Get our free Debt vs Invest Calculator — click here to access it

Six Common TFSA Mistakes & How to Avoid Them

Avoid these common TFSA mistakes and maximize your tax-free savings. Learn how to use your TFSA correctly, avoid penalties, and grow your wealth tax-free.

TFSATAX FREE SAVINGS ACCOUNT

3/22/202514 min read

Introduction

A quote by James Joyce that we really like is “ mistakes are the portals of discovery” [1]. If you read our previous blog post here, you would know that we highly rate the TFSA. Now we’re sure you’re excited to throw everything but the kitchen sink at it.

However, before you do that, we want to highlight the six most common mistakes we have noticed most people make when it comes to the TFSA. We’re happy enough to teach you the common areas to avoid, so you can skip the “discovery” phase and start off on the right foot (at least in regards to investing).

Let's get started with the first huge mistake that the financial post says that half of Canadians make [2]:

1. Treating a TFSA as a Savings Account Instead of an Investment Account

One of the most common mistakes people make is viewing the TFSA as a traditional savings account. It is understandable though because the TFSA suffers from what we call “accidental false advertising” due to the poor naming of the account. A more appropriate name would be something like a Tax Free Investment Account. While TFSAs do allow you to save money, their true potential is in their ability to serve as investment vehicles.

The primary benefit of a TFSA is tax-free growth.

Example: If you invest $10,000 today and it grows to $20,000 in 20 years, you are not taxed on the $10,000 of gain made over this time period.

Many people commonly deposit their money into a traditional tax free savings account at their institution of choice. These accounts generally provide low-interest returns. However, within a TFSA you have the opportunity to invest in a wide range of assets, including:

Stocks & Bonds

Mutual funds, Index Funds, Exchange Traded Funds (ETF’s)

Guaranteed Investment Certificates (GIC’s)

Money Market Funds

Etc.

Each of these investments has the potential to generate substantial returns over time, all of which remain tax-free within the account.

In summary, TFSA's are not limited to low-yield savings options; they are a versatile investment tools that can help you achieve your long-term financial goals. By thinking of your TFSA as an investment account, you can take advantage of the power of compounding and potentially build substantial wealth over the course of your life.

2. Confusing Contribution Limits with Maximum Holdings

There is an annual contribution limit which varies from year to year. Your total contribution limit depends on how old you are, and whether or not you have previously contributed. However, it's important to understand that this limit doesn't represent the maximum amount you can hold in your TFSA. In fact, your TFSA can grow substantially beyond the contribution limits.

Example: Consider Becky, who turned 18 in 2009 and was eligible to open a TFSA. Suppose her contribution room for the years 2009 to 2024 amounted to a total of $95,000 based on the varying annual limits.

In 2009, Becky deposited the maximum allowable amount, which was $5,000. Over the next 13 years, she continued to contribute the maximum annual amount. During this time, she made a consistent 7% annual return on her investments within the TFSA by investing in a low cost index fund.

By 2024, her cumulative contributions would have reached $95,000, which is her contribution limit. However, the magic of tax-free growth allowed her investments to grow significantly. Her TFSA was actually worth $175,000, far exceeding her contribution limit.

The two key take-away’s are:

The contribution limit represents the maximum amount you can contribute (deposit) to your TFSA in any given year.

The total value of your TFSA can surpass that limit as your investments grow over time.

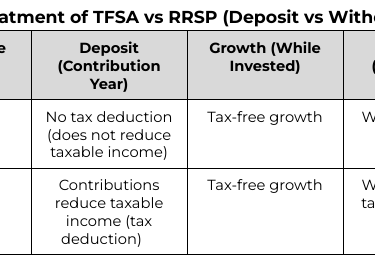

3. Not Understanding TFSA Tax Benefits

Another common mistake is that people often group the TFSA and RRSP into the same category of accounts. We will discuss the RRSP in further detail in our next post, but for today’s sake here are the main differences:

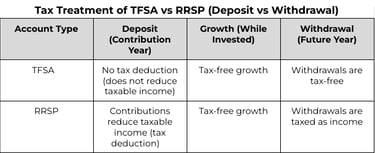

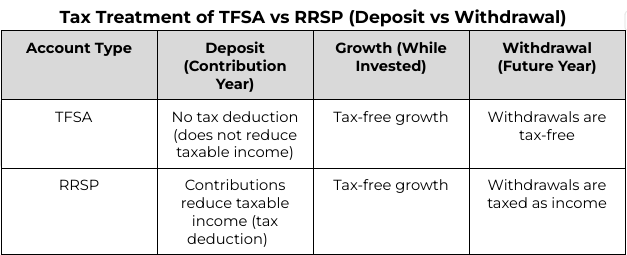

Both accounts enable your money to grow tax-free while in the account. The main difference occurs in the year of deposit, and the year of withdrawal.

