Get our free Debt vs Invest Calculator — click here to access it

Charlie Munger Was Right: Why the First $100K Matters Most

Learn why Charlie Munger stressed saving your first $100K—and how compound interest makes it the most important financial milestone on your journey to wealth.

INVESTING FOR BEGINNERS

5/24/202522 min read

Introduction

In 1990, the late great investor Charlie Munger was asked by a young inspired man the question “How do I create wealth?”. To that, Charlie responded with:

"The first $100,000 is a b**, but you gotta do it. I don’t care what you have to do—if it means walking everywhere and not eating anything that wasn’t purchased with a coupon, find a way to get your hands on $100,000. After that, you can ease off the gas a little bit."- Charlie Munger

For today’s blog, we are going to break down:

Why is saving $100,000 so hard for Canadians?

Why is your first $100,000 critical to your long term wealth building?

How can you accomplish this?

What are some common mistakes people make on their journey to this golden number?

Why the First $100K is the Hardest

Saving the first $100K is the hardest thing you will do on your journey towards financial independence. The reason why comes down to the concept of compounding.

Compound Interest

As we discussed in a previous blog post on investing, compounding is the process by which the interest you earn on your investments works for you and earns interest on itself.

For Example: If you invest $100 in an Exchange Traded Fund (ETF) earning 7% per year. The returns will look like this:

Year 1: $107 ($7 Increase)

Year 2: $114.49 ($7.49 Increase)

Year 3: $122.50 ($8.01 Increase)

Year 4: $131.08 ($8.58 Increase)

As you can see, each subsequent year the growth amount increases with no additional investment. This is because the interest you earned in the previous year is now also earning interest on itself.

Compound interest is amazing over the course of your investing life, however, early on in your investment journey, the impact of compound interest is slow and minimal. Although your money is working for you, you have not yet saved enough money to see a dramatic increase in your net worth. As a result, it takes a long time to reach this $100K target.

For Example: If you started investing $500/month when you were 18 years old, in a low cost index ETF, growing at 7% per year. It would take you until you were 29 years of age (and 2 months) or 11.1 years to reach your first $100K.

Frugality and Discipline

The time frame to reach your first $100K will likely be long. Often times people make the mistake of thinking that they can fast track this process, by trying to find the “optimal” way to invest. Because the numbers are so small early in your investing journey, chasing excess return isn’t very impactful. Add to that, the risk of partial or total loss increases as you focus on chasing returns.

Ex: Imagine you have two people who have $5,000 invested. One person has a 7% return and the other a 10% return.

A 7% annual return= $350

A 10% annual return = $500

As you can see, the excess 3% returns only produced a $150 difference between the two investment portfolios. As a result, we emphasize that the goal early on for most investors should be to increase your income, while reducing your spending in order to maximize your savings. This simple equation is why most of the popular financial “guru’s” focus on budgeting:

Decreased Spending + Increased Income = Maximized Savings

Unfortunately, this period is not just time consuming, but also mentally taxing. It requires you to look at your monthly spending. Then cut out unnecessary activities such as eating out or ordering in, subscriptions, video games, travel, etc. In other words, you have to delay short to medium term satisfaction for long term gain, which is challenging.

The Low Income Problem

Most people will begin their investment journey when they are in their 20's, or early 30’s. At which time, you are likely not in your peak income earning years. Add to this that you may also be dealing with large financial expenses such as student loans, credit card debt, and so on that cut into your savings each month.

Remember the other half of the equation is to increase your income. In order to do this you may be required to pick up a second job, or extra hours at your current one. Regardless of which choice you make, it is highly unlikely that your current income is high enough to speed up the process towards this $100K objective.

So during this time keep trying to stay consistent and not get discouraged. Our message to young Canadians is “Rome wasn’t built in a day”. Your financial situation will likely improve as you get older with a higher income, lower debt, and investing.

