Get our free Debt vs Invest Calculator — click here to access it

Budgeting for Beginners: How to Take Control of Your Money

Learn budgeting for beginners in Canada with real examples, Canadian-specific percentages, debt strategies, and practical tools to take control of your money.

FINANCIAL BASICSBUDGETING

9/22/202539 min read

Introduction

If you've ever reached the end of the month wondering where all your money went, this guide is for you. Whether you're drowning in debt, living paycheck to paycheck, or just want to be more strategic with your finances, we'll walk you through everything you need to know about budgeting using real Canadian numbers and practical tools you can start using today.

What is Budgeting?

“The highest form of wealth is the ability to wake up every morning and say, ‘I can do whatever I want today.’”- Morgan Housel

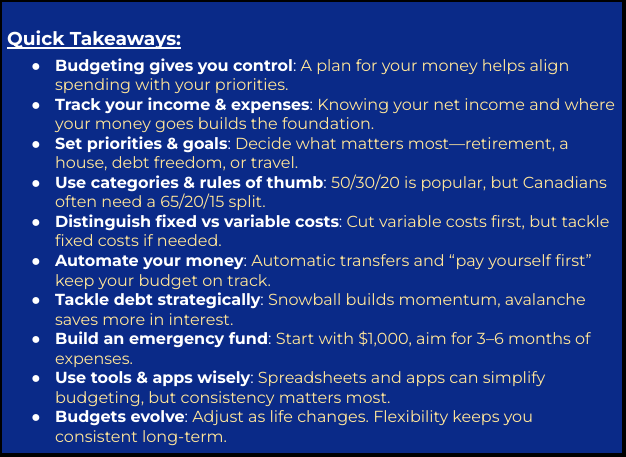

Budgeting is simply creating a plan for how you’ll use your money. It’s about deciding ahead of time where each dollar will go so that your spending matches your priorities. A budget doesn’t have to feel restrictive. Instead, it gives you control. It allows you to better align your values with your spending habits. The objective is that by laying out your income, expenses, savings, and debt payments you can develop a roadmap to reaching your financial goals with less stress.

Why Does Budgeting Matter?

In recent years, budgeting has become increasingly more important for the average Canadian. Factors such as the rising cost of living, increasing debt levels, and a slow wage growth have increased the financial burden for many households. Between the years 2010 and 2024:

Overall prices have increased by 38%, as measured by the Consumer Price Index (CPI)

Average real wages (inflation-adjusted) have only increased by 10-11%.

In 2024 dollars, the 2010 average hourly wage was $31.90, and it has since increased to $35.20.

The average household debt increased from 159-160% of household income to 175-185% of household income.

The average house price in Canada has more than doubled.

$339,100 (2010) vs $694,173 (2024)

Unfortunately, this has created significant friction amongst competing financial demands. We have to now be more selective with where our limited financial resources are allocated. Hence why setting up a budget is so important to helping you reach your financial goals.

How to Make A Budget (Step-by Step)

“You don’t have to optimize everything. You just have to avoid the big mistakes.”- Nick Maggiulli

We will dive further into each of the sub-categories throughout this blog. However, the following is an overview of the 6-step process of developing a budget:

Know your income

Track your expenses

Set priorities

Create categories and assign money

Automate allocation

Review and adjust

Know your Income

There are two very important numbers you should be aware of regarding your income:

How much you make before taxes, benefits, and pensions (Gross Income).

How much you make after taxes, benefits, and pensions (Net Income).

Both are important (as you will see later in this blog), but in your day to day life, the only number that really matters is how much you take home (ie. Net income). It is recommended that you know your monthly income amounts because many expenses in life occur at this frequency (ex. Rent and Bills).

For example: Judy earns $60,000/year (Gross Income) at her job as an administrative assistant in Ontario. Based on this income, she thinks that she will have $5,000 per month to spend (ie. $60,000/12). However, in reality she has to pay income taxes, CPP, and EI. This brings her take home pay closer to $47,000/year (Net Income), or approx $3,900/month. This $1,100 difference is significant when she tries to balance her budget

A Word On Variable Pay

Many employed individuals will receive a consistent income stream each month making it easy to track. However, there are occupations that do not provide this luxury.

Self-employed, or commission-based workers often receive highly variable income where they make a lot one month, and almost nothing the next. On the other hand, seasonal workers such as those in the fishing and farming industry earn most, or all of their income in only a few months. If you are in one of these categories, the best way to calculate your monthly income is using your average monthly income:

Annual Net Income (Prior Year)/ 12 months = Average Monthly Income

If you have multiple years in the industry, this is even better, because you can calculate your average annual income from the last three years.

Unfortunately, regardless of your calculation there is always a risk in these occupations that your actual income is below your projected income (Ex. Real Estate Industry when interest rates are high). This is why it is particularly important that you have a financial safety net in the form of an emergency fund.

Track your Expenses

The next step in the process of building a budget is to track your expenses.

Often, we have no understanding of how much of our money is being spent. In some cases, we even spend more than we earn which is why consumer debt has increased. Even if you are good with your money, you may have certain financial objectives you would like to achieve. This could be going on a trip to Europe, buying your first house, paying for your children's schooling, or investing for retirement. By getting a grip of where your money is being spent, you can choose to redirect to the areas that matter to you in order to achieve your goals.

Developing a Baseline

When making your budget it is important to gather at least 3 months of expenses initially.

Although there will be many aspects of your budget that are consistent, you won’t spend the exact same amount each month. We often make irregular purchases that don’t occur every week, or month. If you shop at Costco, you know this experience all too well. Every few visits you have to restock up on items such as toilet paper, paper towel, laundry detergent, cooking oil, etc, but there are times when you buy items that are not on the shopping list. When you do this, your bill increases significantly. Add to this that you may incur unpredictable expenses such as a car or house repair that may be missed when tracking for only a few weeks.

If you do all your spending using cards and online banking, you can develop your budget today using your last three months expenses. However, if you make purchases using cash, it's best to track the next three months.

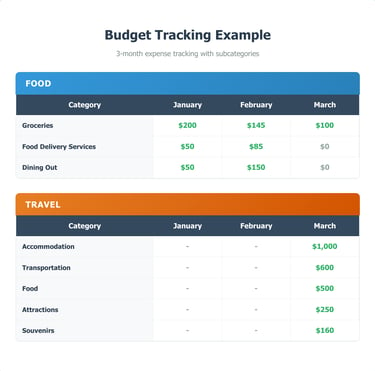

Categories of Expenses

When tracking your expenses, it is important to organize them into categories. This helps you to see clearly, not just how much you are spending, but where the funds are being spent.

There are several budget templates that you can find online. However, we like to separate ours into the following sections:

Savings & Investing

Debt Repayment

Housing Expenses

Food

Transportation

Travel

Personal Care

Leisure and Entertainment

After developing your broad categories, you can increase clarity in your expenses by adding subcategories.

Set Priorities

After you have tracked your expenses, the next step is to figure out where you want to spend your money going forward.

