Get our free Debt vs Invest Calculator — click here to access it

RRSP Guide 2025: Canada's Powerful Retirement Savings Tool

Discover how RRSPs work in Canada, including tax benefits, contribution limits, and withdrawal strategies to maximize your retirement savings.

RRSPREGISTERED RETIREMENT SAVINGS PLANRETIREMENT

3/29/202518 min read

Introduction

If you read our recent blog here, you would know that we awarded the TFSA the gold medal it rightfully deserves. It’s ability to allow anyone to both grow money in their account, and be able to withdraw it tax-free makes it a wonderful tool for young Canadians. Going along with that theme, the silver medal must be awarded to the runner up. In 2023, only 51% of Canadians said they would contribute to this account. It is the…Registered Retirement Savings Plan, also referred to as the RRSP. In today’s installment we will be going through the RRSP basics with you to ensure you have a good understanding of the account and how it works.

Unlike the TFSA, the government “incentivizes” you to contribute to the RRSP for the intention of saving for retirement. It discourages you from pulling the money out of this account until you’re older (think 60 plus).

For some historical context, the RRSP was introduced in 1957 by the Liberal Louis St.Laurent government. Ironically, the Liberals would be swept aside within months by John Diefenbaker and the Conservatives. But before that, the Liberal finance minister Walter Harris unknowingly gave a budget speech that would shape millions of peoples lives

The argument was that some fortunate employees worked for companies that contributed to pension plans. A benefit of these pension plans is that they didn’t have to pay tax on their contributions, until they were withdrawn after retirement. So, they wanted to create a general policy for any taxpayer, whether an employee or not, to have similar benefits.. This would allow all taxpayers to set aside a limited amount of their earned income for retirement.

Where can you open a RRSP?

Just like the TFSA, the RRSP is a Canadian specific account that can be opened at any financial institution.

What’s So Special About the RRSP?

There are three main benefits to the RRSP.

1. Contributions made to an RRSP are tax deductible

In other words, you can reduce your taxable income the year you contribute to an RRSP. Let’s use an example of two individuals who live in Ontario named Betty and Bill. Both of these individuals made $60,000 in 2024 from their job as bookkeepers. Betty is a saver, and decided to deposit a total of $10,000 into her RRSP over the course of the year. Bill on the other hand is a spender, and didn’t contribute to the RRSP. In this case

Bill will be taxed on the entire $60,000 of earned income, and will have to pay $13,441 of income tax.

Betty, on the other hand, will be taxed on $50,000 of earned income and will have to pay $10,304 of income tax

In other words, Betty saved over $3,137 of income tax by contributing $10,000 to her RRSP.