Why the First $100k is the Most Important

Compounding on Steroids

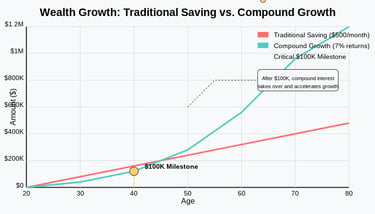

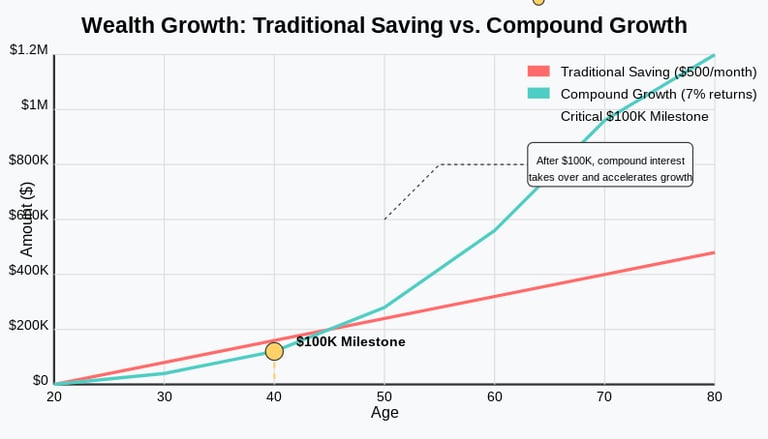

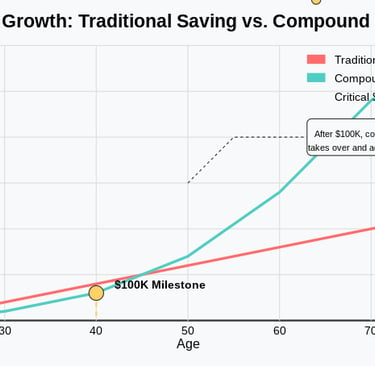

The first $100K is the most important because compound interest starts to perform its magic. At this point you have saved enough money that the incremental returns start to become significant.

Ex. Using our previous example, imagine you are 18 years of age saving $500 per month, and investing it into a low cost index ETF earning 7% per year. Here is what your investment portfolio would look like as you got older:

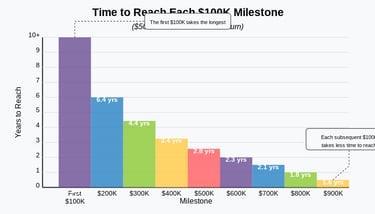

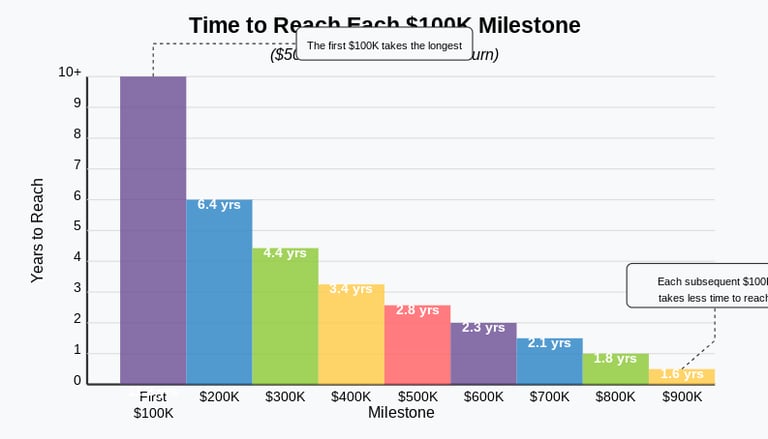

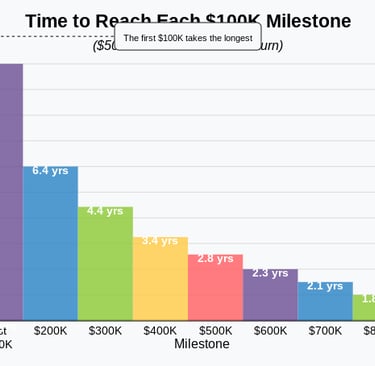

By 29 years of age you will have $100,000 (134 months or 11.16 years)

