Get our free Debt vs Invest Calculator — click here to access it

ETFs in Canada: The Smart Way to Start Investing

New to investing? Learn how ETFs offer low fees, easy diversification, and long-term returns—perfect for young Canadians getting started with money.

INVESTING FOR BEGINNERSEXCHANGE TRADED FUNDSETFS

6/9/202515 min read

Introduction: Why ETFs Matter for Young Canadians

Learning how to invest your money through a traditional stock picking approach is very complex, and time consuming to learn. In fact, a majority of people who try often lose money, or achieve below market average returns. Only a select handful of people consistently outperform the market over time.

The common solution to this problem is to outsource the management of your own money to a financial advisor. This has several benefits from a psychological perspective. However, the result is often investments in high fee, low return, and minimal transparency mutual funds. Many of which underperform relative to common stock market indices.

Fortunately, products such as index ETFs and Index funds were created to provide investors with the opportunity to access market matching returns. They do this with lower fees, and less jargon. The result is a more effective approach towards reaching your financial goals. You don’t have to believe me though…

“The winning formula for success in investing is owning the entire stock market through an index fund, and then doing nothing. Just stay the course.” - John C Bogle (Founder of Vanguard Group)

ETF Basics – Explained Simply

What exactly is an ETF?

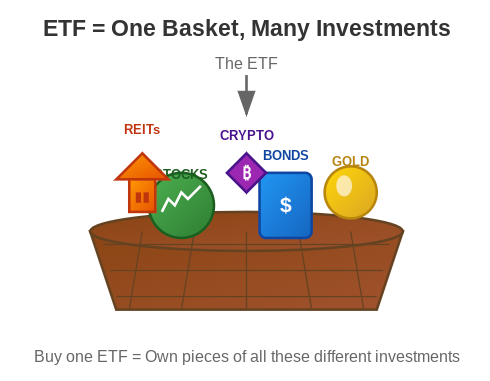

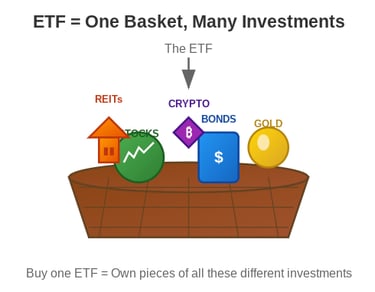

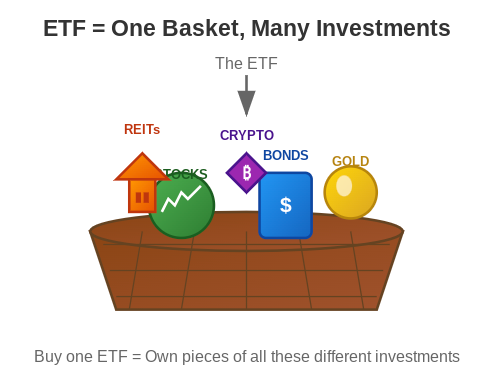

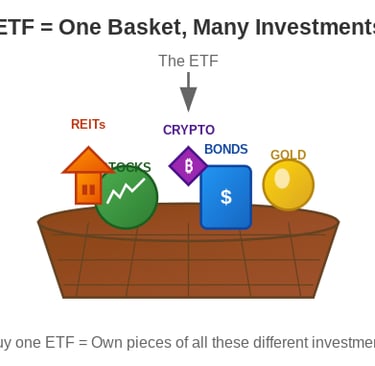

An ETF stands for Exchange Traded Fund. You can think of an ETF as a basket filled with a variety of different investments. In this analogy, the basket itself is the ETF, while the individual assets inside– stocks, bonds, REITs, gold, or cryptocurrency– are the underlying holdings.

There are a variety of different types of ETFs. Some focus on only one kind of investment class, such as stocks. Others bundle a variety of different assets into one ETF. An example of this would be ticker VGRO which consists of 80% stocks, and 20% fixed income assets such as bonds.

Following the Big Indexes

The most popular ETFs follow a major index such as the S&P 500, TSX, NASDAQ, etc.