There should be an emphasis directed towards saving for your retirement, and reaching financial freedom. You may have additional goals you would like to achieve such as home ownership, or travel. Regardless of what they are, we need to set priorities in our budget. This involves identifying how much we should spend in each category in order to achieve those goals.

Here's a simple exercise to help clarify your priorities. List your top 3 financial goals and categorize them as:

Short-term (1-3 years)- Ex. Emergency fund, vacation, car down payment

Medium-term (3-10 years)- Ex. House down payment, children's education

Long-term (10+ years)- Ex. Retirement, financial independence

Your budget should reflect your priorities. If home ownership is your biggest goal, housing-related savings should get priority over entertainment spending.

Create Categories & Assign Money

How much to Budget for Each Category

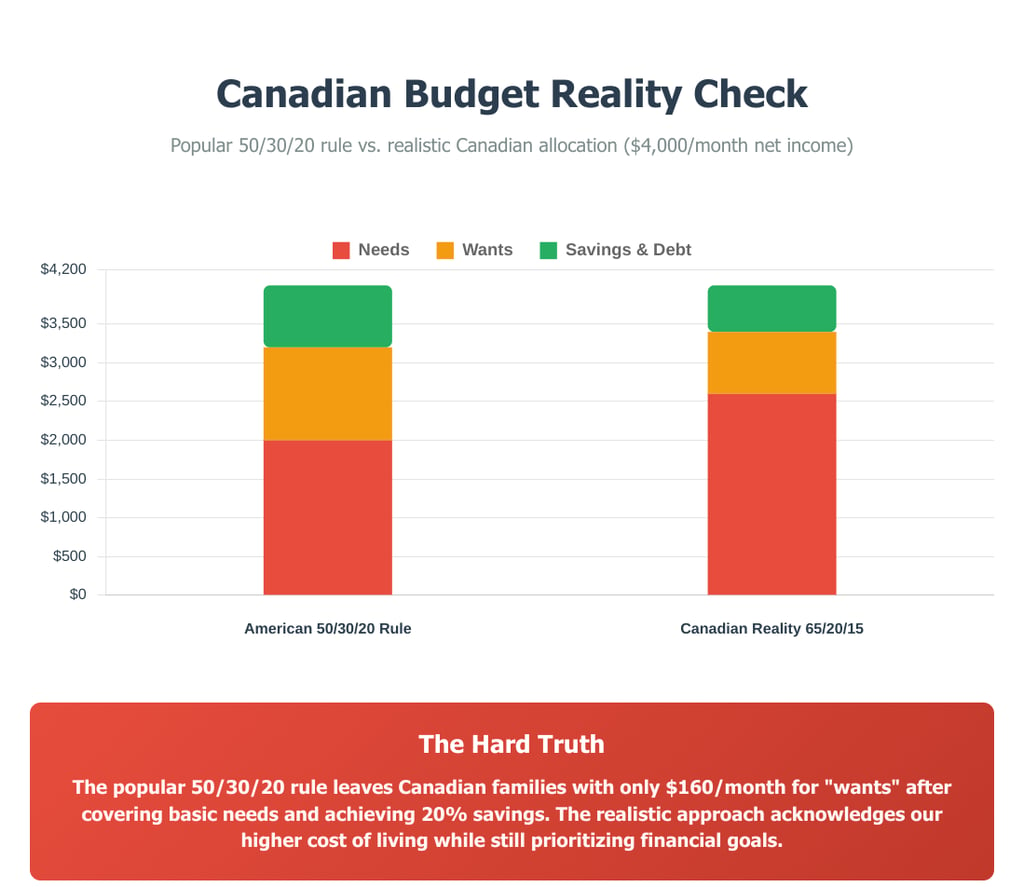

If you have read any personal finance books, you have inevitably come across several rules of thumb in terms of how much to budget for each category. The most popular of which is likely the 50/30/20 Rule created by Elizabeth Warren (yes the US Senator). This rule suggests that your budget should consist of:

50% Needs

Housing, food, transportation, insurance, phone and car bills.

30% Wants

Entertainment, travel, dining out

20% Wealth Generation

Savings (emergency fund, & retirement accounts)

Debt Repayment

Other financial experts will recommend different variations of this same calculation. However, in almost all cases the amount allocated to each category is within 5-10% of the numbers stated above.

Example: Imagine Judy earns $4,000/month net income. She may do the following allocation:

50% Needs ($2,000)

Rent ($1,200), Groceries ($300), Transportation ($200), Utilities/Phone ($200), Insurance ($100)

30% Wants ($1,200)

Dining out ($300), Entertainment ($200), Hobbies ($300), Miscellaneous ($400)

20% Savings/Debt ($800)

Emergency fund ($300), TFSA ($300), Debt payments ($200)

What about Canada?

Although these hard and fast rules are helpful as general guidelines, they may not be appropriate for you. Many of these were created by individuals in the USA where cost of living is significantly different than Canada. According to Statistics Canada, in their Survey of Household Spending, Canadians spent an average of the following in 2023:

$24,671 on Shelter

$8,659 on Groceries

$12,090 on Transportation

$9,404 on Household operations, furnishings, and equipment

Total = $54,824

Meanwhile, the median after-tax family income was $72,400 in 2023.

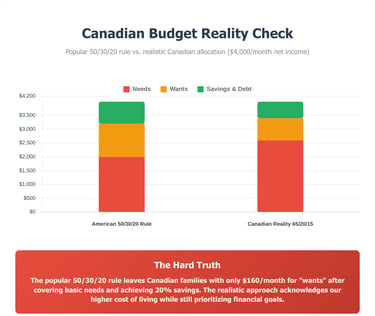

Based on these figures the average Canadian spent almost 76% of their take home income on their needs. In order to reach the coveted 20% savings, you would only have 4% left for wants…. you better enjoy dollar store arts and crafts.

A more realistic Canadian allocation for that same $4,000/month net income may look like this :

65% Needs ($2,600)

Housing ($1,650, Groceries ($325), Transportation ($275), Utilities/phone ($225), Insurance ($125)

20% Wants ($800):

Dining out ($300), Entertainment ($100), Hobbies ($200), Miscellaneous ($200)

15% Savings/Debt ($600)

Emergency fund ($200), TFSA ($200), Debt payments ($200)

Debt Repayment

For many people, an important reason to create a budget is to get out of debt.

A high amount of debt, especially high interest debt, can do significant damage to your financial future. As we noted above, there is already limited room in the average Canadian’s budget due to high cost of living. Debt can drain your cash flow, limit your ability to save, and cause you a lot of stress.

Budgeting gives you a plan so you can consistently make progress and eventually free yourself from this burden.

Good Debt vs Bad Debt

Although all debt weighs down your budget, there should be a delineation between different types of debt.

Good debt is when you borrow money to spend on something that is expected to appreciate in value, or provide some monetary benefit. These would be things like purchasing a house, stocks, or business related expenses. How good the debt is exists on a spectrum. For example, we could say using debt to purchase a rental property would be better than a primary residence because it produces near term cash flows.