By 35 years of age you will have $200,000 (75 months or 6.35 years)

By 39 years of age you will have $300,000 (53 months or 4.42 years)

By 43 years of age you will have $400,000 (41 months or 3.41 years)

By 46 years of age you will have $500,000 (33 months or 2.75 years)

By 48 years of age you will have $600,000 (27 months or 2.25 years)

By 50 years of age you will have $700,000 (25 months or 2.08 years)

By 52 years of age you will have $800,000 (21 months or 1.75 years)

By 53 years of age you will have $900,000 (19 months or 1.58 years)

By 55 years of age you will have $1,000,000 (17 months or 1.41 years)

As you can see, due to the wonders of compound interest the time frame to reach each subsequent $100K shortens as you get older. What makes this even more mind blowing is the fact that by the time you reach 55 years of age, of the $1,000,000 you have, only $222,500 is from what you have saved and invested. That means that the remaining $777,500 is all interest. That is compounding on steroids!!!

Positive Psychology

The sad part about hitting your first $100K, is that people feel like they are walking through mud, so they give up and quit before ever achieving this milestone. However, once the compound interest snowball starts to roll (after $100K), each additional $1 of savings starts to feel as if it is producing significant returns. You will no longer feel that you need to work insane hours, or make tough sacrifices to reach your financial goals. Instead you can start to live your life freely knowing that in the background your money is working just as hard (if not even harder) for you as you are.

How to Save your First $100K (Step-by-Step Guide)

The process to save your first $100K is actually very simple… but not easy. The following are the steps you need to take:

Obtain a Primary Job

I do not care if your job is flipping burgers or working in a financial firm. You just need a primary consistent income source. Ideally, the job should be full time with the potential to pick up overtime hours.

Reduce Large Fixed Costs

Most Canadians' three largest fixed costs are rent, transportation, and food.

Rent- Live with your parents, or find roommates.

There are several options for finding roommates such as roomies.ca, kijiji.ca, or roomster.com.

You can also find roommates through mutual friends.

Transportation- If you can’t walk, take the bus. If you can’t take the bus then buy an affordable used car.

There are many options to find a used car such as autotrader.ca, cargurus.ca, or kijijiautos.ca.

When we say used car, we’re not talking about a BMW or Lexus. Make sure it’s reasonable and affordable for your budget. Remember, that a car is only to get you from point A to point B, it’s not supposed to be a wealth status symbol.

Another option is to ask around in your family or friend group. Someone may have a used car they will sell you at a steep discount, or even gift you.

Food- Buy your own groceries and cook your own food at home, as much as possible. I know it is time consuming and inconvenient, but if you want to save money you have to do it. Reserve eating out for special occasions.

Save 25% of net income

Every time you receive a paycheck, take the amount you receive and multiply it by 0.25, that is how much you have to save.

For Example: Imagine you receive two paychecks each month of $1,800, for a total of $3,600. Each time you receive a paycheck you will save $450, for a total of $900/month:

$1,800 x 0.25 (25%) = $450 x 2 = $900

For young Canadians under 30 years old, we know that saving 25% can be aspirational. You can start with saving 10-15% of your gross income (income before taxes) and try to increase it to 25% by age 30.

Invest the money in a low cost index ETF

Open up a TFSA or RRSP with a low cost brokerage firm such as questrade.com or wealthsimple.com.

Set up direct deposit from your primary bank account to the brokerage firm.

Once the money is deposited you can purchase a low cost index ETF such as tickers VFV, VEQT, or VGRO.

Repeat every month.

Increase your earnings vehicles

Overtime

The easiest option would be to pick up additional hours from your primary job.

Secondary Job

You could also pick up a second part time job in order to make extra income.

