Get our free Debt vs Invest Calculator — click here to access it

How to Use Your RRSP for Education and Home Buying (HBP & LLP Guide)

Learn how Canada's Home Buyer's Plan (HBP) and Lifelong Learning Plan (LLP) let you withdraw from your RRSP tax-free for home purchases and education.

RRSPFHSA

4/11/202517 min read

Refresher of RRSP

In our post on the RRSP we discussed that it is a tax-deferred account. This means that:

Any deposits you make into your RRSP will be deducted from your earned income during the tax year the deposit is made. (Ex. You make $90,000 from your occupation and contribute $10,000 to an RRSP, then your taxable income will be $80,000)

Meanwhile, any investment income (ie. capital gains, interest, distributions, and dividends) you make over the life of the account will not be subjected to tax in the year it is made.

However, when the money is withdrawn from the account it will be taxed at your marginal tax rate. In other words, it will be added to your taxable income in the year it is withdrawn. (Ex. You make $90,000 from your occupation and withdraw $10,000 from your RRSP, then your taxable income will be $100,000)

In order to avoid/minimize issues during tax season the financial institution that you bank with will put a withholding tax on the funds withdrawn. However, there are two common circumstances whereby the funds can be withdrawn without tax implications. These are The Home Buyer’s Plan (HBP) & The Lifelong Learning Plan (LLP).

Home Buyer’s Plan (HBP)

The Home Buyers Plan is a program that was set up in 1992 by the government to help individuals save for a house purchase. It allows you to withdraw money from your RRSP in order to purchase, or build your first home. The money withdrawn will act like a “interest free” loan to yourself. Any money withdrawn will not be subjected to withholding tax. However, you will have to re-contribute the funds to your RRSP over a defined time period.

