Get our free Debt vs Invest Calculator — click here to access it

How Much Emergency Fund Do You Need in Canada (2025 Guide)

Learn how much emergency fund do you need in Canada and how to calculate it using EI benefits, average unemployment length, and your essential monthly expenses.

EMERGENCY FUNDFINANCIAL BASICS

10/13/202527 min read

Introduction

In our last post here we discussed the best options as of October 2025 for where to park your emergency fund. The next question becomes how much do you actually need in an emergency fund in order to feel secure? The right amount varies according to your level of income stability, whether or not you have dependents, and how long it will take you to replace your income if you ever become unemployed. This post is aimed at showing you how to calculate your ideal emergency fund amount. We will provide you with a step-by step process to help you identify your number using Canadian specific data.

Why an Emergency Fund Matters (Canadian Reality)

Many Canadians are just one unexpected bill away from financial stress. Recent surveys show that over one in four Canadians couldn’t afford a $500 emergency, and nearly half have no dedicated emergency savings at all. In fact, 46% of Canadians experienced a major unexpected expense last year, with most having to borrow or dip into other savings to cover the cost. This highlights just how crucial an emergency fund is for financial stability.

Purpose of an Emergency Fund

An emergency fund is meant to pay for unanticipated expenses and provide support during income gaps that may occur throughout your life. Situations that would be better managed with an emergency fund include:

Major car or house repair

Replacement of a furnace, water heater, or other appliance.

Medical emergency (Less of a concern in Canada due to the tax funded health care system).

Vet expenses

Legal fees

Income loss

Avoid Credit

In order to manage these types of situations, many Canadians rely on credit products. According to Statistics Canada, total household credit liabilities increased to $3.11 trillion as of July 2025. This is an increase of 3.15% from the prior year.

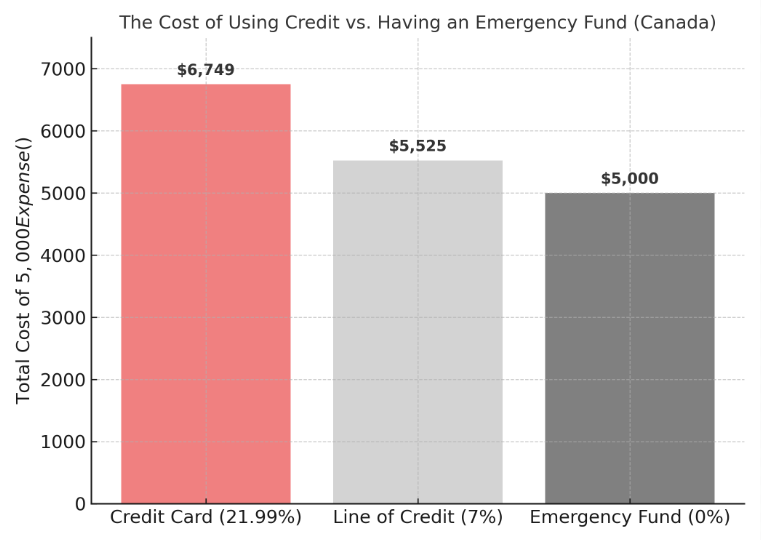

Not all credit is created equal. If you have access to a low interest line of credit (< 7%), this could be used to deal with emergencies. The interest costs are relatively low, making it manageable to pay off. Not optimal, but not terrible. Unfortunately, many don’t have this option. Add to this that lenders (ex. banks) are not open to giving you a low interest loan when you need it the most. They like to lend money to those they know have it, and are more likely to pay them back.

The consequence is that many people resort to high interest forms of debt such as credit cards, personal loans, and Buy Now, Pay Later (BNPL) services. Worse yet is that they gradually pay off these debts over time, letting interest compound, making their total purchase cost even higher. A report by the Bank Of Canada in 2024 showed that 46% of Canadians carry an outstanding balance on their credit cards. Of those individuals, 23% have a balance that is 80% or more of their borrowing limit.

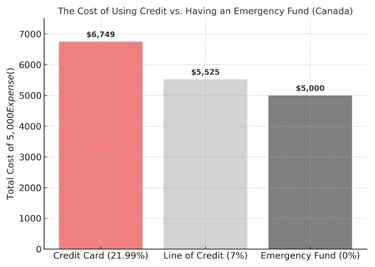

Ex. Your water heater tank breaks down, and the replacement cost is $5,000. Since you have no emergency fund, you have to pay for it with your credit card. The interest rate on the credit card is 21.99% (which is common). You, like most Canadians, don’t have a lot of money to spare after all your bills, so you decide to put the $5,000 on a credit card and pay $200/month. The result of this situation:

It will take you 2 years and 10 months to pay off the loan.

You will pay an additional $1,748.69 in interest.

The total cost of the water heater increases from $5,000 to $6,748.69.

If you repeat this with several expenses throughout your lifetime, the total impact on your ability to build wealth could be unbelievable. What doesn’t get calculated though is the impact on your mental health. All of these little expenses eat away at your budget, making you feel like you never have enough money to go around…no wonder why you are so stressed about money.