Side Gig or Small Business

Everyone has a skill that they have not currently monetized.

If you are good at math or science, you could be a tutor.

If you are good at a sport, you could be a skills instructor.

If you are good at art, you could sell artwork.

If you are good with computers, you could troubleshoot for others.

If you are interested in a subject or know a lot about it you can even start a Youtube channel, blog, or podcast.

Even if you don’t have a “specialty” there are several lower skill or easier to learn options such as:

Mowing lawns, shoveling driveways or walkways, reselling, etc.

How to Invest Your First $100K Wisely

On your way to your first $100K, you want your investing to be as simple as possible. Your focus is not on maximizing returns, but rather minimizing the time you need to think about it. This is why buying a low cost, well diversified, index ETF is the best option in our opinion. There are a variety of options such as:

VEQT (or XEQT, ZEQT)

100% Stocks

Globally Diversified

VGRO (or XGRO, ZGRO)

80% Stocks, 20% Bonds

Globally Diversified

VFV

100% Stocks

US Based

Based on extensive research, this remains the most effective way to invest your money regardless of how much you have saved. However, we know that people love to chase returns. If this is you…then once you have saved your first $100K, you can start to venture out into alternative options. You could set aside <5% of your investments for other assets such as:

Individual Stocks

Gold, Silver, or Other Commodities

Cryptocurrencies

Options

However, you have to recognize that this is play money and there is a potential of total or partial loss. Although smart investing decisions can result in phenomenal returns, the more you concentrate your money the greater the risk you expose yourself to.

Common Mistakes to Avoid

The time to reach your first $100K is long, and often difficult. And humans are very poor at tolerating delayed gratification. Consequently, many people make the following mistakes on their way to this $100K target:

Fall Victim to Lifestyle Creep

As people's income and net worth increases, they start to reduce the restrictions on their lifestyle. They purchase a bigger house, or find a nicer place to rent. They may buy a new car instead of a used one. They go on more lavish vacations, buy more expensive clothing, and start to buy food out more.

All of the money they were originally setting aside to save and invest starts to slowly disappear. Or any additional income doesn’t get invested, slowing down the time it takes them to reach their $100K target.

Solution: Automate your finances by setting up direct deposit from your primary bank account to a brokerage firm. If you receive a salary increase, then modify the direct deposit amount immediately.

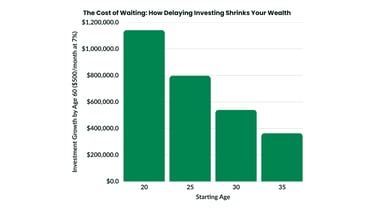

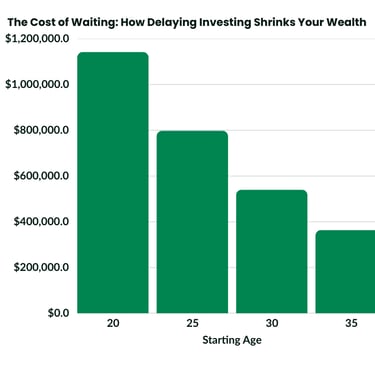

Delaying Investing

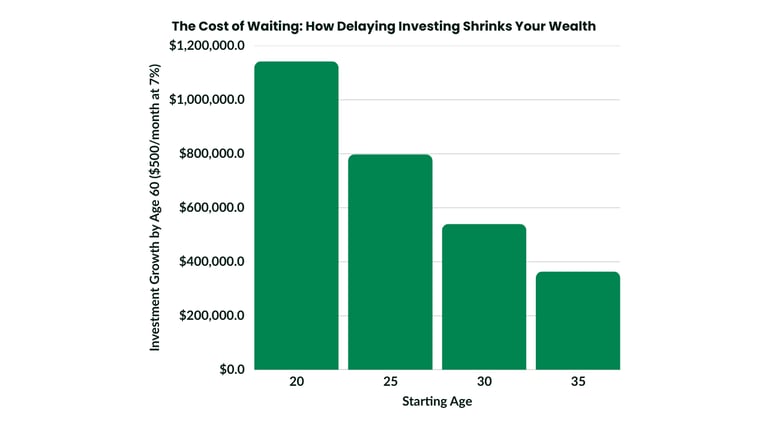

One of the biggest mistakes people make is waiting too long to start investing. Many believe they need a high income, or a large lump sum before getting started. But the truth is, time in the market is far more important than timing the market. The longer you delay, the more you miss out on compound interest working in your favor. Even small monthly investments made early, will grow into significant wealth over decades.

