Get our free Debt vs Invest Calculator — click here to access it

Should You Hire a Financial Advisor in Canada?

Wondering if a financial advisor is worth it? Learn when to hire one, how they charge, and whether a DIY approach could work better for your goals.

INVESTING FOR BEGINNERS

5/3/202512 min read

Introduction

When you start learning about the world of personal finance it may seem very overwhelming. There is a lot to learn. Like most things in life the more you learn, the more you realize how much there is to know. Our goal with this website is to provide you with the information you need to make informed decisions. However, for many, this may be to complex or time consuming. You want to direct your effort towards other endeavours in life such as your occupation, hobbies, and family. In order to provide yourself with peace of mind you outsource the job of dealing with your money to a financial professional. In today’s post we explore the benefits and drawbacks of this strategy.

What Are The Benefits Of Hiring A Financial Advisor?

With most things in life you save yourself money, time, or hardship by going directly to the expert in their respective field.

Need to do your taxes… you hire an accountant.

Need to get in shape but don’t know how to workout… you hire a personal trainer.

When you have a medical issue… you go to your doctor.

The same can be true for managing your money. By going to a professional for money management there are several benefits including:

Identifying the correct investment strategy based on your risk tolerance.

Developing a financial plan to guide saving targets.

Estate Planning.

Retirement planning.

Business Finances.

Avoiding or minimizing tax liabilities.

And access to certain insurance based products.

Some other benefits are less obvious though, such as reducing the impact of human misjudgment.

When investing on your own, people are prone to making poor decisions. This is made worse with the ease of access to brokerage accounts. Many of which allow you to access your account instantaneously directly on your phone via a mobile app. This means that you can constantly get access to real time data of what is going on in the market. And the market is a roller coaster ride consisting of large ups and downs.

If you have a low tolerance for this degree of volatility, having total control over your investments could result in you making poor selling or buying decisions. By introducing a middle man you have an opportunity to talk through a decision before it is made irrationally.

What Are The Drawbacks Of Hiring A Financial Advisor?

The benefits of having someone manage your money are extensive, and not to be ignored.

But what if we told you that it doesn’t mean you will get a better return on your money?

Actually, it is highly likely that it will mean exactly the opposite. Worse returns in exchange for guidance.

According to legendary index fund investor John Bogle there are three broad reasons why this is the case:

Poor Selection/Timing of Selection

High Management Fees

Tax Implications

Poor Selection/ Timing of Selection

Based on an assessment of risk tolerance a financial professional will generally invest your money in one, or more mutual funds. Broadly speaking, these are funds that are actively managed. That is someone is responsible for buying, and selling securities (ie. stocks, bonds, etc) with the money provided by their depositors (ie. you). The objective of these funds are to produce an above average return on your money, in exchange for a fee.

So what is the problem?

The problem is that a vast majority do not accomplish this objective. In fact there are only a select few mutual funds that have consistently beat a stock market index like the S&P 500. According to a SPIVA report, 65% of all actively managed funds underperformed the S&P 500 in 2024.

The reason why is because the person/group of people actively trading in the mutual fund often make selection “errors” that result in below average returns. There are only a select few active money managers that have produced above average returns long enough to suggest that not only luck is involved. The chances that the fund your advisor selected is one of those high performers is in the single digits, if not close to 0%.

Worse yet some financial advisors, like all humans, can be prone to cognitive biases. This may result in them buying funds that have a recent history of high performance, and selling funds with a recent history of low performance. This sounds good on paper until you remember the classic disclaimer that appears on most financial products “past performance is no guarantee of future returns”. In reality, high performing funds are more likely to underperform in the years to come.

Meanwhile, as an self-investor you can very easily obtain average market returns. This can be done by investing on your own in either an index ETF (exchange traded fund) that follows the S&P 500. This can be done in a trading or brokerage account through your bank with no intermediary necessary.

High Management Fees

Let’s just say that in an imaginary world the professional managing your money found the outlier mutual fund that is consistently beating the market (ie. S&P 500 index). As we have said this is rare…but this is a for instance.

Would you still receive above average returns on your money? Unfortunately, probably not.