How Much Should You Keep in an Emergency Fund?

The “right amount” to have in an emergency fund depends on your situation. Fortunately, there are useful anchor points you can use to guide you.

Emergency fund = income gap buffer

At the beginning of this article, we discussed all of the reasons why an emergency fund was important. By far the most important of those reasons is to protect you when your income stops or decreases (job loss, illness, business slowdown). It acts as an income buffer so that you can continue paying your bills while you recover or pivot.

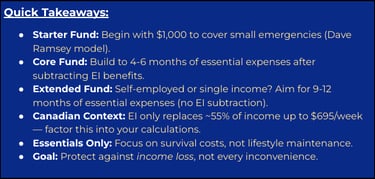

Layer 1: Micro Fund- Immediate Protection

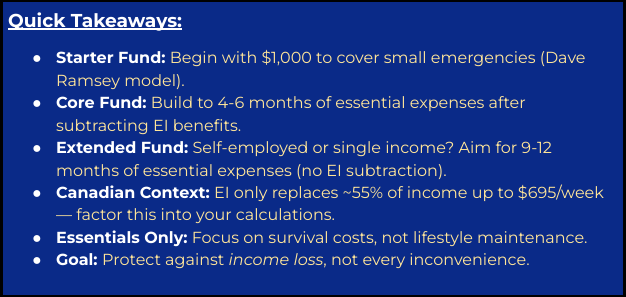

Financial Influencer Dave Ramsey famously recommends that before doing anything else, you should save a small emergency fund of $1,000 to cover any surprises. This acts as a mini buffer to prevent you from digging into credit when minor emergencies strike. It acts like a first line of defence.

This amount of money is not meant to be an entire emergency fund. It will not cover most major expenses that will arise. However, it will cover minor emergencies (ex. replace a tire). Once you have that first $1,000 though, you start to build toward a real full-sized fund.

Layer 2: Core Fund

Once you build your micro fund, it’s time to protect against larger emergencies such as income loss. Common recommendations suggest anywhere from 3-18 months of cash reserves. However, these rules of thumb are generally directed towards a USA audience. They don’t account for specific benefits we have in Canada.

To figure out how much you actually need in your core fund, you have to consider the cost of your essential expenses, the average length of unemployment, as well as any financial benefits you will receive during unemployment.

Essential Expenses

After you have your started fund, it is time to start building towards a full fund. In order to do this, you have to first calculate your weekly essential expenses cost. This includes the cost of:

Shelter

Groceries

Utilities (Hydro, Heat, Water & Sewer)

Household Supplies

Basic Clothing Needs

Transportation

Internet

Phone Bill

Insurance

Minimum Debt Payments.

Some expenses are variable from month to month (ex. Laundry detergent). Especially if you buy these products in bulk. In order to get a better understanding of your essential expenses, it is best to calculate the average cost over a 3 month period.

Only essential expenses?

If you are unemployed, it is assumed that you will engage in some degree of austerity (reduce spending). You will likely avoid living the same lifestyle that you currently live, at least temporarily, until your situation improves. Provided this, you shouldn’t add most discretionary spending to your essential expenses budget. This includes any vacations, entertainment, leisure activities, subscriptions, food delivery services, and social events.

If you are committed to maintaining your same lifestyle in unemployment (which we don’t recommend), then you can just calculate the average weekly cost of all your expenses from your budget over a 3 month period. However, keep in mind, this will require a significantly larger emergency fund.

Add in Dependents

When you do the math, don’t just use your own expenses: include dependents (kids, spouse without income, elderly parents) because if your income drops, they still need their share of essentials.

How Long Might “Lost Income” Last?

After you have determined your essential expenses, the next question becomes, how long will you have to live on this reduced budget? One measurement that can help you determine how much you need for an emergency fund is the average length of unemployment in Canada. Your fund should ideally last through that window (or longer).

According to a 2024 report by Employment and Social Development Canada the average duration of unemployment in Canada is 17 to 25 weeks (~ 4 to 6 months).

So, as a ballpark figure, planning for 4–6 months of income loss is a reasonable starting point (adjusting for your risk tolerance and job security).

The Benefit of Being Canadian (EI)

All employed, and most self-employed Canadians contribute to Employment Insurance (EI). This program provides you with financial assistance if you are laid off from work. It is meant to provide a bridge during a lapse in employment, not to serve as a long term financial support system. In order to qualify for the support you would need to:

Have been employed

Lost your job due to uncontrollable factors

Have been without work for at least 7 consecutive days.

Are capable of working (ie. not disabled or injured), and are actively searching for work.

As of 2025, you may be eligible to receive up to 55% of your average weekly earnings up to a weekly maximum of $695. The maximum length of the benefit is 45 weeks (~10 months). Your average weekly earnings is calculated based on your best 14-22 weeks, in the prior 52 week period before the claim was made. For a better estimate of how much EI benefits you would receive, we suggest you use the Government of Canada calculator here.

