Get our free Debt vs Invest Calculator — click here to access it

What Is Good Debt in Canada (and When It Makes Sense to Borrow)

Discover what is good debt in Canada and when it makes sense to borrow. Learn how mortgages, student loans, and business loans can help build long-term wealth when used wisely.

DEBTFINANCIAL BASICS

NextGenFinance Team

10/27/202528 min read

My post content

Understanding Debt: The Basics

We've all heard the advice: stay out of debt at all costs. Credit cards are dangerous. Loans are traps. If you can't pay cash for it, you can't afford it.

But here's the reality: most Canadians who build significant wealth do it with borrowed money.

That might sound counterintuitive, but debt isn't inherently good or bad. It's a tool. And like any tool, it can either work for you or against you, depending on how you use it.

At its simplest, debt is money you owe to a lender. It occurs when you borrow money today with the intention of repaying it in the future, typically with interest. The vast majority of Canadians will take on some form of debt throughout their lifetime whether it's a mortgage, student loan, car loan, or credit card balance.

The key difference between good debt and bad debt comes down to one question: What are you using the borrowed money for?

When debt is used to purchase assets that have the potential to increase your net worth or boost your income potential, it can be a powerful wealth-building tool. Think of it less as "going into debt" and more as making a leveraged investment. A mortgage lets you buy a home that may appreciate in value. A student loan can give you access to a career that dramatically increases your earning power. A business loan might help you start an enterprise that generates income for decades.

Contrast this with using a high-interest payday loan to fund an all-inclusive trip to Cabo. That's consumer debt where you borrow money for purchases with minimal to no economic return. This is where debt starts falling into the "bad" category: you're left with the bill and the interest charges, but nothing that improves your financial position.

The difference matters. Good debt allows Canadians to purchase homes, get an education, and start businesses. All of which have the potential to improve your economic position and quality of life. Without access to borrowing, most of these opportunities would be out of reach for the average person.

In this article, we'll walk through what qualifies as good debt in the Canadian context, when it makes sense to borrow, and how to evaluate whether taking on debt will actually help you build wealth, or just dig you into a deeper hole.

What Is Good Debt?

Good debt is any form of borrowing that is projected to increase your net worth or income potential over time.

Unlike bad debt—which funds consumption with no economic return—good debt acts as leverage to purchase appreciating assets or income-generating opportunities. The key difference comes down to one question: What are you using the borrowed money for?

Types of Good Debt

The most common forms of good debt include:

Mortgage

Student Loan

Business Loan

Investment Loan

Mortgage

A home has utility beyond an investment opportunity. It provides Canadians with shelter, security, and a sense of independence. It represents a key life milestone for many young Canadians. A survey conducted by Ipsos found that 77% of Canadians agree that owning a home is the best investment a person can make. Contrary to this belief, smart renting decisions may allow you to build long term wealth faster than owning a home. However, it doesn’t fulfill this inherent need.

Purchasing a house by taking out a mortgage can be a good investment decision though. This is particularly true in Canada where house prices have gone through an extended bull market.

Another key feature of having a mortgage is that it acts as a “forced savings". Most people are better at paying off bills than setting money aside for investments. A mortgage acts as both a bill and an investment, while failure to pay means loss of a roof over your house. Pretty good incentives if you ask me.

Primary Residence

According to The Canadian Real Estate Association (CREA) the average house price in Canada as of August 2025 was $664,078. The minimum down payment to avoid paying CMHC insurance on this home would be $132,816 (or 20%) *. If you think that this is out of reach, then you are like most Canadians.

Now imagine you had to pay for the entire house at the time of purchase? That is what would be required if you couldn’t take out debt to pay for it. This is just one example of why borrowing is important.

When you purchase a house as your primary property, the only investment opportunity occurs as a result of capital appreciation (ie. increase in house cost). This is because you aren’t receiving any steady income flow from the home while you live in it. Even without regular income, this has worked out moderately well for Canadians in recent history. As of August 2015, 10 years prior, the average house price was only $430,536. This equates to a 54% total return or 4.43%/year return. Depending on which market you decided to live in, the returns could have been much higher (ex. Toronto vs North Bay).

* The actual minimum payment on this home would be 6.24% or $41,408. However, you will be required to pay CMHC which is an additional $24,907. The result of such a low down payment is that you increase your total borrowing cost on the house by an additional $100K+.