Bad debt is when you borrow money to spend on something that will decrease in value. This could include things such as car loans, credit cards, pay day loans, etc. Similarly, bad debts exist on a spectrum. A car may provide utility especially for an individual that doesn’t live close to their work. However, some consumer debt with very high interest rates would fall into the very bad debt category.

Debt Payoff Strategies

Most loans will require you to make regular payments over a predetermined time period. However, the problem for many people is that they start to accumulate multiple of these debts each of which eats into their monthly budget. The two most common approaches to repaying debt are:

Snowball Method

This was made popular by a popular figure in the personal finance community named Dave Ramsay.

This method recommends focusing on paying off the smallest debt first while making minimum payments on all others. Once the first debt is gone, move on to the next smallest. This method helps with the emotional management of debt repayment, by developing quick wins and building momentum.

Avalanche Method

Focus on paying off the debt with the highest interest rate first while making minimum payments on the rest. This approach saves you the most money in interest over time.

Neither method is “right” or “wrong.” The best strategy is the one that you will stick with consistently.

Why Extra Payments Matter

Adding even a small amount to your debt payments each month can drastically shorten your timeline.

Example: If you owe $10,000 on a credit card at 19% interest and make only the minimum $250 monthly payment, it will take about 5 years to pay off. If you add just $150 more each month, you’ll be debt-free in under 3 years and save thousands in interest

Fixed vs Variable Costs

When making your budget, it's helpful to separate your spending into two categories: fixed and variable costs.

Fixed costs are regular expenses that don’t change much from month to month. However, they are harder to remove without consequences. These include things such as mortgage or rent, phone or internet bill, utilities, groceries, car payment, house or car insurance, etc.

Variable costs are expenses that are more flexible and easier to adjust. These include things such as dining out, clothing, entertainment, vacations, subscriptions, etc. For example: A morning coffee from your local cafe may be convenient, but you can also make it at home for a fraction of the price.

If you don’t have enough disposable cash each month, you will need to find a way to reduce spending. Start by trimming variable costs like dining out, subscriptions, or daily coffee runs. These little expenses can free up quick cash to be directed towards your goals.

However, these small cuts can only go so far. If your housing and debt repayment expenses take up most of your income, you may need to tackle fixed costs instead. This may require measures such as renegotiating bills, debt consolidation, and shopping for discount food. In some cases, you may need to take extreme measures such as downsizing, or selling your car.

Ex. Skipping your $4 coffee each workday saves you approx $80/month. This is a lot of money, however, it won’t matter much if your mortgage already takes up 70% of your income.

Automate Allocation

Once you've created your budget categories and assigned dollar amounts, the next step is to make it as effortless as possible to stick to your plan. This is where automation becomes your best friend.

Set Up Automatic Transfers

The moment your pay cheque hits your account, you want your money automatically flowing to where it needs to go. You can easily set up automatic transfer for the following:

Emergency fund savings

Have a designated high interest savings account that you will title “Emergency Fund”.

Investment accounts:

Debt payments:

Mortgage, car loan, line of credit, and credit card

Bills:

Rent, utilities, insurance, phone

Most Canadian banks offer free automatic transfers, and you can usually set these up online in minutes. For utilities, internet, phone, and insurance you can set-up automatic payment through the provider. Similarly, you can do the same through your lender for loans.

Use the "Pay Yourself First" Strategy

Instead of saving what is left over at the end of the month (spoiler alert: there's usually nothing left), treat your savings like a non-negotiable bill. When you get paid your savings get paid first, then you can live off the remainder. If you have difficulty living off what is left, then either your savings rate is too high, or you are spending too much.

Separate Accounts for Different Goals

Consider opening separate savings accounts for different goals:

Emergency fund

Vacation fund

House down payment

New car fund

Since most of these are short term savings goals, they shouldn’t be invested in risk assets such as stocks. Instead you can look for good high interest savings accounts (HISA’s) like those offered at EQ Bank. If you have a planned date for when you want to use the funds, Guaranteed Interest Certificates (GIC’s) offer a good option as well.

Many banks allow you to nickname these accounts too (“Europe Trip 2025" or "Emergency Fund"). Seeing your progress toward specific goals is incredibly motivating.

Practical Tools and Resources

Building a budget initially seems as if it would be very time intensive. And, it would be if you had to track all of the information using pen and paper in an unorganized notebook. Lucky for you, this is not the case. In fact there are several amazing resources that exist to help you in this process.

Spreadsheets

There are several options in terms of spreadsheets that could range from completely free…up to expensive products.

In google sheets, there is a free to access template titled “Annual Budget". It provides a tracking sheet for your expenses, and income sources for an entire year. Also, it includes a summary sheet to compare expenses and income. Each category has several subcategories to help you better organize your finances. You can find similar templates on Microsoft office and elsewhere. These budget templates tend to lack specificity for Canadians. They can be easily modified, however, the upfront work can be frustrating for some.

One potential solution to this problem is the Government of Canada provides a free downloadable spreadsheet template that you can find here. The positives of this option is that it is tailored to Canadians with subsections under savings for accounts such as the TFSA, RRSP, and RESP. However, it is only a monthly budget so you will need to make copies of it for each month.

Alternatively, you could purchase excel templates on a website like Etsy. The price range could be anywhere from $1-$50. These tend to be more visually appealing, easier to use, include added features, and require less upfront time. The only downside is they may include excessive detail which is directed primarily towards business owners. If you decide to take this option, please make sure it is Canadian specific, and has several positive reviews. Additionally, make sure you are able to preview the product before purchasing it.

Government Of Canada- Interactive Tool

The Government of Canada has an interactive tool that you can find here. This is a free budgeting software that you can input your income, savings, and expenses. It provides you with a downloadable spreadsheet once completed. There are few added benefits such as suggestions, and useful links to help you improve your monthly budget. The main downside is you would need to return to this webpage each month in order to repeat your budget.

Apps

Budgeting apps can be beneficial for someone interested in automating the budgeting process.

Key features of these apps is they allow you to safely, and securely link your banking information. Each transaction can be categorized within the app to build your monthly budget. This removes the time demand of manually inputting your income, expenses, and savings into an excel spreadsheet. They typically gamify the process by helping you to establish monthly targets. Lastly, they often provide learning resources to help you make better budgeting decisions.

The primary downside is that they often come at a cost. Additionally, some people report difficulty with integration between their bank and these apps. This is problematic, considering that the goal of a budget is to save you money, and these apps main selling feature is their integration features.

We are not active users of these apps, so we can’t recommend any. We believe you can do everything you need from an excel spreadsheet. However, based on our research, the top 3 budgeting apps that are commonly recommended are the following:

YNAB- $14.99 USD/month

PocketGuard- $6.25 USD/Month

Monarch Money- $8.33 USD/Month

Setting a Savings Rate

Do you really need to save 20%?

You are not going to like this answer… it depends.

How much you need to save depends on your answer to the following questions:

How much have you already saved?