To illustrate this, let’s compare four different investors. All of which invest $500/month in a low-cost index ETF earning 7% annually.

Person A starts at age 20

Person B starts at age 25

Person C starts at age 30

Person D starts at age 35

As you can see, even waiting 5 years makes a substantial difference in your long term investment outcomes.

Solution: Start investing today, even if it’s just $50 or $100 per month. The earlier you begin, the less money you need to contribute over time. Set up automatic deposits into a low-cost index ETF and let time do the heavy lifting.

Chasing Investment Returns

Deciding to listen to the noise, aka a friend, family member, or reddit forum user who tells someone to invest in xyz stock. Although some investments produce good returns, others end up a total disaster. In the end, these people will probably make less than they would have, if they just left their money in a well diversified index ETF.

Solution:

Automate your purchases of the low cost index ETF of choice so that there is no money left to invest in individual stocks.

Leave at least 7 days before making any investment decision. This gives you time to remember the path you are on towards financial freedom.

Get Spooked Out of the Market

They watch their investment accounts constantly, or listen to financial news too much. They forget that ups and downs are a natural process in the stock market, which we call volatility. When the market is down, the news stories are meant to be bleak in order to catch your attention. People get scared and decide to sell their stocks out of fear of loss, they think "it’s better to lose 20% than 100% of my money”. When the issue eventually gets resolved and the news stories improve, the market will starts going back up and they buy back in.

People tend to do the opposite of the old adage “buy low, sell high”, in that they tend to buy high after stocks have gone up a lot and sell low when the market starts to go down. The result is they receive much worse returns than if they just left their portfolio alone and did nothing.

Solution:

If you’re an emotional person, remove your brokerage account from your phone, only access it on your desktop.

When things are really bleak, type in “S&P 500 Index Historical Chart” on google. Seeing the long term performance of the market will make you feel better

Conclusion

Saving and investing your first $100K is the hardest step—but also the most important. It’s the foundation that sets you up for long-term wealth, thanks to the magic of compound interest. Yes, it requires discipline, sacrifices, and patience, but once you reach this milestone, the journey gets exponentially easier.

Instead of chasing quick gains or over-complicating your investments, focus on the fundamentals: earn more, spend less, invest consistently. Stick to this formula, and your financial freedom will come sooner than you think.

🚀 What’s your biggest challenge in reaching your first $100K? Drop a comment below!

If you found this guide helpful, share it with someone who needs to hear this message!

If you liked this post you may also like:

Introduction

In 1990, the late great investor Charlie Munger was asked by a young inspired man the question “How do I create wealth?”. To that, Charlie responded with:

"The first $100,000 is a b**, but you gotta do it. I don’t care what you have to do—if it means walking everywhere and not eating anything that wasn’t purchased with a coupon, find a way to get your hands on $100,000. After that, you can ease off the gas a little bit."- Charlie Munger

For today’s blog, we are going to break down:

Why is saving $100,000 so hard for Canadians?

Why is your first $100,000 critical to your long term wealth building?

How can you accomplish this?

What are some common mistakes people make on their journey to this golden number?

Why the First $100K is the Hardest

Saving the first $100K is the hardest thing you will do on your journey towards financial independence. The reason why comes down to the concept of compounding.

Compound Interest

As we discussed in a previous blog post on investing, compounding is the process by which the interest you earn on your investments works for you and earns interest on itself.