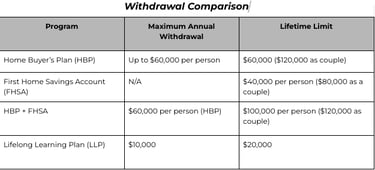

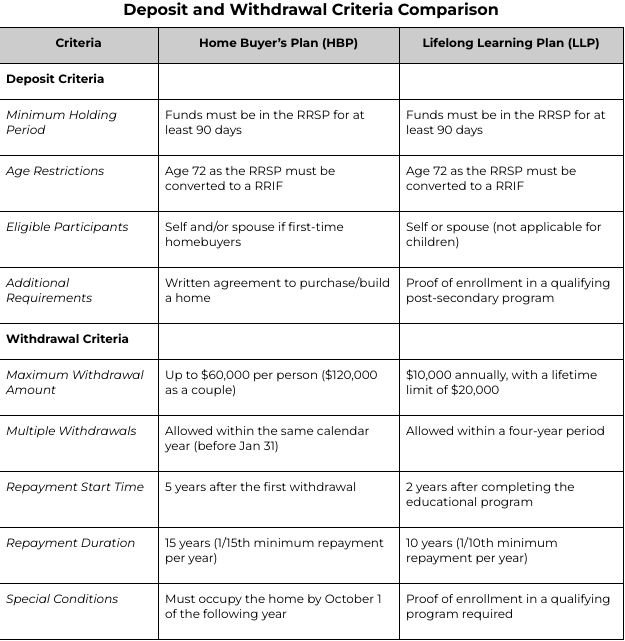

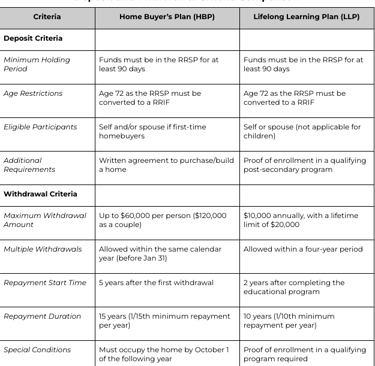

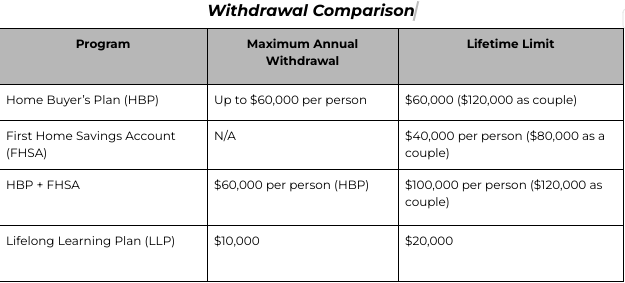

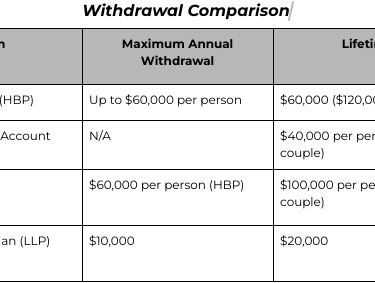

Using this program you can withdraw up to $60,000 per person, or $120,000 as a couple from your RRSP. Once the withdrawal is made you will have to start re-contributing the money to the RRSP within 5 years. However, in order to qualify for the 5- year grace period the house has to be purchased before December 31, 2025. After which point a temporary repayment relief program, introduced by the government to deal with the home affordability crisis, is planned to stop. As of January 1st, 2026 you will have to start repaying the funds 2 years after withdrawal.

After the grace period, all of the funds withdrawn will then need to be re-contributed within 15 years. Each year you will be required to re-contribute a minimum of 1/15th of the total amount withdrawn. This is the minimum payment requirement. However, you can choose to increase your payment amount or make additional lump sum payments if you choose. In the case that you fail to pay back the minimum payment that amount will be added onto your taxable income for that calendar year.

Ex. Imagine you withdraw the full $60,000 from your RRSP as part of the Home Buyer’s Plan to purchase your first home in January 2025. In this case:

You will have until January 2030 to start re-contributing the funds to your RRSP.

As of January 2030, the minimum re-contribution requirement will be $4000 annually, or $334/month for the following 15 years (ie. $60,000 x 1/15= $4000)

If you fail to re-contribute the $4000 minimal payment will be added to your taxable income each of the following 15 years. (ie. If you make $90,000/year from your occupation, your taxable income will increase to $94,000/year).

Qualifying Criteria

It is important to note that you actually need a written agreement to buy, or build a home. A pre-approval will not satisfy the requirements to qualify for this program. Additionally, the funds need to have been in the RRSP for at least 90 days prior to withdrawal. In other words, you can’t just deposit a lump sum of money into your RRSP right before you purchase the home, get the tax break, and expect to use the program.

In order to withdraw funds from an RRSP under the Home Buyer’s Program:

You have to fill out a T1036 form, which you can get from the CRA website.

You must submit the form to your financial institution to authorize the withdrawal.

The withdrawn funds will need to be declared in Schedule 7 of your T1 tax return.

Once your first withdrawal is made you will have until January 31st of the next calendar year to make any further withdrawals. You can make multiple withdrawals as part of this program but you will need to fill out the T1036 each time.

Another important consideration with this program is that you must be able to live in the residence by October 1st of the year following your first withdrawal. This plays an important role in terms of timing of new builds. However, you may be able to provide evidence that you have used the funds to pay for the construction of the home, in the case that it won’t be built prior to the deadline (ie. contractor or material bills).

Exception

Although this program is meant for first time home buyers there is an exception to this rule. Like the FHSA, if you or your partner have not owned a home for the last 4 years you also will be eligible to use this program.

Ex. Imagine you sold a house on January 1, 2021 which you lived in during a previous marriage. Between 2021-2025 you decided to rent. During this period you got into a relationship with a partner that has never owned a home before. As of February 2025 you would be eligible to purchase a home together using the funds from your RRSP Home Buyers Plan.

Combining Programs

Based on current information, the FHSA can be combined with the HBP in order to purchase your first home. As a refresher, the FHSA maximum contribution limit is $40,000 per person, or $80,000 as a couple. However, this could grow to substantially more utilizing effective investment strategies.

Assuming no investment growth though these two programs could potentially enable first time home buyers to save a $100,000 down payment per person, or $200,000 as a couple.

Individual- $60,000 from HBP, $40,000 from FHSA

Couple- $120,000 from HBP, $80,000 from FHSA

Re-contributing the Funds

In order to satisfy the re-payment requirements for the HBP it unfortunately isn’t as simple as just depositing the money back into your RRSP each year. As you may recall when you contribute to your RRSP you get a tax deduction in the year the contribution is made. However, the funds you used as part of the HBP were already contributed to the RRSP (hence you already got the tax break). By re-contributing the funds without declaring it you could potentially get a second tax deduction (ie. double dip).

