Get our free Debt vs Invest Calculator — click here to access it

Stocks vs Bonds in Canada: How Much Should You Invest?

How much should you invest in stocks vs bonds in Canada? Learn how your risk tolerance, age, and income requirements impacts your decision.

INVESTING FOR BEGINNERSINVESTINGSTOCKSBONDS

2/22/202511 min read

Stocks vs Bonds?

The debate of stocks vs bonds is one that has been happening since the dawn of their creation.

Some people go 100% into stocks because they know that based on historical data, doing that will yield the highest returns. On the other hand, there are people who enjoy the safety and stability of bonds and are happy with the monthly/quarterly/annual payments they get.

So, who is right and who is wrong? Or is it actually possible to have your cake and eat it too, despite what your parents told you?

Ask the Right Questions

We believe that the right amount to invest in stocks or bonds hinges on your answers to following three key questions:

What is your risk tolerance?

How old are you?

How much do you rely on your investments for income?

Realistically, we don’t expect you to just magically understand why these questions are important in your decision making. Each question is nuanced, so we have gone through each of them below to help you make up your mind.

Risk Tolerance

On a long enough time horizon (>5 years) stocks almost always outperform bonds. A CIBC report analyzed a century's worth of returns from 1920 to 2019, revealing that stocks averaged a 10.9% return, while bonds delivered a 4.9% return[2].

So why don’t you just hold 100% of your investments in stocks?

Despite superior performance the stock market has a large amount of volatility. What that means is that there is a large range of price fluctuation. Very big drops in price one year could be followed by a very large increase the next year, and vice versa.

We know that the average annual return of the S&P 500 is ~10% / year. However, in a year like 2008 it fell by approximately 39% in one year (3). Meanwhile, between the years 2019-2021 it rose a whopping 72% (3). This means there was an average annualized return of ~24% /year over this time period. Thus, in order to get a 10% return /year on your money you often have to tolerate a roller coaster ride in the process when you decide to invest solely in stocks.

The benefit of holding bonds is less of this volatility, and more consistent returns over time…albeit lower returns than stocks.

Ask yourself: Can you tolerate a 39% drop in the value of your investments? For example, if you had $100,000 in stocks and it went down by $39,000 to $61,000, could you still sleep well at night? If your answer to this question is no, then you should consider allocating a larger percentage of your investments to bonds.

Age

Your investment life should be divided into two main phases:

Wealth Accumulation Phase

In the early stages of investing, your goal is to maximize the growth of your investments. When you are young you have a long time period over which your money can compound. The higher the rate of return over that period the greater your retirement nest egg will be. Additionally, a greater rate of return has the potential to shorten your required investment time frame to reach financial independence. This could allow you to retire earlier then otherwise anticipated.

Achieving maximal growth relies on two key strategies: saving as much as possible and investing in assets with the highest return potential. Stocks often fulfill this role effectively.

Therefore, the younger you are, the higher the percentage of your investments should be allocated to stocks.

Wealth Preservation Phase

As you approach retirement, your focus shifts from aggressive growth to preserving your wealth. By this point, you likely have accumulated the nest egg needed for your retirement years.

This shift in focus is essential not only during retirement but also in the years leading up to it. There's a real risk that a stock market downturn could force you to delay your retirement.

Since bonds provide a steady return with less volatility, holding a higher percentage of bonds as you near retirement serves as an effective risk management tool.

Income

The last section is a simple question, do you rely on your investments for income?

When you are young this seems like a far fetched dream. How could I possibly save enough money to live off my investments?

However, there are a few scenarios where this may be the case such as:

FIRE (Financial Independence Retire Early) Community

Traditional Retirement (~60-65 years old)

Laid off/ Unemployed with a high amount of savings

When you depend on your investments for income the primary thing you seek is not maximal growth… although that would be nice. Rather you want stability.

In each of these scenarios our goal should be maximum risk mitigation and ensure a steady income stream.

The 4% Rule

In traditional retirement planning, the widely used "4% rule" suggests that you can safely withdraw 4% of your total investments (ie. Adjusted for inflation) each year before running out of money.