For Example: If you invest $100 in an Exchange Traded Fund (ETF) earning 7% per year. The returns will look like this:

Year 1: $107 ($7 Increase)

Year 2: $114.49 ($7.49 Increase)

Year 3: $122.50 ($8.01 Increase)

Year 4: $131.08 ($8.58 Increase)

As you can see, each subsequent year the growth amount increases with no additional investment. This is because the interest you earned in the previous year is now also earning interest on itself.

Compound interest is amazing over the course of your investing life, however, early on in your investment journey, the impact of compound interest is slow and minimal. Although your money is working for you, you have not yet saved enough money to see a dramatic increase in your net worth. As a result, it takes a long time to reach this $100K target.

For Example: If you started investing $500/month when you were 18 years old, in a low cost index ETF, growing at 7% per year. It would take you until you were 29 years of age (and 2 months) or 11.1 years to reach your first $100K.

Frugality and Discipline

The time frame to reach your first $100K will likely be long. Often times people make the mistake of thinking that they can fast track this process, by trying to find the “optimal” way to invest. Because the numbers are so small early in your investing journey, chasing excess return isn’t very impactful. Add to that, the risk of partial or total loss increases as you focus on chasing returns.

Ex: Imagine you have two people who have $5,000 invested. One person has a 7% return and the other a 10% return.

A 7% annual return= $350

A 10% annual return = $500

As you can see, the excess 3% returns only produced a $150 difference between the two investment portfolios. As a result, we emphasize that the goal early on for most investors should be to increase your income, while reducing your spending in order to maximize your savings. This simple equation is why most of the popular financial “guru’s” focus on budgeting:

Decreased Spending + Increased Income = Maximized Savings

Unfortunately, this period is not just time consuming, but also mentally taxing. It requires you to look at your monthly spending. Then cut out unnecessary activities such as eating out or ordering in, subscriptions, video games, travel, etc. In other words, you have to delay short to medium term satisfaction for long term gain, which is challenging.

The Low Income Problem

Most people will begin their investment journey when they are in their 20's, or early 30’s. At which time, you are likely not in your peak income earning years. Add to this that you may also be dealing with large financial expenses such as student loans, credit card debt, and so on that cut into your savings each month.

Remember the other half of the equation is to increase your income. In order to do this you may be required to pick up a second job, or extra hours at your current one. Regardless of which choice you make, it is highly unlikely that your current income is high enough to speed up the process towards this $100K objective.

So during this time keep trying to stay consistent and not get discouraged. Our message to young Canadians is “Rome wasn’t built in a day”. Your financial situation will likely improve as you get older with a higher income, lower debt, and investing.

Why the First $100k is the Most Important

Compounding on Steroids

The first $100K is the most important because compound interest starts to perform its magic. At this point you have saved enough money that the incremental returns start to become significant.

Ex. Using our previous example, imagine you are 18 years of age saving $500 per month, and investing it into a low cost index ETF earning 7% per year. Here is what your investment portfolio would look like as you got older:

By 29 years of age you will have $100,000 (134 months or 11.16 years)

By 35 years of age you will have $200,000 (75 months or 6.35 years)

By 39 years of age you will have $300,000 (53 months or 4.42 years)

By 43 years of age you will have $400,000 (41 months or 3.41 years)

By 46 years of age you will have $500,000 (33 months or 2.75 years)

By 48 years of age you will have $600,000 (27 months or 2.25 years)

By 50 years of age you will have $700,000 (25 months or 2.08 years)

By 52 years of age you will have $800,000 (21 months or 1.75 years)

By 53 years of age you will have $900,000 (19 months or 1.58 years)

By 55 years of age you will have $1,000,000 (17 months or 1.41 years)

As you can see, due to the wonders of compound interest the time frame to reach each subsequent $100K shortens as you get older. What makes this even more mind blowing is the fact that by the time you reach 55 years of age, of the $1,000,000 you have, only $222,500 is from what you have saved and invested. That means that the remaining $777,500 is all interest. That is compounding on steroids!!!