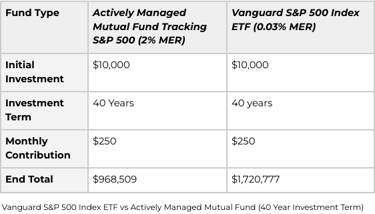

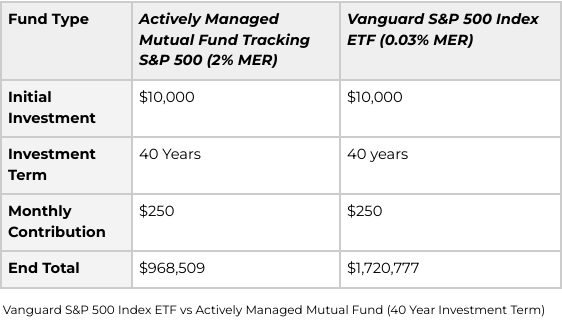

The reason why this is the case is because of high management fees. In Canada the average MER (Management Expense Ratio) for a mutual fund ranges from 1-3%. Meanwhile, the Vanguard S&P 500 ETF (Ticker VOO) which tracks the S&P 500 index has a management expense ratio of 0.03%. Yes, you heard that correctly… 1-3% vs 0.03%

What does this mean?

This means that if both funds increase by 10% before fees (ie. The average return of the S&P 500 in the last 100 years). The individual invested in the mutual fund would see a <8% increase in their portfolio. The individual who put their money in the Vanguard S&P 500 ETF would see a 9.97% increase. Multiply this by 40 years and the implications are massive (See Figure 1):

If this isn’t bad enough there are often additional fees associated with purchasing mutual funds including:

Early Withdrawal Fees

There may be a required minimum holding period. If you decide to withdraw your money prior to this date you may incur a fee.

Transaction Costs

Every time a stock is purchased, or sold there is a commission fee that is charged.

The resulting fees could be high considering that actively managed funds trade a lot.

Front End Load and Back End Load Fees

According to the book Beat the Bank by Larry Bates these costs can add another 0.05 percent or 0.75 percent of lost return annually.

Tax Implications

The last important consideration is tax implications. In Canada we have tax sheltered and tax differed accounts such as the TFSA, RRSP, and FHSA. If you have maximized these accounts then you may start to invest in a taxable account.

Actively managed mutual funds generally have a higher frequency of trading. That is they sell securities (ie. stocks, bonds, etc) more often then an index ETF such as VOO. If a profit is made on these sales then the gains are distributed to their shareholders (ie. you), in the form of capital gains.

On the contrary, the primary source of income distribution in a index ETF is dividends, and not capital gains. Dividends is when the company pays out a portion of their profit to their shareholders usually on some predetermined interval (ie. monthly, biannually, annually). These funds incur less capital gains because they don’t sell as frequently an actively managed fund.

Why does this matter?

Although capital gains are generally taxed at a lower rate than dividends. The high frequency of sales may result in you paying more in taxes on the money you earn in a mutual fund relative to a Index ETF. This is just another contributing factor to the lower returns produced by actively managed mutual funds relative to Index ETFs

Caveat

This is not a pass to think you can outperform your money manager by trading securities on your own. This is simply a comparison of an index ETF to a managed mutual fund with a financial advisor. The results invariably show that Index ETFs on average will outperform. However, you deciding to trade securities on your own is more then likely going to result in catastrophic under performance rather than better returns. This is particularly true if you have no understanding of stock analysis.

Don’t try to be a hero…

If you like this post then you may like:

[How Investments Are Taxed in Canada: Taxable Accounts Guide]

[Why the TFSA Is the Best Registered Account in Canada (2025)]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

Admin. (2022, November 29). Investment fees calculator. Ativa Interactive Corp. https://ativa.com/investment-fees-calculator/

Barnea, A. (2020, June 22). High mutual fund fees can steal thousands of dollars from your retirement savings - here’s a better way. Toronto Star. https://www.thestar.com/business/high-mutual-fund-fees-can-steal-thousands-of-dollars-from-your-retirement-savings-here-s/article_69bcb1c1-eec2-5db8-909e-404872e7aef2.html

Bates, L. (2018). Beat the Bank: The Canadian guide to simply successful investing. Dundurn

Bogle, J. C. (2017). The little book of common sense investing: The only way to guarantee your fair share of stock market returns. John Wiley

Canadian Securities Administrators. (n.d.). Types of fees. Retrieved from https://www.securities-administrators.ca/investor-tools/understanding-your-investments/types-of-fees/

Cory Mitchell. (n.d.). Average historical stock market returns for S&P 500: 5-year up to 150-year averages. Trade That Swing. Retrieved from https://tradethatswing.com/average-historical-stock-market-returns-for-sp-500-5-year-up-to-150-year-averages/#:~:text=The%20average%20yearly%20return%20of,including%20dividends)%20is%207.46%25.%20is%207.46%25.)