The RRSP is often referred to as a tax-deferred account. When you contribute to your RRSP you will receive a tax break on your contributions, which lowers your taxable income in that year.

However, when you go to withdraw the money from your RRSP you will be taxed on the money you withdraw at your marginal tax rate. This includes

Any money initially contributed to the account,

and any earned income acquired via growth of their investments that is withdrawn. This is often a point of frustration for retirees who did not fully understand the details of the RRSP when they decided to use the account.

Lets use an example to illustrate the differences.

Year of Deposit

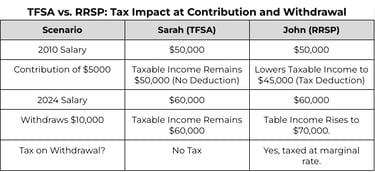

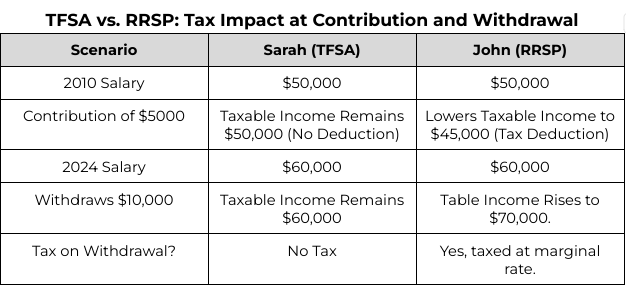

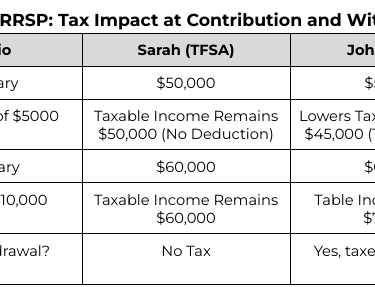

Let's say two people Sarah & John each earned $50,000 in the year 2010. Sarah contributed $5,000 to her TFSA. Meanwhile, John contributed $5,000 to his RRSP. Sarah’s taxable income for that year remained at $50,000 as she doesn't receive any immediate tax deductions for her TFSA contribution. John, on the other hand, would have reduced his taxable income to $45,000.

Year of Withdrawal

Let's assume John has a pre-tax income of $60,000 in 2024. He decides to withdraw $10,000 from his RRSP. This will increase his taxable income to $70,000 because the RRSP is taxed at the time of withdrawal. Meanwhile Sarah, who just so happens to have the same income of $60,000, decided to withdraw $10,000 from her TFSA. Her taxable income remains at $60,000 because the TFSA is not taxed at the time of withdrawal.

4. Failure to Factor in Previous Growth in Re-Contribution Amounts

It is important to understand that the amount you can re-contribute to a TFSA is influenced by three primary factors:

Total Contribution Room Accumulated

Additional Annual Contribution

Previous Withdrawal Amount

The last factor is very important to consider because your total contribution limit based on age may actually be less than you are entitled to re-contribute. This is the case in situations where you had investments within a TFSA that grew, and then you withdrew the money. In this case you would just need to wait until the next calendar year to re-contribute all of the money that was withdrawn.

Example: Becky started contributing to her TFSA at inception. By July 2023, she had reached the maximum contribution limit of $88,000. However, her wise investment decisions resulted in the account growing to $150,000. She decided to withdraw the entire $150,000 for a home purchase. In 2024, she received an inheritance from her Aunt Judy of $250,000. Becky is now able to re-contribute all of the $150,000 that she withdrew in 2023 plus the 2024 annual limit of $7000 for a total of $157,000 to her TFSA.

The breakdown of her re-contribution amount includes:

Total Contribution Room Accumulated as of 2023 ($88,000)

The total amount of contribution room provided by the government from the inception of the TFSA until 2023.

Additional Contribution Room in 2024 ($7,000):

The additional room provided by the government for that specific year.