On a rolling 12 month period, the maximum EI benefits would result in a yearly taxable income of $36,140 (Note: The benefit doesn’t last a full year). In 2023, according to Statistics Canada, the median after tax income was $39,900 (or ~$46,300 pre tax). Assuming 2% wage growth per year, this should have increased to $48,170 by 2025 (*). This means that EI benefits are only 75% of the median income. If you are at or above the median income, this could represent a significant decrease in monthly earnings. However, the benefit of this program is that it reduces the amount of money that you will need in an emergency fund.

(*) This is personal income, not household income which is significantly higher. This assumes that wage growth has increased by 2% per year since 2023, and that you live in Ontario. Other provinces may have higher or lower tax rates.

Margin Of Error

In the investing world, Warren Buffett often talks about the importance of a margin of safety. This is the idea that even well reasoned plans should leave room for error, because the future rarely unfolds exactly as expected. In investing, it means buying an asset for less than its true value to protect yourself from misjudgment or bad luck.

When you calculate your emergency fund, the same philosophy applies. Even after accounting for Employment Insurance (EI) and your typical expenses, there’s always uncertainty. EI may take weeks to arrive, job searches may last longer than average, or unexpected costs might arise.

That’s why your formula shouldn’t stop at just covering expected needs, but instead should look more like this:

(Essential Weekly Expenses – Projected Weekly EI Benefit) × Average Length of Unemployment + Margin of Safety

A practical margin of safety is to add an extra 10–20% on top of your calculated amount, or roughly 2–4 additional weeks of expenses. This extra cushion protects you from delays in EI payments, cost-of-living increases, or expenses that don’t fit neatly into your budget. As Buffett says, “You don’t know who’s swimming naked until the tide goes out.” This margin of safety ensures that when your tide goes out, you’re still financially covered.

Layer 3: Extended Fund

Many Canadians will be able to manage emergencies with a core fund. However, there are some cases where a much larger emergency fund is recommended. These include:

You’re self-employed, a contractor, or not eligible for EI.

You own a home with large liabilities (high debt owing/high payments).

You live in a single income household.

You have several dependents (children, parents, etc).

You rely on investments for income (retirees).

In each of these cases, an income disruption has the potential to significantly impact your livelihood. We suggest you accumulate 9-12 months of essential expenses. Even 18 months may even be warranted. This gives you the flexibility to recover from an extended income disruption without stress.

Ex. Wendy works as a website designer earning $90,000/year ($64,586 Net). She lives in Toronto so her essential expenses are $4,500/month. She currently pays $2,600/month in rent alone living in a small one bedroom apartment. Wendy lives on her own, so her only source of income in the case of unemployment would be EI benefits. This would decrease her income to below her cost of rent alone. Provided this Wendy should have between 9-12 months of essential expenses in an emergency fund.

Low End: $4,500 x 9 = $40,500

High End: $4,500 x 12= $54,000

What about EI?

No EI Benefits should be calculated into an extended emergency fund for a couple of reasons:

Retirees, and some self employed individuals will not receive the benefits.

EI benefits may not extend the entire 9-12 months that are needed.

Even for those eligible for EI, we don’t recommend subtracting that amount from your essential expenses in the extended fund. Income insecurity is too high, during unemployment, for those with a high cost of living. Any additional income from EI should just act as a buffer (or margin of error) to help minimize the risk of financial ruin.

How to Calculate Your Emergency Fund (Step-by-Step)

Core Fund

1. List All Essential Expenses

Housing (rent or mortgage)

Utilities (heat, water, hydro, internet)

Groceries

Insurance payments

Minimum debt payments

Transportation (gas, bus pass, etc.)