S&P Global. (n.d.). SPIVA U.S. Scorecard. Retrieved from https://www.spglobal.com/spdji/en/spiva/article/spiva-us/

Introduction

When you start learning about the world of personal finance it may seem very overwhelming. There is a lot to learn. Like most things in life the more you learn, the more you realize how much there is to know. Our goal with this website is to provide you with the information you need to make informed decisions. However, for many, this may be to complex or time consuming. You want to direct your effort towards other endeavours in life such as your occupation, hobbies, and family. In order to provide yourself with peace of mind you outsource the job of dealing with your money to a financial professional. In today’s post we explore the benefits and drawbacks of this strategy.

What Are The Benefits Of Hiring A Financial Advisor?

With most things in life you save yourself money, time, or hardship by going directly to the expert in their respective field.

Need to do your taxes… you hire an accountant.

Need to get in shape but don’t know how to workout… you hire a personal trainer.

When you have a medical issue… you go to your doctor.

The same can be true for managing your money. By going to a professional for money management there are several benefits including:

Identifying the correct investment strategy based on your risk tolerance.

Developing a financial plan to guide saving targets.

Estate Planning.

Retirement planning.

Business Finances.

Avoiding or minimizing tax liabilities.

And access to certain insurance based products.

Some other benefits are less obvious though, such as reducing the impact of human misjudgment.

When investing on your own, people are prone to making poor decisions. This is made worse with the ease of access to brokerage accounts. Many of which allow you to access your account instantaneously directly on your phone via a mobile app. This means that you can constantly get access to real time data of what is going on in the market. And the market is a roller coaster ride consisting of large ups and downs.

If you have a low tolerance for this degree of volatility, having total control over your investments could result in you making poor selling or buying decisions. By introducing a middle man you have an opportunity to talk through a decision before it is made irrationally.

What Are The Drawbacks Of Hiring A Financial Advisor?

The benefits of having someone manage your money are extensive, and not to be ignored.

But what if we told you that it doesn’t mean you will get a better return on your money?

Actually, it is highly likely that it will mean exactly the opposite. Worse returns in exchange for guidance.

According to legendary index fund investor John Bogle there are three broad reasons why this is the case:

Poor Selection/Timing of Selection

High Management Fees

Tax Implications

Poor Selection/ Timing of Selection

Based on an assessment of risk tolerance a financial professional will generally invest your money in one, or more mutual funds. Broadly speaking, these are funds that are actively managed. That is someone is responsible for buying, and selling securities (ie. stocks, bonds, etc) with the money provided by their depositors (ie. you). The objective of these funds are to produce an above average return on your money, in exchange for a fee.

So what is the problem?

The problem is that a vast majority do not accomplish this objective. In fact there are only a select few mutual funds that have consistently beat a stock market index like the S&P 500. According to a SPIVA report, 65% of all actively managed funds underperformed the S&P 500 in 2024.

The reason why is because the person/group of people actively trading in the mutual fund often make selection “errors” that result in below average returns. There are only a select few active money managers that have produced above average returns long enough to suggest that not only luck is involved. The chances that the fund your advisor selected is one of those high performers is in the single digits, if not close to 0%.

Worse yet some financial advisors, like all humans, can be prone to cognitive biases. This may result in them buying funds that have a recent history of high performance, and selling funds with a recent history of low performance. This sounds good on paper until you remember the classic disclaimer that appears on most financial products “past performance is no guarantee of future returns”. In reality, high performing funds are more likely to underperform in the years to come.

Meanwhile, as an self-investor you can very easily obtain average market returns. This can be done by investing on your own in either an index ETF (exchange traded fund) that follows the S&P 500. This can be done in a trading or brokerage account through your bank with no intermediary necessary.

High Management Fees

Let’s just say that in an imaginary world the professional managing your money found the outlier mutual fund that is consistently beating the market (ie. S&P 500 index). As we have said this is rare…but this is a for instance.

