Get our free Debt vs Invest Calculator — click here to access it

Lump Sum vs. Dollar-Cost Averaging: Top Strategy for 2025

Find out if lump sum investing or dollar-cost averaging is the better 2025 strategy. We explore data and insights to help guide your investing decision.

INVESTING FOR BEGINNERSINVESTING

5/31/202533 min read

Introduction

Investing can feel like navigating a financial maze, but choosing the right strategy can make all the difference! Whether you're a seasoned investor or just starting out, understanding the nuanced battle between lump sum investing and dollar cost averaging could be your key to financial success. In this comprehensive guide, we'll break down these two powerful investment strategies, helping you make informed decisions that align with your financial goals.

Understanding Lump Sum Investing

What is Lump Sum Investing?

Lump sum investing is the process by which you invest a large amount of money all at once instead of progressively over time. This one-time investment could be made into any of a variety of different financial instruments including mutual funds, ETF’s, stocks, or bonds. The decision of when that lump sum investment is made could be strategic. This is when you wait for a “market event”, such as the draw down that occurred in April following President Trump’s Liberation day. Or it could simply be made immediately after it is received.

For example: You received a $10,000 inheritance from your frugal, but sweet grandma Judy. You decide to invest all of those funds into a low cost index ETF such as VOO or VEQT as soon as they are deposited into your account.

There are several life circumstances that may result in you receiving an above normal sum of money such as:

Inheritance

Insurance settlement

Pay bonus

Following the sale of an asset such as stocks, or real estate.

Winning a lottery

A previously saved, but not invested nest egg

Uneven pay schedule (ie. Self employed, or independent contractors)

All of these scenarios may provide you with the opportunity to use a lump sum strategy. Or you could just squander it on degeneracy… but we don’t suggest that.

Benefits of Lump Sum Strategy

There are a few potential benefits to utilizing a lump sum strategy.

Better Returns

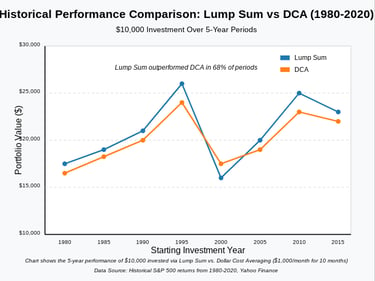

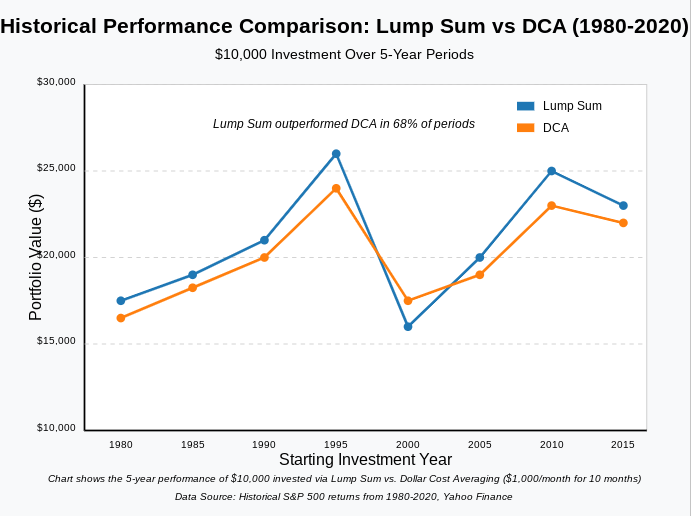

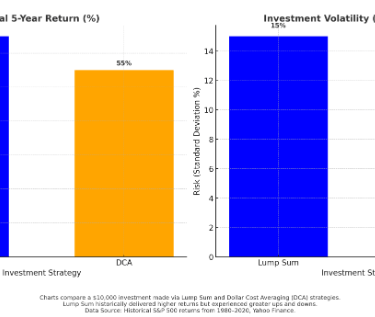

The first of which is that there is a higher statistical likelihood of better returns. A study conducted by Vanguard showed that from 1976 to 2022, if someone had invested in the MSCI World Index using a lump sum strategy, they would have beat a dollar cost averaging strategy 68% of the time.

Logically, this makes a lot of sense. Over your lifetime, the stock market will likely continue to expand and grow (ie. go upwards). Add to this that bull markets generally last longer than bear markets. So in any given year you are more likely to experience positive returns, than negative.

Ex. Imagine in July 2023, Jake and Mark two brothers get an inheritance of $120,000 each from their Grandma Judy.

Jake invests $120,000 in the S&P 500 immediately (Lump Sum Strategy)

Mark invests $12,000 per month in the S&P 500 for the next 10 months (DCA Strategy)

As of March 2025

Jake will have $154, 913 using a lump sum strategy

Mark will have $149,740 using a DCA strategy

In this example, we specifically selected two random months in the stock market avoiding any “market events” which could skew the numbers in favour of any strategy.

Take Advantage of Market Downturns

Another benefit of a lump sum strategy is that it enables you to take advantage of market downturns. When a market correction or crash occurs, the ability to deploy cash towards an investment provides you with a significant advantage. It enables you to buy stocks or even indices when they are potentially mispriced and selling at below their intrinsic value. This strategy has helped many successful investors such as Warren Buffet throughout his investing career.

Ex. Imagine Jake and Mark got their inheritance from their Grandma Judy in March 2009.

Jake invests $120,000 in the S&P 500 immediately (Lump Sum Strategy)

Mark invests $12,000 per month in the S&P 500 for the next 10 months (DCA Strategy)

As of March 2025

Jake will have $1,321,681 using a lump sum strategy

Mark will have $945,733 using a DCA strategy

As you can see, the lump-sum strategy produced almost a $400K better return than DCA. Now to be fair, this example was cherry picked because this was the BEST SITUATION for the lump sum strategy. The stock market had crashed in 2008, and March 2009 was the beginning of a huge recovery period. This example was just to show how advantageous this strategy can be during such “market events”.