Childcare or medical essentials

Basic clothing needs

2. Total Your Monthly Expenses

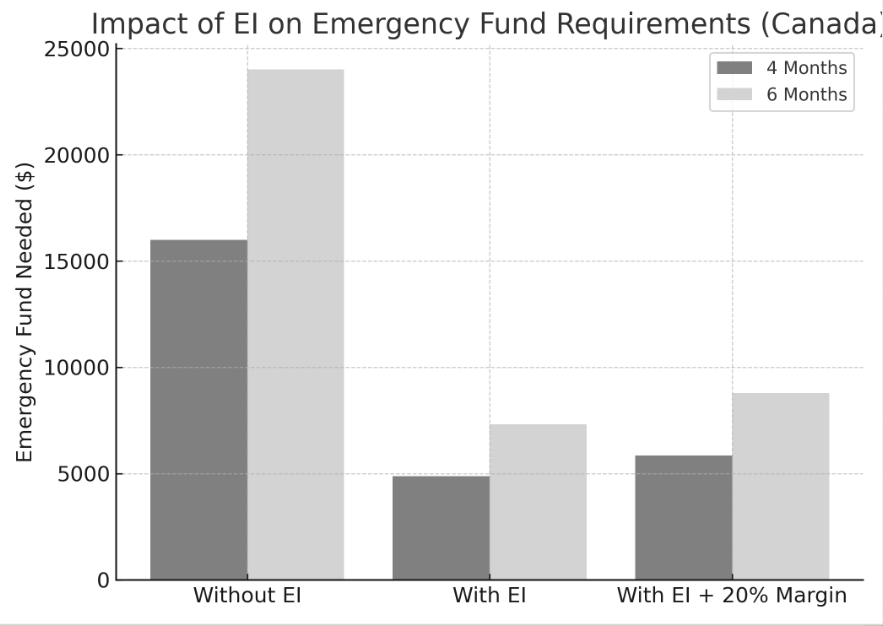

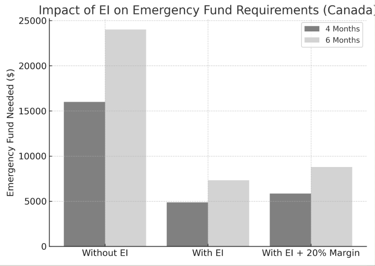

Let’s say your essentials come to $4,000 per month. Your core emergency fund would cover 4–6 months of essential expenses.

$4,000 x 4 = $16,000 (on the low end)

$4,000 × 6 = $24,000 (on the high end)

3. Subtract Projected EI Benefits

If we assume you qualify for the maximum of $695/week, then you should receive ~$2,780/month in EI Benefits.

Monthly Essential Expenses ($4,000) - Projected EI Benefits ($2,780) = $1,220 Monthly Emergency Fund Need

Based on this calculation we should need the following for a core emergency fund:

$1,220 × 4 = $4,880 (on the low end)

$1,220 × 6 = $7,320 (on the high end)

4. Add A Margin of Safety

The last step would be to add the 20% margin of safety.

$4,880 x 1.20 = $5,856 (4 Month Emergency Fund)

$7,320 x 1.20 = $8,784 (6 Month Emergency Fund)

Extended Fund

An extended fund is just 9-12 months of essential expenses, with no EI calculation. So using this same example with monthly essential expenses of $4,000 you should have the following:

$4,000 x 9 = $36,000 (9 Month Emergency Fund)

$4,000 x 12 = $48,000 (12 Month Emergency Fund)

How to Build (and Rebuild) Your Emergency Fund

Now that you know how much you need for an emergency fund in Canada, the next question becomes how do you build it?

Building an emergency fund should be treated like investing, and debt repayment. You should follow these principles:

Set up a separate emergency fund account: There are several options that provide a good interest rate return.

Start small: Even contributing $50-$100 per month will add up over time.

Automate it: Set up automatic transfers right after payday from your chequing account to the new emergency fund.

Treat it like a bill: Pay your future self first.

Rebuild after use: If you withdraw from your emergency fund you want to restart monthly deposits.

Where to Keep Your Emergency Fund?

You could set-up a separate account with your current bank for your emergency fund. However, depending on where you bank, this could mean sacrificing significant returns on your money. Since an emergency fund, in some case, can be quite large (ie. extended fund) you don’t want your money sitting there collecting dust.

A good emergency fund should provide specific criteria:

Be safe, liquid (not locked in), and easily accessible.

Provide a reasonable interest rate return.

Luckily, there are several Canadian options that meet these criteria. Since we don’t want you to lose out on any money, we covered the subject in detail in our post “Best Emergency Fund Accounts in Canada (2025 Guide)”.

How to Adjust Your Emergency Fund Over Time

Your emergency fund isn't a set-it-and-forget-it savings goal. As your life evolves, so should your fund. At minimum, you should reassess your emergency fund annually, or whenever a major life change occurs. This includes getting a new job, buying a home, having a child, taking on new debt, or experiencing a significant change in income.

Lifestyle inflation should also be factored in. If your monthly expenses increase by 5% due to rising cost of living, your emergency fund target should increase proportionally.

Example: Your essential expenses were $3,000/month last year but they increased to $3,300 this year due to a new car purchase with a higher payment than your last one. Now your updated 6-month emergency fund target increases from $18,000 to $19,800.

Similarly, some life changes can reduce your emergency fund needs. If you gain a second household income, secure a more stable job, or pay off significant debt, you may be able to reduce your emergency fund needs. The key is to keep your fund aligned with your current reality, not what it was in years prior.

Common Mistakes That Leave You Underprepared

Not Rebuilding the Fund

Many Canadians make mistakes that undermine their emergency fund. One of the most common is failing to rebuild the fund after using it. Dipping into your emergency fund should not be seen as a failure. It is there to deal with emergency situations. But once the situation passes, you need to restart your monthly contributions to prepare for the next unexpected event, which will inevitably occur.

Underestimating Expenses

Another mistake is underestimating essential expenses. Many people forget to include irregular costs like home or car insurance, property taxes, or annual memberships that are paid quarterly or yearly. These are still essential and need to be factored into your monthly average. I too get surprised when I receive my yearly CAA membership renewal bill.