Investment Growth Prior to Withdrawal ($62,000):

The profit generated by her investments before making the withdrawal.

5. Re-contribution Timelines

Another common mistake people make with the TFSA is failing to monitor their re-contribution timelines. This often results in a scenario where they accidentally over contribute to their TFSA, and receive a penalty. This is generally only a concern for those individuals who have already hit their contribution limit, or are near their contribution limit. However, it can also be a concern for individuals who have made a large purchase (ie. house, car), or have received a windfall.

It is important to note that if you withdraw from your TFSA you lose that contribution room for the remainder of the calendar year.

However, in the following year you will regain the lost contribution room, and receive any additional annual contribution room provided by the government for that year.

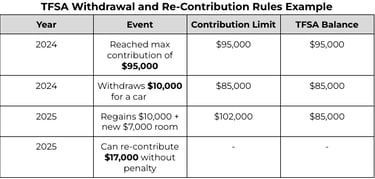

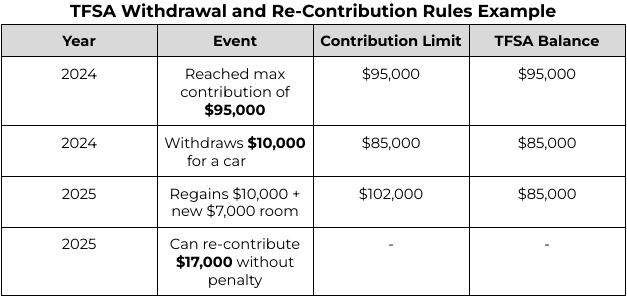

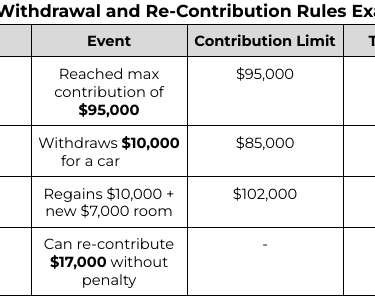

Example: Let’s say that I reached my contribution limit of $95,000 in 2024 but my car breaks down. I decide to withdraw $10,000 from my TFSA as a down payment for a new car. In this case, my contribution limit will fall to $85,000 for the remainder of 2024. I have to wait until 2025 to recoup the $10,000 of contribution room I used to pay for my car. I will also receive $7000 of additional contribution room for the year 2025. So as soon as the new year rolls around I can contribute up to $17,000 to my account without penalty.

It is important to monitor these numbers yourself as the CRA website often takes a very long time to update your contribution limits.

6. High Frequency Trading in a TFSA (Triggering CRA Audits)

The final mistake on our list is one that many Canadians are unaware about, which is high frequency trading of securities. It is important to note that registered accounts such as the TFSA and RRSP are not intended for activities that involve a high volume of selling, and buying securities. Examples of this could be day trading, and options trading. However, it could also include just the act of buying stocks, and selling them on short time frames, not necessarily day trading.

Unfortunately, like many other tax rules the criteria is very ambiguous and vague. Ultimately, the CRA could view frequent trading as business related activity. In which case you will have to file as a business, and all profits will be taxed as income.

Since the TFSA is intended to be a tax sheltered account, being taxed on your income would defeat the purpose. That is why the focus should be primarily on holding long term assets in these accounts, and making sure you minimize trading activity.

Conclusion

Although the TFSA is a great registered account, there are some common mistakes you need to watch out for to really maximize the use of the account. Understanding these mistakes will give you great confidence that you are using the account correctly and will significantly lower the risk of getting into trouble with the CRA.

Related Posts

Disclaimer: The information discussed in this podcast is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Williams, D. (2024, March 25). Mistakes are the portals of discovery. Veterinary Practice. https://www.veterinary-practice.com/article/mistakes-are-the-portals-of-discovery

Harapyn, L. (2023, February 11). Half of TFSA holders are doing it wrong. Financial Post. https://financialpost.com/personal-finance/half-of-tfsa-holders-are-doing-it-wrong

Government of Canada. Tax-Free Savings Account (TFSA), guide for individuals. Government of Canada. Retrieved February 5, 2025, from https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4466/tax-free-savings-account-tfsa-guide-individuals.html

Introduction

A quote by James Joyce that we really like is “ mistakes are the portals of discovery” [1]. If you read our previous blog post here, you would know that we highly rate the TFSA. Now we’re sure you’re excited to throw everything but the kitchen sink at it.

