Get our free Debt vs Invest Calculator — click here to access it

How Do Bonds Work? Beginner’s Guide to Bond Investing

What are bonds and how do they work? Learn how bonds make money, the different types of bonds, the benefits, and whether they are a safe investment for you.

BONDSINVESTING FOR BEGINNERS

2/15/202512 min read

Bonds are like insurance: you don't appreciate them until you need them."

— Bill Bernstein (Financial theorist and author of The Four Pillars of Investing)

What are Bonds?

If the stock market can be described as a violent wild never ending roller coaster, then the bond market could be described as a brisk drive, but on a cloudy day.

A bond is a loan contract that is made by an investor to a borrower. The simplest way to understand what that means is to think about when you borrow money from the bank to purchase a house, or a car. In this case the bank lends you money in exchange for your agreement to pay them back in full, plus interest, over a specified time period.

For example: Let’s imagine I would like to buy a car for $20,000 but I don’t have the cash to pay for the purchase. I go to my bank, and they will loan me the money at 5% interest for 48 months (ie. 4 years). I promise to pay them back the principle (ie. $20,000) plus the interest (ie. $1,000) in monthly installments. In this case I will pay the bank $437.50 for the next 48 months in order to repay my loan.

A bond is the exact same concept, but the roles are reversed. In the case of a bond you lend money to the government, or a corporation for an agreed upon term length. They promise to pay you back your principal (ie. the money you lent them) with interest at the end of the term. In other words, when you buy a bond you are loaning money to a corporation or the government.

Why are Bonds Issued?

Bonds are issued with the intention of raising money in order to fund a variety of business or governmental activities and obligations. For businesses these can include operations, expansions or acquisitions. For government it may be used to fund large projects. Ultimately, they need money, and are willing to pay you interest if you lend yours to them.

Elements of a Bond

There are two key elements to a bond that you need to be aware of:

Term Length- The duration until expiration of the loan contract. The principle is generally repaid at the time the loan contract expires.

Yield- The % return the lender (ie. you) will receive in exchange for purchasing the bonds. The percentage is generally expressed as an annual return rate, and paid out throughout the life of the bond term.

For example: The Ontario government decided that they wanted to rebuild a bridge in 2019 because the old one was starting to look like this...

However, they didn’t have the money for it at the time. So, on January 1st, 2020, they issued a bond to collect your money and guarantee you a 3% interest. They also promise to return your principle back to you on January 1st, 2025 (in 5 years). You, being a savvy bond investor that read this article, decide to purchase $1,000 of this 5 year bond yielding 3% annually. Since this time you received 5 payments:

January 1st (2021)- $30

January 1st (2022)- $30

January 1st (2023)- $30

January 1st (2024)- $30

January 1st (2025)- $1,030

At the end of each year between January 1st 2020 - 2025 (ie. years 1-5), you received $30 of interest only payments for a total of $150. On January 1st 2025, you receive both your yearly interest payment of $30, and a return of your principle payment of $1,000. In this case, you turned $1,000, into $1,150 over a 5 year period by investing in this Ontario Bond.

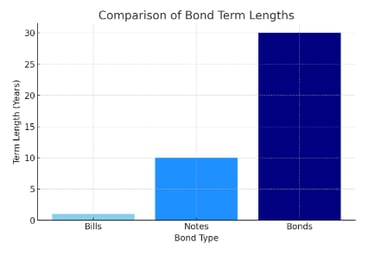

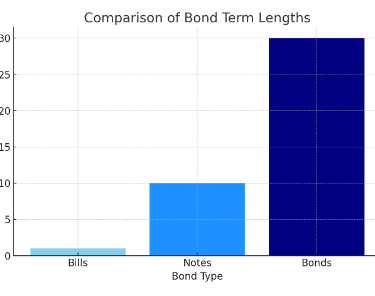

Bonds vs Bills vs Notes

As you start learning about the bond market, you will likely start hearing the terms bonds, bills, and notes. These terms are commonly used in the financial world, however, they all refer to bonds of varying lengths. They are used to distinguish between short, medium, and long term bonds.