Relying On Other Income Sources

Some assume that EI benefits or a partner's income will cover all costs during unemployment. While these can help, EI only replaces about 55% of your income (up to a cap), and relying entirely on a spouse's income can create financial strain if their job security isn't guaranteed. Add to this, it can create mental and emotional strain amongst family members.

Treating It As Fun Money

Many Canadians treat their emergency fund like a discretionary savings account, using it for predictable expenses like car maintenance, holiday shopping, or vacations. Often you will go through extended periods of time without ever needing to dip into your emergency fund. This lulls you into thinking that you should use it for something else. However, this defeats the purpose and leaves you vulnerable when a true emergency strikes. If you know an expense is coming, budget for it separately. Your emergency fund is for the unexpected.

Conclusion

Your emergency fund isn't about perfection, it's about protection. Whether you're saving your first $1,000 or building toward six months of expenses, what matters most is consistency. By calculating a personalized target, reviewing it yearly, and rebuilding when needed, you'll stay financially secure no matter what life throws at you.

The peace of mind that comes from knowing you can handle a job loss, a major repair, or an unexpected expense is invaluable. It removes the stress of wondering how you'll pay for things when life doesn't go according to plan. Start small, automate your savings, and treat your emergency fund like the financial foundation it is. Over time, you'll build not just a fund, but the confidence that comes with being prepared.

Related Posts:

[Budgeting for Beginners: How to Take Control of Your Money]

[Charlie Munger Was Right: Why the First $100K Matters Most]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

Bank of Canada. (2024, July 17). Household debt and credit market trends in Canada (Staff Analytical Note 2024-18). https://www.bankofcanada.ca/2024/07/staff-analytical-note-2024-18/

Dave Ramsey. (n.d.). How much money should I have in an emergency fund? Ramsey Solutions. https://www.ramseysolutions.com/save/how-much-money-should-i-have-in-an-emergency-fund

Employment and Social Development Canada. (2024). Employment Insurance monitoring and assessment report: Chapter 1 – Employment Insurance overview. Government of Canada. https://www.canada.ca/en/employment-social-development/programs/ei/ei-list/reports/monitoring2024/chapter1.html

Government of Canada. (n.d.). Employment Insurance (EI) benefit estimator. https://estimateurae-eiestimator.service.canada.ca/en

Statistics Canada. (2025, July). Table 36-10-0639-01: Credit market summary, financial indicators. https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610063901

Statistics Canada. (2024, March). Table 11-10-0091-01: Distribution of household economic accounts, income, consumption, saving and wealth of Canadians, 2023 results. https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1110009101

Buffett, W. (1991). Berkshire Hathaway shareholder letter. Berkshire Hathaway Inc. https://www.berkshirehathaway.com/letters/1991.html

Introduction

In our last post here we discussed the best options as of October 2025 for where to park your emergency fund. The next question becomes how much do you actually need in an emergency fund in order to feel secure? The right amount varies according to your level of income stability, whether or not you have dependents, and how long it will take you to replace your income if you ever become unemployed. This post is aimed at showing you how to calculate your ideal emergency fund amount. We will provide you with a step-by step process to help you identify your number using Canadian specific data.

Why an Emergency Fund Matters (Canadian Reality)

Many Canadians are just one unexpected bill away from financial stress. Recent surveys show that over one in four Canadians couldn’t afford a $500 emergency, and nearly half have no dedicated emergency savings at all. In fact, 46% of Canadians experienced a major unexpected expense last year, with most having to borrow or dip into other savings to cover the cost. This highlights just how crucial an emergency fund is for financial stability.

Purpose of an Emergency Fund

An emergency fund is meant to pay for unanticipated expenses and provide support during income gaps that may occur throughout your life. Situations that would be better managed with an emergency fund include:

Major car or house repair

Replacement of a furnace, water heater, or other appliance.

Medical emergency (Less of a concern in Canada due to the tax funded health care system).

Vet expenses

Legal fees

Income loss

Avoid Credit

In order to manage these types of situations, many Canadians rely on credit products. According to Statistics Canada, total household credit liabilities increased to $3.11 trillion as of July 2025. This is an increase of 3.15% from the prior year.

Not all credit is created equal. If you have access to a low interest line of credit (< 7%), this could be used to deal with emergencies. The interest costs are relatively low, making it manageable to pay off. Not optimal, but not terrible. Unfortunately, many don’t have this option. Add to this that lenders (ex. banks) are not open to giving you a low interest loan when you need it the most. They like to lend money to those they know have it, and are more likely to pay them back.

The consequence is that many people resort to high interest forms of debt such as credit cards, personal loans, and Buy Now, Pay Later (BNPL) services. Worse yet is that they gradually pay off these debts over time, letting interest compound, making their total purchase cost even higher. A report by the Bank Of Canada in 2024 showed that 46% of Canadians carry an outstanding balance on their credit cards. Of those individuals, 23% have a balance that is 80% or more of their borrowing limit.

