Get our free Debt vs Invest Calculator — click here to access it

Best Emergency Fund Accounts in Canada (2025 Guide)

Discover the best emergency fund accounts in Canada for 2025. Compare rates, accessibility, and safety to find the ideal home for your emergency savings today.

EMERGENCY FUNDFINANCIAL BASICS

NextGenFinance Team

10/6/202529 min read

Introduction

When building an emergency fund in Canada, choosing the right account matters just as much as the amount you save. The difference between a basic savings account, and a high-interest option could mean hundreds or even thousands of dollars in lost returns over time.

Did you know that more than one in four Canadians say they couldn’t afford a $500 emergency expense? This is a reminder of why having a safe, accessible emergency fund is essential.

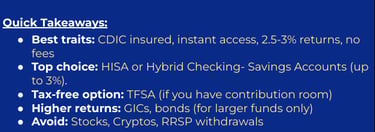

But it's not just about the highest rate. Your emergency fund needs to balance four things: safety, liquidity (quick access), low fees, and competitive returns.

In this guide, we'll compare the best emergency fund accounts available to Canadians in 2025. These range from high-interest savings accounts to TFSAs, GICs, and bond ETFs. Our goal is to help you choose the right fit for your situation.

How Much Should You Keep (Brief Overview)

Most Canadians should aim for 3-6 months of essential expenses in their emergency fund. This calculation should include expenses for dependents (ie. children, spouse, or dependent parents). It should include only the basic necessities, not non-essential expenses (ex. Travel,). Self-employed or single-income households may want to aim for a larger fund of 6-12 months cash reserves.

Ex. If your essential monthly expenses (rent, utilities, groceries, insurance, debt minimum payments) is $3,000 than:

Minimum Emergency Fund is $9,000 (3 months)

Optimal Emergency: $12,000-$18,000 (4-6 months)

What Makes a Good Emergency Fund Account?

An effective emergency fund should contain four key characteristics:

1. Liquidity

Imagine telling your mechanic who just repaired your car that you will get him the funds in 3-5 business days. Probably won’t go over too well… right?

An emergency fund should provide you with the money that you need, when you need it. In order for this to occur, you have to be able to easily, and quickly access the funds.

2. Safety

On a basic level, you don’t want to lose your money. In Canada, we have something called the Canadian Deposit Insurance Corporation (CDIC). They provide insurance for the first $100,000 of deposits into Canadian bank accounts. Provided you don’t have a costly lifestyle, this should cover your emergency fund against total loss.

However, you should also aim to avoid excessive volatility (or fluctuations) in the value of your emergency fund. Since the money may be needed at any moment, you want to ensure that what you expect to be in the account…is actually there.

3. Low (or no) fees

Do you remember the classic arcade game Pac-Man? Fees act like the ghosts going around slowly eating away at your cash reserves.

Just like your investments, the goal of your emergency fund is to avoid fees like the plaque. Remember, the bank is already making money on your deposits, that is a fair trade for your money security… they don’t need any more money.

Put your emergency fund in a bank account that has no fees (Yes, not even account minimum fees). And yes, these accounts do exist, as you will see later.

4. Earn some interest

There is a term in investing known as the risk-reward continuum. It states that:

The higher the risk, the higher the potential return.

Meanwhile, the lower the risk, the lower the potential return.

At no time though does it say no return. Your emergency fund should earn some interest. Just recognize that it may be less than you get in your investment accounts because you want stability and lower risk.

However, it doesn’t mean you should fall victim to highway robbery. The account you decide to use for your emergency fund could mean a 3.0% difference in your interest returns. (Ex. Big Canadian Bank vs EQ Bank).

Top Places to Keep an Emergency Fund in Canada

Now that we know what characteristics make up a good emergency fund, the next reasonable question becomes where can we find it. Luckily, there are a few good options in Canada.

Hybrid Chequing-Savings Accounts

Many discount brokerage firms are offer a hybrid of a chequings and savings account. These accounts offer the flexibility of a chequings account allowing you to withdraw from ATM’s, and engage in online banking (transfers and bill payments) with minimal to no fees. They also provide the benefits of a savings account, allowing you to earn interest on your deposits.

The Pros of a Hybrid Chequing- Savings Accounts for an emergency fund are:

Instant access to funds (High Liquidity)

Earn significantly more than standard savings accounts (Reasonable Interest Return)

CDIC Insured up to $100,000 or more (Safety)

The Cons are the following:

Rates vary from one bank to the next.

Alternatively, they may require certain criteria to be met such as minimum balance amounts, or setting up direct deposits.

Interest earned is taxable.

Some accounts may contain fees.