To avoid this from happening the CRA requires you to report the re-contributions you do make for the HBP on schedule 7 of your T1 tax return. Failure to do so will result in the CRA recognizing the money as a normal RRSP contribution. In which case, they will assume you have not re-contributed the HBP funds. The minimum payment amount will then be added to your taxable income for that year.

Lifelong Learning Plan (LLP)

The Lifelong Learning Plan is another program that was set-up to help individuals afford post-secondary education later in life. It allows you to withdraw money from your RRSP in order to pay for tuition and/or other education related expenses. Like the Home Buyer’s Plan the money withdrawn will act like a “interest free” loan to yourself. Any money withdrawn will not be subjected to withholding tax. However, you have to re-contribute the funds to your RRSP over a defined time period.

In the case of the LLP you have the ability to withdraw $10,000 annually, or a maximum of $20,000 for post-secondary education. However:

You have two years after the completion of the post-secondary program to start repaying the funds.

Once repayment starts you will be required to pay 1/10th of the total amount withdrawn each year for the next 10 years.

Similar to the HBP this is just the minimum payment amount, and you can repay more if you choose.

If you do not re-contribute the funds to the RRSP, 1/10th of the total amount, will be added to your taxable income after the two year grace period.

Ex. Imagine you withdraw $5,000 per year for 4 years, for a total of $20,000 from your RRSP to pay for a 4-year undergraduate degree in nursing. Meanwhile, you graduate from the program in June 2025.

You will have until June 2027 to start contributing the funds to your RRSP.

Once the re-contribution period starts you will have to pay $2,000 annually, or $167/month for the next 10 years. (ie. $20,000 x 1/10= $2000)

If you fail to re-contribute the $2000 it will be added to your taxable income each year.

Criteria

To qualify for the Lifelong Learning Plan, you must be a Canadian resident enrolled in a qualifying educational program at a designated educational institution. The program must last at least three months, with a minimum of 10 hours per week dedicated to courses or work. The LLP also extends eligibility to your spouse or common-law partner, allowing you to fund their education, provided they meet the same requirements. However, you cannot use the LLP for your child's education because a program already exists for this called the RESP. We will discuss this program in a future post.

In order to withdraw funds you’ll need to

Complete Form RC96 which can be obtained from the CRA website.

You must submit the form to your financial institution to authorize the withdrawal.

You’ll need a confirmation of enrollment, or an official letter from the educational institution verifying your enrollment in a qualifying program. This documentation should confirm that the program meets the criteria, such as having a minimum duration of three months and requiring at least 10 hours of coursework per week.

The funds withdrawn must have been in your RRSP for at least 90 days prior to withdrawal.

You can make multiple withdrawals to reach the $20,000 maximum, but they must all occur within a four-year period.

Combining with Other Programs

Unlike the Home Buyer’s Plan, the LLP doesn't currently have a designated program for combining resources like the FHSA. However, you can still use your savings, personal RESPs, or scholarships to supplement the LLP. Proper financial planning can help maximize your education funding without overextending your budget.

Re-Contributing the Funds

Similar to the HBP, repayment for the LLP must be properly reported. To avoid any tax complications. You need to fill out Schedule 7 on your T1 tax return to indicate that your repayments are for the LLP, not a new RRSP contribution. Failure to do so could result in the CRA considering the repayment as a regular RRSP contribution, leading to the withdrawn amount being added to your taxable income.

Exception

If you encounter unforeseen circumstances that prevent you from returning to school or completing your program, the repayment period may be adjusted. The CRA may allow you to cancel or suspend repayments until you're able to return to your studies. This can help alleviate financial strain in the event of unexpected challenges.

Conclusion

Although the RRSP has limitations it can be a very effective tool for young Canadians to build long term wealth. It can also be used as a strategy to fund large expenses you may incur on your way to financial freedom. Instead of borrowing money from the bank, and burring yourself in debt you can lower the financial burden by using the HBP or LLP to fund your education or first home purchase. Combined with the FHSA, and education assistance programs offered in Canada these plans will be very helpful while you navigate the ever increasing cost of living crisis.