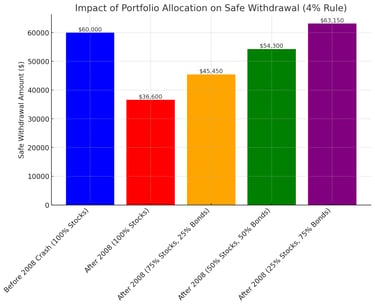

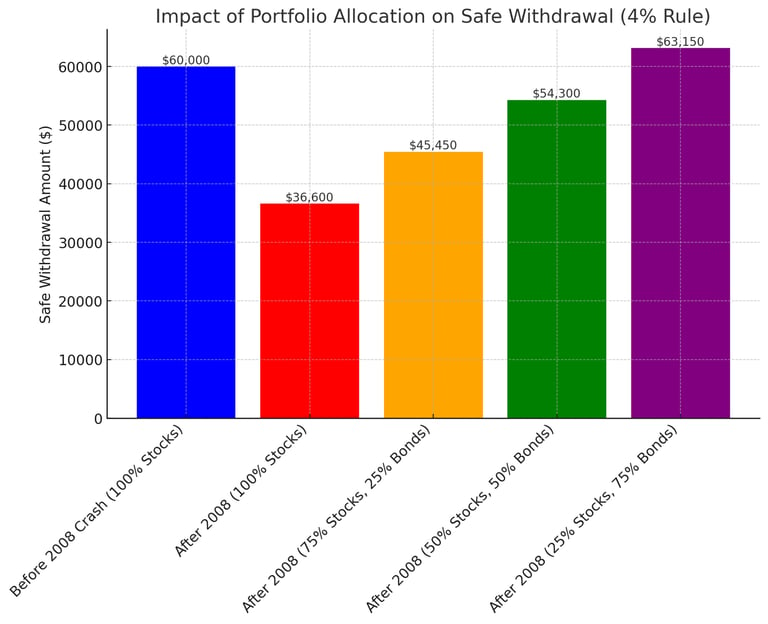

For example: If you retire with a $1,500,000 investment portfolio and use the 4% rule, you would be able to withdraw $60,000 annually, over the course of 30 years, without running out of money.

This rule is highly debated, which we will discuss in a future blog. However, it is a good illustration of a typical retirement planning approach. This withdrawal rate should help prevent you from overspending, and depleting your savings too quickly. Also, it can help the super savers amongst us from being too frugal, and not enjoying their hard-earned money.

Mitigating the Damage

Consider the case of 2008 when the S&P 500 plummeted by 39%. Using the above example, If your entire investment portfolio was in stocks before this downturn, your initial $1,500,000 would have shrunk to $915,000. Applying the 4% rule, you could safely withdraw $36,600 that year without endangering the long-term viability of your investment.

This is a drop from $60,000 during good times to $36,600 because of a poor year in the financial markets…That is a significant pay cut if you ask me.

In contrast, US Treasury Bonds saw gains of over 20% that year, and high-grade Corporate Bonds experienced only a 5% decline[1]. If you held some of your investments in high-quality bonds, you would have fared much better, perhaps experiencing a slight reduction in income rather than a drastic salary cut.

For Example: Let’s now imagine that before 2008 you held 50% in US Treasury bonds (ie. $750,000), and 50% in stocks (ie. $750,000). The crash takes place and the bond portion of your portfolio increases by 20%, and the stock portion of your portfolio decreases by 39%. In this scenario your bonds will grow to $900,000, and your stocks would shrink to $457,500. This would bring your total portfolio to $1,357,500. Applying the 4% rule your safe withdrawal amount would be $54,300. Although there is still a pay cut, it is likely a much more manageable decrease for the average person to tolerate.

While this example is extreme, it underscores the importance of holding a larger percentage of bonds if you depend on your investments for income.

What do the experts say?

There are several allocation recommendations that exist including:

60/40 Split (60% stocks, 40% bonds)

Two Phases Approach

Wealth Accumulation Phase (75% stocks, 25% bonds)

Wealth Preservation Phase (75% bonds, 25% stocks)

50/50 Split (50% bonds, 50% stocks)

Age= % of Bonds (ex. If you are 60 years old you should hold 60% in bonds, 40% in stocks)

As you can see all of the rules are slightly different but we can draw some commonalities:

Invest more in stocks when you are:

Young

Trying to grow your wealth

Have a high risk tolerance

Don’t rely on your investments for income.