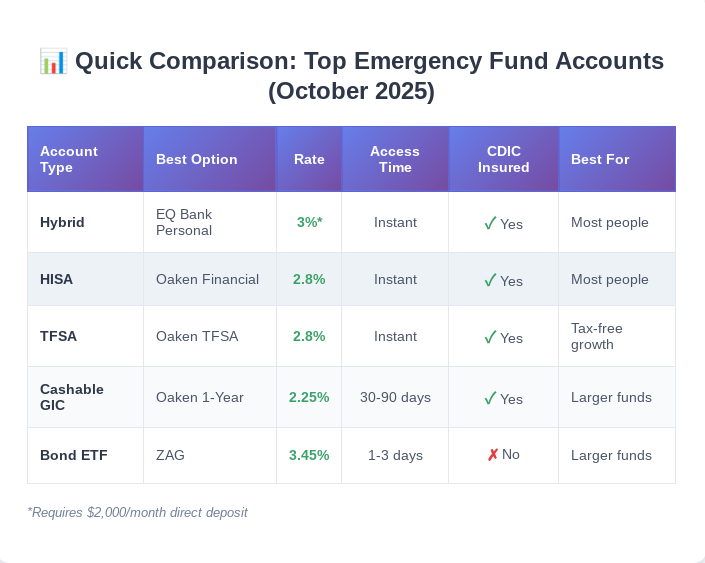

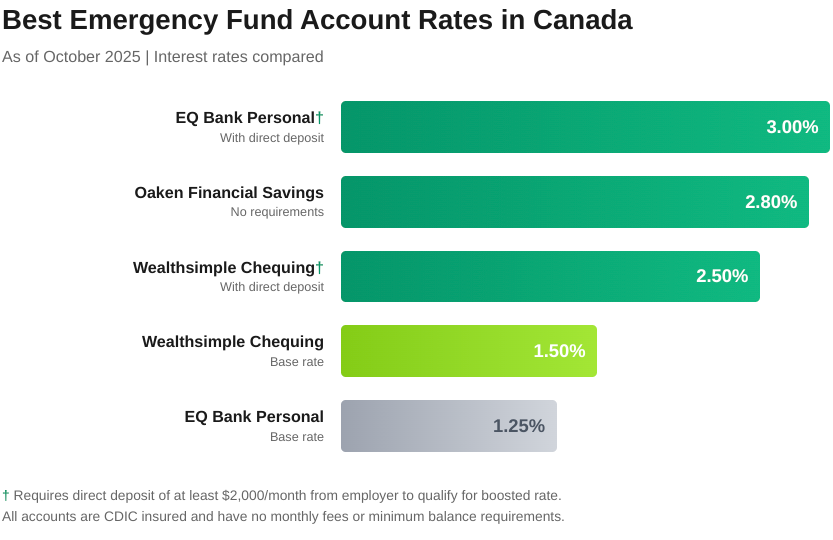

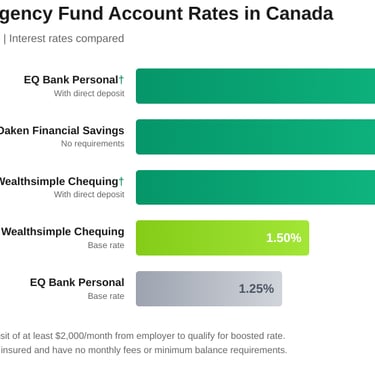

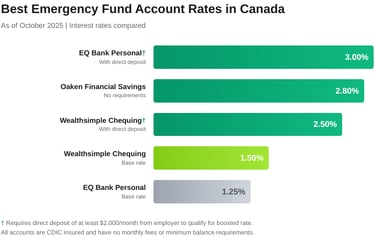

The best options based on current research as of October 2025 are the following:

Wealthsimple- Chequing Account

1.5%/year interest earned

Can boost your rate to 2.5% with a direct deposit of at least $2,000/month.

No fees or minimum balance required.

1.25%/year interest earned

Can boost to 3% with a direct deposit of at least $2,000/month.

No fees or minimum balance required.

Caveat: These types of promotional offers require direct deposit from your employer. Transferring $2,000 into the account each month will not make you eligible. This is an odd feature considering they are receiving the funds regardless.

High-Interest Savings Accounts (HISA’s)

Most major banks will offer High Interest Savings Accounts (HISA’s). HISA’s offer essentially the same pros and cons as the hybrid accounts.

The rates offered for HISA’s, by most major banks, are relatively low though. This is a head scratcher considering the name of these accounts claims they are “high interest”. Due to the low rate of return, they may provide promotional offers to entice you to deposit your funds. This will involve a temporary high rate of return that will decrease after a defined period of time (Ex. 5% for 3 months, then 0.05% afterwards).

In order to find a consistently good rate, you often have to look for smaller financial institutions

As of October 2025, the best options that exist are the following:

Oaken Financial- Savings Account

2.8%/year interest earned

No fees or minimum balance required.

Laurentian Bank- High Interest Savings Account

2.2%/year interest earned

No minimum balance required.

$1.00/transaction fees.

Tax Free Savings Account (TFSA)

The TFSA could be another good option for a location to hold your emergency fund. However, it isn’t recommended that you use it if you are already close to maximizing the account for two reasons.

Regular deposits, and withdrawals reduce your contribution limit in the calendar year they are made. This makes you more susceptible to penalties from the CRA for over-contribution.

The TFSA is great for big financial goals such as retirement, and home purchase. Occupying space for an emergency fund may be dragging down your long term returns.

You can find out how much contribution room you have left by using the calculator here, or by using your MyCRA Account. At a minimum, make sure you have enough contribution room to allow for 6 months of essential expenses. If you need a larger emergency fund (9-12 months) based on life circumstances, this should be factored into the calculation.

Ex. If your essential expenses are $4,000. You should only use a TFSA to place your emergency fund if you have $24,000 in contribution room remaining.

If you regularly use your emergency fund (which you shouldn’t be), then the use of the TFSA becomes significantly more complicated. If this is you, I would only use the TFSA when there is a significant difference between your emergency fund size, and available contribution room. To add a margin of safety, I would aim for 2x your emergency fund.

Ex. If your essential expenses are $4,000, and you regularly use your emergency fund. You should only use a TFSA to place your emergency fund, if you have $48,000 in contribution room remaining.

As of October 2025, the best options are:

Oaken Financial- TFSA Saving Account

2.8%/year interest earned

No fees or minimum balance required.

EQ Bank- Tax Free Savings Account

1.5%/year interest earned

No fees or minimum balance required.

Discount Brokerage Firm (Non-Registered Account or TFSA)

Discount brokerage firms such as Wealthsimple or Questrade provide another good option. Using these firms you could open a Non-registered taxable account or a TFSA.

The primary benefit is these accounts allow you to invest in a variety of different asset classes including stocks, bonds, money market funds, real estate investment trusts (REITs), exchange traded funds (ETFs), etc. Many of which may provide a better rate of return than standard banking accounts.