How old are you? (ie. Do you have time for your money to compound)

What are your retirement goals? (ie. How much do you want to live on in retirement).

What is your risk tolerance? (ie. What is your allocation to stocks and other risk assets in your retirement accounts).

We are lucky that there are smart people who have done extensive research on the topic. An article by T-Rowe Price looked at how much you need to save based on your current salary, and age. They found that if you started saving 15% of your salary at age 25, you should be able to save enough for retirement (*). However, the % of your salary that you will need to save increases significantly as you get older. Provided you haven’t already developed a comfortable nest egg. So much so, that those in their 50’s need to save as much as 30% of their after tax income.

Other research done by the MoneyGuy shows that you may need to save as much as 35-40% if you don’t start investing until age 40. This is why starting young is critical to reaching your financial goals.

(*) Based on the assumption that funds are earning 7% annually in investments, and you plan to live off your working salary in retirement.

Start Where You Can

For high income earners, or those with a low spending rate (ie. living with parents, or just plain frugal) these savings targets may be realistic. However, if 15-20% feels impossible right now, don't let that stop you from starting. Even 1% is better than nothing.

If this is you, here is a more realistic progression:

Year 1

Invest $10-$25/month

The goal is to get the ball rolling, develop a savings habit, and start to experience the pleasure of seeing your money grow.

Year 2

Increase your savings rate to 3-5% of your monthly income.

Year 3 and Beyond

Increase your savings rate by 1%/year until you reach your tolerable threshold.

Maintain this until you reach your financial target.

Bonus Points: Every time you get a raise, put half toward lifestyle inflation and half toward increased savings. This way you still improve your life while building your future.

Other Considerations (Pensions, House, Account Types, Inheritance)

It is important to remember that these assumptions are based on the premise that your only source of income in retirement is your investments.

Pensions

In Canada, we have additional support such as the Canadian Pension Plan (CPP) and Old Age Security (OAS). Also, you may have a work pension that you contribute to. Both of these income sources will reduce the amount you need to save for retirement.

House

A common strategy is for retirees to sell their primary residence and rent in retirement. If your mortgage is paid off then your housing expenses are very low, which means you need less to live off of. However, a sale of your home could provide you with a comfortable nest egg, especially with current house prices in Canada. If you are able to rent at a reasonable price, the funds could go a long way. Whatever you plan to do will also impact how much you need to save for retirement.

Account Types

The amount you need to save depends significantly on where the funds are invested.

Investments in your Registered Retirement Savings Plan (RRSP) and Taxable Accounts will be subjected to different forms of taxation. These taxes require you to withdraw a larger amount in order to receive the same “bang for your buck" as the Tax Free Savings Account (TFSA). If you are in your 30’s or younger right now, it is not unrealistic for you to be able to achieve a TFSA account balance of over $1 million in retirement. This means that you could live almost entirely off the funds from this account… depending on your needs of course.

Ex. Two brothers Mike and Mark, who live in Ontario, both withdraw $50,000 from their investment accounts in 2024. They both weren’t receiving any other income. Mike withdrew the funds from his RRSP, while Mark opted to withdraw them from his TFSA. Unfortunately, both didn’t benefit equally from this decision. Instead they ended up living on the following after tax incomes:

Mike- $39,975

$50,000 (RRSP Withdrawal) - $10,025 (Income tax)

Mark- $50,000

Inheritance

Receiving an inheritance is something that we never want to occur, because it means we have lost a loved one. In our opinion, you shouldn’t bank on it, because it may never occur. However, if you are almost certain that it will occur, this will also impact your retirement needs and your required savings targets.

Common Budgeting Mistakes to Avoid

Being Too Restrictive

The fastest way to abandon your budget is to make it too restrictive that you feel deprived. Instead, you need to create some flexibility. In order to do so, you could create a category called “fun money”. This could be used to pay for events, activities, or items that bring you joy (ex. video games).

Also, set a reasonable savings rate that is something you can stick with. A sustainable 10% savings rate is better than an unsustainable 20% rate.

Not Planning for Irregular Expenses

If you are like most people, you drive your car to work every day hoping that it doesn’t need to be repaired. As my mom used to say “when you hear a sound you don’t like, you just turn the radio up”. When the inevitable day comes that the repair needs to be done, you begrudge it. Unfortunately, people do this with a lot of different expenses in their lives.

The truth is expenses such as car repairs, home maintenance, gifts, and annual insurance payments aren't emergencies. They are actually predictable irregular expenses. If the average life on your brand of water heater is 10 years, you can reasonably estimate that you will need a new one in 10 years.

Create a "sinking fund" by setting aside money monthly for these predictable surprises. If you own a home the rule of thumb is that you should save 1% of the home value per year in order to deal with regular maintenance (ie. $800,000 = $8,000/year).

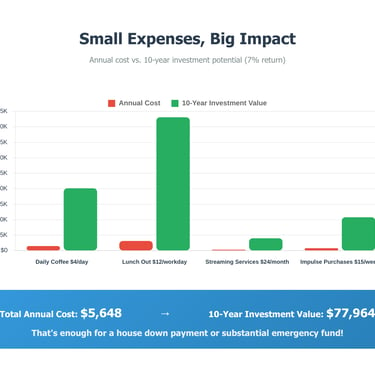

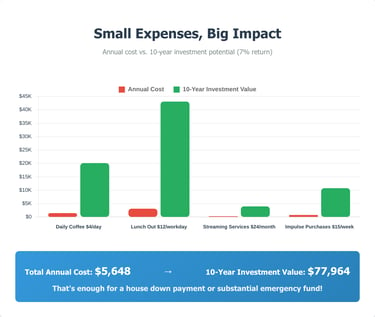

Ignoring Small Expenses

If your goal is to lose weight, one of the first steps is tracking your calories. However, people are chronic “under reporters”. They think the chocolate cookie they ate after lunch won’t make a big difference. Well I have news for you… it does.

You want to treat your budget, like calorie tracking. Every expense has to be recorded, so that you can actually determine how much of your money is being spent. Those $7.99/month app subscriptions, and $4 morning coffees add up quickly. Here's how common small expenses add up and what they could become if invested instead:

Audit your subscriptions quarterly, and cancel anything you're not actively using.

Underestimating Expenses

Have you ever met someone that doesn’t have a clue what items cost anymore? It is usually an older man that maybe his wife or kids do the shopping now. He still thinks you can buy a bag of chips for 50c. I don’t blame him actually… costs have increased significantly.

When making your budget though, you don’t want to be that guy. Instead you have to be realistic with what items cost in your life. This is why you have to develop a baseline of expenses first. Planning to spend $50/month on eating out, when you normally spend $400/month is unrealistic.

Look at your actual spending history rather than what you think you should spend. It's better to overestimate, and have money left over than constantly blow your budget.

Building Your Emergency Fund

"The most important part of every plan is planning on your plan not going according to plan”- Morgan Housel

Before you start investing, or pay extra on your debt payments it is important that you first develop an emergency fund. This is your financial safety net that prevents you from going into debt (or further into debt) when life situations happen.