Removes Psychological Strain

In 2014, during a public Q&A session, the CEO of Meta Mark Zuckerberg stated that he wears the same gray t-shirt every day in order to reduce decision fatigue. By reducing the mental energy he spends on trivial decisions such as clothing choice, it enables him to focus that energy towards solving larger, more important decisions in his life and business.

In much the same way, the act of lump sum investing can reduce the mental burden for many people. Although we enjoy investing, and the thought of tactically planning our decisions to do so is enticing, it may not be for you. Instead, maybe you would rather focus your energy towards your business, hobbies, and family life. In this case, investing your inheritance, or bonus check immediately can be mentally freeing in a way.

Potential Drawbacks of Lump Sum Investing

Although Lump Sum Investing has been shown to be the most effective strategy on average, there are some potential downsides to putting your money to work all at once.

Market Timing Risk

The S&P 500 index is used to track the top 500 companies by market capitalization listed on the New York Stock Exchange. It has existed since 1957. Since this time there has been 10 major market crashes (ie. 20% or > decrease), and 27 market corrections (10% or > decrease). Using a lump sum strategy could result in you purchasing your stocks right before a similar event. The result of which would be a short to medium term decrease in the value of your investments.

Ex. Imagine you invested a $20,000 inheritance from your Uncle Tom on February 19th, 2020 prior to the COVID Crash. During this time period, the market saw a 34% decrease. By March 20th, your investment would have decreased to $13,200.

Although this is a cherry picked example, it demonstrates the extreme swings you may experience in your portfolio if the lump sum investment is made at an inopportune time.

Loss Aversion is a cognitive bias that we all experience which says that we are more emotionally impacted by a loss, then an equivalent gain. In other words, a 20% decrease in your stock portfolio feels horrible. Meanwhile, a 20% gain feels just ok. Due to this inherent bias, the emotional impact of investing right before a “market event” could be traumatic.

However, it is important to remember that as long as you don’t sell your shares, you have not lost money. In the case of 2020, by August 17th the S&P 500 returned to all time highs, and you would have recouped your losses. Although not all recoveries will happen this quickly, history shows us the market always returns to all time highs eventually.

Psychological Strain

Another downside to lump sum investing is the psychological strain you must endure to “pull the trigger”. Investing a large amount of money all at once will inevitably give you anxiety. You will ask yourself questions like “Is this the right time?” or “what if the market goes down after I buy?”.

If you find yourself asking these questions, maybe using a DCA strategy or some hybrid of the two would be better for you.

Opportunity Cost

Have you ever bought something like a pair of shoes, only to find a better option shortly afterwards. If you are lucky, you can go back and return the original item in order to buy the better option. Or maybe you already used it and have to live with buyer’s remorse.

This same feeling can occur when using a lump sum strategy. After the funds are invested. you may find a better stock, or ETF. Or maybe your car breaks down and you realize you need the money to purchase a new one. A number of different and potentially better options may come up. Although you can always sell to switch strategies that may come with its own potential barriers, such as fees, losses, account restrictions, etc.

DCA provides you with the flexibility to take advantage of new opportunities as they arise, and not be anchored to a past decision.

Demystifying Dollar Cost Averaging (DCA)

Dollar Cost Averaging (DCA) is the process of purchasing investments gradually over time on a regular interval. Using a DCA Strategy, you will purchase regardless of the stock price. It is important to make the distinction between two different, but often confused, types of DCA: Traditional and Cash Flow. This distinction was highlighted to us in the amazing investing book “Just Keep Buying” by Nick Maggiuli.

Traditional DCA is what most people will do throughout their lifespan. They will invest a fixed amount of money on a recurring schedule. The timing of those investments is usually coordinated with when they receive their paycheck.

Ex. You receive a $3,000 bi-weekly check from your employer, and you invest 25% or $750 into a low cost index ETF such as VOO or VFV.

Cash Flow DCA, on the other hand, is the process by which you gradually invest a larger sum of money. However, instead of investing the money all at once, as you would using the lump sum strategy, you split it up and invest it bit by bit for a defined time period.

Ex. You receive a $10,000 inheritance from your cousin Sherri, and decide to gradually invest it over the next 12 months. Each month you will invest $833.33.

When the comparison is made between DCA and Lump Sum investing we are generally referring to Cash Flow DCA. In other words you have a large amount of money and would like to know which strategy is better to invest it all at once, or to gradually invest it.

Benefits of DCA

Reduces the Downside Risk

One of the characteristics of stocks is that the price fluctuates on a daily basis. The changes in price may, or may not be associated with the underlying value of the business. The same can be said for other assets such as ETFs, Bonds, REITs, etc. The unfortunate downside of a lump sum strategy is the risk that you may purchase at the “top” of the market cycle (aka when prices are the most expensive). The rationale behind using a DCA strategy is to manage this price risk by purchasing at a variety of different points in time.

For example: Lets imagine you have $500 to invest in a low cost index ETF that currently trades at $50/share. However, after you buy, the price gradually decreases to $42/share (going down by $2 a month) over the next 5 months.

Using a Lump Sum Strategy, your $500 investment would have purchased 10 shares at $50 each. By month 5, the investment would have decreased to $420.