Additionally, they both have no minimum balance fees, and low to no transaction fees. These are perks you will not get when opening up a brokerage account through many of the major providers in Canada.

How to Maximize Your Emergency Fund Returns

If you recall from earlier, an important characteristic of an emergency fund is that it provides a reasonable rate of return. This important because:

Inflation will erode the value of your cash over time.

Inflation is a measurement of the rate of change in prices over time.

Due to inflation, what you can buy with $10 today will be less 1, 3, 5, & 10 years from now.

There is an opportunity cost to idle cash.

“Cash drag” refers to the fact that funds sitting in cash (ie. not invested) drag down the performance of your entire portfolio in a bull market.

This is a delicate balancing act though because an emergency fund should also provide stability, and liquidity. Depositing the funds into any of the account options mentioned above are great options that fulfil these requirements. However, there are some investment strategies that can be used within these accounts to receive an improved return.

Stable Investment Options for Emergency Funds

Cashable or Redeemable GICs

Guaranteed Interest Certificates (GIC’s) provide the following benefits:

Safe and CDIC insured

Guaranteed return

Slightly higher rates than HISAs in some markets.

The only area of concern with GIC’s is the amount of liquidity (ie. how easily you can access your cash). Cashable GIC’s are liquid, but not as much as a standard HISA. Most major Canadian banks require a 30-90 day minimum holding period before you can cash out a ‘cashable’ GIC. This means that if you need the funds in the first 30-90 days after buying the GIC, you will not be able to access it.

It is for this reason that Cashable GIC’s are best for Canadians with a large emergency fund (6-12 months of expenses) that would like to make a better return on a portion of their money (ex. 50%).

The best cashable GIC rate as of October 2025 is:

Oaken Financial- 1 Year Cashable GIC

2.25%/year interest earned

Non-Redeemable GIC Laddering

Non-Redeemable GIC’s have better interest returns than Cashable GIC’s. But they are one of the least liquid assets you can buy. They don’t allow you to access the funds throughout the duration of the loan contract. You have to wait until the end of the term in order to receive your money back, plus any interest accrued over that time period.

Ex. You buy a 1-Year GIC earning 3% with $1,000 in October 2025. You have to wait until October 2026 until you will receive $1,030 ($1,000+3%).

However, there is a partial solution to the liquidity problem. This is a strategy known as GIC Laddering. Using this strategy you will buy GIC’s of varying time lengths (ie. 3 months, 6 months, 9 months, 1-year).

Ex. You have $12,000 in a HISA. You use $6,000 to buy 4 different GIC term lengths.

$1,500 for a 3-Month GIC

$1,500 for a 6-Month GIC

$1,500 for a 9 Month GIC

$1,500 for a 1-Year GIC

Similar to Cashable GIC’s this should only be performed if you have a 6-12 month emergency fund, and are only using 50% or less for this strategy.

As of October 2025, the best options are:

Oaken Financial- 1-Year Non-Redeemable GIC

3.4%/year interest earned

EQ Bank- 1- Year Non-Redeemable GIC

3.15%/year interest earned

Note: EQ Bank would win for an emergency fund though because they provide shorter term options such as 3 month, 6 month, and 9 month GIC’s at lower rates.

Government & Investment-Grade Bonds

Bonds are another great strategy that could be used for an emergency fund. Provided that you purchase government, or investment grade bonds, they are considered relatively low risk. However, they are not CDIC insured like normal bank deposits or GIC’s.

Bonds provide you with steady interest payments throughout the holding period. Depending on the type of bonds that you purchase, you could earn interest rates higher than HISA’s, hybrid chequing-savings accounts, and GIC’s.

The easiest way to purchase bonds is through a bond exchange traded fund (ETF). This requires you to set-up and deposit money into a brokerage account. As always we recommend a discount brokerage firm such as Wealthsimple or Questrade. There you can buy and sell bond ETFs during stock market hours (Mon-Fri 9:30am to 4:00pm). They are relatively liquid during these time periods. Unfortunately, they would not be a good asset to own if your emergency occurs on a weekend.

Since they are traded on the stock exchange the market value fluctuates slightly over time. This means that you could sell when the price is low and lose some of your principle (ie. money you used to buy the bonds).

Due to the liquidity issues with bonds its best to follow a similar strategy as GIC’s (ie. 50% allocation). However, you could increase your allocation slightly to bonds because the worst case is waiting 2-3 days for the stock market to re-open.

As of October 2025, the good bond ETF options are:

XAGH (IShares US Aggregate Bond Index ETF)

3.45% Distribution Yield, MER 0.2%

US investment grade bonds including treasury bonds and corporate bonds.

ZAG (BMO Canada Aggregate Bond Index ETF)

3.45% Distribution Yield, MER 0.09%

Canada investment grade bonds including federal, provincial, and corporate bonds.

Money Market Funds

Money market funds are a tool you can use to store an emergency fund. These funds invest in short-term government and corporate debt, which makes them relatively safe while providing slightly better returns than most savings accounts. However, they may produce less returns than Bond ETF’s and some GIC’s. Their purpose is to give investors a place to keep money with low volatility, steady growth, and quick access when needed.

The main trade-offs with money market funds are they are also not CDIC insured. Also, returns can shift depending on changes in interest rates. Like Bond ETF’s, you will need a brokerage account to buy them, which may add an extra layer of complexity if you are not already using one.

That said, for Canadians who want to balance safety with a bit of extra yield, money market funds can serve as a reasonable option within an emergency fund strategy.

As of October 2025, the a good money market fund option is:

2.77% current yield, MER 0.13%

Cash ETFs

Another option for your emergency fund is a Cash ETF. These funds are designed specifically to hold cash and generate a return that is usually higher than what you would get from a typical savings account. A good example is the Horizons Cash Maximizer ETF (CASH.TO).