Although your budget can be used to plan for most expenses, there are some situations that we just can’t plan for (Ex. Laid off from work). The emergency fund is for when your plan doesn’t go according to plan, as Morgan Housel would say.

How Much Do You Need?

The standard advice is 3-6 months of expenses, but this depends on your situation:

Stable job, dual income: 3 months might be sufficient

Variable income, single income household: Aim for 6+ months

Self-employed: Consider 9-12 months

If this amount seems like a lot for you right now, then start with a goal of $1,000 saved. Gradually work toward one month of expenses, then build from there.

It is important that you calculate the amount you need according to basic necessities. If you aren’t working your expenses for food, transportation, and clothing should decrease. You may even choose to further tighten the belt by pausing subscriptions. In a situation where you need your emergency fund, you shouldn’t be spending the same as you currently are.

Where to Keep It

Your emergency fund should be easily accessible but separate from your daily banking.

High-interest savings account (EQ Bank often offers competitive rates)

Money market funds

Cashable GICs

Don't invest your emergency fund in stocks or other volatile investments. The point is stability and accessibility, not growth.

Conclusion

Budgeting isn't about restriction, it's about freedom to spend on what matters without guilt. A budget helps you work towards your goals instead of just surviving paycheck to paycheck. Your first budget won't be perfect, and that's fine. The goal is building the habit, and awareness that will serve you for life. Personal finance is exactly that… personal. So adapt these principles to your unique situation. The best time to start was yesterday, the second-best time is today.

If you like this post you may also like:

[Charlie Munger Was Right: Why the First $100K Matters Most]

[4 Financial Lessons Traveling Taught Me About Money and Happiness]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Financial Consumer Agency of Canada. (n.d.). Budget planner. Government of Canada. https://itools-ioutils.fcac-acfc.gc.ca/BP-PB/budget-planner

Financial Consumer Agency of Canada. (n.d.). Budgeting spreadsheet. My Money Coach. https://mymoneycoach.ca/budgeting/budgeting-calculators-tools/budgeting-spreadsheet

Housel, M. (2020). The psychology of money: Timeless lessons on wealth, greed, and happiness. Harriman House.

Maggiulli, N. (2021). Just keep buying: Proven ways to save money and build your wealth. Harriman House.

Statistics Canada. (2023, May 2). Survey of household spending, 2021. https://www150.statcan.gc.ca/n1/daily-quotidien/230502/dq230502a-eng.htm

Statistics Canada. (2023, July 13). Distributions of household economic accounts, income, consumption and saving of households, second quarter 2023. https://www150.statcan.gc.ca/n1/pub/11-627-m/11-627-m2023056-eng.htm

The Money Guy Show. (n.d.). Financial order of operations. https://www.moneyguy.com/

T. Rowe Price. (n.d.). Retirement planning guidelines. https://www.troweprice.com/

Warren, E., & Tyagi, A. W. (2003). The two-income trap: Why middle-class mothers and fathers are going broke. Basic Books.

Introduction

If you've ever reached the end of the month wondering where all your money went, this guide is for you. Whether you're drowning in debt, living paycheck to paycheck, or just want to be more strategic with your finances, we'll walk you through everything you need to know about budgeting using real Canadian numbers and practical tools you can start using today.

What is Budgeting?

“The highest form of wealth is the ability to wake up every morning and say, ‘I can do whatever I want today.’”- Morgan Housel

Budgeting is simply creating a plan for how you’ll use your money. It’s about deciding ahead of time where each dollar will go so that your spending matches your priorities. A budget doesn’t have to feel restrictive. Instead, it gives you control. It allows you to better align your values with your spending habits. The objective is that by laying out your income, expenses, savings, and debt payments you can develop a roadmap to reaching your financial goals with less stress.

Why Does Budgeting Matter?

In recent years, budgeting has become increasingly more important for the average Canadian. Factors such as the rising cost of living, increasing debt levels, and a slow wage growth have increased the financial burden for many households. Between the years 2010 and 2024:

Overall prices have increased by 38%, as measured by the Consumer Price Index (CPI)

Average real wages (inflation-adjusted) have only increased by 10-11%.

In 2024 dollars, the 2010 average hourly wage was $31.90, and it has since increased to $35.20.

The average household debt increased from 159-160% of household income to 175-185% of household income.

The average house price in Canada has more than doubled.

$339,100 (2010) vs $694,173 (2024)

Unfortunately, this has created significant friction amongst competing financial demands. We have to now be more selective with where our limited financial resources are allocated. Hence why setting up a budget is so important to helping you reach your financial goals.

How to Make A Budget (Step-by Step)

“You don’t have to optimize everything. You just have to avoid the big mistakes.”- Nick Maggiulli

We will dive further into each of the sub-categories throughout this blog. However, the following is an overview of the 6-step process of developing a budget:

Know your income

Track your expenses

Set priorities

Create categories and assign money

Automate allocation

Review and adjust

Know your Income

There are two very important numbers you should be aware of regarding your income:

How much you make before taxes, benefits, and pensions (Gross Income).

How much you make after taxes, benefits, and pensions (Net Income).

Both are important (as you will see later in this blog), but in your day to day life, the only number that really matters is how much you take home (ie. Net income). It is recommended that you know your monthly income amounts because many expenses in life occur at this frequency (ex. Rent and Bills).

For example: Judy earns $60,000/year (Gross Income) at her job as an administrative assistant in Ontario. Based on this income, she thinks that she will have $5,000 per month to spend (ie. $60,000/12). However, in reality she has to pay income taxes, CPP, and EI. This brings her take home pay closer to $47,000/year (Net Income), or approx $3,900/month. This $1,100 difference is significant when she tries to balance her budget

A Word On Variable Pay

Many employed individuals will receive a consistent income stream each month making it easy to track. However, there are occupations that do not provide this luxury.

Self-employed, or commission-based workers often receive highly variable income where they make a lot one month, and almost nothing the next. On the other hand, seasonal workers such as those in the fishing and farming industry earn most, or all of their income in only a few months. If you are in one of these categories, the best way to calculate your monthly income is using your average monthly income:

Annual Net Income (Prior Year)/ 12 months = Average Monthly Income

If you have multiple years in the industry, this is even better, because you can calculate your average annual income from the last three years.

Unfortunately, regardless of your calculation there is always a risk in these occupations that your actual income is below your projected income (Ex. Real Estate Industry when interest rates are high). This is why it is particularly important that you have a financial safety net in the form of an emergency fund.

Track your Expenses

The next step in the process of building a budget is to track your expenses.

Often, we have no understanding of how much of our money is being spent. In some cases, we even spend more than we earn which is why consumer debt has increased. Even if you are good with your money, you may have certain financial objectives you would like to achieve. This could be going on a trip to Europe, buying your first house, paying for your children's schooling, or investing for retirement. By getting a grip of where your money is being spent, you can choose to redirect to the areas that matter to you in order to achieve your goals.