Ex. Your water heater tank breaks down, and the replacement cost is $5,000. Since you have no emergency fund, you have to pay for it with your credit card. The interest rate on the credit card is 21.99% (which is common). You, like most Canadians, don’t have a lot of money to spare after all your bills, so you decide to put the $5,000 on a credit card and pay $200/month. The result of this situation:

It will take you 2 years and 10 months to pay off the loan.

You will pay an additional $1,748.69 in interest.

The total cost of the water heater increases from $5,000 to $6,748.69.

If you repeat this with several expenses throughout your lifetime, the total impact on your ability to build wealth could be unbelievable. What doesn’t get calculated though is the impact on your mental health. All of these little expenses eat away at your budget, making you feel like you never have enough money to go around…no wonder why you are so stressed about money.

How Much Should You Keep in an Emergency Fund?

The “right amount” to have in an emergency fund depends on your situation. Fortunately, there are useful anchor points you can use to guide you.

Emergency fund = income gap buffer

At the beginning of this article, we discussed all of the reasons why an emergency fund was important. By far the most important of those reasons is to protect you when your income stops or decreases (job loss, illness, business slowdown). It acts as an income buffer so that you can continue paying your bills while you recover or pivot.

Layer 1: Micro Fund- Immediate Protection

Financial Influencer Dave Ramsey famously recommends that before doing anything else, you should save a small emergency fund of $1,000 to cover any surprises. This acts as a mini buffer to prevent you from digging into credit when minor emergencies strike. It acts like a first line of defence.

This amount of money is not meant to be an entire emergency fund. It will not cover most major expenses that will arise. However, it will cover minor emergencies (ex. replace a tire). Once you have that first $1,000 though, you start to build toward a real full-sized fund.

Layer 2: Core Fund

Once you build your micro fund, it’s time to protect against larger emergencies such as income loss. Common recommendations suggest anywhere from 3-18 months of cash reserves. However, these rules of thumb are generally directed towards a USA audience. They don’t account for specific benefits we have in Canada.

To figure out how much you actually need in your core fund, you have to consider the cost of your essential expenses, the average length of unemployment, as well as any financial benefits you will receive during unemployment.

Essential Expenses

After you have your started fund, it is time to start building towards a full fund. In order to do this, you have to first calculate your weekly essential expenses cost. This includes the cost of:

Shelter

Groceries

Utilities (Hydro, Heat, Water & Sewer)

Household Supplies

Basic Clothing Needs

Transportation

Internet

Phone Bill

Insurance

Minimum Debt Payments.

Some expenses are variable from month to month (ex. Laundry detergent). Especially if you buy these products in bulk. In order to get a better understanding of your essential expenses, it is best to calculate the average cost over a 3 month period.

Only essential expenses?

If you are unemployed, it is assumed that you will engage in some degree of austerity (reduce spending). You will likely avoid living the same lifestyle that you currently live, at least temporarily, until your situation improves. Provided this, you shouldn’t add most discretionary spending to your essential expenses budget. This includes any vacations, entertainment, leisure activities, subscriptions, food delivery services, and social events.

If you are committed to maintaining your same lifestyle in unemployment (which we don’t recommend), then you can just calculate the average weekly cost of all your expenses from your budget over a 3 month period. However, keep in mind, this will require a significantly larger emergency fund.

Add in Dependents

When you do the math, don’t just use your own expenses: include dependents (kids, spouse without income, elderly parents) because if your income drops, they still need their share of essentials.

How Long Might “Lost Income” Last?

After you have determined your essential expenses, the next question becomes, how long will you have to live on this reduced budget? One measurement that can help you determine how much you need for an emergency fund is the average length of unemployment in Canada. Your fund should ideally last through that window (or longer).

According to a 2024 report by Employment and Social Development Canada the average duration of unemployment in Canada is 17 to 25 weeks (~ 4 to 6 months).

So, as a ballpark figure, planning for 4–6 months of income loss is a reasonable starting point (adjusting for your risk tolerance and job security).

The Benefit of Being Canadian (EI)

All employed, and most self-employed Canadians contribute to Employment Insurance (EI). This program provides you with financial assistance if you are laid off from work. It is meant to provide a bridge during a lapse in employment, not to serve as a long term financial support system. In order to qualify for the support you would need to:

Have been employed

Lost your job due to uncontrollable factors

Have been without work for at least 7 consecutive days.

Are capable of working (ie. not disabled or injured), and are actively searching for work.

As of 2025, you may be eligible to receive up to 55% of your average weekly earnings up to a weekly maximum of $695. The maximum length of the benefit is 45 weeks (~10 months). Your average weekly earnings is calculated based on your best 14-22 weeks, in the prior 52 week period before the claim was made. For a better estimate of how much EI benefits you would receive, we suggest you use the Government of Canada calculator here.

On a rolling 12 month period, the maximum EI benefits would result in a yearly taxable income of $36,140 (Note: The benefit doesn’t last a full year). In 2023, according to Statistics Canada, the median after tax income was $39,900 (or ~$46,300 pre tax). Assuming 2% wage growth per year, this should have increased to $48,170 by 2025 (*). This means that EI benefits are only 75% of the median income. If you are at or above the median income, this could represent a significant decrease in monthly earnings. However, the benefit of this program is that it reduces the amount of money that you will need in an emergency fund.