Bills- Short Term Length

Notes- Medium Length

Bonds - Long Term Length

There are some distinguishing features between them. One would be that with short term bonds (ie. bills) the interest is generally paid out at the end of the term length, and not throughout the holding period. However, for simplification for this blog we will refer to all of these as bonds.

What Are the Different Types of Bonds?

There are several different types of bonds, however, the most common are:

Government Bonds (ie. US Treasury Bonds, or Government of Canada Bonds)

Used to fund government projects or to reduce the debt of the government.

Corporate Bonds

Used to fund companies operations.

Provincial Bonds

Used to fund government projects or to reduce the debt of the government.

Municipal Bonds

Used to fund projects such as roads, schools, hospitals, etc.

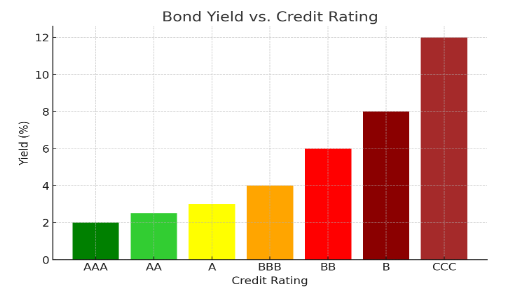

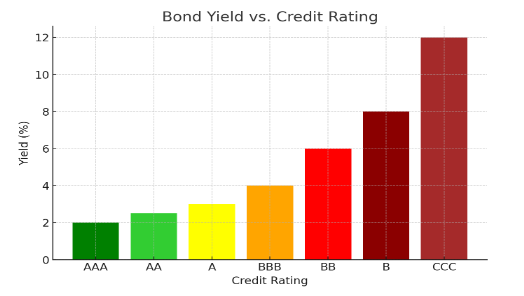

Credit Rating vs Yield

An important feature to note when purchasing bonds is that the yield is highly influenced by the credit rating of the bond. Credit rating is essentially just a measurement of the corporation, or government entity's risk of defaulting on their obligation to pay bond holders. It is very similar to our credit score. An individual with a low credit score would have to pay higher interest to a bank for a loan, than an individual with a good credit score.

For example: Using the $20,000 vehicle purchase discussed above. If you have a good credit score the bank will be more enticed to provide you with the loan at the best available interest rate, let's say 3%. Meanwhile, if I go to the bank with a poor credit score, they may provide me with the same loan at 7%. I am considered a higher risk of not paying them back, so they ask for a higher interest rate.

Similarly, a corporation or government with a low credit rating generally will have to pay a higher yield on their bonds in order to entice investors to buy. Government bonds (ie. US Treasury Bonds, or Government of Canada Bonds) have the highest credit rating, and are considered the safest of all bonds for this reason. Provincial and municipal bonds often provide a higher yield because they have a lower credit rating than federal government bonds.

Corporate bonds on the other hand are commonly divided into two main categories:

Investment Grade Bonds- Credit rating of BBB or higher (ie. AAA is considered the highest grade or most secure bonds)

High-yield Bonds- Credit rating of BBB or lower. Often referred to as junk bonds for this reason.

Figure 1: Bar graph showing the relationship between a bond credit rating, and the yield. Note these are not current rates, and are only used to illustrate the point.

This is important to note because although the highest yielding bonds may look appealing…it is generally a sign there is an increased risk of you losing your money.

What Are The Benefits to Holding Bonds?

The two main benefits of holding bonds are:

Low Risk/Safe

Provided that you hold the bond until the end of the term length you will receive your principle, and agreed upon interest.

This differs from stocks whereby the price is highly variable, and there is no guaranteed return of your principle investment.

Fixed Income

If you are retired, or rely on your investments for income the regular payment of interest is viewed as beneficial.

Stocks that provide dividends, or GICs are another option which we will discuss in upcoming blogs.

Conclusion

Bonds remain a foundational element of any diversified investment portfolio, offering stability and predictable income streams. Whether you’re a conservative investor seeking safety or someone looking to balance risk, understanding the different types of bonds and their role in your financial strategy is crucial.

