Get our free Debt vs Invest Calculator — click here to access it

FHSA Canada Guide: How It Works for First-Time Home Buyers

Learn how the First Home Savings Account works in Canada. Tax benefits, contribution limits, and withdrawal rules for first-time home buyers.

FHSAFIRST HOME SAVINGS ACCOUNT

4/5/202519 min read

Introduction

This Olympic tournament is almost at its conclusion, the gold medal has been given to the TFSA, the silver to the RRSP. Historically the bronze medal has always been given to the Registered Education Savings Plan (RESP). This is the answer we would have given, pre-2023. However, after several hours of deliberation, we have reversed that decision. Post 2023, we will now be giving the bronze medal to… the FHSA.

What Is the First Home Savings Account (FHSA)?

The FHSA stands for the First Home Savings Account. Not to be confused with the Home Buyers Plan (HBP). The HBP is a program available for first time home buyers to use funds from their RRSP for home purchase. That program will be discussed in detail during our next blog post.

The FHSA is a registered account that was created on April 1st, 2023. After months of rumors, the Liberal party in the Federal Government introduced the account as a supplementary method for Canadians to save for their first home. The account was created to address the issues young Canadians have had with regards to home affordability.

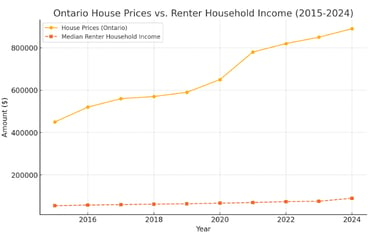

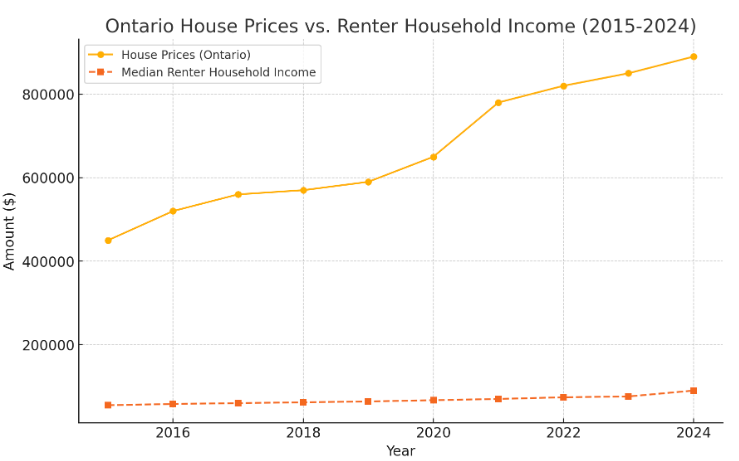

According to wowa.ca, as of January 2025, the average house price in Ontario has grown to $834,050. Meanwhile, data from the CMHC shows that the average household income for renters in Ontario was only $76,100 in 2022. Even if we were to be generous, and say household incomes for renters have risen to $90,000 as of 2025. This would still mean that the current house cost is almost 10x household income. Consequently, many young Canadians have had significant difficulty getting into the housing market in recent years.

Who Can Open A FHSA?

In order to be able to open an FHSA account, three conditions need to be met. These are:

You need to be a Canadian resident (not to be confused with a Canadian Citizen)

You need to be at least 18 years of age or older

You have to be a first time home buyer*

However, there is an exception to the last rule. There is actually a circumstance whereby you can use the account, despite being a previous home owner. The Government of Canada considers you eligible for this account, if you or a spouse/common law partner, did not own a home for 4 years. After 4 years, then you are eligible to start contributing to a FHSA.

For Example: Michael, a manager at a bank, got transferred from Ottawa to Toronto in February 2021. He sold his house in Ottawa but decided to rent a townhouse in Toronto. As of February 2025, he would be eligible to start contributing to a FHSA. He now falls within the guidelines of a first time home buyer under this program.

This account can stay open for a maximum of 15 years or until the end of the year you turn 71 (whichever comes first).

The Benefits of an FHSA – Why It’s the Best of a TFSA & RRSP

I tell people who ask, that the FHSA is the amazing love child of the TFSA and RRSP. It takes the best of both worlds, and combines them together to create an amazing account. The FHSA has a maximum contribution limit of $8,000 per year, up to a lifetime limit of $40,000. The contributions you make to a FHSA are tax deductible like an RRSP. However, the withdrawals are also tax free like a TFSA. That is provided that the withdrawals are used for the purchase of a home.