Using a DCA strategy though:

Month 1: $100 buys 2 shares at $50/share

Month 2: $100 buys 2.08 shares at $48/share

Month 3: $100 buys 2.17 shares at $46/share

Month 4: $100 buys 2.27 shares at $44/share

Month 5: $100 buys 2.38 shares at $42/share

Using the DCA strategy you would have purchased a total of 10.9 shares at an average buy price of ~$45.83/share. The value of the investments by month 5 would be $457.80 (ie. number of shares x current market price).

Although statistically DCA is not the most effective strategy on average, it reduces the potential risk of these outlier events. Using the Vanguard study, described above there are still 32% of circumstances whereby a DCA strategy outperforms lump sum. During these situations, a gradual investment of the money allows you to take advantage of a market downturn by buying at progressively lower price points.

Removes Emotions

Imagine you receive a large sum of money all at once from an inheritance, lottery, etc. On one end, your brain tells you that the smartest strategy based on research is to invest that money today. But you are worried, and you ask yourself questions like “what if my investments go down after I buy?” or “I don’t want to lose my money”.

There is a quote by Morgan Housel from the book “Psychology of Money” that explains this dilemma very clearly:

“Finance is overwhelmingly taught as a math-based field, where you put data into a formula and the formula tells you what to do, and it’s assumed that you’ll just go do it. ... It’s not that any of these things are bad or wrong. It’s that knowing what to do tells you nothing about what happens in your head when you try to do it.”

The truth is that there is a large psychological barrier for many people when they have to invest a lot of money, all at once. DCA may not resolve this issue, but it eases the burden by allowing you to start. It provides you with the optionality to switch strategies or stop if you don’t feel comfortable investing all of the funds. Ultimately, it allows you to ignore market timing risks and just start investing today.

It Is Realistic

Although there are certain circumstances where you may have enough money to make the choice between DCA and Lump Sum, it isn’t a common scenario. For most people, they will have to invest on a regular interval because well…that's when they get paid.

Potential Drawbacks of DCA

Cash Drag

The main drawback of a DCA strategy, as we stated earlier, is lower total returns on average. The reason for this underperformance is due to a term called “cash drag”. By holding money in “cash” you will generally have lower returns then another individual who is fully invested into the stock market. The reason why is because the market, despite some periods of volatility, increases over time. Since inception, the average return of the S&P 500 is 10.22%.

Other sources of fixed income such as GICs and bonds have produced significantly lower total returns. And as we described in our post “The Hidden Tax That Everyone Pays (and Most People Don’t Even Know About)”, holding cash is actually destroying the buying power of your money.

Using a Cash Flow DCA strategy, most of your money will be sitting in cash initially, and gradually deployed over time. It will act like a weighted vest, slowing down your growth, and dragging down your performance.

Transaction Costs

A major downside to DCA strategy is that you are required to make multiple deposits, transactions, and possibly currency conversions. Each of which may require you to pay fees or commissions to your brokerage firm. In some cases you may be required to pay as much as $10/ transaction for trades on stocks, and ETF’s.

Let’s imagine two individuals Brian, and Susy are both 20 years of age. Both invest with a bank (ie. which will not be named) that charges a $10/transaction fee. Brian invests $200/month into a low cost index ETF such as VOO. Susy wants to minimize fees so she invests $2,400 on January 1st of each year into the same fund. By age 65:

Brian will have $676,146 (DCA Strategy)

Susy will have $780,942 (Lump Sum Strategy)

Much of these fees can be avoided though by just switching to a discount brokerage firm such as Questrade or Wealthsimple. Both of which charge a whopping… $0/transaction.

Lets use the previous example, but this time they both used a discount brokerage firm. By age 65:

Brian will have $715,733 (DCA Strategy)

Susy will have $784,210 (Lump Sum Strategy)

In other words, avoiding unnecessary transaction fees alone earned Brian an additional $39,587. Susy saved $3,268 by avoiding the one time transaction fee each year.

Procrastination

DCA is often used as an excuse to delay fully investing your money into the market. Instead you invest small amounts gradually over time minimizing your exposure. This is potentially due to a fear of losing your money.

If this is you then maybe you should consider a safer investment strategy, such as the 60/40 portfolio which is 60% stocks, and 40% bonds (ie. alternatively GIC’s). Although historically, 100% stocks have been shown to be the most effective strategy for long term gains, it may not fit with your psychology.

Knowing you are using a safer strategy may allow you to avoid delaying, and just invest all of your funds today.

Practical Implementation Strategies

For those of you who skipped to this part in the article, the short answer is that Lump Sum is better. Obviously, there is nuance to that answer though and that is why this article is not one sentence long. Hopefully, at this point, you have weighed the pros and cons, and determined which strategy you would like to implement. The next reasonable question though is how do I do it?

Lump Sum Implementation

Although there are a few steps involved in Lump Sum investing if you are a beginner, it is actually pretty straight forward:

Open one or more investment accounts with a brokerage firm. This could be a TFSA, RRSP, FHSA, or Taxable Account.

Be careful to check your eligibility and contribution limits to avoid incurring any penalties. For more info on the rules of these accounts, you can review our posts on the subjects.

We like Questrade and Wealthsimple because they are discount brokerage firms. However, you can choose whatever firm you like.

Once the account is open there will be a clickable option to add money, or move money.

You can set up a pre-authorized debit, visa debit, interac e-transfer or simply add the account as a payee on your primary bank account.

Once this is set-up, you can go ahead and transfer the funds from your primary bank account to your investment account.

Depending on the method, it could take a few business days for the transfer to occur.

Once the funds arrive in the investment account, they are now ready to be invested. At this time, you can go to the search menu (🔍) and type in the ticker of the fund you would like to invest in.

The ETF’s we invest in are tickers VEQT, XEQT, & VOO. However, you can invest in whatever stock or ETF that fits your investing strategy.