Positive Psychology

The sad part about hitting your first $100K, is that people feel like they are walking through mud, so they give up and quit before ever achieving this milestone. However, once the compound interest snowball starts to roll (after $100K), each additional $1 of savings starts to feel as if it is producing significant returns. You will no longer feel that you need to work insane hours, or make tough sacrifices to reach your financial goals. Instead you can start to live your life freely knowing that in the background your money is working just as hard (if not even harder) for you as you are.

How to Save your First $100K (Step-by-Step Guide)

The process to save your first $100K is actually very simple… but not easy. The following are the steps you need to take:

Obtain a Primary Job

I do not care if your job is flipping burgers or working in a financial firm. You just need a primary consistent income source. Ideally, the job should be full time with the potential to pick up overtime hours.

Reduce Large Fixed Costs

Most Canadians' three largest fixed costs are rent, transportation, and food.

Rent- Live with your parents, or find roommates.

There are several options for finding roommates such as roomies.ca, kijiji.ca, or roomster.com.

You can also find roommates through mutual friends.

Transportation- If you can’t walk, take the bus. If you can’t take the bus then buy an affordable used car.

There are many options to find a used car such as autotrader.ca, cargurus.ca, or kijijiautos.ca.

When we say used car, we’re not talking about a BMW or Lexus. Make sure it’s reasonable and affordable for your budget. Remember, that a car is only to get you from point A to point B, it’s not supposed to be a wealth status symbol.

Another option is to ask around in your family or friend group. Someone may have a used car they will sell you at a steep discount, or even gift you.

Food- Buy your own groceries and cook your own food at home, as much as possible. I know it is time consuming and inconvenient, but if you want to save money you have to do it. Reserve eating out for special occasions.

Save 25% of net income

Every time you receive a paycheck, take the amount you receive and multiply it by 0.25, that is how much you have to save.

For Example: Imagine you receive two paychecks each month of $1,800, for a total of $3,600. Each time you receive a paycheck you will save $450, for a total of $900/month:

$1,800 x 0.25 (25%) = $450 x 2 = $900

For young Canadians under 30 years old, we know that saving 25% can be aspirational. You can start with saving 10-15% of your gross income (income before taxes) and try to increase it to 25% by age 30.

Invest the money in a low cost index ETF

Open up a TFSA or RRSP with a low cost brokerage firm such as questrade.com or wealthsimple.com.

Set up direct deposit from your primary bank account to the brokerage firm.

Once the money is deposited you can purchase a low cost index ETF such as tickers VFV, VEQT, or VGRO.

Repeat every month.

Increase your earnings vehicles

Overtime

The easiest option would be to pick up additional hours from your primary job.

Secondary Job

You could also pick up a second part time job in order to make extra income.

Side Gig or Small Business

Everyone has a skill that they have not currently monetized.

If you are good at math or science, you could be a tutor.

If you are good at a sport, you could be a skills instructor.

If you are good at art, you could sell artwork.

If you are good with computers, you could troubleshoot for others.

If you are interested in a subject or know a lot about it you can even start a Youtube channel, blog, or podcast.

Even if you don’t have a “specialty” there are several lower skill or easier to learn options such as:

Mowing lawns, shoveling driveways or walkways, reselling, etc.

How to Invest Your First $100K Wisely

On your way to your first $100K, you want your investing to be as simple as possible. Your focus is not on maximizing returns, but rather minimizing the time you need to think about it. This is why buying a low cost, well diversified, index ETF is the best option in our opinion. There are a variety of options such as:

VEQT (or XEQT, ZEQT)

100% Stocks

Globally Diversified

VGRO (or XGRO, ZGRO)

80% Stocks, 20% Bonds

Globally Diversified

VFV

100% Stocks

US Based

Based on extensive research, this remains the most effective way to invest your money regardless of how much you have saved. However, we know that people love to chase returns. If this is you…then once you have saved your first $100K, you can start to venture out into alternative options. You could set aside <5% of your investments for other assets such as:

Individual Stocks

Gold, Silver, or Other Commodities

Cryptocurrencies

Options

However, you have to recognize that this is play money and there is a potential of total or partial loss. Although smart investing decisions can result in phenomenal returns, the more you concentrate your money the greater the risk you expose yourself to.