The S&P 500 tracks the 500 largest companies on the New York Stock Exchange (NYSE). This index weights these companies based on their market capitalization– in other words their size. They are not equally weighted though, which is often a point of confusion. If this were the case each company would make up 0.2% of the index. Instead, some companies make up a larger percentage of the index, relative to others. At the time I am writing this sentence Microsoft makes up 6.73% of the entire S&P 500 index because it’s the largest company. Meanwhile, Davita Inc sitting at position #500, makes up just 0.01%.

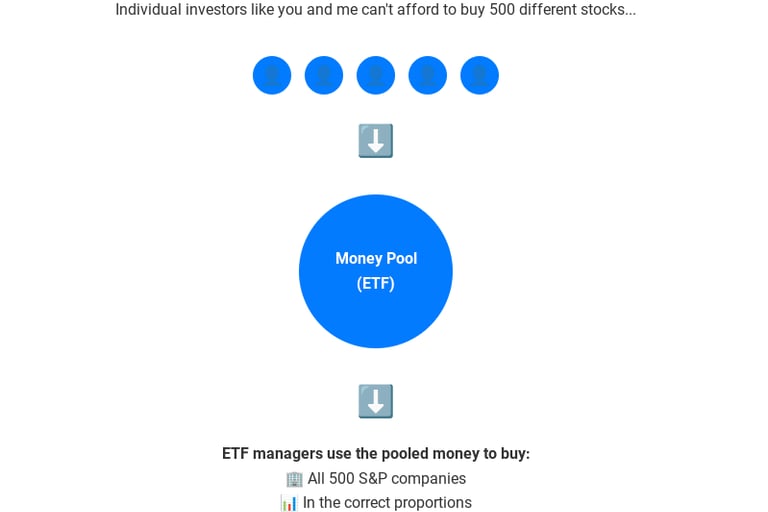

When you buy an ETF like VFV (which tracks the S&P 500), the fund managers use your money– along with money from thousands of other investors– to buy all 500 companies in their exact proportions as indicated on the S&P 500 index.

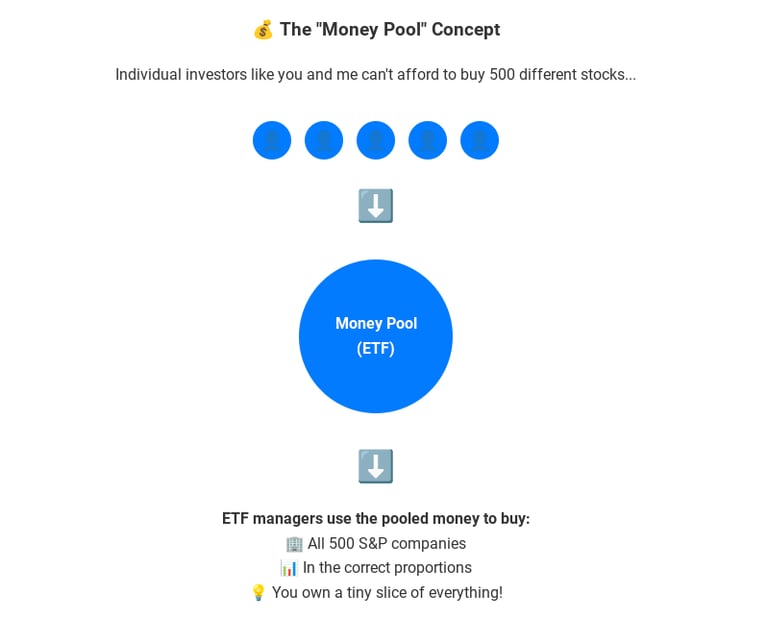

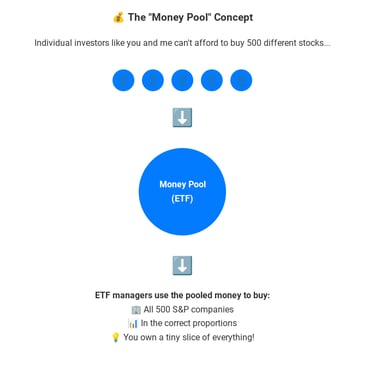

The “Money Pool” That Makes it All Work

Here’s where ETFs become very powerful. Think of it as a giant “money pool”.