Bonds may not be as fun and exciting as stocks (or deliver similar high returns). However, their reliability and relatively lower volatility make them a valuable tool in managing risk and achieving long-term financial goals. Make sure to stay informed about market conditions and interest rate trends to help ensure your bond investments continue to meet your needs.

Related Posts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

NerdWallet. (n.d.). What is a bond? NerdWallet Canada. Retrieved February 7, 2025, from https://www.nerdwallet.com/ca/investing/what-is-a-bond

Collins, J. L. (2016). The simple path to wealth: Your road map to financial independence and a rich, free life. CreateSpace Independent Publishing Platform.

Questrade. (n.d.). All you need to know about bonds. Questrade. Retrieved February 7, 2025, fromhttps://www.questrade.com/learning/investment-concepts/fixed-income-investments/all-you-need-to-know-about-bonds

OpenAI. (2025). Graph comparing bond term lengths [AI-generated graph]. ChatGPT. https://chat.openai.com/

OpenAI. (2025). Graph comparing bond yeild vs credit rating [AI-generated graph]. ChatGPT. https://chat.openai.com/

Bonds are like insurance: you don't appreciate them until you need them."

— Bill Bernstein (Financial theorist and author of The Four Pillars of Investing)

What are Bonds?

If the stock market can be described as a violent wild never ending roller coaster, then the bond market could be described as a brisk drive, but on a cloudy day.

A bond is a loan contract that is made by an investor to a borrower. The simplest way to understand what that means is to think about when you borrow money from the bank to purchase a house, or a car. In this case the bank lends you money in exchange for your agreement to pay them back in full, plus interest, over a specified time period.

For example: Let’s imagine I would like to buy a car for $20,000 but I don’t have the cash to pay for the purchase. I go to my bank, and they will loan me the money at 5% interest for 48 months (ie. 4 years). I promise to pay them back the principle (ie. $20,000) plus the interest (ie. $1,000) in monthly installments. In this case I will pay the bank $437.50 for the next 48 months in order to repay my loan.

A bond is the exact same concept, but the roles are reversed. In the case of a bond you lend money to the government, or a corporation for an agreed upon term length. They promise to pay you back your principal (ie. the money you lent them) with interest at the end of the term. In other words, when you buy a bond you are loaning money to a corporation or the government.

Why are Bonds Issued?

Bonds are issued with the intention of raising money in order to fund a variety of business or governmental activities and obligations. For businesses these can include operations, expansions or acquisitions. For government it may be used to fund large projects. Ultimately, they need money, and are willing to pay you interest if you lend yours to them.

Elements of a Bond

There are two key elements to a bond that you need to be aware of:

Term Length- The duration until expiration of the loan contract. The principle is generally repaid at the time the loan contract expires.

Yield- The % return the lender (ie. you) will receive in exchange for purchasing the bonds. The percentage is generally expressed as an annual return rate, and paid out throughout the life of the bond term.

For example: The Ontario government decided that they wanted to rebuild a bridge in 2019 because the old one was starting to look like this...

However, they didn’t have the money for it at the time. So, on January 1st, 2020, they issued a bond to collect your money and guarantee you a 3% interest. They also promise to return your principal back to you on January 1st, 2025 (in 5 years). You, being a savvy bond investor that read this article, decide to purchase $1,000 of this 5 year bond yielding 3% annually. Since this time you received 5 payments:

January 1st (2021)- $30

January 1st (2022)- $30

January 1st (2023)- $30

January 1st (2024)- $30

January 1st (2025)- $1,030

At the end of each year between January 1st 2020 - 2025 (ie. years 1-5), you received $30 of interest only payments for a total of $150. On January 1st 2025, you receive both your yearly interest payment of $30, and a return of your principle payment of $1,000. In this case, you turned $1,000, into $1,150 over a 5 year period by investing in this Ontario Bond.

Bonds vs Bills vs Notes

As you start learning about the bond market, you will likely start hearing the terms bonds, bills, and notes. These terms are commonly used in the financial world, however, they all refer to bonds of varying lengths. They are used to distinguish between short, medium, and long term bonds.