Similar to Bond ETF’s, they trade just like a stock. This means that you can buy and sell them during normal market hours. They are very liquid during those times. Also, for the most part , you don’t have to worry about large swings in value since they are meant to be stable.

The downside with Cash ETFs is that they are not CDIC insured. Also, they are not liquid when the market is closed (ex. weekend).

As of October 2025, the a good cash ETF option is:

CASH.TO (Horizons Cash Maximizer ETF)

2.39% Distribution yield, MER 0.11%

Summary

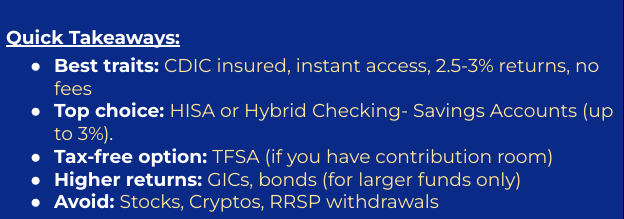

Provided that you can receive 3% in a EQ Bank personal account by just setting up direct deposit, most other options don't look enticing unless you are willing to go out the risk curve by buying bonds. Even GIC rates in most cases are lower than 3%, especially on shorter term length (ie. Less than 1 year).

Bonds could provide slightly higher returns at 3.45%, but you sacrifice CDIC insurance, there is some risk of volatility, and you have to wait for market hours to access your funds. For most Canadians, the simplicity of a savings account makes it the best choice for an emergency fund at current rates.

Places NOT to Keep Your Emergency Fund

Some people may not like the answer of a savings account (such as that offered at EQ Bank) being the best place to keep their emergency fund. That is ok, we can agree to disagree. However, there are some places you should avoid putting your emergency fund regardless.

Stocks or Stock ETF’s

Stocks and Stock ETFs are an amazing option for growing your wealth in your investment accounts. Unfortunately, there is too much risk associated with using the same strategy with your emergency fund. The value of stocks can fluctuate on a daily basis. Furthermore, there is a risk of market corrections, and crashes that can significantly impact the value of your investments. For context, in recent memory during the COVID-19 crash of 2020, the S&P 500 fell 34% in five weeks.

Cryptocurrency

I am not here to argue the utility of cryptocurrency as an investment choice. You may like it, or despise it. But it doesn’t belong in your emergency fund. The fluctuations in the price of cryptos are like putting stocks on steroids. It isn’t unusual to see 10-20% or more changes in their value during a single day. During that same COVID-19 crash on March 12, 2020, Bitcoin fell by more than 39% in a single day.

Registered Retirement Savings Plan (RRSP)

The TFSA is not a great choice because of the impact on your contribution limit, however, there are no direct tax implications until you over contribute. The RRSP, on the other hand, is a very poor location to put an emergency fund because of tax implications.

Every time you withdraw funds from an RRSP they will be added to your taxable income for the year of the withdrawal. Add to this that you receive a withholding tax of 10-20% at source (time of withdrawal). This means that you will need to withdraw 10-20% more than you actually need in order to pay for the emergency.

Best Strategy for Canadians

The truth is, there isn’t a single “best” emergency fund strategy that works for everyone. However, there are principles most Canadians can follow.

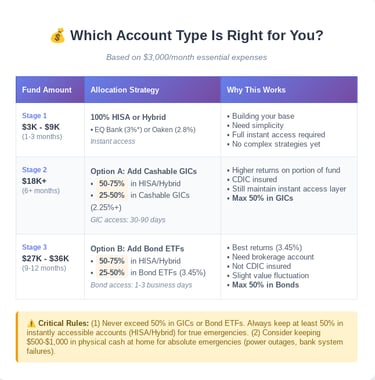

A layered approach often makes the most sense:

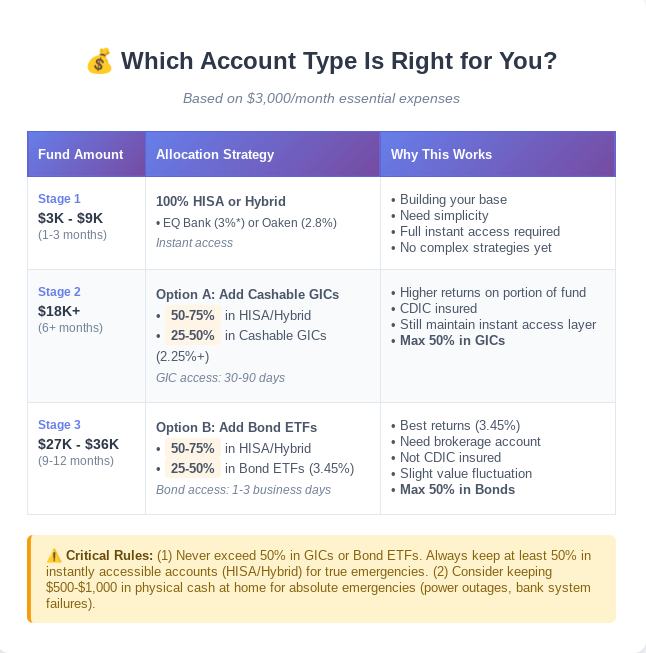

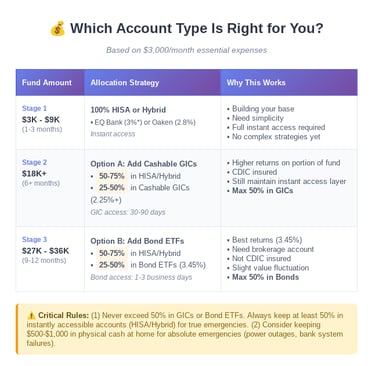

Immediate access: Keep $500–$1,000 in your everyday chequing account.