As individual investors, we can’t afford to buy shares in all of the 500 different companies, especially not in the exact proportions needed to match the S&P 500. However, when thousands of investors pool their money together through an ETF, suddenly there’s enough cash to buy all of these holdings.

Every time you purchase shares in your ETF of choice, you are essentially buying a tiny slice of all of the underlying holdings. This pooling system is what makes ETFs so accessible for everyday investors like you and I. It allows us access to broad market exposure without the complexity of building a diversified portfolio from scratch, and the cost of actively managed funds.

Why ETFs Are Perfect for Beginners

If you are new to investing, ETFs offer several advantages that make them an ideal option to get started on your investment journey. Let's break down why they have become the go-to choice for beginner investors in Canada like yourself:

Super Easy

ETF investments are known as “passive investing”, and the name says it all. There is a small amount of upfront research required to find an ETF that matches your risk tolerance. After which point you can compare similar ETF options to find the lowest fee provider. Despite this the barrier to entry is very low.

This method of investing differs from the active approach of picking individual stocks. You don’t need to analyze complex financial statements, predict market trends, or constantly monitor your holdings. Instead ETFs let you “set it and forget it”. They allow you to automate your investments through regular purchases, and move on to more important areas of your life. They provide you with the freedom to focus on what really matters: your career, family, and hobbies. All while your investments grow in the background, with little to no work on your part.

Low Fees

Probably the greatest benefit of ETFs is the low cost structure. As we discussed in our post titled “Should You Hire a Financial Advisor in Canada?” the fees of mutual funds in Canada can range from anywhere between 1-3%. Most ETFs charge a fraction of that. Take VFV, for example– it has a management expense ratio (MER) of just 0.09%.

What does this mean in real dollars?

Let's say that you earn an average of 7% annual return:

Average Mutual Fund: You keep 4-6% after fees

Exchange Traded Fund (ie. VFV): You keep 6.91% after fees

The Long-Term Impact Will Shock You

Just to show you how incomprehensible the impact of fees are on long term returns lets use a real life example: Imagine you start investing at 20 years old with $10,000. You invest an additional $200/month until you’re 65 years of age, this is how much your will have:

Index ETF= $890,734

Mutual Fund= $662,124

The Difference= $228,610

In other words, those “small” extra fees charged by an actively managed mutual fund could cost you nearly a quarter of a million dollars over your investing lifetime. I don’t know about you but that seems like an expensive price to pay if you ask me.