For example: Let's imagine your taxable income in 2024 was $60,000, and you plan to purchase a house in December. If you contribute the maximum of $8,000 to an FHSA:

The $8000 will be deducted from your taxable income bringing it down to $52,000 for 2024.

You can then turn around, and use the $8,000 on your first home purchase without triggering a tax event.

Similar to the TFSA, the FHSA suffers from poor marketing. Due to the naming of the account, it is mistakenly viewed as a traditional savings account. However, you can use the account to invest in a wide range of different products including:

Guaranteed Interest Certificates (GIC’s),

Exchange Traded Funds (ETF’s)

Stocks

Bonds

Or Mutual Funds.

All growth in the account via interest, capital gains, and dividends are tax-free like a TFSA. This means that despite a total contribution limit of $40,000, the account can grow substantially beyond this amount by the time you decide to purchase a home.

For example: Let's imagine you were 18 years of age in 2023 when the account opened, and you contributed $8,000 to the account. You decided to do this for the next four years (ie. 2024. 2025, 2026, 2027). However, you don’t plan on purchasing your first house until you are 30 years old. So instead you invest all the money into an S&P 500 index ETF that yields ~7%/ year. Over that time period your money grows to a whopping $80,000, which you can use towards your first home purchase.

FHSA Contribution Rules & Limits

Unlike the TFSA, contribution room does not start accumulating when you turn 18 years old. Instead you are required to open an account in order for contribution room to start accumulating. In the first year you can contribute $8,000. You can also carry forward $8,000 into the next calendar year.

For example: Imagine John opened a FHSA in 2024 but didn’t have any funds to contribute. However, he received a very good bonus of $16,000 at the end of the year. As of January 2025, he is now able to contribute the entire $16,000 into his FHSA. This is because he has the $8,000 of contribution room from 2024, and an additional $8,000 from 2025.

However, you can not carry forward anymore then $8,000. In other words, you can’t just open the account, wait 5 years and contribute $40,000.

Combining Programs

Another major benefit is that this account can be combined with a partner’s FHSA to purchase the same home. So a total of $80,000 of contribution room can be used towards your first house. Note that as per a previous example, with smart investing decisions this $80,000 of contribution room could grow to substantially more money.

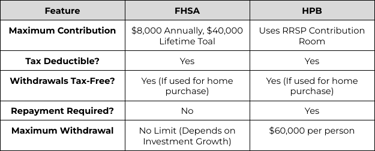

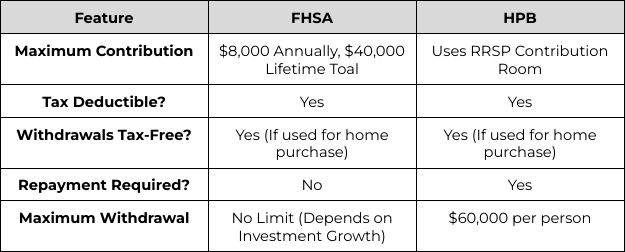

Also, the FHSA can be combined with the Home Buyers Plan which has a maximum withdrawal amount of $60,000 per person, or $120,000 for a couple.

So, based solely on contribution alone, not factoring in the potential growth of your FHSA and RRSP, the two plans can be combined for a total of $200,000 towards your first home as a couple in Canada.

FHSA vs Home Buyer’s Plan (HBP) – Key Differences

Although both of these programs can be combined to purchase a house, it is important to understand the differences between them:

The main differences are these:

Repayment Requirements

HBP- Any money withdrawn from the RRSP for the HPB must be repaid within 15 years after withdrawal. You must start repayment at least five years after withdrawal.

FHSA- The money withdrawn from the FHSA for the purchase of your first home does not have to be repaid.

Maximum Contribution/Withdrawal

HBP- The maximum withdrawal amount is $60,000 per person, or $120,000 for a couple. You can’t withdraw any more than this for the purchase of a home without triggering a tax event.

FHSA- The FHSA only sets a contribution limit of $40,000 per person. Provided smart investing decisions, and opening the account early, the amount you may be able to withdraw for your home purchase could be substantially higher.

What Happens If You Don’t Buy a Home?

In the case that you contribute to the FHSA, but do not purchase a home within the 15 year time limit, what do you do?