Rental Property

The potential investment returns of a mortgage loan increase significantly when you use the funds to purchase a rental property. Instead of relying on only price appreciation, you also have a steady flow of rental income. In a perfect world, the rental income should cover mortgage payments, property taxes, and maintenance costs. This means that your initial investment consists of only your down payment, and any start up costs. Your expenses are any taxes on rental income, and capital gains upon sale.

Because, in an ideal scenario, your regular expenses are covered by rental income alone, your returns should be calculated based on your initial investment costs. For example:

Initial Investment= $80,000

Purchase Price (2015)= $430,000

Equity Built from 2015- 2025 =$242,000

Built through payments made on your mortgage loan throughout the term.

Sale Price (2025)= $660,000

Capital Gains = $230,000

Total Returns = $472,000 (Capital Gains + Equity Built)

Rate of Return = 490% or 19.42%/year

Unfortunately, many people do not receive a return even close to this amount because their rental income does not fully cover the operational costs of the rental unit. Even well managed properties should only expect between a 7-10% annual return. As a stock investor at heart, this seems like an incredible amount of work and risk for a rather average return.

Student Loan

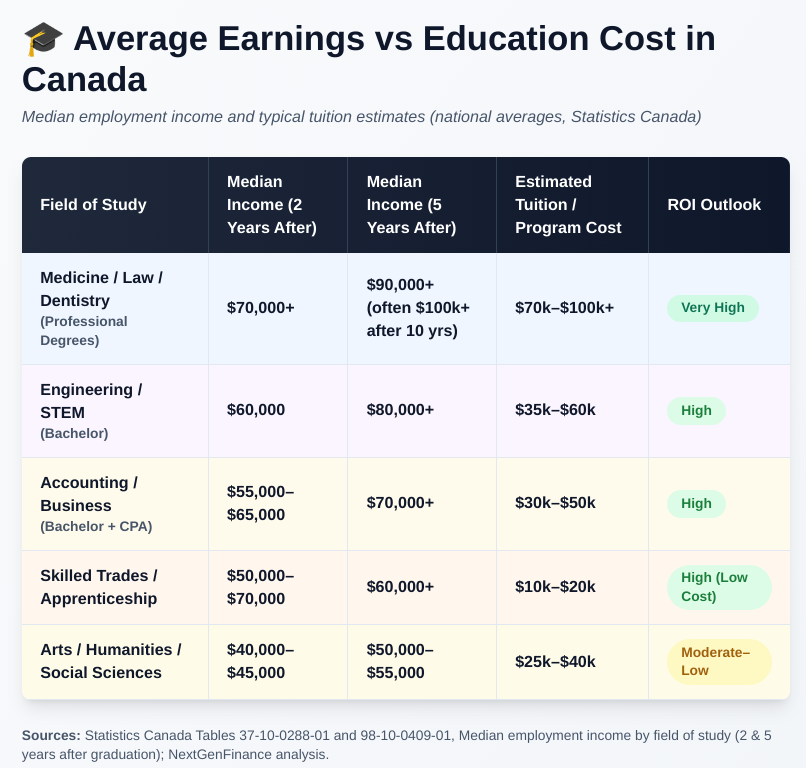

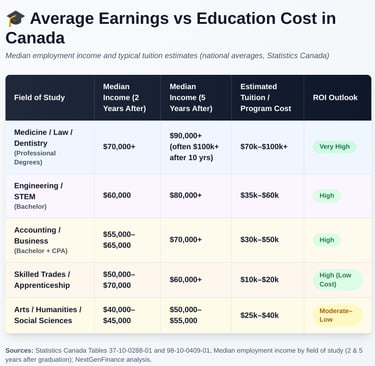

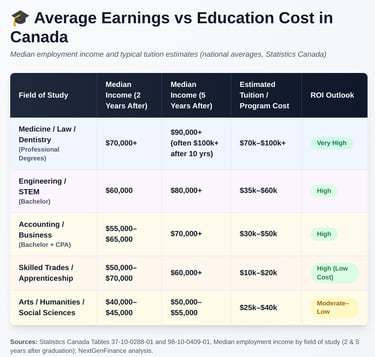

A student loan could also be considered a good source of debt when it provides you access to an education that meaningfully improves your earning potential. However, like any other good debt, the quality of the return matters. In the case of a student loan, the question becomes what are the employment opportunities and income levels associated with your program of study?