Invest more in bonds when you are:

Nearing or in retirement

Trying to preserve your wealth

Have a low risk tolerance

Rely on your investments for income.

Related Posts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Historical returns on stocks, Bonds and bills: 1928-2022. Welcome to Pages at the Stern School of Business, New York University. (n.d.). https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html.

OpenAI. (2025). Graph comparing 4% safe withdrawal rate of $1, 500, 000 before and after the 2008 financial crash using different bond and stock allocations [AI-generated graph]. ChatGPT. https://chat.openai.com/.

Loo, E. (n.d.). Stocks vs. bonds over the past 100 years . woogundyadvisors.cibc.com. https://woodgundyadvisors.cibc.com/documents/525322/667371/V11I02-AA.pdf/0f4c9ed7-2e68-4497-9994-1556b6f93eeb.

S&P 500 historical annual returns. MacroTrends. (n.d.). https://www.macrotrends.net/2526/sp-500-historical-annual-returns.

Stocks vs Bonds?

The debate of stocks vs bonds is one that has been happening since the dawn of their creation.

Some people go 100% into stocks because they know that based on historical data, doing that will yield the highest returns. On the other hand, there are people who enjoy the safety and stability of bonds and are happy with the monthly/quarterly/annual payments they get.

So, who is right and who is wrong? Or is it actually possible to have your cake and eat it too, despite what your parents told you?

Ask the Right Questions

We believe that the right amount to invest in stocks or bonds hinges on your answers to following three key questions:

What is your risk tolerance?

How old are you?

How much do you rely on your investments for income?

Realistically, we don’t expect you to just magically understand why these questions are important in your decision making. Each question is nuanced, so we have gone through each of them below to help you make up your mind.

Risk Tolerance

On a long enough time horizon (>5 years) stocks almost always outperform bonds. A CIBC report analyzed a century's worth of returns from 1920 to 2019, revealing that stocks averaged a 10.9% return, while bonds delivered a 4.9% return[2].

So why don’t you just hold 100% of your investments in stocks?

Despite superior performance the stock market has a large amount of volatility. What that means is that there is a large range of price fluctuation. Very big drops in price one year could be followed by a very large increase the next year, and vice versa.

We know that the average annual return of the S&P 500 is ~10% / year. However, in a year like 2008 it fell by approximately 39% in one year (3). Meanwhile, between the years 2019-2021 it rose a whopping 72% (3). This means there was an average annualized return of ~24% /year over this time period. Thus, in order to get a 10% return /year on your money you often have to tolerate a roller coaster ride in the process when you decide to invest solely in stocks.

The benefit of holding bonds is less of this volatility, and more consistent returns over time…albeit lower returns than stocks.

Ask yourself: Can you tolerate a 39% drop in the value of your investments? For example, if you had $100,000 in stocks and it went down by $39,000 to $61,000, could you still sleep well at night? If your answer to this question is no, then you should consider allocating a larger percentage of your investments to bonds.

Age

Your investment life should be divided into two main phases:

Wealth Accumulation Phase

In the early stages of investing, your goal is to maximize the growth of your investments. When you are young you have a long time period over which your money can compound. The higher the rate of return over that period the greater your retirement nest egg will be. Additionally, a greater rate of return has the potential to shorten your required investment time frame to reach financial independence. This could allow you to retire earlier then otherwise anticipated.

Achieving maximal growth relies on two key strategies: saving as much as possible and investing in assets with the highest return potential. Stocks often fulfill this role effectively.

Therefore, the younger you are, the higher the percentage of your investments should be allocated to stocks.

Wealth Preservation Phase

As you approach retirement, your focus shifts from aggressive growth to preserving your wealth. By this point, you likely have accumulated the nest egg needed for your retirement years.

This shift in focus is essential not only during retirement but also in the years leading up to it. There's a real risk that a stock market downturn could force you to delay your retirement.