At this point, the money contributed to the account gets treated like an RRSP. That means you have two options:

Option 1: You can withdraw the funds.

In which case the funds you withdraw will be added to your taxable income in that year.

For example: Jeff opened an FHSA when he turned 18 years of age, and contributed $40,000 to his FHSA in the first five years. Due to life circumstances, Jeff decides he would like to continue renting, and never purchases a house. In his 30’s, Jeff is a teacher making $90,000/year. At 33 years old he decides to withdraw the money from his FHSA to spend on a new car. Without realizing, Jeff accidentally increased his taxable income to $130,000 ($90k salary plus $40k from his FHSA) by withdrawing the money.

Option 2: The funds can be transferred to an RRSP.

In which case, the money can continue to grow tax-free until you decide to withdraw the funds in retirement. It will be taxed upon withdrawal in retirement. According to current rules this additional amount does not impact your RRSP contribution limit.

Drawbacks to the FHSA

As we have mentioned, the FHSA is an amazing option for young Canadians looking to buy a house within the next 15 years. The younger you are when you open an account, and max out the contributions the better. Also, if you make intelligent investing decisions the account can be even more beneficial. However, like with all things in life (and all accounts) there are some drawbacks:

Cost of Living Crisis

The big question is, do young Canadians even have another $8,000 annually of savings to contribute to a program like the FHSA? According to Stats Canada the average Canadian household savings rate in 2024 was approximately 6%. Based on this figure a couple would need a household income of $267,000 (or $133,500 for an individual) in order to maximize this account.

Canadians also already had access to the Home Buyer’s Plan before this program was even rolled out. Unsurprisingly, it didn’t address the housing crisis. So, what makes us think that an additional $80,000 of potential contribution room for a couple is going to help?

Negatively Impacts Single People

If you decide to purchase a house as a single person, this account provides less potential upside relative to a couple. A total of $40,000 provides minimal benefit considering the current average price of a house in Ontario is over $800,000. The minimum down payment on a $800,000 property is actually $55,000. Assuming a 4% fixed interest rate (ie. average rate at time of this post) that would yield you a whopping $4,075 monthly mortgage payment... nevermind other household expenses.

It doesn’t accurately address home affordability.

House prices have become unaffordable for many young Canadians. The primary reason for this is due to a lack of supply of homes. Data by CMHC compared 2024 housing starts (ie. new houses) with population growth. It showed that despite a growth in housing construction of 4% compared to 2023, it was still insufficient to meet demand. In other words, home builders aren’t building homes fast enough relative to the amount of people in Canada that want one.

This account tries to address this issue by giving Canadians another savings engine. Unfortunately, it is likely only going to increase demand. However, it won’t address the current supply issue. More people will have the required down payment, which means more people will want homes, and on paper be able to afford those homes. However, this may just drive up home prices further until the supply issue is addressed.

What about current homeowners?

Don’t get me wrong, it would be the wild west (and basically useless) if current homeowners got access to these accounts. They would try to use the money to buy other properties, further worsening the current problem. But, it would be nice to give current homeowners access to this account to use for any current home expenses.

The second most painful experience you will ever have when it comes to a home (other than buying one), is actually owning one. The amount of expenses that come up after buying a home would make your head spin (twice!). For example, a current homeowner could have used this account to pay for a roof repair, broken HVAC system, or some other home improvement/quality of life expenses.

For those that might be slightly annoyed by this, don’t forget that those first time home buyers may one day also need to have money to complete these repairs (assuming they didn’t use it all purchasing their first home).

Conclusion

With this, we conclude our Olympics tournament. The First Home Savings Account (FHSA) is a great tool for Canadians looking to save for their first home. The FHSA, having both tax-deductible contributions and tax-free withdrawals for home purchases, gives Canadians looking to buy their first home the best of both worlds. Whether you're just starting to save, or looking to make the most of your home-buying journey, the FHSA takes you one step closer to your first ever home. We hope that after reading this post you feel more knowledgeable and comfortable using this account. So, take advantage of this opportunity and start saving smartly today!