Related Posts

[The Silver Medal of Registered Accounts: Why the RRSP Is a Powerful Retirement Tool (2025 Guide)]

[FHSA Canada Guide: How It Works for First-Time Home Buyers]

Charts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Canada Revenue Agency. (n.d.). What is the Home Buyer's Plan (HBP)?. Retrieved from https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan/repay-funds-withdrawn-rrsp-s-under-home-buyers-plan.html

Canada Revenue Agency. (n.d.). Repayments to your RRSP under the Lifelong Learning Plan (LLP). Retrieved from https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/lifelong-learning-plan/repayments-your-rrsp-under.html#contributions

Rates.ca. (n.d.). Career do-over: Everything you need to know about the Lifelong Learning Plan. Retrieved from https://rates.ca/resources/career-do-over-everything-you-need-know-about-lifelong-learning-plan#:~

=the%20LLP%20conditions.-,How%20do%20you%20repay%20the%20Lifelong%20Learning%20Plan%3F,after%20the%20first%20LLP%20withdrawalWealthsimple. (n.d.). Repay a withdrawal under the Home Buyer’s Plan or Lifelong Learning Plan. Retrieved from https://help.wealthsimple.com/hc/en-ca/articles/115015797648-Repay-a-withdrawal-under-the-Home-Buyer-s-Plan-or-Lifelong-Learning-Plan

OpenAI. (2025). Chart of Deposit and Withdrawal Criteria for HBP, and LLP [AI-generated chart]. ChatGPT. https://chat.openai.com/

OpenAI. (2025). Chart of Withdrawal Comparison for HBP, FHSA, and LLP [AI-generated chart]. ChatGPT.https://chat.openai.com/

Refresher of RRSP

In our post on the RRSP we discussed that it is a tax-deferred account. This means that:

Any deposits you make into your RRSP will be deducted from your earned income during the tax year the deposit is made. (Ex. You make $90,000 from your occupation and contribute $10,000 to an RRSP, then your taxable income will be $80,000)

Meanwhile, any investment income (ie. capital gains, interest, distributions, and dividends) you make over the life of the account will not be subjected to tax in the year it is made.

However, when the money is withdrawn from the account it will be taxed at your marginal tax rate. In other words, it will be added to your taxable income in the year it is withdrawn. (Ex. You make $90,000 from your occupation and withdraw $10,000 from your RRSP, then your taxable income will be $100,000)

In order to avoid/minimize issues during tax season the financial institution that you bank with will put a withholding tax on the funds withdrawn. However, there are two common circumstances whereby the funds can be withdrawn without tax implications. These are The Home Buyer’s Plan (HBP) & The Lifelong Learning Plan (LLP).

Home Buyer’s Plan

The Home Buyers Plan is a program that was set up in 1992 by the government to help individuals save for a house purchase. It allows you to withdraw money from your RRSP in order to purchase, or build your first home. The money withdrawn will act like a “interest free” loan to yourself. Any money withdrawn will not be subjected to withholding tax. However, you will have to re-contribute the funds to your RRSP over a defined time period.

Using this program you can withdraw up to $60,000 per person, or $120,000 as a couple from your RRSP. Once the withdrawal is made you will have to start re-contributing the money to the RRSP within 5 years. However, in order to qualify for the 5- year grace period the house has to be purchased before December 31, 2025. After which point a temporary repayment relief program, introduced by the government to deal with the home affordability crisis, is planned to stop. As of January 1st, 2026 you will have to start repaying the funds 2 years after withdrawal.

After the grace period, all of the funds withdrawn will then need to be re-contributed within 15 years. Each year you will be required to re-contribute a minimum of 1/15th of the total amount withdrawn. This is the minimum payment requirement. However, you can choose to increase your payment amount or make additional lump sum payments if you choose. In the case that you fail to pay back the minimum payment that amount will be added onto your taxable income for that calendar year.

Ex. Imagine you withdraw the full $60,000 from your RRSP as part of the Home Buyer’s Plan to purchase your first home in January 2025. In this case:

You will have until January 2030 to start re-contributing the funds to your RRSP.