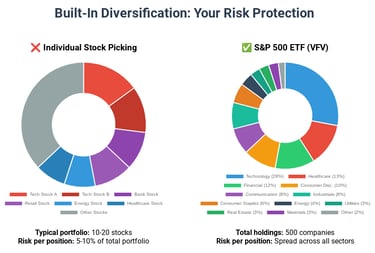

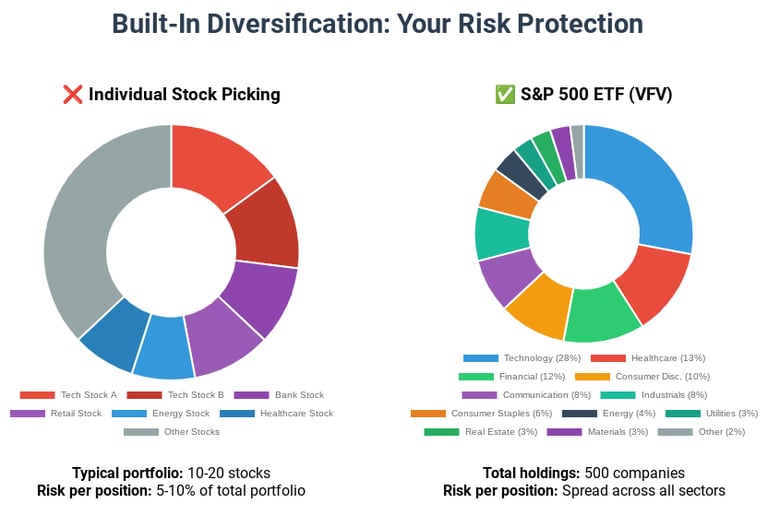

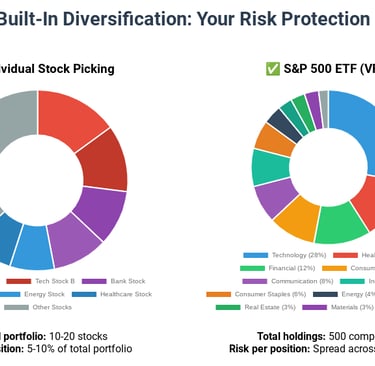

Diversified

A mistake often made by new investors is putting all of their eggs in one basket. We have all heard the stories of people who invested their life savings in Gamestop. This is risky because all that needs to happen is for that one company to fail and will lose all of your money. ETFs solve this issue.

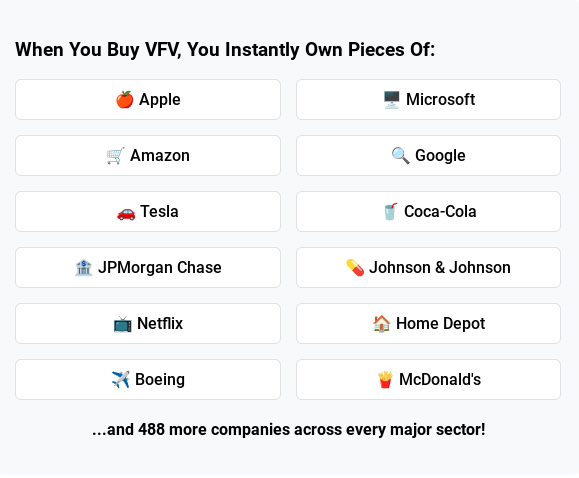

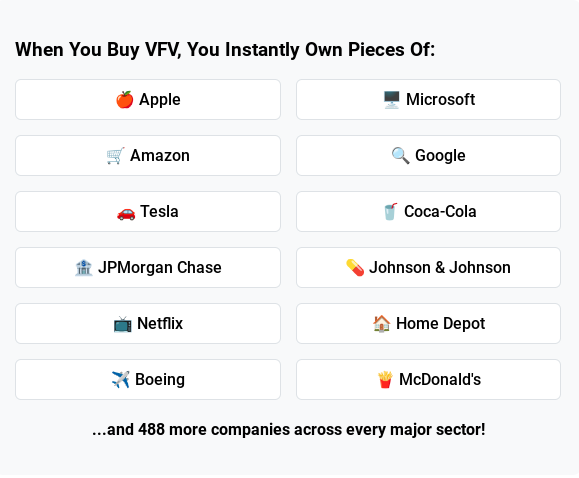

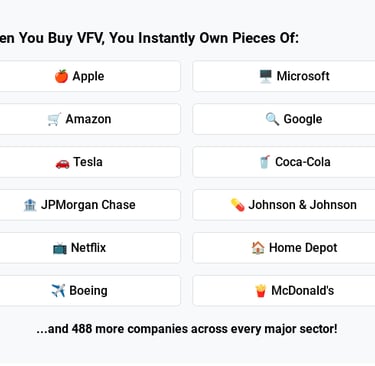

A stock index ETF, like VFV, allows you to purchase shares in 500 different companies, across a variety of different sectors.

Technology Companies like Microsoft and Apple

Financial Institutions like JPMorgan Chase

Healthcare Giants like Johnson & Johnson

Consumer Brands like Coca-Cola

Etc

This diversification provides protection against three major risks:

Company Specific Risk (One company going bankrupt)

Sector Specific Risk (Entire Sector Headwinds)

Country Specific Risk (Problems in One Country/Economy, or Currency Depreciation)

In other words, your long term returns will be less impacted by head winds to a specific company, sector, or country. Much of which are uncontrollable, and in many cases unpredictable to the average investor.

Most active investors opt for a portfolio of 10-20 stocks at most, meaning each individual position represents 5-10% of their portfolio. The problem with this is that if on company tanks, it could result in a precipitous drop in your overall returns. With 500+ companies in your ETF, even if several fail, your returns will likely remain relatively stable. Thus, the benefit of diversification is that it smooths out the results of long term returns, and reduces the downside risk.