Developing a Baseline

When making your budget it is important to gather at least 3 months of expenses initially.

Although there will be many aspects of your budget that are consistent, you won’t spend the exact same amount each month. We often make irregular purchases that don’t occur every week, or month. If you shop at Costco, you know this experience all too well. Every few visits you have to restock up on items such as toilet paper, paper towel, laundry detergent, cooking oil, etc, but there are times when you buy items that are not on the shopping list. When you do this, your bill increases significantly. Add to this that you may incur unpredictable expenses such as a car or house repair that may be missed when tracking for only a few weeks.

If you do all your spending using cards and online banking, you can develop your budget today using your last three months expenses. However, if you make purchases using cash, it's best to track the next three months.

Categories of Expenses

When tracking your expenses, it is important to organize them into categories. This helps you to see clearly, not just how much you are spending, but where the funds are being spent.

There are several budget templates that you can find online. However, we like to separate ours into the following sections:

Savings & Investing

Debt Repayment

Housing Expenses

Food

Transportation

Travel

Personal Care

Leisure and Entertainment

After developing your broad categories, you can increase clarity in your expenses by adding subcategories.

Set Priorities

After you have tracked your expenses, the next step is to figure out where you want to spend your money going forward.

There should be an emphasis directed towards saving for your retirement, and reaching financial freedom. You may have additional goals you would like to achieve such as home ownership, or travel. Regardless of what they are, we need to set priorities in our budget. This involves identifying how much we should spend in each category in order to achieve those goals.

Here's a simple exercise to help clarify your priorities. List your top 3 financial goals and categorize them as:

Short-term (1-3 years)- Ex. Emergency fund, vacation, car down payment

Medium-term (3-10 years)- Ex. House down payment, children's education

Long-term (10+ years)- Ex. Retirement, financial independence

Your budget should reflect your priorities. If home ownership is your biggest goal, housing-related savings should get priority over entertainment spending.

Create Categories & Assign Money

How much to Budget for Each Category

If you have read any personal finance books, you have inevitably come across several rules of thumb in terms of how much to budget for each category. The most popular of which is likely the 50/30/20 Rule created by Elizabeth Warren (yes the US Senator). This rule suggests that your budget should consist of:

50% Needs

Housing, food, transportation, insurance, phone and car bills.

30% Wants

Entertainment, travel, dining out

20% Wealth Generation

Savings (emergency fund, & retirement accounts)

Debt Repayment

Other financial experts will recommend different variations of this same calculation. However, in almost all cases the amount allocated to each category is within 5-10% of the numbers stated above.

Example: Imagine Judy earns $4,000/month net income. She may do the following allocation:

50% Needs ($2,000)

Rent ($1,200), Groceries ($300), Transportation ($200), Utilities/Phone ($200), Insurance ($100)

30% Wants ($1,200)

Dining out ($300), Entertainment ($200), Hobbies ($300), Miscellaneous ($400)

20% Savings/Debt ($800)

Emergency fund ($300), TFSA ($300), Debt payments ($200)

What about Canada?

Although these hard and fast rules are helpful as general guidelines, they may not be appropriate for you. Many of these were created by individuals in the USA where cost of living is significantly different than Canada. According to Statistics Canada, in their Survey of Household Spending, Canadians spent an average of the following in 2023:

$24,671 on Shelter

$8,659 on Groceries

$12,090 on Transportation

$9,404 on Household operations, furnishings, and equipment

Total = $54,824

Meanwhile, the median after-tax family income was $72,400 in 2023.

Based on these figures the average Canadian spent almost 76% of their take home income on their needs. In order to reach the coveted 20% savings, you would only have 4% left for wants…. you better enjoy dollar store arts and crafts.

A more realistic Canadian allocation for that same $4,000/month net income may look like this :

65% Needs ($2,600)

Housing ($1,650, Groceries ($325), Transportation ($275), Utilities/phone ($225), Insurance ($125)

20% Wants ($800):

Dining out ($300), Entertainment ($100), Hobbies ($200), Miscellaneous ($200)

15% Savings/Debt ($600)

Emergency fund ($200), TFSA ($200), Debt payments ($200)

Debt Repayment

For many people, an important reason to create a budget is to get out of debt.

A high amount of debt, especially high interest debt, can do significant damage to your financial future. As we noted above, there is already limited room in the average Canadian’s budget due to high cost of living. Debt can drain your cash flow, limit your ability to save, and cause you a lot of stress.

Budgeting gives you a plan so you can consistently make progress and eventually free yourself from this burden.

Good Debt vs Bad Debt

Although all debt weighs down your budget, there should be a delineation between different types of debt.

Good debt is when you borrow money to spend on something that is expected to appreciate in value, or provide some monetary benefit. These would be things like purchasing a house, stocks, or business related expenses. How good the debt is exists on a spectrum. For example, we could say using debt to purchase a rental property would be better than a primary residence because it produces near term cash flows.

Bad debt is when you borrow money to spend on something that will decrease in value. This could include things such as car loans, credit cards, pay day loans, etc. Similarly, bad debts exist on a spectrum. A car may provide utility especially for an individual that doesn’t live close to their work. However, some consumer debt with very high interest rates would fall into the very bad debt category.

Debt Payoff Strategies

Most loans will require you to make regular payments over a predetermined time period. However, the problem for many people is that they start to accumulate multiple of these debts each of which eats into their monthly budget. The two most common approaches to repaying debt are:

Snowball Method

This was made popular by a popular figure in the personal finance community named Dave Ramsay.

This method recommends focusing on paying off the smallest debt first while making minimum payments on all others. Once the first debt is gone, move on to the next smallest. This method helps with the emotional management of debt repayment, by developing quick wins and building momentum.

Avalanche Method

Focus on paying off the debt with the highest interest rate first while making minimum payments on the rest. This approach saves you the most money in interest over time.

Neither method is “right” or “wrong.” The best strategy is the one that you will stick with consistently.

Why Extra Payments Matter

Adding even a small amount to your debt payments each month can drastically shorten your timeline.

Example: If you owe $10,000 on a credit card at 19% interest and make only the minimum $250 monthly payment, it will take about 5 years to pay off. If you add just $150 more each month, you’ll be debt-free in under 3 years and save thousands in interest

Fixed vs Variable Costs

When making your budget, it's helpful to separate your spending into two categories: fixed and variable costs.

Fixed costs are regular expenses that don’t change much from month to month. However, they are harder to remove without consequences. These include things such as mortgage or rent, phone or internet bill, utilities, groceries, car payment, house or car insurance, etc.

Variable costs are expenses that are more flexible and easier to adjust. These include things such as dining out, clothing, entertainment, vacations, subscriptions, etc. For example: A morning coffee from your local cafe may be convenient, but you can also make it at home for a fraction of the price.

If you don’t have enough disposable cash each month, you will need to find a way to reduce spending. Start by trimming variable costs like dining out, subscriptions, or daily coffee runs. These little expenses can free up quick cash to be directed towards your goals.