In fields such as the skilled trades, medicine, law, engineering, and business the results are more clear. According to Statistics Canada, these fields have the highest employment rates, and earrings within just a few years of graduation. Five years after finishing school, median employment income typically exceeds $90,000 for medical fields, $80,000 for engineering, and $70,000 for business and accounting graduates. These figures often continue to rise sharply over time.

In contrast, graduates in arts, humanities, and certain social sciences often earn less and take longer to see a financial return from their education. Median income for these fields can range from $40,000–$50,000 five years after graduation.

This doesn’t mean that an arts degree or similar program lacks value. Education can offer personal growth, communication skills, and adaptability that are valuable across careers. But from a purely investment-return perspective, it’s important to evaluate whether the cost of your education, and the debt required to finance it, aligns with the financial opportunities it’s likely to provide.

Investment Loan

An investment loan is when you borrow money in order to increase your returns in the stock market. Unlike a mortgage, which provides utility outside of investment returns (ie. place to lay your head at night), investment loans are intended solely to earn more money. The problem is like with all asset classes they can go up…or down. This means that the benefits you receive in a bull market could be tremendous. You could also experience massive losses in a bear market.

Risk Assessment

A normal process in investing is to evaluate risk. In recent memory, assets such as small to medium size tech stocks and cryptocurrencies would fit into the high risk category. Despite this, many people continue to invest into them…why? They have “recently” earned returns significantly above the market average. Between October 2015 and October 2025, Bitcoin has returned a 39,351% return. This is an annualized return of 82% per year.

To many individuals, the risk of investing in these assets is worth the reward. This may work when gambling your own money. However, when borrowing money from someone else (ie. bank) the risk increases significantly.

The amount of risk of an investment loan depends significantly on a variety of factors:

The expected rate of return of the asset

The relative safety or stability of the asset

The loan interest rate

Market Factors (economic, government, etc)

How Investment Loans Boost Your Returns

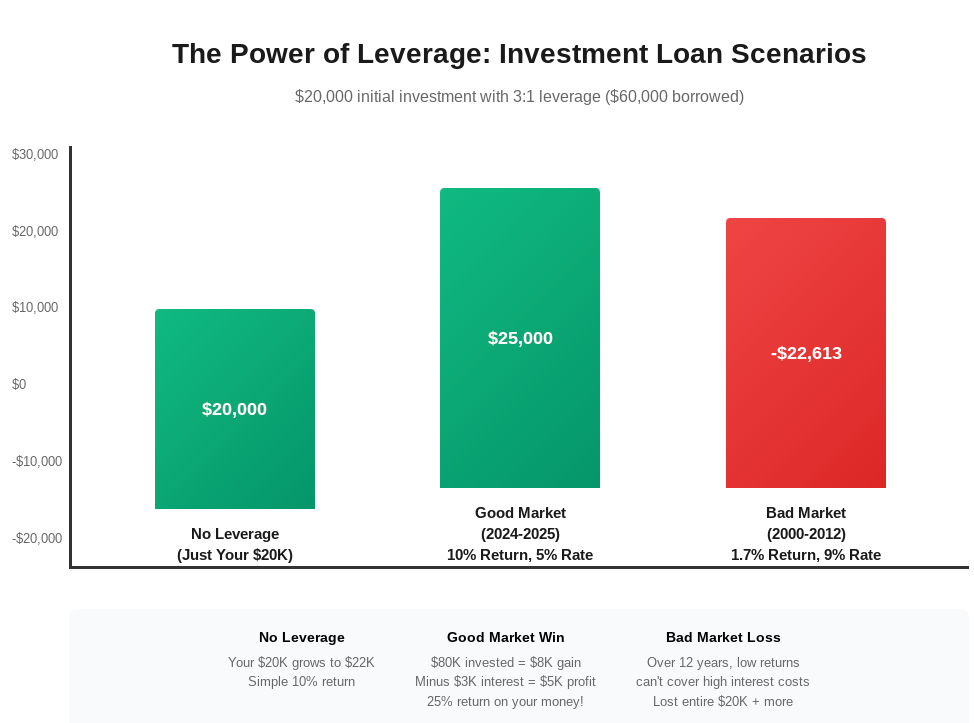

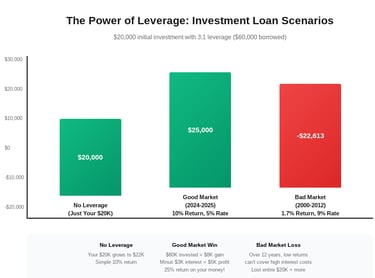

In simple terms, investment loans allow you to boost your returns by increasing your bet size. The historical average rate of return of the S&P 500 is ~10%/year. The current investment loan interest rate offered at most banks is between 5-7%. Depending on the bank you may be able to borrow up to 3x your initial investment.