Flexibility

ETFs trade on stock exchanges just like individual stocks. This means that you can buy and sell them during market hours, in a moment’s notice. Think about that power– you can instantly buy or sell your stake in 500+ companies with the click of a button.

Compare this to other investment options:

Mutual Funds

Often requires you to call your financial advisor/money manager.

They may have minimal holding periods, and/or penalties for early selling.

Individual Stocks

Need to make separate buy/sell decisions for each individual holding, which is time consuming.

Trading fees incurred with each action.

No Minimums Investment Barriers

Traditional investing used to require significant upfront capital. This high frictional cost to starting made it unavailable to many beginner investors. Shares in an individual company can be costly. For example: One of Canada’s top performing companies is Constellation Software (Ticker: CSU) currently trades at $5,063 per share.

Fortunately, most ETFs trade between $20-50/share, making them accessible to almost anyone. Even better, the introduction of fractional shares by discount brokerage firms such as Questrade and Wealthsimple means you can get started with as little as $1.

This feature now also exists for individual stocks as well. For example: You can currently buy 0.00197% of CSU with $10. This is an option that until recently never existed. Unfortunately, not all brokerage firms offer partial shares yet which means the barrier still exists for some Canadians though.

Important Caveat: Index Only

Here is where we need to pump the brakes. The world of ETF investing has become extremely complex with the introduction of products such as leveraged ETFs, sector-specific funds, ESG-focused options, and other specialized products.

This isn’t to say that these choices won’t perform well, as they can and some have. However, these products often just reintroduce the complexity and higher fees that the ETF market was originally created to avoid. They are often just disguised forms of active management. The manager of the ETF can increase their fee structure because there is now research involved on their part. The result of which is often worse performance, and higher fees…both of which eat into your long term returns.

Although we don’t provide recommendations. Historical returns suggest that a broad based market index ETF that tracks established indexes like the S&P 500 is likely to outperform over the long term. In which case keeping it simple, reducing your fees, and letting the market do the work appears to be the smarter option. Don’t let Wall Street trick you into thinking complexity is the solution.

Conclusion

ETFs provide all investors, especially beginners, with an opportunity to to grow their wealth. They are better then other products because of their flexibility, diversification, and ease of access. Meanwhile, they do this all at a low cost. Next week we will dive into the top 3 types of ETFs you should know about when making your investment portfolio.

If you like this post you may also like:

[Charlie Munger Was Right: The First $100K Matters More Than You Think]

[How Investments Are Taxed in Canada: Taxable Accounts Guide]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

Bogle, J. C. (2017). The little book of common sense investing: The only way to guarantee your fair share of stock market returns (10th anniversary ed.). Wiley.

Fernando, J. (2024, October 31). What is the average annual return for the S&P 500? Investopedia. https://www.investopedia.com/ask/answers/042415/what-average-annual-return-sp-500.asp

Get Smarter About Money. (n.d.). Compound interest calculator. https://www.getsmarteraboutmoney.ca/calculators/compound-interest-calculator/

SlickCharts. (n.d.). S&P 500 companies list. https://www.slickcharts.com/sp500

Vanguard Canada. (n.d.). Vanguard S&P 500 index ETF (VFV). https://www.vanguard.ca/en/product/etf/equity/9563/vanguard-sp-500-index-etf

Introduction: Why ETFs Matter for Young Canadians

Learning how to invest your money through a traditional stock picking approach is very complex, and time consuming to learn. In fact, a majority of people who try often lose money, or achieve below market average returns. Only a select handful of people consistently outperform the market over time.

The common solution to this problem is to outsource the management of your own money to a financial advisor. This has several benefits from a psychological perspective. However, the result is often investments in high fee, low return, and minimal transparency mutual funds. Many of which underperform relative to common stock market indices.

Fortunately, products such as index ETFs and Index funds were created to provide investors with the opportunity to access market matching returns. They do this with lower fees, and less jargon. The result is a more effective approach towards reaching your financial goals. You don’t have to believe me though…

“The winning formula for success in investing is owning the entire stock market through an index fund, and then doing nothing. Just stay the course.” - John C Bogle (Founder of Vanguard Group)

ETF Basics – Explained Simply

What exactly is an ETF?