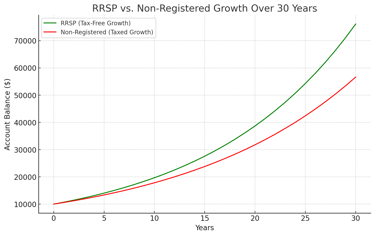

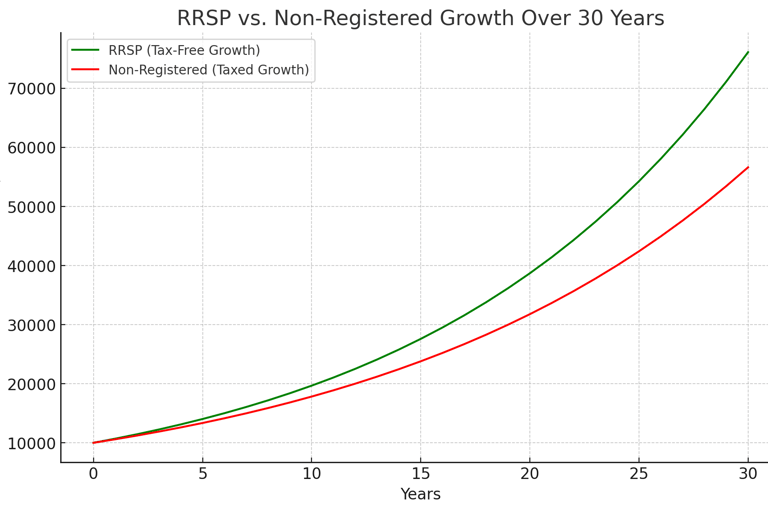

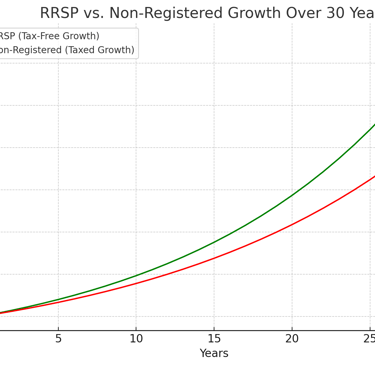

2. Income earned in an RRSP is not taxable while in the account

Similar to the TFSA, all gains within the RRSP are not taxed while the money remains within the account.

For example: Let’s imagine you own $100,000 worth of Bell stocks. Bell is currently paying a 11.81% dividend (yes you read that right). Provided the stock price remains the same, you should receive $11,830 of dividend income in 2025.

If the money was held within a non-registered taxable account you would have to claim that $11,830 as dividend income on your tax return.

However, within the TFSA or RRSP you do not claim this as income.

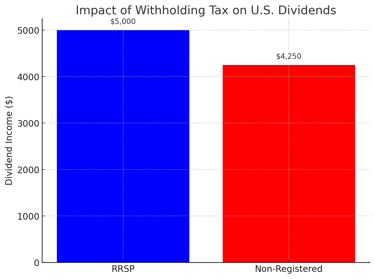

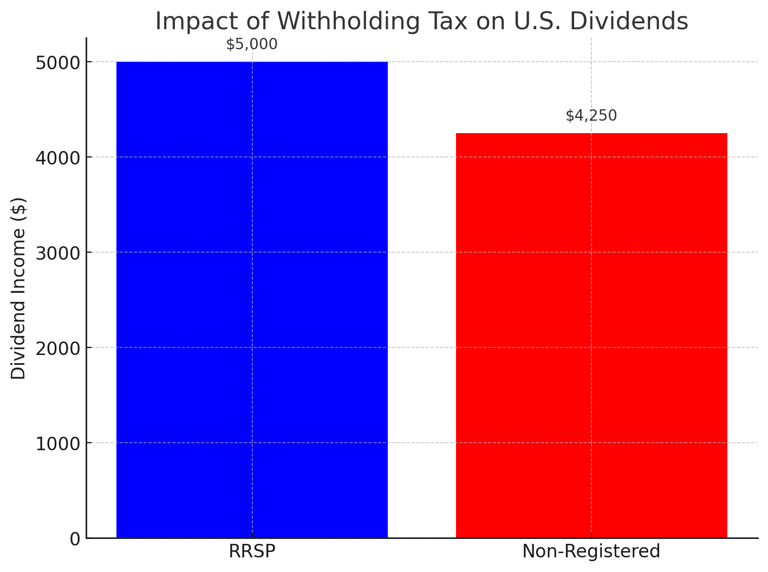

3. Investments in USD do not face any withholding taxes (15-30%) while in an RRSP

The last major benefit to the RRSP, that we will discuss today, is the ability to save on withholding taxes. Generally, the US charges something called withholding taxes on all dividends earned by non-US Citizens. This is important to understand because many stocks pay out dividends to their shareholders. Also, many of the successful companies that people want to invest in are listed on the New York Stock Exchange in US dollars.

Due to tax treaties between Canada and the US, the withholding tax is generally 15%. However, within an RRSP these taxes are 0%. This is important as any tax (or additional fees) would eat into your total returns.

Example: In order to make this simple to understand, the implications we use will be round numbers. Let’s Imagine you have $100,000 invested in a US company that is paying out a 5% dividend annually.

If the $100,000 was invested in an RRSP you should theoretically receive $5,000 of dividends this year. This income will not be taxed until it is withdrawn from the account.