Once you type in your ticker of choice, it should present a graph of the company's recent performance, and financial information such as the bid-ask spread, market cap, P/E ratio, etc.

There should also be two buttons which read Buy and Sell. Click on the buy button.

Now, this is where it becomes confusing for many, as there are two different options which are a limit buy/order or a market buy/order.

For simplicity let's choose market order, which just simply means you are buying the shares at their current price.

Type in the # of shares you would like to purchase.

It may also give you the option to just input the amount of money you would like to invest.

Provided that you didn’t type in a # larger than the amount of money in your account, it should provide you with a button to review your order.

Click on review order

After this you will be provided with the details of your order including the account type, the ETF/Stock you are purchasing, and the # of shares.

If the details match what you would like to purchase, then you can click the button saying “sent order”.

Once the order is complete you are now an investor… go ahead and add that in your bio on instagram.

DCA Implementation

Setting up a DCA strategy is slightly more challenging as you will have to make deposits every month. However, many brokerage firms provide you with the ability to automate both recurring deposits and buys. How this is set-up though can vary from one firm to the next. Regardless of which brokerage firm you use though, the steps should be similar:

Open one or more investment accounts with a brokerage firm. This could be a TFSA, RRSP, FHSA, or Taxable Account.

Be careful to check your eligibility and contribution limits to avoid incurring any penalties. For more info on the rules of these accounts you can review our posts on the subjects.

We like Questrade and Wealthsimple because they are discount brokerage firms. However, you can choose whatever firm you like.

Once the account is open there will be a clickable option to add money, or move money.

You will have to set up a pre-authorized debit and input your primary bank account information.

You should be provided with a page that allows you to select the following:

The account the money will be transferred too (ie brokerage account)

The account the money will be transferred from (ie. primary bank account)

The amount that will be transferred.

The frequency of those transfers/deposits (ie. weekly, biweekly, monthly)

The start date

The end date

Once this is complete, you can press ok and complete the PAD agreement.

It is important to note that although the transfer is set-up for a specific date, it may take a few business days to be ready to be invested.

Once the funds are deposited into the account you can:

Type in the ticker you would like to purchase by using the search menu (🔍).

Click the Buy button

Select Market Order/Buy

Type in the # of shares or $ amount you would like to invest.

Click Review Order

Click Send Order

Some brokerage firms such as Wealthsimple provide you with the option of setting up recurring investments. This is amazing, as it allows you to completely automate this process. Here is how you set it up.

Type in the ticker you would like to purchase by using the search menu (🔍).

Click the Buy button

Select Recurring

Type in the # of shares or $ amount you would like to invest.

Type in the start date, and frequency

Make sure it occurs after your deposit date.

Click Review Order

If prompted with the option to reinvest dividends you can check yes to further automate this process.

Click Send Order

Conclusion: Making the Right Investment Choice for Your Financial Journey

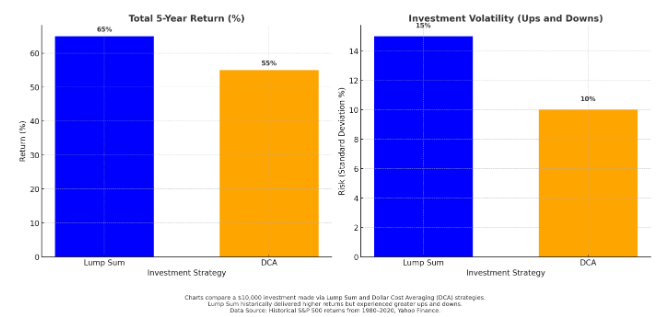

When deciding between lump sum investing and dollar cost averaging, there's no one-size-fits-all answer. The data clearly shows that lump sum investing has historically outperformed DCA approximately 68% of the time, making it statistically the better choice for maximizing returns. This advantage comes from keeping your money in the market longer and avoiding the "cash drag" that can hamper DCA strategies. It is important to note that although Lump Sum usually wins, it's a bumpier ride!

However, investing isn't purely a mathematical equation—it's deeply psychological. DCA offers significant emotional benefits by reducing the anxiety of market timing and providing protection against the pain of investing right before a downturn. For many investors, particularly beginners or those with lower risk tolerance, the peace of mind from DCA may outweigh the potential for slightly higher returns from lump sum investing.

Your personal circumstances also play a crucial role in this decision:

If you have a high risk tolerance, a long investment horizon, and are comfortable with potential short-term volatility, lump sum investing may be your optimal strategy.

If you're concerned about market timing, have a lower risk tolerance, or would experience significant stress from short-term market drops, DCA might be the better approach for you.

Consider a hybrid approach: invest a portion as a lump sum immediately (perhaps 50-70%) and then dollar cost average the remainder over a few months to balance statistical advantage with psychological comfort.

Remember that the most important investment decision isn't necessarily how you start—it's that you start and stay consistent. Whether you choose lump sum investing or DCA, the commitment to a long-term investment strategy aligned with your financial goals and risk tolerance is what truly drives wealth creation over time.

The best investment strategy is one you can confidently stick with through market ups and downs. By understanding both approaches, you've already taken a significant step toward making an informed decision that works for your unique financial journey.

If you like this post you may also like:

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Fifth Person. (n.d.). Every US stock market crash since the 1950s. Retrieved from https://fifthperson.com/every-us-stock-market-crash-since-the-1950s/

Housel, M. (2020). The psychology of money: Timeless lessons on wealth, greed, and happiness. Harriman House.