This covers those “need cash now” moments like an urgent car repair.

Main reserve: Put several months of expenses in a high-interest savings account (HISA).

Something like EQ Bank’s Personal Account at 3% (with direct deposit) is a good example. It’s CDIC insured, pays a decent return, and you can access it instantly.

Optional growth layer: If you have a larger emergency fund (6–12 months of expenses), you could put part of it (say 25–50%) into a slightly higher-yield option like a cashable GIC or a bond ETF.

This gives you a better return without putting the whole fund at risk.

Here’s how that might play out in real life:

Example 1: Your fridge breaks down, so you dip into the $1,000 you have in chequing to pay the repair cost.

Example 2: You get laid off. After you burn through your first $1,000, you draw from your HISA to pay for monthly bills.

Example 3: The layoff lasts longer than expected so you tap into the portion you’ve put into GICs or bonds.

This gives time for non-redeemable GIC’s to expire, or you to pass the required waiting period for cashable GIC’s.

Conclusion

Your emergency fund isn’t about chasing the highest return. Instead it’s about having money that’s safe, accessible, and ready when life happens. For most Canadians, that means keeping the majority of your fund in a high-interest savings account. This provides CDIC protection, no fees, and instant access. If you’ve built a larger cushion, you can layer in some cashable GICs, or low-risk bond ETFs to squeeze out a bit more return without putting your whole safety net at risk.

The best approach is simple: a small buffer in chequing for quick expenses, several months of essentials in a HISA, and optional growth through GICs or ETFs if your fund is bigger. Build it gradually, treat contributions like a monthly bill, and stick with it. When the unexpected happens, whether it’s a flat tire, a broken fridge, or a job loss, you’ll be glad you made your emergency fund a priority.

If you like this post you may also like:

[Budgeting for Beginners: How to Take Control of Your Money]

[What Is a GIC and How Does It Work in Canada? (2025 Guide)]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

BlackRock. (2025). iShares Core U.S. Aggregate Bond ETF (XAGH). iShares by BlackRock. Retrieved October 2025, from https://www.blackrock.com

BMO Global Asset Management. (2025). BMO Aggregate Bond Index ETF (ZAG) & BMO Money Market Fund (ZMMK). Bank of Montreal. Retrieved October 2025, from https://www.bmo.com

Canadian Deposit Insurance Corporation. (2025). Protecting your deposits. https://www.cdic.ca

Canadian Social Survey / Statistics Canada. (2023, February 13). One in four Canadians are unable to cover an unexpected expense of $500. The Daily. https://www150.statcan.gc.ca/n1/daily-quotidien/230213/dq230213b-eng.htm Statistics Canada+1

Employment and Social Development Canada. (2025). Employment Insurance monitoring and assessment report. Government of Canada. Retrieved October 2025, from https://www.canada.ca

EQ Bank. (2025). Personal account and TFSA rates. Equitable Bank. Retrieved October 2025, from https://www.eqbank.ca

Horizons ETFs. (2025). Horizons Cash Maximizer ETF (CASH.TO). Horizons ETFs Management. https://www.horizonsetfs.com

Laurentian Bank of Canada. (2025). High Interest Savings Account. https://www.laurentianbank.ca

Oaken Financial. (2025). Oaken savings accounts and GICs. https://www.oaken.com

Questrade, Inc. (2025). Self-directed investing with Questrade. https://www.questrade.com

Wealthsimple. (2025). Cash account and chequing options. Wealthsimple Technologies Inc. Retrieved October 2025, from https://www.wealthsimple.com

Introduction

When building an emergency fund in Canada, choosing the right account matters just as much as the amount you save. The difference between a basic savings account, and a high-interest option could mean hundreds or even thousands of dollars in lost returns over time.

Did you know that more than one in four Canadians say they couldn’t afford a $500 emergency expense? This is a reminder of why having a safe, accessible emergency fund is essential.

But it's not just about the highest rate. Your emergency fund needs to balance four things: safety, liquidity (quick access), low fees, and competitive returns.

In this guide, we'll compare the best emergency fund accounts available to Canadians in 2025. These range from high-interest savings accounts to TFSAs, GICs, and bond ETFs. Our goal is to help you choose the right fit for your situation.

How Much Should You Keep (Brief Overview)

Most Canadians should aim for 3-6 months of essential expenses in their emergency fund. This calculation should include expenses for dependents (ie. children, spouse, or dependent parents). It should include only the basic necessities, not non-essential expenses (ex. Travel,). Self-employed or single-income households may want to aim for a larger fund of 6-12 months cash reserves.

Ex. If your essential monthly expenses (rent, utilities, groceries, insurance, debt minimum payments) is $3,000 than:

Minimum Emergency Fund is $9,000 (3 months)

Optimal Emergency: $12,000-$18,000 (4-6 months)

What Makes a Good Emergency Fund Account?

An effective emergency fund should contain four key characteristics:

1. Liquidity

Imagine telling your mechanic who just repaired your car that you will get him the funds in 3-5 business days. Probably won’t go over too well… right?

An emergency fund should provide you with the money that you need, when you need it. In order for this to occur, you have to be able to easily, and quickly access the funds.

2. Safety

On a basic level, you don’t want to lose your money. In Canada, we have something called the Canadian Deposit Insurance Corporation (CDIC). They provide insurance for the first $100,000 of deposits into Canadian bank accounts. Provided you don’t have a costly lifestyle, this should cover your emergency fund against total loss.

However, you should also aim to avoid excessive volatility (or fluctuations) in the value of your emergency fund. Since the money may be needed at any moment, you want to ensure that what you expect to be in the account…is actually there.

3. Low (or no) fees

Do you remember the classic arcade game Pac-Man? Fees act like the ghosts going around slowly eating away at your cash reserves.