Related Posts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

Canada Mortgage and Housing Corporation. (n.d.). Real average total household income before taxes. Canada Mortgage and Housing Corporation. Retrieved July 5, 2024, from https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/housing-data/data-tables/household-characteristics/real-average-total-household-income-before-taxes

Canada Mortgage and Housing Corporation. (n.d.). Mortgage calculator. Canada Mortgage and Housing Corporation. Retrieved from https://www.cmhc-schl.gc.ca/consumers/home-buying/calculators/mortgage-calculator

Canada Mortgage and Housing Corporation. (n.d.). Housing supply report. Canada Mortgage and Housing Corporation. Retrieved from https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/market-reports/housing-market/housing-supply-report

Government of Canada. (n.d.). First Home Savings Account (FHSA). Canada Revenue Agency. Retrieved from https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account.html

TD. (n.d.). Home Buyers’ Plan (HBP). TD Direct Investing. Retrieved February 15, 2025, from https://www.td.com/ca/en/investing/direct-investing/articles/home-buyers-plan

U.S. Securities and Exchange Commission. (n.d.). Compound interest calculator. U.S. Securities and Exchange Commission. Retrieved February 15, 2025, from https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator

WOWA. (n.d.). Ontario housing market. WOWA. Retrieved from https://wowa.ca/ontario-housing-market

Trading Economics. (n.d.). Canada personal savings. Retrieved from https://tradingeconomics.com/canada/personal-savings

Ratehub. (n.d.). Mortgage rates in Ottawa. Retrieved from https://www.ratehub.ca/mortgage-rates-ottawa

Introduction

This Olympic tournament is almost at its conclusion, the gold medal has been given to the TFSA, the silver to the RRSP. Historically the bronze medal has always been given to the Registered Education Savings Plan (RESP). This is the answer we would have given, pre-2023. However, after several hours of deliberation, we have reversed that decision. Post 2023, we will now be giving the bronze medal to… the FHSA.

What Is the First Home Savings Account (FHSA)?

The FHSA stands for the First Home Savings Account. Not to be confused with the Home Buyers Plan (HBP). The HBP is a program available for first time home buyers to use funds from their RRSP for home purchase. That program will be discussed in detail during our next blog post.

The FHSA is a registered account that was created on April 1st, 2023. After months of rumors, the Liberal party in the Federal Government introduced the account as a supplementary method for Canadians to save for their first home. The account was created to address the issues young Canadians have had with regards to home affordability.

According to wowa.ca, as of January 2025, the average house price in Ontario has grown to $834,050. Meanwhile, data from the CMHC shows that the average household income for renters in Ontario was only $76,100 in 2022. Even if we were to be generous, and say household incomes for renters have risen to $90,000 as of 2025. This would still mean that the current house cost is almost 10x household income. Consequently, many young Canadians have had significant difficulty getting into the housing market in recent years.

Who Can Open A FHSA?

In order to be able to open an FHSA account, three conditions need to be met. These are:

You need to be a Canadian resident (not to be confused with a Canadian Citizen)

You need to be at least 18 years of age or older

You have to be a first time home buyer*

However, there is an exception to the last rule. There is actually a circumstance whereby you can use the account, despite being a previous home owner. The Government of Canada considers you eligible for this account, if you or a spouse/common law partner, did not own a home for 4 years. After 4 years, then you are eligible to start contributing to a FHSA.

For Example: Michael, a manager at a bank, got transferred from Ottawa to Toronto in February 2021. He sold his house in Ottawa but decided to rent a townhouse in Toronto. As of February 2025, he would be eligible to start contributing to a FHSA. He now falls within the guidelines of a first time home buyer under this program.

This account can stay open for a maximum of 15 years or until the end of the year you turn 71 (whichever comes first).

The Benefits of an FHSA – Why It’s the Best of a TFSA & RRSP

I tell people who ask, that the FHSA is the amazing love child of the TFSA and RRSP. It takes the best of both worlds, and combines them together to create an amazing account. The FHSA has a maximum contribution limit of $8,000 per year, up to a lifetime limit of $40,000. The contributions you make to a FHSA are tax deductible like an RRSP. However, the withdrawals are also tax free like a TFSA. That is provided that the withdrawals are used for the purchase of a home.

For example: Let's imagine your taxable income in 2024 was $60,000, and you plan to purchase a house in December. If you contribute the maximum of $8,000 to an FHSA:

The $8000 will be deducted from your taxable income bringing it down to $52,000 for 2024.

You can then turn around, and use the $8,000 on your first home purchase without triggering a tax event.