However, if the money was held in a taxable non-registered account you would only receive $4,250. This includes the $5,000 of dividends initially paid out minus 15% withholding tax of $750.

In addition to this, the remaining $4,250 would be taxed as dividend income in Canada.

Hence, the cost savings can be large especially if you have a high amount of holdings.

How Much Can You Contribute?

Each individual can contribute up to 18% of their earned income of the previous year to a RRSP. This amount is referred to as your deduction limit (ie. how much you can deduct from your income for this year).

For Example: Imagine Brian made $60,000 in 2024 working as a carpenter. He would be allowed to contribute a maximum of $10,800 to his RRSP in 2025.

The RRSP is similar to the TFSA in that you can carry forward unused RRSP contribution room to future years.

For Example: Now imagine Brian made $50,000 in 2023, in which case his deduction limit for 2024 was $9,000. However, he didn’t contribute to his RRSP in 2024. So now instead of having $10,800 of deduction limit, as per the prior example, he actually has $19,800 of deduction limit which he can use in 2025.

The maximum allowable deduction limit for 2025 is $32,490. So you could reach this number in one of two ways:

Having a 2024 earned income of $180,500 (ie. 18% is $32,490)

Or by carrying forward past years contributions.

Unlike the TFSA, you will not receive additional contribution room every year unless you earn an income.

Pension Considerations

If you have a pension plan through work, you can also contribute to an RRSP. However, your contribution room will be lower then non-pensioned employees. This is due to what is called a Pension Adjustment (PA). The PA is where the government will reduce your RRSP contribution limit proportional to the estimated value of your pension.

Where Can you Find your RRSP Limits?

You can find your RRSP contribution room (ie. total amount available to be deducted in future years), and 2025 deduction limit (ie. total amount you can deduct in this year) on your myCRA account here.

Special Withdrawal Circumstances

There are two special circumstances whereby funds can be withdrawn from the RRSP without taxation. These are for the First Time Home Buyers Plan and Lifelong Learning Plan. We plan to dive into these during future articles but for now understand that there are rules and regulations regarding the withdrawal of the money. Also, all money has to be re-contributed to the account over a specified time period. In other words, you can’t just walk away with the funds tax-free and claim you are using it for a home purchase or school.

RRSP to RRIF: What Happens at Retirement?

Your RRSP is great for accumulating retirement savings, but it isn’t meant to last forever. What happens when you’re ready to retire and start using your RRSP savings… enter the RRIF. By December 31 of the year you turn 71, you must convert your RRSP into a Registered Retirement Income Fund (RRIF), or withdraw the money (which is usually a bad idea due to taxes). You can convert the RRSP to a RRIF earlier if you choose to do so.

A RRIF works like an RRSP in that your investments still grow tax-free. However, once converted to a RRIF you can no longer contribute more money. Instead you are required to withdraw a minimum amount each year as income. The amount you must withdraw is based on your age, and increases every year. At 71 the minimum withdrawal amount is 5.4%, increasing each year. By 95, you must withdraw at least 20% of your RRIF balance annually. You are able to withdraw more then the minimum each year if your choose to do so. Similar to the RRSP, withdrawals from your RRIF are taxable.

Example: David turns 71 in 2030, and has a $500,000 nest egg in his RRSP.

He converts his RRSP to a RRIF before the deadline.

Based on government rules, at age 72, he must withdraw at least 5.4% of his RRIF balance.

His minimum withdrawal amount is $27,000 that year which is added to his taxable income. (ie. $500,000 x 0.054)

Provided that he is no longer working, his tax rate is likely lower than when he was earning a salary.

A common strategy is to start withdrawing RRSP funds earlier (ie. in your 60’s) if you expect to be in a high tax bracket when converting to a RRIF to minimize the tax impact.