Just like your investments, the goal of your emergency fund is to avoid fees like the plaque. Remember, the bank is already making money on your deposits, that is a fair trade for your money security… they don’t need any more money.

Put your emergency fund in a bank account that has no fees (Yes, not even account minimum fees). And yes, these accounts do exist, as you will see later.

4. Earn some interest

There is a term in investing known as the risk-reward continuum. It states that:

The higher the risk, the higher the potential return.

Meanwhile, the lower the risk, the lower the potential return.

At no time though does it say no return. Your emergency fund should earn some interest. Just recognize that it may be less than you get in your investment accounts because you want stability and lower risk.

However, it doesn’t mean you should fall victim to highway robbery. The account you decide to use for your emergency fund could mean a 3.0% difference in your interest returns. (Ex. Big Canadian Bank vs EQ Bank).

Top Places to Keep an Emergency Fund in Canada

Now that we know what characteristics make up a good emergency fund, the next reasonable question becomes where can we find it. Luckily, there are a few good options in Canada.

Hybrid Chequing-Savings Accounts

Many discount brokerage firms are offer a hybrid of a chequings and savings account. These accounts offer the flexibility of a chequings account allowing you to withdraw from ATM’s, and engage in online banking (transfers and bill payments) with minimal to no fees. They also provide the benefits of a savings account, allowing you to earn interest on your deposits.

The Pros of a Hybrid Chequing- Savings Accounts for an emergency fund are:

Instant access to funds (High Liquidity)

Earn significantly more than standard savings accounts (Reasonable Interest Return)

CDIC Insured up to $100,000 or more (Safety)

The Cons are the following:

Rates vary from one bank to the next.

Alternatively, they may require certain criteria to be met such as minimum balance amounts, or setting up direct deposits.

Interest earned is taxable.

Some accounts may contain fees.

The best options based on current research as of October 2025 are the following:

Wealthsimple- Chequing Account

1.5%/year interest earned

Can boost your rate to 2.5% with a direct deposit of at least $2,000/month.

No fees or minimum balance required.

1.25%/year interest earned

Can boost to 3% with a direct deposit of at least $2,000/month.

No fees or minimum balance required.

Caveat: These types of promotional offers require direct deposit from your employer. Transferring $2,000 into the account each month will not make you eligible. This is an odd feature considering they are receiving the funds regardless.

High-Interest Savings Accounts (HISA’s)

Most major banks will offer High Interest Savings Accounts (HISA’s). HISA’s offer essentially the same pros and cons as the hybrid accounts.

The rates offered for HISA’s, by most major banks, are relatively low though. This is a head scratcher considering the name of these accounts claims they are “high interest”. Due to the low rate of return, they may provide promotional offers to entice you to deposit your funds. This will involve a temporary high rate of return that will decrease after a defined period of time (Ex. 5% for 3 months, then 0.05% afterwards).

In order to find a consistently good rate, you often have to look for smaller financial institutions

As of October 2025, the best options that exist are the following:

Oaken Financial- Savings Account

2.8%/year interest earned

No fees or minimum balance required.

Laurentian Bank- High Interest Savings Account

2.2%/year interest earned

No minimum balance required.

$1.00/transaction fees.

Tax Free Savings Account (TFSA)

The TFSA could be another good option for a location to hold your emergency fund. However, it isn’t recommended that you use it if you are already close to maximizing the account for two reasons.

Regular deposits, and withdrawals reduce your contribution limit in the calendar year they are made. This makes you more susceptible to penalties from the CRA for over-contribution.

The TFSA is great for big financial goals such as retirement, and home purchase. Occupying space for an emergency fund may be dragging down your long term returns.

You can find out how much contribution room you have left by using the calculator here, or by using your MyCRA Account. At a minimum, make sure you have enough contribution room to allow for 6 months of essential expenses. If you need a larger emergency fund (9-12 months) based on life circumstances, this should be factored into the calculation.

Ex. If your essential expenses are $4,000. You should only use a TFSA to place your emergency fund if you have $24,000 in contribution room remaining.

If you regularly use your emergency fund (which you shouldn’t be), then the use of the TFSA becomes significantly more complicated. If this is you, I would only use the TFSA when there is a significant difference between your emergency fund size, and available contribution room. To add a margin of safety, I would aim for 2x your emergency fund.

Ex. If your essential expenses are $4,000, and you regularly use your emergency fund. You should only use a TFSA to place your emergency fund, if you have $48,000 in contribution room remaining.

As of October 2025, the best options are:

Oaken Financial- TFSA Saving Account

2.8%/year interest earned

No fees or minimum balance required.

EQ Bank- Tax Free Savings Account

1.5%/year interest earned

No fees or minimum balance required.

Discount Brokerage Firm (Non-Registered Account or TFSA)

Discount brokerage firms such as Wealthsimple or Questrade provide another good option. Using these firms you could open a Non-registered taxable account or a TFSA.

The primary benefit is these accounts allow you to invest in a variety of different asset classes including stocks, bonds, money market funds, real estate investment trusts (REITs), exchange traded funds (ETFs), etc. Many of which may provide a better rate of return than standard banking accounts.

Additionally, they both have no minimum balance fees, and low to no transaction fees. These are perks you will not get when opening up a brokerage account through many of the major providers in Canada.

How to Maximize Your Emergency Fund Returns

If you recall from earlier, an important characteristic of an emergency fund is that it provides a reasonable rate of return. This important because:

Inflation will erode the value of your cash over time.

Inflation is a measurement of the rate of change in prices over time.

Due to inflation, what you can buy with $10 today will be less 1, 3, 5, & 10 years from now.

There is an opportunity cost to idle cash.