Investopedia. (n.d.). Market correction. Investopedia. Retrieved from https://www.investopedia.com/terms/marketcorrection.asp

Investopedia. (n.d.). Stock market crash. Investopedia. Retrieved from https://www.investopedia.com/terms/marketcrash.asp

Investor.Vanguard. (n.d.). Lump-sum investing versus dollar-cost averaging: Which is better? Retrieved from https://investor.vanguard.com/investor-resources-education/news/lump-sum-investing-versus-cost-averaging-which-is-better

Maggiulli, N. (2022). Just keep buying: Proven ways to save money and build long-term wealth. Harriman House.

Maggiulli, N. (n.d.). S&P 500 DCA calculator. Retrieved from https://ofdollarsanddata.com/sp500-dca-calculator/

Maggiulli, N. (n.d.). S&P 500 calculator. Retrieved from https://ofdollarsanddata.com/sp500-calculator/

Nisen, M. (2014, November 6). Mark Zuckerberg wears the same gray t-shirt every day to avoid 'decision fatigue'. Business Insider. Retrieved from https://www.businessinsider.com/mark-zuckerberg-same-t-shirt-2014-11?utm_source=[invalid URL removed]

Officialdata.org. (n.d.). US stocks: S&P 500. Retrieved from https://www.officialdata.org/us/stocks/s-p-500/1926

Reilly, F. K., & Brown, K. C. (2012). Investment analysis and portfolio management (10th ed.). South-Western Cengage Learning.

Siegel, J. J. (2014). Stocks for the long run: The definitive guide to financial market returns and long-term investment strategies (5th ed.). McGraw-Hill Education.

Media, S. P. Global. (n.d.). S&P DJI: Where it all began. Retrieved from https://www.spglobal.com/spdji/en/documents/education/spdji-where-it-all-began.pdf

Introduction

Investing can feel like navigating a financial maze, but choosing the right strategy can make all the difference! Whether you're a seasoned investor or just starting out, understanding the nuanced battle between lump sum investing and dollar cost averaging could be your key to financial success. In this comprehensive guide, we'll break down these two powerful investment strategies, helping you make informed decisions that align with your financial goals.

Understanding Lump Sum Investing

What is Lump Sum Investing?

Lump sum investing is the process by which you invest a large amount of money all at once instead of progressively over time. This one-time investment could be made into any of a variety of different financial instruments including mutual funds, ETF’s, stocks, or bonds. The decision of when that lump sum investment is made could be strategic. This is when you wait for a “market event”, such as the draw down that occurred in April following President Trump’s Liberation day. Or it could simply be made immediately after it is received.

For example: You received a $10,000 inheritance from your frugal, but sweet grandma Judy. You decide to invest all of those funds into a low cost index ETF such as VOO or VEQT as soon as they are deposited into your account.

There are several life circumstances that may result in you receiving an above normal sum of money such as:

Inheritance

Insurance settlement

Pay bonus

Following the sale of an asset such as stocks, or real estate.

Winning a lottery

A previously saved, but not invested nest egg

Uneven pay schedule (ie. Self employed, or independent contractors)

All of these scenarios may provide you with the opportunity to use a lump sum strategy. Or you could just squander it on degeneracy… but we don’t suggest that.

Benefits of Lump Sum Strategy

There are a few potential benefits to utilizing a lump sum strategy.

Better Returns

The first of which is that there is a higher statistical likelihood of better returns. A study conducted by Vanguard showed that from 1976 to 2022, if someone had invested in the MSCI World Index using a lump sum strategy, they would have beat a dollar cost averaging strategy 68% of the time.

Logically, this makes a lot of sense. Over your lifetime, the stock market will likely continue to expand and grow (ie. go upwards). Add to this that bull markets generally last longer than bear markets. So in any given year you are more likely to experience positive returns, than negative.

Ex. Imagine in July 2023, Jake and Mark two brothers get an inheritance of $120,000 each from their Grandma Judy.

Jake invests $120,000 in the S&P 500 immediately (Lump Sum Strategy)

Mark invests $12,000 per month in the S&P 500 for the next 10 months (DCA Strategy)

As of March 2025

Jake will have $154, 913 using a lump sum strategy

Mark will have $149,740 using a DCA strategy

In this example, we specifically selected two random months in the stock market avoiding any “market events” which could skew the numbers in favour of any strategy.

Take Advantage of Market Downturns

Another benefit of a lump sum strategy is that it enables you to take advantage of market downturns. When a market correction or crash occurs, the ability to deploy cash towards an investment provides you with a significant advantage. It enables you to buy stocks or even indices when they are potentially mis-priced and selling at below their intrinsic value. This strategy has helped many successful investors such as Warren Buffet throughout his investing career.

Ex. Imagine Jake and Mark got their inheritance from their Grandma Judy in March 2009.

Jake invests $120,000 in the S&P 500 immediately (Lump Sum Strategy)

Mark invests $12,000 per month in the S&P 500 for the next 10 months (DCA Strategy)

As of March 2025

Jake will have $1,321,681 using a lump sum strategy

Mark will have $945,733 using a DCA strategy

As you can see, the lump-sum strategy produced almost a $400K better return than DCA. Now to be fair, this example was cherry picked because this was the BEST SITUATION for the lump sum strategy. The stock market had crashed in 2008, and March 2009 was the beginning of a huge recovery period. This example was just to show how advantageous this strategy can be during such “market events”.

Removes Psychological Strain

In 2014, during a public Q&A session, the CEO of Meta Mark Zuckerberg stated that he wears the same gray t-shirt every day in order to reduce decision fatigue. By reducing the mental energy he spends on trivial decisions such as clothing choice, it enables him to focus that energy towards solving larger, more important decisions in his life and business.

In much the same way, the act of lump sum investing can reduce the mental burden for many people. Although we enjoy investing, and the thought of tactically planning our decisions to do so is enticing, it may not be for you. Instead, maybe you would rather focus your energy towards your business, hobbies, and family life. In this case, investing your inheritance, or bonus check immediately can be mentally freeing in a way.