Bills- Short Term Length

Notes- Medium Length

Bonds - Long Term Length

There are some distinguishing features between them. One would be that with short term bonds (ie. bills) the interest is generally paid out at the end of the term length, and not throughout the holding period. However, for simplification for this blog we will refer to all of these as bonds.

What Are the Different Types of Bonds?

There are several different types of bonds, however, the most common are:

Government Bonds (ie. US Treasury Bonds, or Government of Canada Bonds)

Used to fund government projects or to reduce the debt of the government.

Corporate Bonds

Used to fund companies operations.

Provincial Bonds

Used to fund government projects or to reduce the debt of the government.

Municipal Bonds

Used to fund projects such as roads, schools, hospitals, etc.

Credit Rating vs Yield

An important feature to note when purchasing bonds is that the yield is highly influenced by the credit rating of the bond. Credit rating is essentially just a measurement of the corporation, or government entity's risk of defaulting on their obligation to pay bond holders. It is very similar to our credit score. An individual with a low credit score would have to pay higher interest to a bank for a loan, than an individual with a good credit score.

For example: Using the $20,000 vehicle purchase discussed above. If you have a good credit score the bank will be more enticed to provide you with the loan at the best available interest rate, lets say 3%. Meanwhile, if I go to the bank with a poor credit score, they may provide me with the same loan at 7%. I am considered a higher risk of not paying them back, so they must ask for a higher interest rate.

Similarly, a corporation or government with a low credit rating generally will have to pay a higher yield on their bonds in order to entice investors to buy. Government bonds (ie. US Treasury Bonds, or Government of Canada Bonds) have the highest credit rating, and are considered the safest of all bonds for this reason. Provincial and municipal bonds often provide a higher yield because they have a lower credit rating than federal government bonds.

Corporate bonds on the other hand are commonly divided into two main categories:

Investment Grade Bonds- Credit rating of BBB or higher (ie. AAA is considered the highest grade or most secure bonds)

High-yield Bonds- Credit rating of BBB or lower. Often referred to as junk bonds for this reason.

Figure 1: Bar graph showing the relationship between a bond credit rating, and the yield. Note these are not current rates, and are only used to illustrate the point.

This is important to note because although the highest yielding bonds may look appealing…it is generally a sign there is an increased risk of you losing your money.

What Are The Benefits to Holding Bonds?

The two main benefits of holding bonds are:

Low Risk/Safe

Provided that you hold the bond until the end of the term length you will receive your principle, and agreed upon interest.

This differs from stocks whereby the price is highly variable, and there is no guaranteed return of your principle investment.

Fixed Income

If you are retired, or rely on your investments for income the regular payment of interest is viewed as beneficial.

Stocks that provide dividends, or GICs are another option which we will discuss in upcoming blogs.

Conclusion

Bonds remain a foundational element of any diversified investment portfolio, offering stability and predictable income streams. Whether you’re a conservative investor seeking safety or someone looking to balance risk, understanding the different types of bonds and their role in your financial strategy is crucial.

Bonds may not be as fun and exciting as stocks (or deliver similar high returns). However, their reliability and relatively lower volatility make them a valuable tool in managing risk and achieving long-term financial goals. Make sure to stay informed about market conditions and interest rate trends to help ensure your bond investments continue to meet your needs.

Related Posts

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

NerdWallet. (n.d.). What is a bond? NerdWallet Canada. Retrieved February 7, 2025, from https://www.nerdwallet.com/ca/investing/what-is-a-bond

Collins, J. L. (2016). The simple path to wealth: Your road map to financial independence and a rich, free life. CreateSpace Independent Publishing Platform.

Questrade. (n.d.). All you need to know about bonds. Questrade. Retrieved February 7, 2025, fromhttps://www.questrade.com/learning/investment-concepts/fixed-income-investments/all-you-need-to-know-about-bonds

OpenAI. (2025). Graph comparing bond term lengths [AI-generated graph]. ChatGPT. https://chat.openai.com/

OpenAI. (2025). Graph comparing bond yeild vs credit rating [AI-generated graph]. ChatGPT. https://chat.openai.com/