An ETF stands for Exchange Traded Fund. You can think of an ETF as a basket filled with a variety of different investments. In this analogy, the basket itself is the ETF, while the individual assets inside– stocks, bonds, REITs, gold, or cryptocurrency– are the underlying holdings.

There are a variety of different types of ETFs. Some focus on only one kind of investment class, such as stocks. Others bundle a variety of different assets into one ETF. An example of this would be ticker VGRO which consists of 80% stocks, and 20% fixed income assets such as bonds.

Following the Big Indexes

The most popular ETFs follow a major index such as the S&P 500, TSX, NASDAQ, etc.

The S&P 500 tracks the 500 largest companies on the New York Stock Exchange (NYSE). This index weights these companies based on their market capitalization– in other words their size. They are not equally weighted though, which is often a point of confusion. If this were the case each company would make up 0.2% of the index. Instead, some companies make up a larger percentage of the index, relative to others. At the time I am writing this sentence Microsoft makes up 6.73% of the entire S&P 500 index because it’s the largest company. Meanwhile, Davita Inc sitting at position #500, makes up just 0.01%.

When you buy an ETF like VFV (which tracks the S&P 500), the fund managers use your money– along with money from thousands of other investors– to buy all 500 companies in their exact proportions as indicated on the S&P 500 index.

The “Money Pool” That Makes it All Work

Here’s where ETFs become very powerful. Think of it as a giant “money pool”.

As individual investors, we can’t afford to buy shares in all of the 500 different companies, especially not in the exact proportions needed to match the S&P 500. However, when thousands of investors pool their money together through an ETF, suddenly there’s enough cash to buy all of these holdings.

Every time you purchase shares in your ETF of choice, you are essentially buying a tiny slice of all of the underlying holdings. This pooling system is what makes ETFs so accessible for everyday investors like you and I. It allows us access to broad market exposure without the complexity of building a diversified portfolio from scratch, and the cost of actively managed funds.

Why ETFs Are Perfect for Beginners

If you are new to investing, ETFs offer several advantages that make them an ideal option to get started on your investment journey. Let's break down why they have become the go-to choice for beginner investors in Canada like yourself:

Super Easy

ETF investments are known as “passive investing”, and the name says it all. There is a small amount of upfront research required to find an ETF that matches your risk tolerance. After which point you can compare similar ETF options to find the lowest fee provider. Despite this the barrier to entry is very low.

This method of investing differs from the active approach of picking individual stocks. You don’t need to analyze complex financial statements, predict market trends, or constantly monitor your holdings. Instead ETFs let you “set it and forget it”. They allow you to automate your investments through regular purchases, and move on to more important areas of your life. They provide you with the freedom to focus on what really matters: your career, family, and hobbies. All while your investments grow in the background, with little to no work on your part.

Low Fees

Probably the greatest benefit of ETFs is the low cost structure. As we discussed in our post titled “Should You Hire a Financial Advisor in Canada?” the fees of mutual funds in Canada can range from anywhere between 1-3%. Most ETFs charge a fraction of that. Take VFV, for example– it has a management expense ratio (MER) of just 0.09%.

What does this mean in real dollars?

Let's say that you earn an average of 7% annual return:

Average Mutual Fund: You keep 4-6% after fees

Exchange Traded Fund (ie. VFV): You keep 6.91% after fees

The Long-Term Impact Will Shock You

Just to show you how incomprehensible the impact of fees are on long term returns lets use a real life example: Imagine you start investing at 20 years old with $10,000. You invest an additional $200/month until you’re 65 years of age, this is how much your will have:

Index ETF= $890,734

Mutual Fund= $662,124

The Difference= $228,610

In other words, those “small” extra fees charged by an actively managed mutual fund could cost you nearly a quarter of a million dollars over your investing lifetime. I don’t know about you but that seems like an expensive price to pay if you ask me.

Diversified

A mistake often made by new investors is putting all of their eggs in one basket. We have all heard the stories of people who invested their life savings in Gamestop. This is risky because all that needs to happen is for that one company to fail and will lose all of your money. ETFs solve this issue.

A stock index ETF, like VFV, allows you to purchase shares in 500 different companies, across a variety of different sectors.