Potential Drawbacks of Lump Sum Investing

Although Lump Sum Investing has been shown to be the most effective strategy on average, there are some potential downsides to putting your money to work all at once.

Market Timing Risk

The S&P 500 index is used to track the top 500 companies by market capitalization listed on the New York Stock Exchange. It has existed since 1957. Since this time there has been 10 major market crashes (ie. 20% or > decrease), and 27 market corrections (10% or > decrease). Using a lump sum strategy could result in you purchasing your stocks right before a similar event. The result of which would be a short to medium term decrease in the value of your investments.

Ex. Imagine you invested a $20,000 inheritance from your Uncle Tom on February 19th, 2020 prior to the COVID Crash. During this time period, the market saw a 34% decrease. By March 20th, your investment would have decreased to $13,200.

Although this is a cherry picked example, it demonstrates the extreme swings you may experience in your portfolio if the lump sum investment is made at an inopportune time.

Loss Aversion is a cognitive bias that we all experience which says that we are more emotionally impacted by a loss, then an equivalent gain. In other words, a 20% decrease in your stock portfolio feels horrible. Meanwhile, a 20% gain feels just ok. Due to this inherent bias, the emotional impact of investing right before a “market event” could be traumatic.

However, it is important to remember that as long as you don’t sell your shares, you have not lost money. In the case of 2020, by August 17th the S&P 500 returned to all time highs, and you would have recouped your losses. Although not all recoveries will happen this quickly, history shows us the market always returns to all time highs eventually.

Psychological Strain

Another downside to lump sum investing is the psychological strain you must endure to “pull the trigger”. Investing a large amount of money all at once will inevitably give you anxiety. You will ask yourself questions like “Is this the right time?” or “what if the market goes down after I buy?”.

If you find yourself asking these questions, maybe using a DCA strategy or some hybrid of the two would be better for you.

Opportunity Cost

Have you ever bought something like a pair of shoes, only to find a better option shortly afterwards. If you are lucky, you can go back and return the original item in order to buy the better option. Or maybe you already used it and have to live with buyer’s remorse.

This same feeling can occur when using a lump sum strategy. After the funds are invested. you may find a better stock, or ETF. Or maybe your car breaks down and you realize you need the money to purchase a new one. A number of different and potentially better options may come up. Although you can always sell to switch strategies that may come with its own potential barriers, such as fees, losses, account restrictions, etc.

DCA provides you with the flexibility to take advantage of new opportunities as they arise, and not be anchored to a past decision.

Demystifying Dollar Cost Averaging (DCA)

Dollar Cost Averaging (DCA) is the process of purchasing investments gradually over time on a regular interval. Using a DCA Strategy, you will purchase regardless of the stock price. It is important to make the distinction between two different, but often confused, types of DCA: Traditional and Cash Flow. This distinction was highlighted to us in the amazing investing book “Just Keep Buying” by Nick Maggiuli.

Traditional DCA is what most people will do throughout their lifespan. They will invest a fixed amount of money on a recurring schedule. The timing of those investments is usually coordinated with when they receive their paycheck.

Ex. You receive a $3,000 bi-weekly check from your employer, and you invest 25% or $750 into a low cost index ETF such as VOO or VFV.

Cash Flow DCA, on the other hand, is the process by which you gradually invest a larger sum of money. However, instead of investing the money all at once, as you would using the lump sum strategy, you split it up and invest it bit by bit for a defined time period.

Ex. You receive a $10,000 inheritance from your cousin Sherri, and decide to gradually invest it over the next 12 months. Each month you will invest $833.33.

When the comparison is made between DCA and Lump Sum investing we are generally referring to Cash Flow DCA. In other words you have a large amount of money and would like to know which strategy is better to invest it all at once, or to gradually invest it.

Benefits of DCA

Reduces the Downside Risk

One of the characteristics of stocks is that the price fluctuates on a daily basis. The changes in price may, or may not be associated with the underlying value of the business. The same can be said for other assets such as ETFs, Bonds, REITs, etc. The unfortunate downside of a lump sum strategy is the risk that you may purchase at the “top” of the market cycle (aka when prices are the most expensive). The rationale behind using a DCA strategy is to manage this price risk by purchasing at a variety of different points in time.

For example: Lets imagine you have $500 to invest in a low cost index ETF that currently trades at $50/share. However, after you buy, the price gradually decreases to $42/share (going down by $2 a month) over the next 5 months.

Using a Lump Sum Strategy, your $500 investment would have purchased 10 shares at $50 each. By month 5, the investment would have decreased to $420.

Using a DCA strategy though:

Month 1: $100 buys 2 shares at $50/share

Month 2: $100 buys 2.08 shares at $48/share

Month 3: $100 buys 2.17 shares at $46/share

Month 4: $100 buys 2.27 shares at $44/share

Month 5: $100 buys 2.38 shares at $42/share

Using the DCA strategy you would have purchased a total of 10.9 shares at an average buy price of ~$45.83/share. The value of the investments by month 5 would be $457.80 (ie. number of shares x current market price).

Although statistically DCA is not the most effective strategy on average, it reduces the potential risk of these outlier events. Using the Vanguard study, described above there are still 32% of circumstances whereby a DCA strategy outperforms lump sum. During these situations, a gradual investment of the money allows you to take advantage of a market downturn by buying at progressively lower price points.

Removes Emotions

Imagine you receive a large sum of money all at once from an inheritance, lottery, etc. On one end, your brain tells you that the smartest strategy based on research is to invest that money today. But you are worried, and you ask yourself questions like “what if my investments go down after I buy?” or “I don’t want to lose my money”.