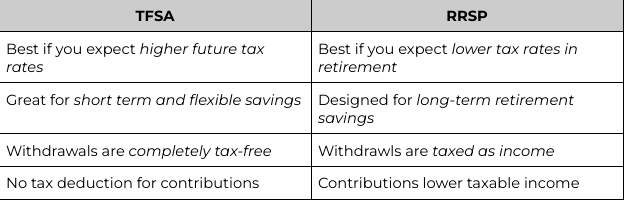

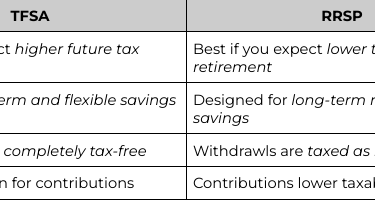

TFSA VS RRSP

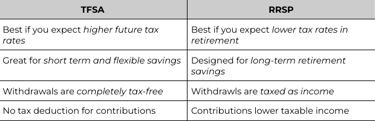

One of the questions we get asked alot is whether it’s better to put money in a TFSA or RRSP first (now FHSA too, but we’ll talk about that in another blog). My answer to this question is a big fat…”it depends”.

What does it depend on?

The individual's income (now and in the future)

And, what they think tax rates will be in the future

If you think your income is going to increase in the future, then waiting to invest in your RRSP will allow you to gain a better deduction on your taxes. However, there are also circumstance where people assume there income will decrease in the future. This could be because you plan to drop down to part time, or switch to a more fulfilling but lower paid occupation. In which case, maximizing the benefits of the RRSP today may be better for you.

Another factor to consider is that taxes may increase in the future. This is not an unrealistic expectation considering that government deficits are increasing, and there primary revenue source is taxation. If this is something that concerns you then in that case it may be better to get your tax refund now, and invest the funds.

One of the common misconceptions about this whole TFSA vs RRSP knockout fight is that the TFSA is automatically better, in all circumstances. The reason why this belief exists is because your TFSA withdrawals are tax-free vs the RRSP where you have to pay them in the future. This often is a pain point for retirees, who realize at retirement, when there income is generally lower, that they must pay taxes to use their “own” money.

This may come as a surprise to many, but you could actually save more money by using your RRSP, rather than your TFSA. This is even after factoring in taxes from withdrawing. The result of which strategy is better highly depends on your tax rate when you put the money in, and your tax rate when you take it out.

Example: If you put $100 in an RRSP at a tax rate of 30%, then you’re saving 30% of that $100 from your taxes. In the future, when you take that $100 out of your RRSP at a tax rate of 20% (because you’re retired and as such your income is lower) then you’ve effectively saved 10% from taxes. As opposed to someone who put it only in a TFSA and paid the 30% tax on the $100.

Conclusion

The RRSP is a very effective strategy for long term wealth accumulation. Although we like the TFSA more due to its flexibility (ie. Can withdraw any time without penalty), it doesn’t mean it is any better of a tool. As we discussed you must evaluate your current and future circumstances to determine if it is the RRSP is the right tool for you. And if you are able to maximize both… well then you may just take home all the medals on your journey to financial freedom.

Related Posts

[Why the TFSA Is the Best Registered Account in Canada (2025)]

[How Investments Are Taxed in Canada: Taxable Accounts Guide]

[Canada's HBP & LLP: Using Your RRSP for Home Buying & Education]

Disclaimer: The information discussed in this podcast is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Edward Jones. (2023, February 13). Sharp increase in RRSP contributions expected in 2023 despite half of Canadians nervous about their finances. Edward Jones. https://www.edwardjones.ca/ca-en/why-edward-jones/news-media/press-releases/increase-rrsp-contributions

Healing, D. (2017, February 13). RRSPs one of the last gasps of the Louis St. Laurent government 60 years ago. CTV News. https://www.ctvnews.ca/business/article/rrsps-one-of-the-last-gasps-of-the-louis-st-laurent-government-60-years-ago/

Heath, J. (2023, June 9). Tax planning for Canadians who invest in the U.S. MoneySense. https://www.moneysense.ca/columns/ask-a-planner/tax-planning-for-canadians-who-invest-in-the-u-s/

Questrade. (n.d.). If you have a pension plan, do you need an RRSP? https://www.questrade.com/learning/goal-tracking/retiring-comfortably/if-you-have-a-pension-plan-do-you-need-an-rrsp