(*) This is personal income, not household income which is significantly higher. This assumes that wage growth has increased by 2% per year since 2023, and that you live in Ontario. Other provinces may have higher or lower tax rates.

Margin Of Error

In the investing world, Warren Buffett often talks about the importance of a margin of safety. This is the idea that even well reasoned plans should leave room for error, because the future rarely unfolds exactly as expected. In investing, it means buying an asset for less than its true value to protect yourself from misjudgment or bad luck.

When you calculate your emergency fund, the same philosophy applies. Even after accounting for Employment Insurance (EI) and your typical expenses, there’s always uncertainty. EI may take weeks to arrive, job searches may last longer than average, or unexpected costs might arise.

That’s why your formula shouldn’t stop at just covering expected needs, but instead should look more like this:

(Essential Weekly Expenses – Projected Weekly EI Benefit) × Average Length of Unemployment + Margin of Safety

A practical margin of safety is to add an extra 10–20% on top of your calculated amount, or roughly 2–4 additional weeks of expenses. This extra cushion protects you from delays in EI payments, cost-of-living increases, or expenses that don’t fit neatly into your budget. As Buffett says, “You don’t know who’s swimming naked until the tide goes out.” This margin of safety ensures that when your tide goes out, you’re still financially covered.

Layer 3: Extended Fund

Many Canadians will be able to manage emergencies with a core fund. However, there are some cases where a much larger emergency fund is recommended. These include:

You’re self-employed, a contractor, or not eligible for EI.

You own a home with large liabilities (high debt owing/high payments).

You live in a single income household.

You have several dependents (children, parents, etc).

You rely on investments for income (retirees).

In each of these cases, an income disruption has the potential to significantly impact your livelihood. We suggest you accumulate 9-12 months of essential expenses. Even 18 months may even be warranted. This gives you the flexibility to recover from an extended income disruption without stress.

Ex. Wendy works as a website designer earning $90,000/year ($64,586 Net). She lives in Toronto so her essential expenses are $4,500/month. She currently pays $2,600/month in rent alone living in a small one bedroom apartment. Wendy lives on her own, so her only source of income in the case of unemployment would be EI benefits. This would decrease her income to below her cost of rent alone. Provided this Wendy should have between 9-12 months of essential expenses in an emergency fund.

Low End: $4,500 x 9 = $40,500

High End: $4,500 x 12= $54,000

What about EI?

No EI Benefits should be calculated into an extended emergency fund for a couple of reasons:

Retirees, and some self employed individuals will not receive the benefits.

EI benefits may not extend the entire 9-12 months that are needed.

Even for those eligible for EI, we don’t recommend subtracting that amount from your essential expenses in the extended fund. Income insecurity is too high, during unemployment, for those with a high cost of living. Any additional income from EI should just act as a buffer (or margin of error) to help minimize the risk of financial ruin.

How to Calculate Your Emergency Fund (Step-by-Step)

Core Fund

1. List All Essential Expenses

Housing (rent or mortgage)

Utilities (heat, water, hydro, internet)

Groceries

Insurance payments

Minimum debt payments

Transportation (gas, bus pass, etc.)

Childcare or medical essentials

Basic clothing needs

2. Total Your Monthly Expenses

Let’s say your essentials come to $4,000 per month. Your core emergency fund would cover 4–6 months of essential expenses.

$4,000 x 4 = $16,000 (on the low end)

$4,000 × 6 = $24,000 (on the high end)

3. Subtract Projected EI Benefits

If we assume you qualify for the maximum of $695/week, then you should receive ~$2,780/month in EI Benefits.

Monthly Essential Expenses ($4,000) - Projected EI Benefits ($2,780) = $1,220 Monthly Emergency Fund Need

Based on this calculation we should need the following for a core emergency fund:

$1,220 × 4 = $4,880 (on the low end)

$1,220 × 6 = $7,320 (on the high end)

4. Add A Margin of Safety

The last step would be to add the 20% margin of safety.

$4,880 x 1.20 = $5,856 (4 Month Emergency Fund)

$7,320 x 1.20 = $8,784 (6 Month Emergency Fund)

Extended Fund

An extended fund is just 9-12 months of essential expenses, with no EI calculation. So using this same example with monthly essential expenses of $4,000 you should have the following:

$4,000 x 9 = $36,000 (9 Month Emergency Fund)

$4,000 x 12 = $48,000 (12 Month Emergency Fund)

How to Build (and Rebuild) Your Emergency Fund

Now that you know how much you need for an emergency fund in Canada, the next question becomes how do you build it?

Building an emergency fund should be treated like investing, and debt repayment. You should follow these principles:

Set up a separate emergency fund account: There are several options that provide a good interest rate return.

Start small: Even contributing $50-$100 per month will add up over time.

Automate it: Set up automatic transfers right after payday from your chequing account to the new emergency fund.

Treat it like a bill: Pay your future self first.