As of January 2030, the minimum re-contribution requirement will be $4000 annually, or $334/month for the following 15 years (ie. $60,000 x 1/15= $4000)

If you fail to re-contribute the $4000 minimal payment will be added to your taxable income each of the following 15 years. (ie. If you make $90,000/year from your occupation, your taxable income will increase to $94,000/year).

Qualifying Criteria

It is important to note that you actually need a written agreement to buy, or build a home. A pre-approval will not satisfy the requirements to qualify for this program. Additionally, the funds need to have been in the RRSP for at least 90 days prior to withdrawal. In other words, you can’t just deposit a lump sum of money into your RRSP right before you purchase the home, get the tax break, and expect to use the program.

In order to withdraw funds from an RRSP under the Home Buyer’s Program:

You have to fill out a T1036 form, which you can get from the CRA website.

You must submit the form to your financial institution to authorize the withdrawal.

The withdrawn funds will need to be declared in Schedule 7 of your T1 tax return.

Once your first withdrawal is made you will have until January 31st of the next calendar year to make any further withdrawals. You can make multiple withdrawals as part of this program but you will need to fill out the T1036 each time.

Another important consideration with this program is that you must be able to live in the residence by October 1st of the year following your first withdrawal. This plays an important role in terms of timing of new builds. However, you may be able to provide evidence that you have used the funds to pay for the construction of the home, in the case that it won’t be built prior to the deadline (ie. contractor or material bills).

Exception

Although this program is meant for first time home buyers there is an exception to this rule. Like the FHSA, if you or your partner have not owned a home for the last 4 years you also will be eligible to use this program.

Ex. Imagine you sold a house on January 1, 2021 which you lived in during a previous marriage. Between 2021-2025 you decided to rent. During this period you got into a relationship with a partner that has never owned a home before. As of February 2025 you would be eligible to purchase a home together using the funds from your RRSP Home Buyers Plan.

Combining Programs

Based on current information, the FHSA can be combined with the HBP in order to purchase your first home. As a refresher, the FHSA maximum contribution limit is $40,000 per person, or $80,000 as a couple. However, this could grow to substantially more utilizing effective investment strategies.

Assuming no investment growth though these two programs could potentially enable first time home buyers to save a $100,000 down payment per person, or $200,000 as a couple.

Individual- $60,000 from HBP, $40,000 from FHSA

Couple- $120,000 from HBP, $80,000 from FHSA

Re-contributing the Funds

In order to satisfy the re-payment requirements for the HBP it unfortunately isn’t as simple as just depositing the money back into your RRSP each year. As you may recall when you contribute to your RRSP you get a tax deduction in the year the contribution is made. However, the funds you used as part of the HBP were already contributed to the RRSP (hence you already got the tax break). By re-contributing the funds without declaring it you could potentially get a second tax deduction (ie. double dip).

To avoid this from happening the CRA requires you to report the re-contributions you do make for the HBP on schedule 7 of your T1 tax return. Failure to do so will result in the CRA recognizing the money as a normal RRSP contribution. In which case, they will assume you have not re-contributed the HBP funds. The minimum payment amount will then be added to your taxable income for that year.

Lifelong Learning Plan

The Lifelong Learning Plan is another program that was set-up to help individuals afford post-secondary education later in life. It allows you to withdraw money from your RRSP in order to pay for tuition and/or other education related expenses. Like the Home Buyer’s Plan the money withdrawn will act like a “interest free” loan to yourself. Any money withdrawn will not be subjected to withholding tax. However, you have to re-contribute the funds to your RRSP over a defined time period.

In the case of the LLP you have the ability to withdraw $10,000 annually, or a maximum of $20,000 for post-secondary education. However:

You have two years after the completion of the post-secondary program to start repaying the funds.

Once repayment starts you will be required to pay 1/10th of the total amount withdrawn each year for the next 10 years.

Similar to the HBP this is just the minimum payment amount, and you can repay more if you choose.

If you do not re-contribute the funds to the RRSP, 1/10th of the total amount, will be added to your taxable income after the two year grace period.

Ex. Imagine you withdraw $5,000 per year for 4 years, for a total of $20,000 from your RRSP to pay for a 4-year undergraduate degree in nursing. Meanwhile, you graduate from the program in June 2025.

You will have until June 2027 to start contributing the funds to your RRSP.