There is a quote by Morgan Housel from the book “Psychology of Money” that explains this dilemma very clearly:

“Finance is overwhelmingly taught as a math-based field, where you put data into a formula and the formula tells you what to do, and it’s assumed that you’ll just go do it. ... It’s not that any of these things are bad or wrong. It’s that knowing what to do tells you nothing about what happens in your head when you try to do it.”

The truth is that there is a large psychological barrier for many people when they have to invest a lot of money, all at once. DCA may not resolve this issue, but it eases the burden by allowing you to start. It provides you with the optionality to switch strategies or stop if you don’t feel comfortable investing all of the funds. Ultimately, it allows you to ignore market timing risks and just start investing today.

It Is Realistic

Although there are certain circumstances where you may have enough money to make the choice between DCA and Lump Sum, it isn’t a common scenario. For most people, they will have to invest on a regular interval because well…that's when they get paid.

Potential Drawbacks of DCA

Cash Drag

The main drawback of a DCA strategy, as we stated earlier, is lower total returns on average. The reason for this underperformance is due to a term called “cash drag”. By holding money in “cash” you will generally have lower returns then another individual who is fully invested into the stock market. The reason why is because the market, despite some periods of volatility, increases over time. Since inception, the average return of the S&P 500 is 10.22%.

Other sources of fixed income such as GICs and bonds have produced significantly lower total returns. And as we described in our post “The Hidden Tax That Everyone Pays (and Most People Don’t Even Know About)”, holding cash is actually destroying the buying power of your money.

Using a Cash Flow DCA strategy, most of your money will be sitting in cash initially, and gradually deployed over time. It will act like a weighted vest, slowing down your growth, and dragging down your performance.

Transaction Costs

A major downside to DCA strategy is that you are required to make multiple deposits, transactions, and possibly currency conversions. Each of which may require you to pay fees or commissions to your brokerage firm. In some cases you may be required to pay as much as $10/ transaction for trades on stocks, and ETF’s.

Let’s imagine two individuals Brian, and Susy are both 20 years of age. Both invest with a bank (ie. which will not be named) that charges a $10/transaction fee. Brian invests $200/month into a low cost index ETF such as VOO. Susy wants to minimize fees so she invests $2,400 on January 1st of each year into the same fund. By age 65:

Brian will have $676,146 (DCA Strategy)

Susy will have $780,942 (Lump Sum Strategy)

Much of these fees can be avoided though by just switching to a discount brokerage firm such as Questrade or Wealthsimple. Both of which charge a whopping… $0/transaction.

Lets use the previous example, but this time they both used a discount brokerage firm. By age 65:

Brian will have $715,733 (DCA Strategy)

Susy will have $784,210 (Lump Sum Strategy)

In other words, avoiding unnecessary transaction fees alone earned Brian an additional $39,587. Susy saved $3,268 by avoiding the one time transaction fee each year.

Procrastination

DCA is often used as an excuse to delay fully investing your money into the market. Instead you invest small amounts gradually over time minimizing your exposure. This is potentially due to a fear of losing your money.

If this is you then maybe you should consider a safer investment strategy, such as the 60/40 portfolio which is 60% stocks, and 40% bonds (ie. alternatively GIC’s). Although historically, 100% stocks have been shown to be the most effective strategy for long term gains, it may not fit with your psychology.

Knowing you are using a safer strategy may allow you to avoid delaying, and just invest all of your funds today.

Practical Implementation Strategies

For those of you who skipped to this part in the article, the short answer is that Lump Sum is better. Obviously, there is nuance to that answer though and that is why this article is not one sentence long. Hopefully, at this point, you have weighed the pros and cons, and determined which strategy you would like to implement. The next reasonable question though is how do I do it?

Lump Sum Implementation

Although there are a few steps involved in Lump Sum investing if you are a beginner, it is actually pretty straight forward:

Open one or more investment accounts with a brokerage firm. This could be a TFSA, RRSP, FHSA, or Taxable Account.

Be careful to check your eligibility and contribution limits to avoid incurring any penalties. For more info on the rules of these accounts, you can review our posts on the subjects.

We like Questrade and Wealthsimple because they are discount brokerage firms. However, you can choose whatever firm you like.

Once the account is open there will be a clickable option to add money, or move money.

You can set up a pre-authorized debit, visa debit, interac e-transfer or simply add the account as a payee on your primary bank account.

Once this is set-up, you can go ahead and transfer the funds from your primary bank account to your investment account.

Depending on the method, it could take a few business days for the transfer to occur.

Once the funds arrive in the investment account, they are now ready to be invested. At this time, you can go to the search menu (🔍) and type in the ticker of the fund you would like to invest in.

The ETF’s we invest in are tickers VEQT, XEQT, & VOO. However, you can invest in whatever stock or ETF that fits your investing strategy.

Once you type in your ticker of choice, it should present a graph of the company's recent performance, and financial information such as the bid-ask spread, market cap, P/E ratio, etc.

There should also be two buttons which read Buy and Sell. Click on the buy button.

Now, this is where it becomes confusing for many, as there are two different options which are a limit buy/order or a market buy/order.

For simplicity let's choose market order, which just simply means you are buying the shares at their current price.

Type in the # of shares you would like to purchase.

It may also give you the option to just input the amount of money you would like to invest.

Provided that you didn’t type in a # larger than the amount of money in your account, it should provide you with a button to review your order.

Click on review order

After this you will be provided with the details of your order including the account type, the ETF/Stock you are purchasing, and the # of shares.

If the details match what you would like to purchase, then you can click the button saying “sent order”.

Once the order is complete you are now an investor… go ahead and add that in your bio on instagram.