Rebuild after use: If you withdraw from your emergency fund you want to restart monthly deposits.

Where to Keep Your Emergency Fund?

You could set-up a separate account with your current bank for your emergency fund. However, depending on where you bank, this could mean sacrificing significant returns on your money. Since an emergency fund, in some case, can be quite large (ie. extended fund) you don’t want your money sitting there collecting dust.

A good emergency fund should provide specific criteria:

Be safe, liquid (not locked in), and easily accessible.

Provide a reasonable interest rate return.

Luckily, there are several Canadian options that meet these criteria. Since we don’t want you to lose out on any money, we covered the subject in detail in our post “Best Emergency Fund Accounts in Canada (2025 Guide)”.

How to Adjust Your Emergency Fund Over Time

Your emergency fund isn't a set-it-and-forget-it savings goal. As your life evolves, so should your fund. At minimum, you should reassess your emergency fund annually, or whenever a major life change occurs. This includes getting a new job, buying a home, having a child, taking on new debt, or experiencing a significant change in income.

Lifestyle inflation should also be factored in. If your monthly expenses increase by 5% due to rising cost of living, your emergency fund target should increase proportionally.

Example: Your essential expenses were $3,000/month last year but they increased to $3,300 this year due to a new car purchase with a higher payment than your last one. Now your updated 6-month emergency fund target increases from $18,000 to $19,800.

Similarly, some life changes can reduce your emergency fund needs. If you gain a second household income, secure a more stable job, or pay off significant debt, you may be able to reduce your emergency fund needs. The key is to keep your fund aligned with your current reality, not what it was in years prior.

Common Mistakes That Leave You Underprepared

Not Rebuilding the Fund

Many Canadians make mistakes that undermine their emergency fund. One of the most common is failing to rebuild the fund after using it. Dipping into your emergency fund should not be seen as a failure. It is there to deal with emergency situations. But once the situation passes, you need to restart your monthly contributions to prepare for the next unexpected event, which will inevitably occur.

Underestimating Expenses

Another mistake is underestimating essential expenses. Many people forget to include irregular costs like home or car insurance, property taxes, or annual memberships that are paid quarterly or yearly. These are still essential and need to be factored into your monthly average. I too get surprised when I receive my yearly CAA membership renewal bill.

Relying On Other Income Sources

Some assume that EI benefits or a partner's income will cover all costs during unemployment. While these can help, EI only replaces about 55% of your income (up to a cap), and relying entirely on a spouse's income can create financial strain if their job security isn't guaranteed. Add to this, it can create mental and emotional strain amongst family members.

Treating It As Fun Money

Many Canadians treat their emergency fund like a discretionary savings account, using it for predictable expenses like car maintenance, holiday shopping, or vacations. Often you will go through extended periods of time without ever needing to dip into your emergency fund. This lulls you into thinking that you should use it for something else. However, this defeats the purpose and leaves you vulnerable when a true emergency strikes. If you know an expense is coming, budget for it separately. Your emergency fund is for the unexpected.

Conclusion

Your emergency fund isn't about perfection, it's about protection. Whether you're saving your first $1,000 or building toward six months of expenses, what matters most is consistency. By calculating a personalized target, reviewing it yearly, and rebuilding when needed, you'll stay financially secure no matter what life throws at you.

The peace of mind that comes from knowing you can handle a job loss, a major repair, or an unexpected expense is invaluable. It removes the stress of wondering how you'll pay for things when life doesn't go according to plan. Start small, automate your savings, and treat your emergency fund like the financial foundation it is. Over time, you'll build not just a fund, but the confidence that comes with being prepared.

Related Posts:

[Budgeting for Beginners: How to Take Control of Your Money]

[Charlie Munger Was Right: Why the First $100K Matters Most]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

Bank of Canada. (2024, July 17). Household debt and credit market trends in Canada (Staff Analytical Note 2024-18). https://www.bankofcanada.ca/2024/07/staff-analytical-note-2024-18/

Dave Ramsey. (n.d.). How much money should I have in an emergency fund? Ramsey Solutions. https://www.ramseysolutions.com/save/how-much-money-should-i-have-in-an-emergency-fund

Employment and Social Development Canada. (2024). Employment Insurance monitoring and assessment report: Chapter 1 – Employment Insurance overview. Government of Canada. https://www.canada.ca/en/employment-social-development/programs/ei/ei-list/reports/monitoring2024/chapter1.html

Government of Canada. (n.d.). Employment Insurance (EI) benefit estimator. https://estimateurae-eiestimator.service.canada.ca/en

Statistics Canada. (2025, July). Table 36-10-0639-01: Credit market summary, financial indicators. https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610063901

Statistics Canada. (2024, March). Table 11-10-0091-01: Distribution of household economic accounts, income, consumption, saving and wealth of Canadians, 2023 results. https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1110009101

Buffett, W. (1991). Berkshire Hathaway shareholder letter. Berkshire Hathaway Inc. https://www.berkshirehathaway.com/letters/1991.html