However, before you do that, we want to highlight the six most common mistakes we have noticed most people make when it comes to the TFSA. We’re happy enough to teach you the common areas to avoid, so you can skip the “discovery” phase and start off on the right foot (at least in regards to investing).

Let's get started with the first huge mistake that the financial post says that half of Canadians make [2]:

1. Viewing the TFSA as a Savings Account and NOT an Investment Account

One of the most common mistakes people make is viewing the TFSA as a traditional savings account. It is understandable though because the TFSA suffers from what we call “accidental false advertising” due to the poor naming of the account. A more appropriate name would be something like a Tax Free Investment Account. While TFSAs do allow you to save money, their true potential is in their ability to serve as investment vehicles.

The primary benefit of a TFSA is tax-free growth.

Example: If you invest $10,000 today and it grows to $20,000 in 20 years, you are not taxed on the $10,000 of gain made over this time period.

Many people commonly deposit their money into a traditional tax free savings account at their institution of choice. These accounts generally provide low-interest returns. However, within a TFSA you have the opportunity to invest in a wide range of assets, including:

Stocks & Bonds

Mutual funds, Index Funds, Exchange Traded Funds (ETF’s)

Guaranteed Investment Certificates (GIC’s)

Money Market Funds

Etc.

Each of these investments has the potential to generate substantial returns over time, all of which remain tax-free within the account.

In summary, TFSA's are not limited to low-yield savings options; they are a versatile investment tools that can help you achieve your long-term financial goals. By thinking of your TFSA as an investment account, you can take advantage of the power of compounding and potentially build substantial wealth over the course of your life.

2. Conflating Contribution Limit with Maximum Holdings

There is an annual contribution limit which varies from year to year. Your total contribution limit depends on how old you are, and whether or not you have previously contributed. However, it's important to understand that this limit doesn't represent the maximum amount you can hold in your TFSA. In fact, your TFSA can grow substantially beyond the contribution limits.

Example: Consider Becky, who turned 18 in 2009 and was eligible to open a TFSA. Suppose her contribution room for the years 2009 to 2024 amounted to a total of $95,000 based on the varying annual limits.

In 2009, Becky deposited the maximum allowable amount, which was $5,000. Over the next 13 years, she continued to contribute the maximum annual amount. During this time, she made a consistent 7% annual return on her investments within the TFSA by investing in a low cost index fund.

By 2024, her cumulative contributions would have reached $95,000, which is her contribution limit. However, the magic of tax-free growth allowed her investments to grow significantly. Her TFSA was actually worth $175,000, far exceeding her contribution limit.

The two key take-away’s are:

The contribution limit represents the maximum amount you can contribute (deposit) to your TFSA in any given year.

The total value of your TFSA can surpass that limit as your investments grow over time.

3. Not Understanding the Tax Benefits of the Account

Another common mistake is that people often group the TFSA and RRSP into the same category of accounts. We will discuss the RRSP in further detail in our next post, but for today’s sake here are the main differences:

Both accounts enable your money to grow tax-free while in the account. The main difference occurs in the year of deposit, and the year of withdrawal.

The RRSP is often referred to as a tax-deferred account. When you contribute to your RRSP you will receive a tax break on your contributions, which lowers your taxable income in that year.

However, when you go to withdraw the money from your RRSP you will be taxed on the money you withdraw at your marginal tax rate. This includes

Any money initially contributed to the account,

and any earned income acquired via growth of their investments that is withdrawn. This is often a point of frustration for retirees who did not fully understand the details of the RRSP when they decided to use the account.

Lets use an example to illustrate the differences.

Year of Deposit

Let's say two people Sarah & John each earned $50,000 in the year 2010. Sarah contributed $5,000 to her TFSA. Meanwhile, John contributed $5,000 to his RRSP. Sarah’s taxable income for that year remained at $50,000 as she doesn't receive any immediate tax deductions for her TFSA contribution. John, on the other hand, would have reduced his taxable income to $45,000.

Year of Withdrawal

Let's assume John has a pre-tax income of $60,000 in 2024. He decides to withdraw $10,000 from his RRSP. This will increase his taxable income to $70,000 because the RRSP is taxed at the time of withdrawal. Meanwhile Sarah, who just so happens to have the same income of $60,000, decided to withdraw $10,000 from her TFSA. Her taxable income remains at $60,000 because the TFSA is not taxed at the time of withdrawal.