“Cash drag” refers to the fact that funds sitting in cash (ie. not invested) drag down the performance of your entire portfolio in a bull market.

This is a delicate balancing act though because an emergency fund should also provide stability, and liquidity. Depositing the funds into any of the account options mentioned above are great options that fulfil these requirements. However, there are some investment strategies that can be used within these accounts to receive an improved return.

Stable Investment Options for Emergency Funds

Cashable or Redeemable GICs

Guaranteed Interest Certificates (GIC’s) provide the following benefits:

Safe and CDIC insured

Guaranteed return

Slightly higher rates than HISAs in some markets.

The only area of concern with GIC’s is the amount of liquidity (ie. how easily you can access your cash). Cashable GIC’s are liquid, but not as much as a standard HISA. Most major Canadian banks require a 30-90 day minimum holding period before you can cash out a ‘cashable’ GIC. This means that if you need the funds in the first 30-90 days after buying the GIC, you will not be able to access it.

It is for this reason that Cashable GIC’s are best for Canadians with a large emergency fund (6-12 months of expenses) that would like to make a better return on a portion of their money (ex. 50%).

The best cashable GIC rate as of October 2025 is:

Oaken Financial- 1 Year Cashable GIC

2.25%/year interest earned

Non-Redeemable GIC Laddering

Non-Redeemable GIC’s have better interest returns than Cashable GIC’s. But they are one of the least liquid assets you can buy. They don’t allow you to access the funds throughout the duration of the loan contract. You have to wait until the end of the term in order to receive your money back, plus any interest accrued over that time period.

Ex. You buy a 1-Year GIC earning 3% with $1,000 in October 2025. You have to wait until October 2026 until you will receive $1,030 ($1,000+3%).

However, there is a partial solution to the liquidity problem. This is a strategy known as GIC Laddering. Using this strategy you will buy GIC’s of varying time lengths (ie. 3 months, 6 months, 9 months, 1-year).

Ex. You have $12,000 in a HISA. You use $6,000 to buy 4 different GIC term lengths.

$1,500 for a 3-Month GIC

$1,500 for a 6-Month GIC

$1,500 for a 9 Month GIC

$1,500 for a 1-Year GIC

Similar to Cashable GIC’s this should only be performed if you have a 6-12 month emergency fund, and are only using 50% or less for this strategy.

As of October 2025, the best options are:

Oaken Financial- 1-Year Non-Redeemable GIC

3.4%/year interest earned

EQ Bank- 1- Year Non-Redeemable GIC

3.15%/year interest earned

Note: EQ Bank would win for an emergency fund though because they provide shorter term options such as 3 month, 6 month, and 9 month GIC’s at lower rates.

Government & Investment-Grade Bonds

Bonds are another great strategy that could be used for an emergency fund. Provided that you purchase government, or investment grade bonds, they are considered relatively low risk. However, they are not CDIC insured like normal bank deposits or GIC’s.

Bonds provide you with steady interest payments throughout the holding period. Depending on the type of bonds that you purchase, you could earn interest rates higher than HISA’s, hybrid chequing-savings accounts, and GIC’s.

The easiest way to purchase bonds is through a bond exchange traded fund (ETF). This requires you to set-up and deposit money into a brokerage account. As always we recommend a discount brokerage firm such as Wealthsimple or Questrade. There you can buy and sell bond ETFs during stock market hours (Mon-Fri 9:30am to 4:00pm). They are relatively liquid during these time periods. Unfortunately, they would not be a good asset to own if your emergency occurs on a weekend.

Since they are traded on the stock exchange the market value fluctuates slightly over time. This means that you could sell when the price is low and lose some of your principle (ie. money you used to buy the bonds).

Due to the liquidity issues with bonds its best to follow a similar strategy as GIC’s (ie. 50% allocation). However, you could increase your allocation slightly to bonds because the worst case is waiting 2-3 days for the stock market to re-open.

As of October 2025, the good bond ETF options are:

XAGH (IShares US Aggregate Bond Index ETF)

3.45% Distribution Yield, MER 0.2%

US investment grade bonds including treasury bonds and corporate bonds.

ZAG (BMO Canada Aggregate Bond Index ETF)

3.45% Distribution Yield, MER 0.09%

Canada investment grade bonds including federal, provincial, and corporate bonds.

Money Market Funds

Money market funds are a tool you can use to store an emergency fund. These funds invest in short-term government and corporate debt, which makes them relatively safe while providing slightly better returns than most savings accounts. However, they may produce less returns than Bond ETF’s and some GIC’s. Their purpose is to give investors a place to keep money with low volatility, steady growth, and quick access when needed.

The main trade-offs with money market funds are they are also not CDIC insured. Also, returns can shift depending on changes in interest rates. Like Bond ETF’s, you will need a brokerage account to buy them, which may add an extra layer of complexity if you are not already using one.

That said, for Canadians who want to balance safety with a bit of extra yield, money market funds can serve as a reasonable option within an emergency fund strategy.

As of October 2025, the a good money market fund option is:

2.77% current yield, MER 0.13%

Cash ETFs

Another option for your emergency fund is a Cash ETF. These funds are designed specifically to hold cash and generate a return that is usually higher than what you would get from a typical savings account. A good example is the Horizons Cash Maximizer ETF (CASH.TO).

Similar to Bond ETF’s, they trade just like a stock. This means that you can buy and sell them during normal market hours. They are very liquid during those times. Also, for the most part , you don’t have to worry about large swings in value since they are meant to be stable.

The downside with Cash ETFs is that they are not CDIC insured. Also, they are not liquid when the market is closed (ex. weekend).

As of October 2025, the a good cash ETF option is:

CASH.TO (Horizons Cash Maximizer ETF)

2.39% Distribution yield, MER 0.11%

Summary

Provided that you can receive 3% in a EQ Bank personal account by just setting up direct deposit, most other options don't look enticing unless you are willing to go out the risk curve by buying bonds. Even GIC rates in most cases are lower than 3%, especially on shorter term length (ie. Less than 1 year).