Similar to the TFSA, the FHSA suffers from poor marketing. Due to the naming of the account, it is mistakenly viewed as a traditional savings account. However, you can use the account to invest in a wide range of different products including:

Guaranteed Interest Certificates (GIC’s),

Exchange Traded Funds (ETF’s)

Stocks

Bonds

Or Mutual Funds.

All growth in the account via interest, capital gains, and dividends are tax-free like a TFSA. This means that despite a total contribution limit of $40,000, the account can grow substantially beyond this amount by the time you decide to purchase a home.

For example: Let's imagine you were 18 years of age in 2023 when the account opened, and you contributed $8,000 to the account. You decided to do this for the next four years (ie. 2024. 2025, 2026, 2027). However, you don’t plan on purchasing your first house until you are 30 years old. So instead you invest all the money into an S&P 500 index ETF that yields ~7%/ year. Over that time period your money grows to a whopping $80,000, which you can use towards your first home purchase.

FHSA Contribution Rules & Limits

Unlike the TFSA, contribution room does not start accumulating when you turn 18 years old. Instead you are required to open an account in order for contribution room to start accumulating. In the first year you can contribute $8,000. You can also carry forward $8,000 into the next calendar year.

For example: Imagine John opened a FHSA in 2024 but didn’t have any funds to contribute. However, he received a very good bonus of $16,000 at the end of the year. As of January 2025, he is now able to contribute the entire $16,000 into his FHSA. This is because he has the $8,000 of contribution room from 2024, and an additional $8,000 from 2025.

However, you can not carry forward anymore then $8,000. In other words, you can’t just open the account, wait 5 years and contribute $40,000.

Combining Programs

Another major benefit is that this account can be combined with a partner’s FHSA to purchase the same home. So a total of $80,000 of contribution room can be used towards your first house. Note that as per a previous example, with smart investing decisions this $80,000 of contribution room could grow to substantially more money.

Also, the FHSA can be combined with the Home Buyers Plan which has a maximum withdrawal amount of $60,000 per person, or $120,000 for a couple.

So, based solely on contribution alone, not factoring in the potential growth of your FHSA and RRSP, the two plans can be combined for a total of $200,000 towards your first home as a couple in Canada.

FHSA vs Home Buyer’s Plan (HBP) – Key Differences

Although both of these programs can be combined to purchase a house, it is important to understand the differences between them:

The main differences are these:

Repayment Requirements

HBP- Any money withdrawn from the RRSP for the HPB must be repaid within 15 years after withdrawal. You must start repayment at least five years after withdrawal.

FHSA- The money withdrawn from the FHSA for the purchase of your first home does not have to be repaid.

Maximum Contribution/Withdrawal

HBP- The maximum withdrawal amount is $60,000 per person, or $120,000 for a couple. You can’t withdraw any more than this for the purchase of a home without triggering a tax event.

FHSA- The FHSA only sets a contribution limit of $40,000 per person. Provided smart investing decisions, and opening the account early, the amount you may be able to withdraw for your home purchase could be substantially higher.

What Happens If You Don’t Buy a Home?

In the case that you contribute to the FHSA, but do not purchase a home within the 15 year time limit, what do you do?

At this point, the money contributed to the account gets treated like an RRSP. That means you have two options:

Option 1: You can withdraw the funds.

In which case the funds you withdraw will be added to your taxable income in that year.

For example: Jeff opened an FHSA when he turned 18 years of age, and contributed $40,000 to his FHSA in the first five years. Due to life circumstances, Jeff decides he would like to continue renting, and never purchases a house. In his 30’s, Jeff is a teacher making $90,000/year. At 33 years old he decides to withdraw the money from his FHSA to spend on a new car. Without realizing, Jeff accidentally increased his taxable income to $130,000 ($90k salary plus $40k from his FHSA) by withdrawing the money.

Option 2: The funds can be transferred to an RRSP.

In which case, the money can continue to grow tax-free until you decide to withdraw the funds in retirement. It will be taxed upon withdrawal in retirement. According to current rules this additional amount does not impact your RRSP contribution limit.

Drawbacks to the FHSA

As we have mentioned, the FHSA is an amazing option for young Canadians looking to buy a house within the next 15 years. The younger you are when you open an account, and max out the contributions the better. Also, if you make intelligent investing decisions the account can be even more beneficial. However, like with all things in life (and all accounts) there are some drawbacks:

Cost of Living Crisis

The big question is, do young Canadians even have another $8,000 annually of savings to contribute to a program like the FHSA? According to Stats Canada the average Canadian household savings rate in 2024 was approximately 6%. Based on this figure a couple would need a household income of $267,000 (or $133,500 for an individual) in order to maximize this account.