Common Mistakes to Avoid

The time to reach your first $100K is long, and often difficult. And humans are very poor at tolerating delayed gratification. Consequently, many people make the following mistakes on their way to this $100K target:

Fall Victim to Lifestyle Creep

As people's income and net worth increases, they start to reduce the restrictions on their lifestyle. They purchase a bigger house, or find a nicer place to rent. They may buy a new car instead of a used one. They go on more lavish vacations, buy more expensive clothing, and start to buy food out more.

All of the money they were originally setting aside to save and invest starts to slowly disappear. Or any additional income doesn’t get invested, slowing down the time it takes them to reach their $100K target.

Solution: Automate your finances by setting up direct deposit from your primary bank account to a brokerage firm. If you receive a salary increase, then modify the direct deposit amount immediately.

Delaying Investing

One of the biggest mistakes people make is waiting too long to start investing. Many believe they need a high income, or a large lump sum before getting started. But the truth is, time in the market is far more important than timing the market. The longer you delay, the more you miss out on compound interest working in your favor. Even small monthly investments made early, will grow into significant wealth over decades.

To illustrate this, let’s compare four different investors. All of which invest $500/month in a low-cost index ETF earning 7% annually.

Person A starts at age 20

Person B starts at age 25

Person C starts at age 30

Person D starts at age 35

As you can see, even waiting 5 years makes a substantial difference in your long term investment outcomes.

Solution: Start investing today, even if it’s just $50 or $100 per month. The earlier you begin, the less money you need to contribute over time. Set up automatic deposits into a low-cost index ETF and let time do the heavy lifting.

Chasing Investment Returns

Deciding to listen to the noise, aka a friend, family member, or reddit forum user who tells someone to invest in xyz stock. Although some investments produce good returns, others end up a total disaster. In the end, these people will probably make less than they would have, if they just left their money in a well diversified index ETF.

Solution:

Automate your purchases of the low cost index ETF of choice so that there is no money left to invest in individual stocks.

Leave at least 7 days before making any investment decision. This gives you time to remember the path you are on towards financial freedom.

Get Spooked Out of the Market

They watch their investment accounts constantly, or listen to financial news too much. They forget that ups and downs are a natural process in the stock market, which we call volatility. When the market is down, the news stories are meant to be bleak in order to catch your attention. People get scared and decide to sell their stocks out of fear of loss, they think "it’s better to lose 20% than 100% of my money”. When the issue eventually gets resolved and the news stories improve, the market will starts going back up and they buy back in.

People tend to do the opposite of the old adage “buy low, sell high”, in that they tend to buy high after stocks have gone up a lot and sell low when the market starts to go down. The result is they receive much worse returns than if they just left their portfolio alone and did nothing.

Solution:

If you’re an emotional person, remove your brokerage account from your phone, only access it on your desktop.

When things are really bleak, type in “S&P 500 Index Historical Chart” on google. Seeing the long term performance of the market will make you feel better

Conclusion

Saving and investing your first $100K is the hardest step—but also the most important. It’s the foundation that sets you up for long-term wealth, thanks to the magic of compound interest. Yes, it requires discipline, sacrifices, and patience, but once you reach this milestone, the journey gets exponentially easier.

Instead of chasing quick gains or over-complicating your investments, focus on the fundamentals: earn more, spend less, invest consistently. Stick to this formula, and your financial freedom will come sooner than you think.

🚀 What’s your biggest challenge in reaching your first $100K? Drop a comment below!

If you found this guide helpful, share it with someone who needs to hear this message!

If you liked this post you may also like: