Get our free Debt vs Invest Calculator — click here to access it

4 Financial Lessons Traveling Taught Me About Money and Happiness

Discover 4 powerful lessons travel taught me about money, purpose, and happiness—why saving without living is missing the point of financial freedom.

MONEY AND HAPPINESSPSYCHOLOGY OF MONEYFIRE

8/5/202517 min read

Introduction

In Good Will Hunting, Sean Maquire tells Will Hunting that despite all his book smarts, he’ll never know what it really feels like to stand beneath the Sistine Chapel and look up. He can read about it, study its history… but until he experiences it for himself, he’ll never truly understand.

For years, I didn’t get it. Why would anyone spend thousands of dollars just to experience something, when you can see photos online? Growing up, I never travelled anywhere, other than to hockey arenas. I didn’t take my first flight until I was 18 years old, just before university.

Two years ago I decided that my 30th birthday was fast approaching, and it was time I start exploring the world. First stop: the motherland (aka. Ireland).

The next year: mini Ireland (aka. Newfoundland).

To my surprise these two trips didn’t just give me new memories—they reshaped how I think about money, happiness, and how to actually live life.

Here’s what I learned.

Lesson 1: Experiences Are the Best Investments

In investing, dividends are the payments companies make to shareholders. They are small but steady returns that add up over time. But dividends don’t just apply to money.

When we experience something meaningful it provides us with both joy now and in the future. On my recent trip to Newfoundland, I got the opportunity to watch two humpback whales play near our boat. Something I could never have experienced unless I was there at that time, on that day. That moment was unforgettable, and the pictures and videos I took keep that memory alive, paying me “dividends” every time I revisit them.

In the book Die With Zero by Bill Perkins, he calls this concept a “memory dividend”. It says that experiences compound in value over time, because we get to relive them. Unfortunately, we live in a commoditized world that shifts our focus towards superficial things such as brand names, luxury vehicles, and fancy gadgets. Much of which produce minimal long term enjoyment.

Much of this problem can be attributed to something called “hedonic adaptation”. It says that as our income and lifestyle rise, our standards adjust upward. This means that the heated seats, which were once very effective at making our morning on a cold winter day, become the new standard. Experiences don’t follow that same curve— they instead tend to grow richer with time, not stale.

Takeaway: Spend intentionally on experiences that create lasting memories. Their value compounds long after the trip ends, unlike most “things” that lose their shine.

Lesson 2: Money Needs a Purpose (Not Just a Number)

A report by BMO in 2023 found that Canadians feel they need $1.7 million to retire. Similarly, the FIRE community espouses chasing an arbitrary "retirement number”. The goal being to cut costs aggressively, and try to make as much money as you can while you are young. All with the hopes of retiring early so that you can “enjoy your life”. The objective is to sacrifice today for some long term fulfillment.

I actually support many of the strategies promoted by the FIRE community. These include cutting costs on unnecessary expenses, building a saving and investing habit, and developing a financial plan. However, where travelling made me start to disagree with the community is in the “why’s?”.

On the surface, the $1.7 million figure checks out. If we were to apply the “4% rule” this suggests we could live off $68,000/year + CPP benefits and any other work related pensions we receive. This is near the median income in Canada. Assuming reduced expenses in retirement (ie. paid off mortgage, less vehicles, potential downsizing, etc), it should provide you with excess disposable income for hobbies, travel, etc.

However, there are two problems with this theory.

Hedonic Adaptation (See above)

Chances are that you have someone in your family that is retired, and their spending habits have not changed. If they paid of their mortgage, they will start spending the excess money on renovations/updates to their home. They will refuse to downsize because they love their home, and don’t want to leave.

The truth is people are really poor at reducing their living standards, and really good at increasing them.

Life Circumstances Change

Just because you have the money doesn’t mean that you’ll be able to fully enjoy it. Health complications are more common than the FIRE community likes to admit. Luckily in Canada we generally don’t have to worry about lighting our money on fire to pay for medical expenses. However, there is a high probability that we will not be able to make full use of our savings because of a physical or mental barrier to doing the things we enjoy.

What is the solution then?

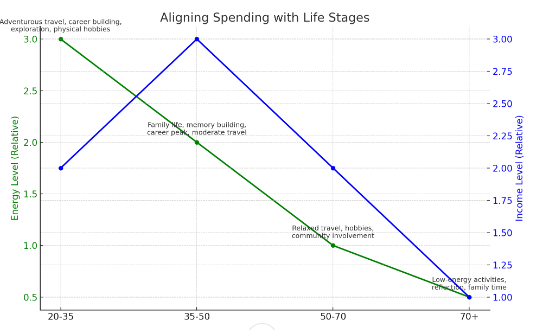

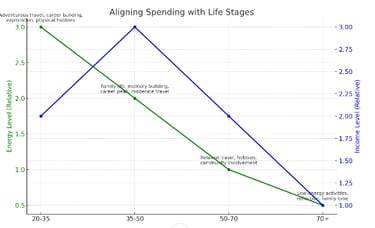

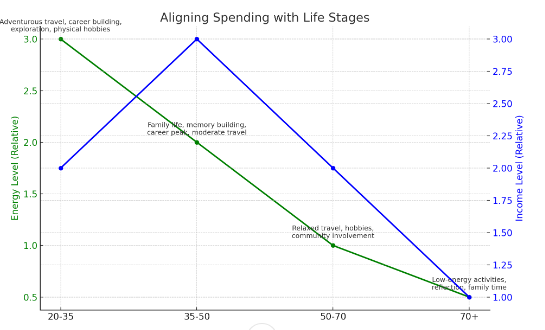

The solution to this problem also comes from Perkins book Die with Zero. He suggests aligning your spending habits with your life stages. If one of your goals is to climb Mount Everest would it make more sense to do it at 20 years old, or 70 years old? This is an extreme example but you should ask yourself these kinds of questions about all of your goals.

For Example: I would love to sit on a beach in Mexico for 10 days, and sip on Margarita’s. However, I am relatively young now, and I may only be able to do the kind of travelling I do (ie. hiking, exploring, etc) for the next 20-30 years. After that I will gladly sit under a cabana, and watch the waves.

The goal of aligning your spending with life stages, is to avoid delaying enjoyment until you are too old.

Takeaway: Decide what you are actually saving for— Travel, family time, hobbies, or freedom. Start putting your money towards those things now, instead of delaying until a arbitrary future. Make sure your wealth serves your life, and not the other way around.

Lesson 3: Learn to Spend Without Guilt

I have a Uncle who I would consider to be well off. Though he probably doesn’t even know what the acronym FIRE means, he fits the description perfectly. He always earned a good income in sales, but what set him apart was his ruthless ability to save. In our family he is referred to as a “cheapskate”.

The stories are endless, but the one that stands out most is when he’d take me down to Tim Hortons for Timbits. Before we left, he’d make sure I wore my Tim Hortons house league hockey jersey. Because if you wore the jersey, the Timbits were free.

To be honest, his ability to save was admirable. He always found a way to get what he wanted at the lowest possible cost. It was great… until it wasn’t. I believe his spending habits never evolved with his growing wealth. You know the saying: “what got you here won’t get you there”. It’s true for a lot of people in the FIRE community.

Early on, saving is everything

In the beginning of your investment journey, the only thing that matters is how much you can save. The reason is quite simple… you don’t have enough money for compounding to make a meaningful difference.

Consider this:

The difference between a 10% and 7% return on $1000 is just $30.

That is why most personal finance advice focuses on two components: increasing your income, and cutting your expenses. In the early stages, saving is everything, and chasing high returns is virtually irrelevant.

Later on, compounding takes over

Something magical happens later in your investment journey:

Eventually, the interest you earn outpaces how much you can save in a year.

Then, it may even outpace how much you can earn in a year.

At this point, the marginal impact of savings becomes minimal. And ironically, that is around the time many people will decide to retire, and begin living off their investments.

Unfortunately, some never do.

The FIRE Trap: Saving Without Spending

Many in the FIRE community end up working too long, or spending too little. Not because they need to, but because they have never built the habit of spending. If you have trained yourself to fear spending money, you may never feel comfortable doing so. Even when the amount you are about to spend has no real implication on your wealth.

The result? Your money keeps growing, untouched, and someone else will inherit it.

Solution: Travel might not be your thing. That’s fine. But you owe it to yourself to find what brings you joy in life. And spend unapologetically on that thing. Cut costs on everything else if you must.

Because if you don’t enjoy the money you’ve worked so hard to save…what was the point of saving it in the first place?

Lesson 4: You Need Less to Be Happy Than You Think

Have you ever read the parable of the fisherman? If you haven’t I encourage you to read it.

In essence, it tells the story of a fisherman who lives in a small village and catches just enough fish each day to feed his family. This simple lifestyle gives him time to relax, enjoy long meals, play music, and spend time with his loved ones. One day, a visiting investor tells him he could turn his fishing skills into a massive business — build a fleet, expand globally, and eventually retire rich. When the fisherman asks what he would do after retiring, the investor replies, “Well, you could fish a little in the morning, spend time with your family, and enjoy life in a quiet village.”

In other words, the fisherman is already living the life the investor is chasing — just without the detour through decades of stress and hustle.

Before you commit your life to chasing more money, take a money to ask yourself: What do I actually want? You might find that a modest lifestyle already delivers most of what your after in life such as time, connection, and peace of mind.

While travelling, I’ve met people with low paying jobs who are content. They prioritize being close to family and friends, living in places they love, and having time to enjoy the simple pleasures in life. For them, trading their current life for a higher paycheck, at the cost of freedom or happiness, is a recipe for disappointment.

A common trap of the FIRE community is delaying happiness in the name of future freedom. But what if the life you’re working towards is already within reach? Worse yet, what if the future life you desire never comes? After all nothing is guaranteed.

That’s where the The 4-Hour Workweek by Tim Ferris offers a compelling alternative. In this book, he introduces the concept of "mini-retirements". These are intentional breaks scattered throughout life, rather then a single far-off retirement at the end of your life. His broader message is about aligning how you make money with why you want it. It’s not about escaping work entirely — it’s about designing a life you don’t need to escape from.

Not everyone needs to be an entrepreneur to align their work their lifestyle. Today’s economy offers endless opportunities including remote work, freelance platforms, and project based income options. The goal isn’t to stop work, but to start living.

Takeaway: Chasing more money won’t make you happier if you’re already living the life you’re working so hard to afford.

Conclusion

Traveling taught me that life isn’t just about how much you save—it’s about why you’re saving and how you choose to use that money to enrich your life. The FIRE mindset offers a powerful framework for financial independence, but it too often overlooks what that freedom is actually for.

Experiences, not things, are what create long-lasting joy. Money is a tool—not a scoreboard—and its value comes from how well it helps you live a life aligned with your values. Whether it’s seeing humpback whales off the coast of Newfoundland or simply having time to sit with family over dinner, your financial plan should be designed to support your best life now, not just someday.

So ask yourself: Are you building wealth just to watch it grow? Or are you investing in the things that make life worth living?

If you liked this post you may also like:

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Böll, H. (1963). Anekdote zur Senkung der Arbeitsmoral [Anecdote Concerning the Lowering of Productivity].

Ferriss, T. (2007). The 4-Hour Workweek: Escape 9-5, Live Anywhere, and Join the New Rich. Harmony Books.

Perkins, B. (2020). Die With Zero: Getting All You Can from Your Money and Your Life. Houghton Mifflin Harcourt.

BMO. (2023). Annual Retirement Report. Retrieved from https://www.bmo.com

Introduction

In Good Will Hunting, Sean Maquire tells Will Hunting that despite all his book smarts, he’ll never know what it really feels like to stand beneath the Sistine Chapel and look up. He can read about it, study its history… but until he experiences it for himself, he’ll never truly understand.

For years, I didn’t get it. Why would anyone spend thousands of dollars just to experience something, when you can see photos online? Growing up, I never travelled anywhere, other than to hockey arenas. I didn’t take my first flight until I was 18 years old, just before university.

Two years ago I decided that my 30th birthday was fast approaching, and it was time I start exploring the world. First stop: the motherland (aka. Ireland).

The next year: mini Ireland (aka. Newfoundland).

To my surprise these two trips didn’t just give me new memories—they reshaped how I think about money, happiness, and how to actually live life.

Here’s what I learned.

Lesson 1: Experiences Are the Best Investments

In investing, dividends are the payments companies make to shareholders. They are small but steady returns that add up over time. But dividends don’t just apply to money.

When we experience something meaningful it provides us with both joy now and in the future. On my recent trip to Newfoundland, I got the opportunity to watch two humpback whales play near our boat. Something I could never have experienced unless I was there at that time, on that day. That moment was unforgettable, and the pictures and videos I took keep that memory alive, paying me “dividends” every time I revisit them.

In the book Die With Zero by Bill Perkins, he calls this concept a “memory dividend”. It says that experiences compound in value over time, because we get to relive them. Unfortunately, we live in a commoditized world that shifts our focus towards superficial things such as brand names, luxury vehicles, and fancy gadgets. Much of which produce minimal long term enjoyment.

Much of this problem can be attributed to something called “hedonic adaptation”. It says that as our income and lifestyle rise, our standards adjust upward. This means that the heated seats, which were once very effective at making our morning on a cold winter day, become the new standard. Experiences don’t follow that same curve— they instead tend to grow richer with time, not stale.

Takeaway: Spend intentionally on experiences that create lasting memories. Their value compounds long after the trip ends, unlike most “things” that lose their shine.

Lesson 2: Money Needs a Purpose (Not Just a Number)

A report by BMO in 2023 found that Canadians feel they need $1.7 million to retire. Similarly, the FIRE community espouses chasing an arbitrary "retirement number”. The goal being to cut costs aggressively, and try to make as much money as you can while you are young. All with the hopes of retiring early so that you can “enjoy your life”. The objective is to sacrifice today for some long term fulfillment.

I actually support many of the strategies promoted by the FIRE community. These include cutting costs on unnecessary expenses, building a saving and investing habit, and developing a financial plan. However, where travelling made me start to disagree with the community is in the “why’s?”.

On the surface, the $1.7 million figure checks out. If we were to apply the “4% rule” this suggests we could live off $68,000/year + CPP benefits and any other work related pensions we receive. This is near the median income in Canada. Assuming reduced expenses in retirement (ie. paid off mortgage, less vehicles, potential downsizing, etc), it should provide you with excess disposable income for hobbies, travel, etc.

However, there are two problems with this theory.

Hedonic Adaptation (See above)

Chances are that you have someone in your family that is retired, and their spending habits have not changed. If they paid of their mortgage, they will start spending the excess money on renovations/updates to their home. They will refuse to downsize because they love their home, and don’t want to leave.

The truth is people are really poor at reducing their living standards, and really good at increasing them.

Life Circumstances Change

Just because you have the money doesn’t mean that you’ll be able to fully enjoy it. Health complications are more common than the FIRE community likes to admit. Luckily in Canada we generally don’t have to worry about lighting our money on fire to pay for medical expenses. However, there is a high probability that we will not be able to make full use of our savings because of a physical or mental barrier to doing the things we enjoy.

What is the solution then?

The solution to this problem also comes from Perkins book Die with Zero. He suggests aligning your spending habits with your life stages. If one of your goals is to climb Mount Everest would it make more sense to do it at 20 years old, or 70 years old? This is an extreme example but you should ask yourself these kinds of questions about all of your goals.

For Example: I would love to sit on a beach in Mexico for 10 days, and sip on Margarita’s. However, I am relatively young now, and I may only be able to do the kind of travelling I do (ie. hiking, exploring, etc) for the next 20-30 years. After that I will gladly sit under a cabana, and watch the waves.

The goal of aligning your spending with life stages, is to avoid delaying enjoyment until you are too old.

Takeaway: Decide what you are actually saving for— Travel, family time, hobbies, or freedom. Start putting your money towards those things now, instead of delaying until a arbitrary future. Make sure your wealth serves your life, and not the other way around.

Lesson 3: Learn to Spend Without Guilt

I have a Uncle who I would consider to be well off. Though he probably doesn’t even know what the acronym FIRE means, he fits the description perfectly. He always earned a good income in sales, but what set him apart was his ruthless ability to save. In our family he is referred to as a “cheapskate”.

The stories are endless, but the one that stands out most is when he’d take me down to Tim Hortons for Timbits. Before we left, he’d make sure I wore my Tim Hortons house league hockey jersey. Because if you wore the jersey, the Timbits were free.

To be honest, his ability to save was admirable. He always found a way to get what he wanted at the lowest possible cost. It was great… until it wasn’t. I believe his spending habits never evolved with his growing wealth. You know the saying: “what got you here won’t get you there”. It’s true for a lot of people in the FIRE community.

Early on, saving is everything

In the beginning of your investment journey, the only thing that matters is how much you can save. The reason is quite simple… you don’t have enough money for compounding to make a meaningful difference.