Would you still receive above average returns on your money? Unfortunately, probably not.

The reason why this is the case is because of high management fees. In Canada the average MER (Management Expense Ratio) for a mutual fund ranges from 1-3%. Meanwhile, the Vanguard S&P 500 ETF (Ticker VOO) which tracks the S&P 500 index has a management expense ratio of 0.03%. Yes, you heard that correctly… 1-3% vs 0.03%

What does this mean?

This means that if both funds increase by 10% before fees (ie. The average return of the S&P 500 in the last 100 years). The individual invested in the mutual fund would see a <8% increase in their portfolio. The individual who put their money in the Vanguard S&P 500 ETF would see a 9.97% increase. Multiply this by 40 years and the implications are massive (See Figure 1):

If this isn’t bad enough there are often additional fees associated with purchasing mutual funds including:

Early Withdrawal Fees

There may be a required minimum holding period. If you decide to withdraw your money prior to this date you may incur a fee.

Transaction Costs

Every time a stock is purchased, or sold there is a commission fee that is charged.

The resulting fees could be high considering that actively managed funds trade a lot.

Front End Load and Back End Load Fees

According to the book Beat the Bank by Larry Bates these costs can add another 0.05 percent or 0.75 percent of lost return annually.

Tax Implications

The last important consideration is tax implications. In Canada we have tax sheltered and tax differed accounts such as the TFSA, RRSP, and FHSA. If you have maximized these accounts then you may start to invest in a taxable account.

Actively managed mutual funds generally have a higher frequency of trading. That is they sell securities (ie. stocks, bonds, etc) more often then an index ETF such as VOO. If a profit is made on these sales then the gains are distributed to their shareholders (ie. you), in the form of capital gains.

On the contrary, the primary source of income distribution in a index ETF is dividends, and not capital gains. Dividends is when the company pays out a portion of their profit to their shareholders usually on some predetermined interval (ie. monthly, biannually, annually). These funds incur less capital gains because they don’t sell as frequently an actively managed fund.

Why does this matter?

Although capital gains are generally taxed at a lower rate than dividends. The high frequency of sales may result in you paying more in taxes on the money you earn in a mutual fund relative to a Index ETF. This is just another contributing factor to the lower returns produced by actively managed mutual funds relative to Index ETFs

Caveat

This is not a pass to think you can outperform your money manager by trading securities on your own. This is simply a comparison of an index ETF to a managed mutual fund with a financial advisor. The results invariably show that Index ETFs on average will outperform. However, you deciding to trade securities on your own is more then likely going to result in catastrophic under performance rather than better returns. This is particularly true if you have no understanding of stock analysis.

Don’t try to be a hero…

If you like this post then you may like:

[How Investments Are Taxed in Canada: Taxable Accounts Guide]

[Why the TFSA Is the Best Registered Account in Canada (2025)]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

Admin. (2022, November 29). Investment fees calculator. Ativa Interactive Corp. https://ativa.com/investment-fees-calculator/

Barnea, A. (2020, June 22). High mutual fund fees can steal thousands of dollars from your retirement savings - here’s a better way. Toronto Star. https://www.thestar.com/business/high-mutual-fund-fees-can-steal-thousands-of-dollars-from-your-retirement-savings-here-s/article_69bcb1c1-eec2-5db8-909e-404872e7aef2.html

Bates, L. (2018). Beat the Bank: The Canadian guide to simply successful investing. Dundurn

Bogle, J. C. (2017). The little book of common sense investing: The only way to guarantee your fair share of stock market returns. John Wiley

Canadian Securities Administrators. (n.d.). Types of fees. Retrieved from https://www.securities-administrators.ca/investor-tools/understanding-your-investments/types-of-fees/

Cory Mitchell. (n.d.). Average historical stock market returns for S&P 500: 5-year up to 150-year averages. Trade That Swing. Retrieved from https://tradethatswing.com/average-historical-stock-market-returns-for-sp-500-5-year-up-to-150-year-averages/#:~:text=The%20average%20yearly%20return%20of,including%20dividends)%20is%207.46%25.%20is%207.46%25.)

S&P Global. (n.d.). SPIVA U.S. Scorecard. Retrieved from https://www.spglobal.com/spdji/en/spiva/article/spiva-us/