Technology Companies like Microsoft and Apple

Financial Institutions like JPMorgan Chase

Healthcare Giants like Johnson & Johnson

Consumer Brands like Coca-Cola

Etc

This diversification provides protection against three major risks:

Company Specific Risk (One company going bankrupt)

Sector Specific Risk (Entire Sector Headwinds)

Country Specific Risk (Problems in One Country/Economy, or Currency Depreciation)

In other words, your long term returns will be less impacted by head winds to a specific company, sector, or country. Much of which are uncontrollable, and in many cases unpredictable to the average investor.

Most active investors opt for a portfolio of 10-20 stocks at most, meaning each individual position represents 5-10% of their portfolio. The problem with this is that if on company tanks, it could result in a precipitous drop in your overall returns. With 500+ companies in your ETF, even if several fail, your returns will likely remain relatively stable. Thus, the benefit of diversification is that it smooths out the results of long term returns, and reduces the downside risk.

Flexibility

ETFs trade on stock exchanges just like individual stocks. This means that you can buy and sell them during market hours, in a moment’s notice. Think about that power– you can instantly buy or sell your stake in 500+ companies with the click of a button.

Compare this to other investment options:

Mutual Funds

Often requires you to call your financial advisor/money manager.

They may have minimal holding periods, and/or penalties for early selling.

Individual Stocks

Need to make separate buy/sell decisions for each individual holding, which is time consuming.

Trading fees incurred with each action.

No Minimums Investment Barriers

Traditional investing used to require significant upfront capital. This high frictional cost to starting made it unavailable to many beginner investors. Shares in an individual company can be costly. For example: One of Canada’s top performing companies is Constellation Software (Ticker: CSU) currently trades at $5,063 per share.

Fortunately, most ETFs trade between $20-50/share, making them accessible to almost anyone. Even better, the introduction of fractional shares by discount brokerage firms such as Questrade and Wealthsimple means you can get started with as little as $1.

This feature now also exists for individual stocks as well. For example: You can currently buy 0.00197% of CSU with $10. This is an option that until recently never existed. Unfortunately, not all brokerage firms offer partial shares yet which means the barrier still exists for some Canadians though.

Important Caveat: Index Only

Here is where we need to pump the brakes. The world of ETF investing has become extremely complex with the introduction of products such as leveraged ETFs, sector-specific funds, ESG-focused options, and other specialized products.

This isn’t to say that these choices won’t perform well, as they can and some have. However, these products often just reintroduce the complexity and higher fees that the ETF market was originally created to avoid. They are often just disguised forms of active management. The manager of the ETF can increase their fee structure because there is now research involved on their part. The result of which is often worse performance, and higher fees…both of which eat into your long term returns.

Although we don’t provide recommendations. Historical returns suggest that a broad based market index ETF that tracks established indexes like the S&P 500 is likely to outperform over the long term. In which case keeping it simple, reducing your fees, and letting the market do the work appears to be the smarter option. Don’t let Wall Street trick you into thinking complexity is the solution.

Conclusion

ETFs provide all investors, especially beginners, with an opportunity to to grow their wealth. They are better then other products because of their flexibility, diversification, and ease of access. Meanwhile, they do this all at a low cost. Next week we will dive into the top 3 types of ETFs you should know about when making your investment portfolio.

If you like this post you may also like:

[Charlie Munger Was Right: The First $100K Matters More Than You Think]

[How Investments Are Taxed in Canada: Taxable Accounts Guide]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

Bogle, J. C. (2017). The little book of common sense investing: The only way to guarantee your fair share of stock market returns (10th anniversary ed.). Wiley.

Fernando, J. (2024, October 31). What is the average annual return for the S&P 500? Investopedia. https://www.investopedia.com/ask/answers/042415/what-average-annual-return-sp-500.asp

Get Smarter About Money. (n.d.). Compound interest calculator. https://www.getsmarteraboutmoney.ca/calculators/compound-interest-calculator/

SlickCharts. (n.d.). S&P 500 companies list. https://www.slickcharts.com/sp500

Vanguard Canada. (n.d.). Vanguard S&P 500 index ETF (VFV). https://www.vanguard.ca/en/product/etf/equity/9563/vanguard-sp-500-index-etf