Since bonds provide a steady return with less volatility, holding a higher percentage of bonds as you near retirement serves as an effective risk management tool.

Income

The last section is a simple question, do you rely on your investments for income?

When you are young this seems like a far fetched dream. How could I possibly save enough money to live off my investments?

However, there are a few scenarios where this may be the case such as:

FIRE (Financial Independence Retire Early) Community

Traditional Retirement (~60-65 years old)

Laid off/ Unemployed with a high amount of savings

When you depend on your investments for income the primary thing you seek is not maximal growth… although that would be nice. Rather you want stability.

In each of these scenarios our goal should be maximum risk mitigation and ensure a steady income stream.

The 4% Rule

In traditional retirement planning, the widely used "4% rule" suggests that you can safely withdraw 4% of your total investments (ie. Adjusted for inflation) each year before running out of money.

For example: If you retire with a $1,500,000 investment portfolio and use the 4% rule, you would be able to withdraw $60,000 annually, over the course of 30 years, without running out of money.

This rule is highly debated, which we will discuss in a future blog. However, it is a good illustration of a typical retirement planning approach. This withdrawal rate should help prevent you from overspending, and depleting your savings too quickly. Also, it can help the super savers amongst us from being too frugal, and not enjoying their hard-earned money.

Mitigating the Damage

Consider the case of 2008 when the S&P 500 plummeted by 39%. Using the above example, If your entire investment portfolio was in stocks before this downturn, your initial $1,500,000 would have shrunk to $915,000. Applying the 4% rule, you could safely withdraw $36,600 that year without endangering the long-term viability of your investment.

This is a drop from $60,000 during good times to $36,600 because of a poor year in the financial markets…That is a significant pay cut if you ask me.

In contrast, US Treasury Bonds saw gains of over 20% that year, and high-grade Corporate Bonds experienced only a 5% decline[1]. If you held some of your investments in high-quality bonds, you would have fared much better, perhaps experiencing a slight reduction in income rather than a drastic salary cut.

For Example: Let’s now imagine that before 2008 you held 50% in US Treasury bonds (ie. $750,000), and 50% in stocks (ie. $750,000). The crash takes place and the bond portion of your portfolio increases by 20%, and the stock portion of your portfolio decreases by 39%. In this scenario your bonds will grow to $900,000, and your stocks would shrink to $457,500. This would bring your total portfolio to $1,357,500. Applying the 4% rule your safe withdrawal amount would be $54,300. Although there is still a pay cut, it is likely a much more manageable decrease for the average person to tolerate.

While this example is extreme, it underscores the importance of holding a larger percentage of bonds if you depend on your investments for income.

What do the experts say?

There are several allocation recommendations that exist including:

60/40 Split (60% stocks, 40% bonds)

Two Phases Approach

Wealth Accumulation Phase (75% stocks, 25% bonds)

Wealth Preservation Phase (75% bonds, 25% stocks)

50/50 Split (50% bonds, 50% stocks)

Age= % of Bonds (ex. If you are 60 years old you should hold 60% in bonds, 40% in stocks)

As you can see all of the rules are slightly different but we can draw some commonalities:

Invest more in stocks when you are:

Young

Trying to grow your wealth

Have a high risk tolerance

Don’t rely on your investments for income.

Invest more in bonds when you are:

Nearing or in retirement

Trying to preserve your wealth

Have a low risk tolerance

Rely on your investments for income.

Related Posts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Historical returns on stocks, Bonds and bills: 1928-2022. Welcome to Pages at the Stern School of Business, New York University. (n.d.). https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html.

OpenAI. (2025). Graph comparing 4% safe withdrawal rate of $1, 500, 000 before and after the 2008 financial crash using different bond and stock allocations [AI-generated graph]. ChatGPT. https://chat.openai.com/.

Loo, E. (n.d.). Stocks vs. bonds over the past 100 years . woogundyadvisors.cibc.com. https://woodgundyadvisors.cibc.com/documents/525322/667371/V11I02-AA.pdf/0f4c9ed7-2e68-4497-9994-1556b6f93eeb.

S&P 500 historical annual returns. MacroTrends. (n.d.). https://www.macrotrends.net/2526/sp-500-historical-annual-returns.