CIBC Wood Gundy. (n.d.). RRIF minimum withdrawal. https://www.woodgundy.cibc.com/en/reference/retirement-planning/rrif-minimum-withdrawal.html

Canada Revenue Agency. (n.d.). Repay funds withdrawn from RRSPs under the Home Buyers' Plan. Government of Canada. https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan/repay-funds-withdrawn-rrsp-s-under-home-buyers-plan.html

Canada Revenue Agency. (n.d.). Registered Retirement Savings Plan (RRSP). Government of Canada. https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/registered-retirement-savings-plan-rrsp.html

Introduction

If you read our recent blog here, you would know that we awarded the TFSA the gold medal it rightfully deserves. It’s ability to allow anyone to both grow money in their account, and be able to withdraw it tax-free makes it a wonderful tool for young Canadians. Going along with that theme, the silver medal must be awarded to the runner up. In 2023, only 51% of Canadians said they would contribute to this account. It is the…Registered Retirement Savings Plan, also referred to as the RRSP. In today’s installment we will be going through the RRSP basics with you to ensure you have a good understanding of the account and how it works.

Unlike the TFSA, the government “incentivizes” you to contribute to the RRSP for the intention of saving for retirement. It discourages you from pulling the money out of this account until you’re older (think 60 plus).

For some historical context, the RRSP was introduced in 1957 by the Liberal Louis St.Laurent government. Ironically, the Liberals would be swept aside within months by John Diefenbaker and the Conservatives. But before that, the Liberal finance minister Walter Harris unknowingly gave a budget speech that would shape millions of peoples lives

The argument was that some fortunate employees worked for companies that contributed to pension plans. A benefit of these pension plans is that they didn’t have to pay tax on their contributions, until they were withdrawn after retirement. So, they wanted to create a general policy for any taxpayer, whether an employee or not, to have similar benefits.. This would allow all taxpayers to set aside a limited amount of their earned income for retirement.

Where can you open a RRSP?

Just like the TFSA, the RRSP is a Canadian specific account that can be opened at any financial institution.

What’s So Special About the RRSP?

There are three main benefits to the RRSP.

Contributions made to an RRSP are tax deductible

In other words, you can reduce your taxable income the year you contribute to an RRSP.

Let’s use an example of two individuals who live in Ontario named Betty and Bill. Both of these individuals made $60,000 in 2024 from their job as bookkeepers. Betty is a saver, and decided to deposit a total of $10,000 into her RRSP over the course of the year. Bill on the other hand is a spender, and didn’t contribute to the RRSP. In this case

Bill will be taxed on the entire $60,000 of earned income, and will have to pay $13,441 of income tax.

Betty, on the other hand, will be taxed on $50,000 of earned income and will have to pay $10,304 of income tax

In other words, Betty saved over $3,137 of income tax by contributing $10,000 to her RRSP.

Income earned in an RRSP is not taxable while in the account

Similar to the TFSA, all gains within the RRSP are not taxed while the money remains within the account.

For example: Let’s imagine you own $100,000 worth of Bell stocks. Bell is currently paying a 11.81% dividend (yes you read that right). Provided the stock price remains the same, you should receive $11,830 of dividend income in 2025.

If the money was held within a non-registered taxable account you would have to claim that $11,830 as dividend income on your tax return.

However, within the TFSA or RRSP you do not claim this as income.

Investments in USD do not face any withholding taxes (15-30%) while in an RRSP

The last major benefit to the RRSP, that we will discuss today, is the ability to save on withholding taxes. Generally, the US charges something called withholding taxes on all dividends earned by non-US Citizens. This is important to understand because many stocks pay out dividends to their shareholders. Also, many of the successful companies that people want to invest in are listed on the New York Stock Exchange in US dollars.

Due to tax treaties between Canada and the US, the withholding tax is generally 15%. However, within an RRSP these taxes are 0%. This is important as any tax (or additional fees) would eat into your total returns.