However, these small cuts can only go so far. If your housing and debt repayment expenses take up most of your income, you may need to tackle fixed costs instead. This may require measures such as renegotiating bills, debt consolidation, and shopping for discount food. In some cases, you may need to take extreme measures such as downsizing, or selling your car.

Ex. Skipping your $4 coffee each workday saves you approx $80/month. This is a lot of money, however, it won’t matter much if your mortgage already takes up 70% of your income.

Automate Allocation

Once you've created your budget categories and assigned dollar amounts, the next step is to make it as effortless as possible to stick to your plan. This is where automation becomes your best friend.

Set Up Automatic Transfers

The moment your pay cheque hits your account, you want your money automatically flowing to where it needs to go. You can easily set up automatic transfer for the following:

Emergency fund savings

Have a designated high interest savings account that you will title “Emergency Fund”.

Investment accounts:

Debt payments:

Mortgage, car loan, line of credit, and credit card

Bills:

Rent, utilities, insurance, phone

Most Canadian banks offer free automatic transfers, and you can usually set these up online in minutes. For utilities, internet, phone, and insurance you can set-up automatic payment through the provider. Similarly, you can do the same through your lender for loans.

Use the "Pay Yourself First" Strategy

Instead of saving what is left over at the end of the month (spoiler alert: there's usually nothing left), treat your savings like a non-negotiable bill. When you get paid your savings get paid first, then you can live off the remainder. If you have difficulty living off what is left, then either your savings rate is too high, or you are spending too much.

Separate Accounts for Different Goals

Consider opening separate savings accounts for different goals:

Emergency fund

Vacation fund

House down payment

New car fund

Since most of these are short term savings goals, they shouldn’t be invested in risk assets such as stocks. Instead you can look for good high interest savings accounts (HISA’s) like those offered at EQ Bank. If you have a planned date for when you want to use the funds, Guaranteed Interest Certificates (GIC’s) offer a good option as well.

Many banks allow you to nickname these accounts too (“Europe Trip 2025" or "Emergency Fund"). Seeing your progress toward specific goals is incredibly motivating.

Practical Tools and Resources

Building a budget initially seems as if it would be very time intensive. And, it would be if you had to track all of the information using pen and paper in an unorganized notebook. Lucky for you, this is not the case. In fact there are several amazing resources that exist to help you in this process.

Spreadsheets

There are several options in terms of spreadsheets that could range from completely free…up to expensive products.

In google sheets, there is a free to access template titled “Annual Budget". It provides a tracking sheet for your expenses, and income sources for an entire year. Also, it includes a summary sheet to compare expenses and income. Each category has several subcategories to help you better organize your finances. You can find similar templates on Microsoft office and elsewhere. These budget templates tend to lack specificity for Canadians. They can be easily modified, however, the upfront work can be frustrating for some.

One potential solution to this problem is the Government of Canada provides a free downloadable spreadsheet template that you can find here. The positives of this option is that it is tailored to Canadians with subsections under savings for accounts such as the TFSA, RRSP, and RESP. However, it is only a monthly budget so you will need to make copies of it for each month.

Alternatively, you could purchase excel templates on a website like Etsy. The price range could be anywhere from $1-$50. These tend to be more visually appealing, easier to use, include added features, and require less upfront time. The only downside is they may include excessive detail which is directed primarily towards business owners. If you decide to take this option, please make sure it is Canadian specific, and has several positive reviews. Additionally, make sure you are able to preview the product before purchasing it.

Government Of Canada- Interactive Tool

The Government of Canada has an interactive tool that you can find here. This is a free budgeting software that you can input your income, savings, and expenses. It provides you with a downloadable spreadsheet once completed. There are few added benefits such as suggestions, and useful links to help you improve your monthly budget. The main downside is you would need to return to this webpage each month in order to repeat your budget.

Apps

Budgeting apps can be beneficial for someone interested in automating the budgeting process.

Key features of these apps is they allow you to safely, and securely link your banking information. Each transaction can be categorized within the app to build your monthly budget. This removes the time demand of manually inputting your income, expenses, and savings into an excel spreadsheet. They typically gamify the process by helping you to establish monthly targets. Lastly, they often provide learning resources to help you make better budgeting decisions.

The primary downside is that they often come at a cost. Additionally, some people report difficulty with integration between their bank and these apps. This is problematic, considering that the goal of a budget is to save you money, and these apps main selling feature is their integration features.

We are not active users of these apps, so we can’t recommend any. We believe you can do everything you need from an excel spreadsheet. However, based on our research, the top 3 budgeting apps that are commonly recommended are the following:

YNAB- $14.99 USD/month

PocketGuard- $6.25 USD/Month

Monarch Money- $8.33 USD/Month

Setting a Savings Rate

Do you really need to save 20%?

You are not going to like this answer… it depends.

How much you need to save depends on your answer to the following questions:

How much have you already saved?

How old are you? (ie. Do you have time for your money to compound)

What are your retirement goals? (ie. How much do you want to live on in retirement).

What is your risk tolerance? (ie. What is your allocation to stocks and other risk assets in your retirement accounts).

We are lucky that there are smart people who have done extensive research on the topic. An article by T-Rowe Price looked at how much you need to save based on your current salary, and age. They found that if you started saving 15% of your salary at age 25, you should be able to save enough for retirement (*). However, the % of your salary that you will need to save increases significantly as you get older. Provided you haven’t already developed a comfortable nest egg. So much so, that those in their 50’s need to save as much as 30% of their after tax income.

Other research done by the MoneyGuy shows that you may need to save as much as 35-40% if you don’t start investing until age 40. This is why starting young is critical to reaching your financial goals.

(*) Based on the assumption that funds are earning 7% annually in investments, and you plan to live off your working salary in retirement.

Start Where You Can

For high income earners, or those with a low spending rate (ie. living with parents, or just plain frugal) these savings targets may be realistic. However, if 15-20% feels impossible right now, don't let that stop you from starting. Even 1% is better than nothing.

If this is you, here is a more realistic progression:

Year 1

Invest $10-$25/month

The goal is to get the ball rolling, develop a savings habit, and start to experience the pleasure of seeing your money grow.

Year 2

Increase your savings rate to 3-5% of your monthly income.

Year 3 and Beyond

Increase your savings rate by 1%/year until you reach your tolerable threshold.

Maintain this until you reach your financial target.

Bonus Points: Every time you get a raise, put half toward lifestyle inflation and half toward increased savings. This way you still improve your life while building your future.

Other Considerations (Pensions, House, Account Types, Inheritance)

It is important to remember that these assumptions are based on the premise that your only source of income in retirement is your investments.

Pensions

In Canada, we have additional support such as the Canadian Pension Plan (CPP) and Old Age Security (OAS). Also, you may have a work pension that you contribute to. Both of these income sources will reduce the amount you need to save for retirement.

