual may be required to undergo periodic re-evaluations. The frequency of these evaluations depends on the medical condition.

Permanent conditions (ex. Blindness)

May involve the CRA approving the DTC with no expiry date.

In which case no re-evaluation will occur.

Conditions that are expected to improve (ex. Physical Injuries)

CRA may grant approval for a shorter period of time, often 2-5 years.

Re-evaluation of eligibility will occur, and they may need a new T2201 Disability Tax Credit Certificate from a doctor.

In some cases, upon re-evaluation you may lose your DTC status. When this occurs you will not be able to make any further contributions to the RDSP, and you will not receive any further grants or bonds.

Changes to Loss of DTC

Prior to 2014, if you lost DTC status you were required to close your RDSP and repay all government grants/bonds obtained within the last 10 years. However, these rules were relaxed.

Now, even if you lose DTC eligibility, you are no longer required to close your RDSP immediately. Instead you have a five year “grace period” whereby the account can remain open. This is intended for circumstances whereby you expect to re-qualify again in the future. During this time, you will not be able to make further contributions or receive additional grants/bonds. However, your investments can continue to grow tax-deferred, and you will not be required to repay any grants/bonds that you have previously received.

Conclusion

The RDSP stands out as an unmatched tool for building financial security for Canadians with disabilities. With up to $90,000 available in government grants and bonds, plus the power of tax-deferred growth, it provides opportunities that no other registered account can match. While the application process may seem daunting at first, the long-term benefits far outweigh the initial complexity. If you or a loved one qualifies for the Disability Tax Credit, don’t wait. The earlier you open an RDSP, the greater the impact compounding and government support can have.

If you like this post you may also like:

[Old Age Security (OAS) in Canada 2025: Eligibility, Payments, and Clawback Explained]

[Complete Guide to Canada Pension Plan (CPP) 2025: Maximize Your Benefits & Contributions]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Canada Revenue Agency. (2023). Disability Tax Credit (DTC). Government of Canada. https://www.canada.ca/en/revenue-agency/services/tax/individuals/segments/tax-credits-deductions-persons-disabilities/disability-tax-credit.html

Canada Revenue Agency. (2023). Form RC435: Rollover from a Registered Education Savings Plan to a Registered Disability Savings Plan. Government of Canada. https://www.canada.ca/en/revenue-agency/services/forms-publications/forms/rc435.html

Canada Revenue Agency. (2023). Form RC4625: Rollover to a Registered Disability Savings Plan (RDSP) under Paragraph 60(l). Government of Canada. https://www.canada.ca/en/revenue-agency/services/forms-publications/forms/rc4625.html

Canada Revenue Agency. (2023d). Registered Disability Savings Plan (RDSP). Government of Canada. https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/registered-disability-savings-plan-rdsp.html

Employment and Social Development Canada. (2022). Canada Disability Savings Grant and Canada Disability Savings Bond. Government of Canada. https://www.canada.ca/en/employment-social-development/programs/disability/savings/eligibility.html

RBC Wealth Management. (2023). An In-Depth Look at RDSPs. https://ca.rbcwealthmanagement.com/documents/266841/1274778/An+In-Depth+Look+at+RDSPs.pdf/5d31aa7f-4e5c-4909-99e6-7134abc38c6b

Scotiabank. (2023). A Guide to the Registered Disability Savings Plan (RDSP). Scotiabank. https://www.scotiabank.com/ca/en/personal/investing/registered-disability-savings-plan.html

TD Wealth. (2023). Registered Disability Savings Plan (RDSP) Explained. TD Bank. https://www.td.com/ca/en/investing/registered-disability-savings-plan/

The Team Ability No Excuses Podcast. (2020). Episode 31: What the heck is an RDSP? [Audio podcast]. https://teamabilitypodcast.libsyn.com/episode-31-what-the-heck-is-an-rdsp

Watt, J. (Host). (2021). RDSP specialist [Audio podcast episode]. CE Drive with Jason Watt. Buzzsprout. https://www.buzzsprout.com/1593283/episodes/7978919-rdsp-specialist

Plan Institute. (n.d.). RDSP calculator. Retrieved September 13, 2025, from https://www.rdsp.com/calculator/