Consider this:

The difference between a 10% and 7% return on $1000 is just $30.

That is why most personal finance advice focuses on two components: increasing your income, and cutting your expenses. In the early stages, saving is everything, and chasing high returns is virtually irrelevant.

Later on, compounding takes over

Something magical happens later in your investment journey:

Eventually, the interest you earn outpaces how much you can save in a year.

Then, it may even outpace how much you can earn in a year.

At this point, the marginal impact of savings becomes minimal. And ironically, that is around the time many people will decide to retire, and begin living off their investments.

Unfortunately, some never do.

The FIRE Trap: Saving Without Spending

Many in the FIRE community end up working too long, or spending too little. Not because they need to, but because they have never built the habit of spending. If you have trained yourself to fear spending money, you may never feel comfortable doing so. Even when the amount you are about to spend has no real implication on your wealth.

The result? Your money keeps growing, untouched, and someone else will inherit it.

Solution: Travel might not be your thing. That’s fine. But you owe it to yourself to find what brings you joy in life. And spend unapologetically on that thing. Cut costs on everything else if you must.

Because if you don’t enjoy the money you’ve worked so hard to save…what was the point of saving it in the first place?

Lesson 4: You Need Less to Be Happy Than You Think

Have you ever read the parable of the fisherman? If you haven’t I encourage you to read it.

In essence, it tells the story of a fisherman who lives in a small village and catches just enough fish each day to feed his family. This simple lifestyle gives him time to relax, enjoy long meals, play music, and spend time with his loved ones. One day, a visiting investor tells him he could turn his fishing skills into a massive business — build a fleet, expand globally, and eventually retire rich. When the fisherman asks what he would do after retiring, the investor replies, “Well, you could fish a little in the morning, spend time with your family, and enjoy life in a quiet village.”

In other words, the fisherman is already living the life the investor is chasing — just without the detour through decades of stress and hustle.

Before you commit your life to chasing more money, take a money to ask yourself: What do I actually want? You might find that a modest lifestyle already delivers most of what your after in life such as time, connection, and peace of mind.

While travelling, I’ve met people with low paying jobs who are content. They prioritize being close to family and friends, living in places they love, and having time to enjoy the simple pleasures in life. For them, trading their current life for a higher paycheck, at the cost of freedom or happiness, is a recipe for disappointment.

A common trap of the FIRE community is delaying happiness in the name of future freedom. But what if the life you’re working towards is already within reach? Worse yet, what if the future life you desire never comes? After all nothing is guaranteed.

That’s where the The 4-Hour Workweek by Tim Ferris offers a compelling alternative. In this book, he introduces the concept of "mini-retirements". These are intentional breaks scattered throughout life, rather then a single far-off retirement at the end of your life. His broader message is about aligning how you make money with why you want it. It’s not about escaping work entirely — it’s about designing a life you don’t need to escape from.

Not everyone needs to be an entrepreneur to align their work their lifestyle. Today’s economy offers endless opportunities including remote work, freelance platforms, and project based income options. The goal isn’t to stop work, but to start living.

Takeaway: Chasing more money won’t make you happier if you’re already living the life you’re working so hard to afford.

Conclusion

Traveling taught me that life isn’t just about how much you save—it’s about why you’re saving and how you choose to use that money to enrich your life. The FIRE mindset offers a powerful framework for financial independence, but it too often overlooks what that freedom is actually for.

Experiences, not things, are what create long-lasting joy. Money is a tool—not a scoreboard—and its value comes from how well it helps you live a life aligned with your values. Whether it’s seeing humpback whales off the coast of Newfoundland or simply having time to sit with family over dinner, your financial plan should be designed to support your best life now, not just someday.

So ask yourself: Are you building wealth just to watch it grow? Or are you investing in the things that make life worth living?

If you liked this post you may also like:

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Böll, H. (1963). Anekdote zur Senkung der Arbeitsmoral [Anecdote Concerning the Lowering of Productivity].

Ferriss, T. (2007). The 4-Hour Workweek: Escape 9-5, Live Anywhere, and Join the New Rich. Harmony Books.

Perkins, B. (2020). Die With Zero: Getting All You Can from Your Money and Your Life. Houghton Mifflin Harcourt.

BMO. (2023). Annual Retirement Report. Retrieved from https://www.bmo.com