House

A common strategy is for retirees to sell their primary residence and rent in retirement. If your mortgage is paid off then your housing expenses are very low, which means you need less to live off of. However, a sale of your home could provide you with a comfortable nest egg, especially with current house prices in Canada. If you are able to rent at a reasonable price, the funds could go a long way. Whatever you plan to do will also impact how much you need to save for retirement.

Account Types

The amount you need to save depends significantly on where the funds are invested.

Investments in your Registered Retirement Savings Plan (RRSP) and Taxable Accounts will be subjected to different forms of taxation. These taxes require you to withdraw a larger amount in order to receive the same “bang for your buck" as the Tax Free Savings Account (TFSA). If you are in your 30’s or younger right now, it is not unrealistic for you to be able to achieve a TFSA account balance of over $1 million in retirement. This means that you could live almost entirely off the funds from this account… depending on your needs of course.

Ex. Two brothers Mike and Mark, who live in Ontario, both withdraw $50,000 from their investment accounts in 2024. They both weren’t receiving any other income. Mike withdrew the funds from his RRSP, while Mark opted to withdraw them from his TFSA. Unfortunately, both didn’t benefit equally from this decision. Instead they ended up living on the following after tax incomes:

Mike- $39,975

$50,000 (RRSP Withdrawal) - $10,025 (Income tax)

Mark- $50,000

Inheritance

Receiving an inheritance is something that we never want to occur, because it means we have lost a loved one. In our opinion, you shouldn’t bank on it, because it may never occur. However, if you are almost certain that it will occur, this will also impact your retirement needs and your required savings targets.

Common Budgeting Mistakes to Avoid

Being Too Restrictive

The fastest way to abandon your budget is to make it too restrictive that you feel deprived. Instead, you need to create some flexibility. In order to do so, you could create a category called “fun money”. This could be used to pay for events, activities, or items that bring you joy (ex. video games).

Also, set a reasonable savings rate that is something you can stick with. A sustainable 10% savings rate is better than an unsustainable 20% rate.

Not Planning for Irregular Expenses

If you are like most people, you drive your car to work every day hoping that it doesn’t need to be repaired. As my mom used to say “when you hear a sound you don’t like, you just turn the radio up”. When the inevitable day comes that the repair needs to be done, you begrudge it. Unfortunately, people do this with a lot of different expenses in their lives.

The truth is expenses such as car repairs, home maintenance, gifts, and annual insurance payments aren't emergencies. They are actually predictable irregular expenses. If the average life on your brand of water heater is 10 years, you can reasonably estimate that you will need a new one in 10 years.

Create a "sinking fund" by setting aside money monthly for these predictable surprises. If you own a home the rule of thumb is that you should save 1% of the home value per year in order to deal with regular maintenance (ie. $800,000 = $8,000/year).

Ignoring Small Expenses

If your goal is to lose weight, one of the first steps is tracking your calories. However, people are chronic “under reporters”. They think the chocolate cookie they ate after lunch won’t make a big difference. Well I have news for you… it does.

You want to treat your budget, like calorie tracking. Every expense has to be recorded, so that you can actually determine how much of your money is being spent. Those $7.99/month app subscriptions, and $4 morning coffees add up quickly. Here's how common small expenses add up and what they could become if invested instead:

Audit your subscriptions quarterly, and cancel anything you're not actively using.

Underestimating Expenses

Have you ever met someone that doesn’t have a clue what items cost anymore? It is usually an older man that maybe his wife or kids do the shopping now. He still thinks you can buy a bag of chips for 50c. I don’t blame him actually… costs have increased significantly.

When making your budget though, you don’t want to be that guy. Instead you have to be realistic with what items cost in your life. This is why you have to develop a baseline of expenses first. Planning to spend $50/month on eating out, when you normally spend $400/month is unrealistic.

Look at your actual spending history rather than what you think you should spend. It's better to overestimate, and have money left over than constantly blow your budget.

Building Your Emergency Fund

"The most important part of every plan is planning on your plan not going according to plan”- Morgan Housel

Before you start investing, or pay extra on your debt payments it is important that you first develop an emergency fund. This is your financial safety net that prevents you from going into debt (or further into debt) when life situations happen.

Although your budget can be used to plan for most expenses, there are some situations that we just can’t plan for (Ex. Laid off from work). The emergency fund is for when your plan doesn’t go according to plan, as Morgan Housel would say.

How Much Do You Need?

The standard advice is 3-6 months of expenses, but this depends on your situation:

Stable job, dual income: 3 months might be sufficient

Variable income, single income household: Aim for 6+ months

Self-employed: Consider 9-12 months

If this amount seems like a lot for you right now, then start with a goal of $1,000 saved. Gradually work toward one month of expenses, then build from there.

It is important that you calculate the amount you need according to basic necessities. If you aren’t working your expenses for food, transportation, and clothing should decrease. You may even choose to further tighten the belt by pausing subscriptions. In a situation where you need your emergency fund, you shouldn’t be spending the same as you currently are.

Where to Keep It

Your emergency fund should be easily accessible but separate from your daily banking.

High-interest savings account (EQ Bank often offers competitive rates)

Money market funds

Cashable GICs

Don't invest your emergency fund in stocks or other volatile investments. The point is stability and accessibility, not growth.

Conclusion

Budgeting isn't about restriction, it's about freedom to spend on what matters without guilt. A budget helps you work towards your goals instead of just surviving paycheck to paycheck. Your first budget won't be perfect, and that's fine. The goal is building the habit, and awareness that will serve you for life. Personal finance is exactly that… personal. So adapt these principles to your unique situation. The best time to start was yesterday, the second-best time is today.

If you like this post you may also like:

[What Is a GIC and How Does It Work in Canada? (2025 Guide)]

[Charlie Munger Was Right: Why the First $100K Matters Most]

[4 Financial Lessons Traveling Taught Me About Money and Happiness]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Financial Consumer Agency of Canada. (n.d.). Budget planner. Government of Canada. https://itools-ioutils.fcac-acfc.gc.ca/BP-PB/budget-planner

Financial Consumer Agency of Canada. (n.d.). Budgeting spreadsheet. My Money Coach. https://mymoneycoach.ca/budgeting/budgeting-calculators-tools/budgeting-spreadsheet

Housel, M. (2020). The psychology of money: Timeless lessons on wealth, greed, and happiness. Harriman House.

Maggiulli, N. (2021). Just keep buying: Proven ways to save money and build your wealth. Harriman House.

Statistics Canada. (2023, May 2). Survey of household spending, 2021. https://www150.statcan.gc.ca/n1/daily-quotidien/230502/dq230502a-eng.htm

Statistics Canada. (2023, July 13). Distributions of household economic accounts, income, consumption and saving of households, second quarter 2023. https://www150.statcan.gc.ca/n1/pub/11-627-m/11-627-m2023056-eng.htm

The Money Guy Show. (n.d.). Financial order of operations. https://www.moneyguy.com/

T. Rowe Price. (n.d.). Retirement planning guidelines. https://www.troweprice.com/

Warren, E., & Tyagi, A. W. (2003). The two-income trap: Why middle-class mothers and fathers are going broke. Basic Books.