4. Failure to Factor in Previous Growth in Re-Contribution Amounts

It is important to understand that the amount you can re-contribute to a TFSA is influenced by three primary factors:

Total Contribution Room Accumulated

Additional Annual Contribution

Previous Withdrawal Amount

The last factor is very important to consider because your total contribution limit based on age may actually be less than you are entitled to re-contribute. This is the case in situations where you had investments within a TFSA that grew, and then you withdrew the money. In this case you would just need to wait until the next calendar year to re-contribute all of the money that was withdrawn.

Example: Becky started contributing to her TFSA at inception. By July 2023, she had reached the maximum contribution limit of $88,000. However, her wise investment decisions resulted in the account growing to $150,000. She decided to withdraw the entire $150,000 for a home purchase. In 2024, she received an inheritance from her Aunt Judy of $250,000. Becky is now able to re-contribute all of the $150,000 that she withdrew in 2023 plus the 2024 annual limit of $7000 for a total of $157,000 to her TFSA.

The breakdown of her re-contribution amount includes:

Total Contribution Room Accumulated as of 2023 ($88,000)

The total amount of contribution room provided by the government from the inception of the TFSA until 2023.

Additional Contribution Room in 2024 ($7,000):

The additional room provided by the government for that specific year.

Investment Growth Prior to Withdrawal ($62,000):

The profit generated by her investments before making the withdrawal.

5. Re-contribution Timelines

Another common mistake people make with the TFSA is failing to monitor their re-contribution timelines. This often results in a scenario where they accidentally over contribute to their TFSA, and receive a penalty. This is generally only a concern for those individuals who have already hit their contribution limit, or are near their contribution limit. However, it can also be a concern for individuals who have made a large purchase (ie. house, car), or have received a windfall.

It is important to note that if you withdraw from your TFSA you lose that contribution room for the remainder of the calendar year.

However, in the following year you will regain the lost contribution room, and receive any additional annual contribution room provided by the government for that year.

Example: Let’s say that I reached my contribution limit of $95,000 in 2024 but my car breaks down. I decide to withdraw $10,000 from my TFSA as a down payment for a new car. In this case, my contribution limit will fall to $85,000 for the remainder of 2024. I have to wait until 2025 to recoup the $10,000 of contribution room I used to pay for my car. I will also receive $7000 of additional contribution room for the year 2025. So as soon as the new year rolls around I can contribute up to $17,000 to my account without penalty.

It is important to monitor these numbers yourself as the CRA website often takes a very long time to update your contribution limits.

6. High Frequency Trading

The final mistake on our list is one that many Canadians are unaware about, which is high frequency trading of securities. It is important to note that registered accounts such as the TFSA and RRSP are not intended for activities that involve a high volume of selling, and buying securities. Examples of this could be day trading, and options trading. However, it could also include just the act of buying stocks, and selling them on short time frames, not necessarily day trading.

Unfortunately, like many other tax rules the criteria is very ambiguous and vague. Ultimately, the CRA could view frequent trading as business related activity. In which case you will have to file as a business, and all profits will be taxed as income.

Since the TFSA is intended to be a tax sheltered account, being taxed on your income would defeat the purpose. That is why the focus should be primarily on holding long term assets in these accounts, and making sure you minimize trading activity.

Conclusion

Although the TFSA is a great registered account, there are some common mistakes you need to watch out for to really maximize the use of the account. Understanding these mistakes will give you great confidence that you are using the account correctly and will significantly lower the risk of getting into trouble with the CRA.

Related Posts

Disclaimer: The information discussed in this podcast is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Williams, D. (2024, March 25). Mistakes are the portals of discovery. Veterinary Practice. https://www.veterinary-practice.com/article/mistakes-are-the-portals-of-discovery

Harapyn, L. (2023, February 11). Half of TFSA holders are doing it wrong. Financial Post. https://financialpost.com/personal-finance/half-of-tfsa-holders-are-doing-it-wrong

Government of Canada. Tax-Free Savings Account (TFSA), guide for individuals. Government of Canada. Retrieved February 5, 2025, from https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4466/tax-free-savings-account-tfsa-guide-individuals.html