Bonds could provide slightly higher returns at 3.45%, but you sacrifice CDIC insurance, there is some risk of volatility, and you have to wait for market hours to access your funds. For most Canadians, the simplicity of a savings account makes it the best choice for an emergency fund at current rates.

Places NOT to Keep Your Emergency Fund

Some people may not like the answer of a savings account (such as that offered at EQ Bank) being the best place to keep their emergency fund. That is ok, we can agree to disagree. However, there are some places you should avoid putting your emergency fund regardless.

Stocks or Stock ETF’s

Stocks and Stock ETFs are an amazing option for growing your wealth in your investment accounts. Unfortunately, there is too much risk associated with using the same strategy with your emergency fund. The value of stocks can fluctuate on a daily basis. Furthermore, there is a risk of market corrections, and crashes that can significantly impact the value of your investments. For context, in recent memory during the COVID-19 crash of 2020, the S&P 500 fell 34% in five weeks.

Cryptocurrency

I am not here to argue the utility of cryptocurrency as an investment choice. You may like it, or despise it. But it doesn’t belong in your emergency fund. The fluctuations in the price of cryptos are like putting stocks on steroids. It isn’t unusual to see 10-20% or more changes in their value during a single day. During that same COVID-19 crash on March 12, 2020, Bitcoin fell by more than 39% in a single day.

Registered Retirement Savings Plan (RRSP)

The TFSA is not a great choice because of the impact on your contribution limit, however, there are no direct tax implications until you over contribute. The RRSP, on the other hand, is a very poor location to put an emergency fund because of tax implications.

Every time you withdraw funds from an RRSP they will be added to your taxable income for the year of the withdrawal. Add to this that you receive a withholding tax of 10-20% at source (time of withdrawal). This means that you will need to withdraw 10-20% more than you actually need in order to pay for the emergency.

Best Strategy for Canadians

The truth is, there isn’t a single “best” emergency fund strategy that works for everyone. However, there are principles most Canadians can follow.

A layered approach often makes the most sense:

Immediate access: Keep $500–$1,000 in your everyday chequing account.

This covers those “need cash now” moments like an urgent car repair.

Main reserve: Put several months of expenses in a high-interest savings account (HISA).

Something like EQ Bank’s Personal Account at 3% (with direct deposit) is a good example. It’s CDIC insured, pays a decent return, and you can access it instantly.

Optional growth layer: If you have a larger emergency fund (6–12 months of expenses), you could put part of it (say 25–50%) into a slightly higher-yield option like a cashable GIC or a bond ETF.

This gives you a better return without putting the whole fund at risk.

Here’s how that might play out in real life:

Example 1: Your fridge breaks down, so you dip into the $1,000 you have in chequing to pay the repair cost.

Example 2: You get laid off. After you burn through your first $1,000, you draw from your HISA to pay for monthly bills.

Example 3: The layoff lasts longer than expected so you tap into the portion you’ve put into GICs or bonds.

This gives time for non-redeemable GIC’s to expire, or you to pass the required waiting period for cashable GIC’s.

Conclusion

Your emergency fund isn’t about chasing the highest return. Instead it’s about having money that’s safe, accessible, and ready when life happens. For most Canadians, that means keeping the majority of your fund in a high-interest savings account. This provides CDIC protection, no fees, and instant access. If you’ve built a larger cushion, you can layer in some cashable GICs, or low-risk bond ETFs to squeeze out a bit more return without putting your whole safety net at risk.

The best approach is simple: a small buffer in chequing for quick expenses, several months of essentials in a HISA, and optional growth through GICs or ETFs if your fund is bigger. Build it gradually, treat contributions like a monthly bill, and stick with it. When the unexpected happens, whether it’s a flat tire, a broken fridge, or a job loss, you’ll be glad you made your emergency fund a priority.

If you like this post you may also like:

[Budgeting for Beginners: How to Take Control of Your Money]

[What Is a GIC and How Does It Work in Canada? (2025 Guide)]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

BlackRock. (2025). iShares Core U.S. Aggregate Bond ETF (XAGH). iShares by BlackRock. Retrieved October 2025, from https://www.blackrock.com

BMO Global Asset Management. (2025). BMO Aggregate Bond Index ETF (ZAG) & BMO Money Market Fund (ZMMK). Bank of Montreal. Retrieved October 2025, from https://www.bmo.com

Canadian Deposit Insurance Corporation. (2025). Protecting your deposits. https://www.cdic.ca

Canadian Social Survey / Statistics Canada. (2023, February 13). One in four Canadians are unable to cover an unexpected expense of $500. The Daily. https://www150.statcan.gc.ca/n1/daily-quotidien/230213/dq230213b-eng.htm Statistics Canada+1

Employment and Social Development Canada. (2025). Employment Insurance monitoring and assessment report. Government of Canada. Retrieved October 2025, from https://www.canada.ca

EQ Bank. (2025). Personal account and TFSA rates. Equitable Bank. Retrieved October 2025, from https://www.eqbank.ca

Horizons ETFs. (2025). Horizons Cash Maximizer ETF (CASH.TO). Horizons ETFs Management. https://www.horizonsetfs.com

Laurentian Bank of Canada. (2025). High Interest Savings Account. https://www.laurentianbank.ca

Oaken Financial. (2025). Oaken savings accounts and GICs. https://www.oaken.com

Questrade, Inc. (2025). Self-directed investing with Questrade. https://www.questrade.com

Wealthsimple. (2025). Cash account and chequing options. Wealthsimple Technologies Inc. Retrieved October 2025, from https://www.wealthsimple.com