DCA Implementation

Setting up a DCA strategy is slightly more challenging as you will have to make deposits every month. However, many brokerage firms provide you with the ability to automate both recurring deposits and buys. How this is set-up though can vary from one firm to the next. Regardless of which brokerage firm you use though, the steps should be similar:

Open one or more investment accounts with a brokerage firm. This could be a TFSA, RRSP, FHSA, or Taxable Account.

Be careful to check your eligibility and contribution limits to avoid incurring any penalties. For more info on the rules of these accounts you can review our posts on the subjects.

We like Questrade and Wealthsimple because they are discount brokerage firms. However, you can choose whatever firm you like.

Once the account is open there will be a clickable option to add money, or move money.

You will have to set up a pre-authorized debit and input your primary bank account information.

You should be provided with a page that allows you to select the following:

The account the money will be transferred too (ie brokerage account)

The account the money will be transferred from (ie. primary bank account)

The amount that will be transferred.

The frequency of those transfers/deposits (ie. weekly, biweekly, monthly)

The start date

The end date

Once this is complete, you can press ok and complete the PAD agreement.

It is important to note that although the transfer is set-up for a specific date, it may take a few business days to be ready to be invested.

Once the funds are deposited into the account you can:

Type in the ticker you would like to purchase by using the search menu (🔍).

Click the Buy button

Select Market Order/Buy

Type in the # of shares or $ amount you would like to invest.

Click Review Order

Click Send Order

Some brokerage firms such as Wealthsimple provide you with the option of setting up recurring investments. This is amazing, as it allows you to completely automate this process. Here is how you set it up.

Type in the ticker you would like to purchase by using the search menu (🔍).

Click the Buy button

Select Recurring

Type in the # of shares or $ amount you would like to invest.

Type in the start date, and frequency

Make sure it occurs after your deposit date.

Click Review Order

If prompted with the option to reinvest dividends you can check yes to further automate this process.

Click Send Order

Conclusion: Making the Right Investment Choice for Your Financial Journey

When deciding between lump sum investing and dollar cost averaging, there's no one-size-fits-all answer. The data clearly shows that lump sum investing has historically outperformed DCA approximately 68% of the time, making it statistically the better choice for maximizing returns. This advantage comes from keeping your money in the market longer and avoiding the "cash drag" that can hamper DCA strategies. It is important to note that although Lump Sum usually wins, it's a bumpier ride!

However, investing isn't purely a mathematical equation—it's deeply psychological. DCA offers significant emotional benefits by reducing the anxiety of market timing and providing protection against the pain of investing right before a downturn. For many investors, particularly beginners or those with lower risk tolerance, the peace of mind from DCA may outweigh the potential for slightly higher returns from lump sum investing.

Your personal circumstances also play a crucial role in this decision:

If you have a high risk tolerance, a long investment horizon, and are comfortable with potential short-term volatility, lump sum investing may be your optimal strategy.

If you're concerned about market timing, have a lower risk tolerance, or would experience significant stress from short-term market drops, DCA might be the better approach for you.

Consider a hybrid approach: invest a portion as a lump sum immediately (perhaps 50-70%) and then dollar cost average the remainder over a few months to balance statistical advantage with psychological comfort.

Remember that the most important investment decision isn't necessarily how you start—it's that you start and stay consistent. Whether you choose lump sum investing or DCA, the commitment to a long-term investment strategy aligned with your financial goals and risk tolerance is what truly drives wealth creation over time.

The best investment strategy is one you can confidently stick with through market ups and downs. By understanding both approaches, you've already taken a significant step toward making an informed decision that works for your unique financial journey.

If you like this post you may also like:

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Fifth Person. (n.d.). Every US stock market crash since the 1950s. Retrieved from https://fifthperson.com/every-us-stock-market-crash-since-the-1950s/

Housel, M. (2020). The psychology of money: Timeless lessons on wealth, greed, and happiness. Harriman House.

Investopedia. (n.d.). Market correction. Investopedia. Retrieved from https://www.investopedia.com/terms/marketcorrection.asp

Investopedia. (n.d.). Stock market crash. Investopedia. Retrieved from https://www.investopedia.com/terms/marketcrash.asp

Investor.Vanguard. (n.d.). Lump-sum investing versus dollar-cost averaging: Which is better? Retrieved from https://investor.vanguard.com/investor-resources-education/news/lump-sum-investing-versus-cost-averaging-which-is-better

Maggiulli, N. (2022). Just keep buying: Proven ways to save money and build long-term wealth. Harriman House.

Maggiulli, N. (n.d.). S&P 500 DCA calculator. Retrieved from https://ofdollarsanddata.com/sp500-dca-calculator/

Maggiulli, N. (n.d.). S&P 500 calculator. Retrieved from https://ofdollarsanddata.com/sp500-calculator/

Nisen, M. (2014, November 6). Mark Zuckerberg wears the same gray t-shirt every day to avoid 'decision fatigue'. Business Insider. Retrieved from https://www.businessinsider.com/mark-zuckerberg-same-t-shirt-2014-11?utm_source=[invalid URL removed]

Officialdata.org. (n.d.). US stocks: S&P 500. Retrieved from https://www.officialdata.org/us/stocks/s-p-500/1926

Reilly, F. K., & Brown, K. C. (2012). Investment analysis and portfolio management (10th ed.). South-Western Cengage Learning.

Siegel, J. J. (2014). Stocks for the long run: The definitive guide to financial market returns and long-term investment strategies (5th ed.). McGraw-Hill Education.

Media, S. P. Global. (n.d.). S&P DJI: Where it all began. Retrieved from https://www.spglobal.com/spdji/en/documents/education/spdji-where-it-all-began.pdf