Example: In order to make this simple to understand, the implications we use will be round numbers. Let’s Imagine you have $100,000 invested in a US company that is paying out a 5% dividend annually.

If the $100,000 was invested in an RRSP you should theoretically receive $5,000 of dividends this year. This income will not be taxed until it is withdrawn from the account.

However, if the money was held in a taxable non-registered account you would only receive $4,250. This includes the $5,000 of dividends initially paid out minus 15% withholding tax of $750.

In addition to this, the remaining $4,250 would be taxed as dividend income in Canada.

Hence, the cost savings can be large especially if you have a high amount of holdings.

How Much Can You Contribute?

Each individual can contribute up to 18% of their earned income of the previous year to a RRSP. This amount is referred to as your deduction limit (ie. how much you can deduct from your income for this year).

For Example: Imagine Brian made $60,000 in 2024 working as a carpenter. He would be allowed to contribute a maximum of $10,800 to his RRSP in 2025.

The RRSP is similar to the TFSA in that you can carry forward unused RRSP contribution room to future years.

For Example: Now imagine Brian made $50,000 in 2023, in which case his deduction limit for 2024 was $9,000. However, he didn’t contribute to his RRSP in 2024. So now instead of having $10,800 of deduction limit, as per the prior example, he actually has $19,800 of deduction limit which he can use in 2025.

The maximum allowable deduction limit for 2025 is $32,490. So you could reach this number in one of two ways:

Having a 2024 earned income of $180,500 (ie. 18% is $32,490)

Or by carrying forward past years contributions.

Unlike the TFSA, you will not receive additional contribution room every year unless you earn an income.

Pension Considerations

If you have a pension plan through work, you can also contribute to an RRSP. However, your contribution room will be lower then non-pensioned employees. This is due to what is called a Pension Adjustment (PA). The PA is where the government will reduce your RRSP contribution limit proportional to the estimated value of your pension.

Where Can you Find your RRSP Limits?

You can find your RRSP contribution room (ie. total amount available to be deducted in future years), and 2025 deduction limit (ie. total amount you can deduct in this year) on your myCRA account here.

Special Withdrawal Circumstances

There are two special circumstances whereby funds can be withdrawn from the RRSP without taxation. These are for the First Time Home Buyers Plan and Lifelong Learning Plan. We plan to dive into these during future articles but for now understand that there are rules and regulations regarding the withdrawal of the money. Also, all money has to be re-contributed to the account over a specified time period. In other words, you can’t just walk away with the funds tax-free and claim you are using it for a home purchase or school.

RRSP to RRIF: What Happens at Retirement?

Your RRSP is great for accumulating retirement savings, but it isn’t meant to last forever. What happens when you’re ready to retire and start using your RRSP savings… enter the RRIF. By December 31 of the year you turn 71, you must convert your RRSP into a Registered Retirement Income Fund (RRIF), or withdraw the money (which is usually a bad idea due to taxes). You can convert the RRSP to a RRIF earlier if you choose to do so.

A RRIF works like an RRSP in that your investments still grow tax-free. However, once converted to a RRIF you can no longer contribute more money. Instead you are required to withdraw a minimum amount each year as income. The amount you must withdraw is based on your age, and increases every year. At 71 the minimum withdrawal amount is 5.4%, increasing each year. By 95, you must withdraw at least 20% of your RRIF balance annually. You are able to withdraw more then the minimum each year if your choose to do so. Similar to the RRSP, withdrawals from your RRIF are taxable.

Example: David turns 71 in 2030, and has a $500,000 nest egg in his RRSP.

He converts his RRSP to a RRIF before the deadline.

Based on government rules, at age 72, he must withdraw at least 5.4% of his RRIF balance.

His minimum withdrawal amount is $27,000 that year which is added to his taxable income. (ie. $500,000 x 0.054)

Provided that he is no longer working, his tax rate is likely lower than when he was earning a salary.

A common strategy is to start withdrawing RRSP funds earlier (ie. in your 60’s) if you expect to be in a high tax bracket when converting to a RRIF to minimize the tax impact.