Canadians also already had access to the Home Buyer’s Plan before this program was even rolled out. Unsurprisingly, it didn’t address the housing crisis. So, what makes us think that an additional $80,000 of potential contribution room for a couple is going to help?

Negatively Impacts Single People

If you decide to purchase a house as a single person, this account provides less potential upside relative to a couple. A total of $40,000 provides minimal benefit considering the current average price of a house in Ontario is over $800,000. The minimum down payment on a $800,000 property is actually $55,000. Assuming a 4% fixed interest rate (ie. average rate at time of this post) that would yield you a whopping $4,075 monthly mortgage payment... nevermind other household expenses.

It doesn’t accurately address home affordability.

House prices have become unaffordable for many young Canadians. The primary reason for this is due to a lack of supply of homes. Data by CMHC compared 2024 housing starts (ie. new houses) with population growth. It showed that despite a growth in housing construction of 4% compared to 2023, it was still insufficient to meet demand. In other words, home builders aren’t building homes fast enough relative to the amount of people in Canada that want one.

This account tries to address this issue by giving Canadians another savings engine. Unfortunately, it is likely only going to increase demand. However, it won’t address the current supply issue. More people will have the required down payment, which means more people will want homes, and on paper be able to afford those homes. However, this may just drive up home prices further until the supply issue is addressed.

What about current homeowners?

Don’t get me wrong, it would be the wild west (and basically useless) if current homeowners got access to these accounts. They would try to use the money to buy other properties, further worsening the current problem. But, it would be nice to give current homeowners access to this account to use for any current home expenses.

The second most painful experience you will ever have when it comes to a home (other than buying one), is actually owning one. The amount of expenses that come up after buying a home would make your head spin (twice!). For example, a current homeowner could have used this account to pay for a roof repair, broken HVAC system, or some other home improvement/quality of life expenses.

For those that might be slightly annoyed by this, don’t forget that those first time home buyers may one day also need to have money to complete these repairs (assuming they didn’t use it all purchasing their first home).

Conclusion

With this, we conclude our Olympics tournament. The First Home Savings Account (FHSA) is a great tool for Canadians looking to save for their first home. The FHSA, having both tax-deductible contributions and tax-free withdrawals for home purchases, gives Canadians looking to buy their first home the best of both worlds. Whether you're just starting to save, or looking to make the most of your home-buying journey, the FHSA takes you one step closer to your first ever home. We hope that after reading this post you feel more knowledgeable and comfortable using this account. So, take advantage of this opportunity and start saving smartly today!

Related Posts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

Canada Mortgage and Housing Corporation. (n.d.). Real average total household income before taxes. Canada Mortgage and Housing Corporation. Retrieved July 5, 2024, from https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/housing-data/data-tables/household-characteristics/real-average-total-household-income-before-taxes

Canada Mortgage and Housing Corporation. (n.d.). Mortgage calculator. Canada Mortgage and Housing Corporation. Retrieved from https://www.cmhc-schl.gc.ca/consumers/home-buying/calculators/mortgage-calculator

Canada Mortgage and Housing Corporation. (n.d.). Housing supply report. Canada Mortgage and Housing Corporation. Retrieved from https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/market-reports/housing-market/housing-supply-report

Government of Canada. (n.d.). First Home Savings Account (FHSA). Canada Revenue Agency. Retrieved from https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account.html

TD. (n.d.). Home Buyers’ Plan (HBP). TD Direct Investing. Retrieved February 15, 2025, from https://www.td.com/ca/en/investing/direct-investing/articles/home-buyers-plan

U.S. Securities and Exchange Commission. (n.d.). Compound interest calculator. U.S. Securities and Exchange Commission. Retrieved February 15, 2025, from https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator

WOWA. (n.d.). Ontario housing market. WOWA. Retrieved from https://wowa.ca/ontario-housing-market

Trading Economics. (n.d.). Canada personal savings. Retrieved from https://tradingeconomics.com/canada/personal-savings

Ratehub. (n.d.). Mortgage rates in Ottawa. Retrieved from https://www.ratehub.ca/mortgage-rates-ottawa