Once the re-contribution period starts you will have to pay $2,000 annually, or $167/month for the next 10 years. (ie. $20,000 x 1/10= $2000)

If you fail to re-contribute the $2000 it will be added to your taxable income each year.

Criteria

To qualify for the Lifelong Learning Plan, you must be a Canadian resident enrolled in a qualifying educational program at a designated educational institution. The program must last at least three months, with a minimum of 10 hours per week dedicated to courses or work. The LLP also extends eligibility to your spouse or common-law partner, allowing you to fund their education, provided they meet the same requirements. However, you cannot use the LLP for your child's education because a program already exists for this called the RESP. We will discuss this program in a future post.

In order to withdraw funds you’ll need to

Complete Form RC96 which can be obtained from the CRA website.

You must submit the form to your financial institution to authorize the withdrawal.

You’ll need a confirmation of enrollment, or an official letter from the educational institution verifying your enrollment in a qualifying program. This documentation should confirm that the program meets the criteria, such as having a minimum duration of three months and requiring at least 10 hours of coursework per week.

The funds withdrawn must have been in your RRSP for at least 90 days prior to withdrawal.

You can make multiple withdrawals to reach the $20,000 maximum, but they must all occur within a four-year period.

Combining with Other Programs

Unlike the Home Buyer’s Plan, the LLP doesn't currently have a designated program for combining resources like the FHSA. However, you can still use your savings, personal RESPs, or scholarships to supplement the LLP. Proper financial planning can help maximize your education funding without overextending your budget.

Re-Contributing the Funds

Similar to the HBP, repayment for the LLP must be properly reported. To avoid any tax complications. You need to fill out Schedule 7 on your T1 tax return to indicate that your repayments are for the LLP, not a new RRSP contribution. Failure to do so could result in the CRA considering the repayment as a regular RRSP contribution, leading to the withdrawn amount being added to your taxable income.

Exception

If you encounter unforeseen circumstances that prevent you from returning to school or completing your program, the repayment period may be adjusted. The CRA may allow you to cancel or suspend repayments until you're able to return to your studies. This can help alleviate financial strain in the event of unexpected challenges.

Conclusion

Although the RRSP has limitations it can be a very effective tool for young Canadians to build long term wealth. It can also be used as a strategy to fund large expenses you may incur on your way to financial freedom. Instead of borrowing money from the bank, and burring yourself in debt you can lower the financial burden by using the HBP or LLP to fund your education or first home purchase. Combined with the FHSA, and education assistance programs offered in Canada these plans will be very helpful while you navigate the ever increasing cost of living crisis.

Related Posts

[The Silver Medal of Registered Accounts: Why the RRSP Is a Powerful Retirement Tool (2025 Guide)]

[FHSA Canada Guide: How It Works for First-Time Home Buyers]

Charts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Canada Revenue Agency. (n.d.). What is the Home Buyer's Plan (HBP)?. Retrieved from https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan/repay-funds-withdrawn-rrsp-s-under-home-buyers-plan.html

Canada Revenue Agency. (n.d.). Repayments to your RRSP under the Lifelong Learning Plan (LLP). Retrieved from https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/lifelong-learning-plan/repayments-your-rrsp-under.html#contributions

Rates.ca. (n.d.). Career do-over: Everything you need to know about the Lifelong Learning Plan. Retrieved from https://rates.ca/resources/career-do-over-everything-you-need-know-about-lifelong-learning-plan#:~

=the%20LLP%20conditions.-,How%20do%20you%20repay%20the%20Lifelong%20Learning%20Plan%3F,after%20the%20first%20LLP%20withdrawalWealthsimple. (n.d.). Repay a withdrawal under the Home Buyer’s Plan or Lifelong Learning Plan. Retrieved from https://help.wealthsimple.com/hc/en-ca/articles/115015797648-Repay-a-withdrawal-under-the-Home-Buyer-s-Plan-or-Lifelong-Learning-Plan

OpenAI. (2025). Chart of Deposit and Withdrawal Criteria for HBP, and LLP [AI-generated chart]. ChatGPT. https://chat.openai.com/

OpenAI. (2025). Chart of Withdrawal Comparison for HBP, FHSA, and LLP [AI-generated chart]. ChatGPT.https://chat.openai.com/