TFSA VS RRSP

One of the questions we get asked alot is whether it’s better to put money in a TFSA or RRSP first (now FHSA too, but we’ll talk about that in another blog). My answer to this question is a big fat…”it depends”.

What does it depend on?

The individual's income (now and in the future)

And, what they think tax rates will be in the future

If you think your income is going to increase in the future, then waiting to invest in your RRSP will allow you to gain a better deduction on your taxes. However, there are also circumstance where people assume there income will decrease in the future. This could be because you plan to drop down to part time, or switch to a more fulfilling but lower paid occupation. In which case, maximizing the benefits of the RRSP today may be better for you.

Another factor to consider is that taxes may increase in the future. This is not an unrealistic expectation considering that government deficits are increasing, and there primary revenue source is taxation. If this is something that concerns you then in that case it may be better to get your tax refund now, and invest the funds.

One of the common misconceptions about this whole TFSA vs RRSP knockout fight is that the TFSA is automatically better, in all circumstances. The reason why this belief exists is because your TFSA withdrawals are tax-free vs the RRSP where you have to pay them in the future. This often is a pain point for retirees, who realize at retirement, when there income is generally lower, that they must pay taxes to use their “own” money.

This may come as a surprise to many, but you could actually save more money by using your RRSP, rather than your TFSA. This is even after factoring in taxes from withdrawing. The result of which strategy is better highly depends on your tax rate when you put the money in, and your tax rate when you take it out.

Example: If you put $100 in an RRSP at a tax rate of 30%, then you’re saving 30% of that $100 from your taxes. In the future, when you take that $100 out of your RRSP at a tax rate of 20% (because you’re retired and as such your income is lower) then you’ve effectively saved 10% from taxes. As opposed to someone who put it only in a TFSA and paid the 30% tax on the $100.

Conclusion

The RRSP is a very effective strategy for long term wealth accumulation. Although we like the TFSA more due to its flexibility (ie. Can withdraw any time without penalty), it doesn’t mean it is any better of a tool. As we discussed you must evaluate your current and future circumstances to determine if it is the RRSP is the right tool for you. And if you are able to maximize both… well then you may just take home all the medals on your journey to financial freedom.

Related Posts

[Why the TFSA Is the Best Registered Account in Canada (2025)]

[Canada's HBP & LLP: Using Your RRSP for Home Buying & Education]

[How Investments Are Taxed in Canada: Taxable Accounts Guide]

Disclaimer: The information discussed in this podcast is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Edward Jones. (2023, February 13). Sharp increase in RRSP contributions expected in 2023 despite half of Canadians nervous about their finances. Edward Jones. https://www.edwardjones.ca/ca-en/why-edward-jones/news-media/press-releases/increase-rrsp-contributions

Healing, D. (2017, February 13). RRSPs one of the last gasps of the Louis St. Laurent government 60 years ago. CTV News. https://www.ctvnews.ca/business/article/rrsps-one-of-the-last-gasps-of-the-louis-st-laurent-government-60-years-ago/

Heath, J. (2023, June 9). Tax planning for Canadians who invest in the U.S. MoneySense. https://www.moneysense.ca/columns/ask-a-planner/tax-planning-for-canadians-who-invest-in-the-u-s/

Questrade. (n.d.). If you have a pension plan, do you need an RRSP? https://www.questrade.com/learning/goal-tracking/retiring-comfortably/if-you-have-a-pension-plan-do-you-need-an-rrsp

CIBC Wood Gundy. (n.d.). RRIF minimum withdrawal. https://www.woodgundy.cibc.com/en/reference/retirement-planning/rrif-minimum-withdrawal.html

Canada Revenue Agency. (n.d.). Repay funds withdrawn from RRSPs under the Home Buyers' Plan. Government of Canada. https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan/repay-funds-withdrawn-rrsp-s-under-home-buyers-plan.html

Canada Revenue Agency. (n.d.). Registered Retirement Savings Plan (RRSP). Government of Canada. https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/registered-retirement-savings-plan-rrsp.html