Ex. You borrow 3:1 at a rate of 5% on $20,000 to invest in the S&P 500 today. The bank gives you an additional $60,000 to invest. In October 2026, you cash out and repay your loan. In this case, leverage increased your annual investment returns by >2x.

Leveraged Investment Returns

$80,000 x 10% (S&P 500 Return) = $8,000

Cost to Borrow

$60,000 x 5% (Interest Rate on Loan)= $3,000

Net 1 Year Returns

$5,000 or 25% of initial investment

The Downside of Investment Loans

The choice of borrowing money to invest appears great on the surface. Unfortunately, it isn’t all sunshine and rainbows. The reason why is simple, the market doesn’t always do what we want it to do.

Just because the S&P 500 produces these returns on average doesn’t mean that it will continue to do so. In fact there have been multiple periods throughout history where the average returns were significantly below 10%. Between 2000-2012 we experienced the Dot-com bust and the Global Financial Crisis. The average total return (including dividends) over this 12 year period was 1.7%/year. In real (inflation-adjusted) terms, that is a 0% return which is why this period is referred to as a “lost decade”. To show the consequences of borrowing during this time lets use the following example:

Ex. You borrow 3:1 at a rate of 9% on $20,000 to invest in the S&P 500 in 2000. Since it is 3:1 the bank gives you an additional $60,000 to invest. In 2012, 12 years later, you decide to cash out and repay your loan. In this case, you would have lost your entire principle investment to service the interest costs on the loan.

Leveraged Investment Returns

$80,000 x 1.7%/year compounded = $17,935.79

Cost to Borrow

$60,000 x 9% (Interest Rate on Loan) x 12 years compounded= $40,548.47

Net 12 Year Returns

($22,612.68) or -113% Return

As the late great Charlie Munger said “There are three ways to go broke: liquor, ladies, and leverage”.

Investment Loans for Fixed Income

You may think that the solution to the problem of risk would be to buy stable asset classes such treasury or high grade corporate bonds, money market funds, or GIC’s. Unfortunately, at current rates these asset classes will not provide a significant enough reward to offset the cost of borrowing. As we said above, you can get an investment loan at 5-7% interest. Most of these asset classes currently only yield in the 3-4% range. In order for fixed income to actually work the interest rate on the investment loan has to be less than the projected yield on the investment.

To achieve a significant enough return you will have to look to high yield (ie. junk) bonds, or private credit. Both of which could be as risky, or more so than stocks depending on the market conditions.

When Investment Loans Work to Perfection

In 2020, Warren Buffett’s Berkshire Hathaway made a major investment in Japan’s five largest trading houses, buying about 5% stakes in each. To finance this move, Berkshire issued yen-denominated bonds in Japan rather than using U.S. dollars. This allowed him to borrow at ultra-low interest rates, roughly 0.17% to 1%, depending on the bond maturity. This strategy let Buffett take advantage of Japan’s cheap borrowing costs while gaining exposure to strong, diversified global businesses that pay solid dividends.

RRSP Loan

An RRSP loan is a short term loan that is used to make a lump-sum RRSP contribution. It is a variation of an investment loan. However, it provides a few unique benefits:

Accelerates savings

Boosts tax refund

Helps you catch up on contributions

Tax Refund

Any contributions to an RRSP can be used to offset taxes in the year of the contribution. They can also be carried forward to future years.

Ex. If you earn $100,000 in 2025 but also contributed $10,000 to an RRSP then your taxable income decreases to $90,000.

An RRSP loan allows you to reduce your immediate tax burden after a high earning year (ex. Secondary Property Sale). Since Canada has a progressive tax system, your marginal tax rate increases the more you earn. This means that the benefits of an RRSP are better for high earning individuals (or during a high earning year).

Ex. Imagine you live in Ontario and earn $100,000 in 2025. However, you also sold a family cottage for a capital gain of $400,000. You will be required to pay $120,624 in income tax. In order to offset the immediate tax burden you could take out a $32,490 RRSP loan (maximum 2025 limit) at 5% which you intend to pay back within the year. In this example:

A $32,490 RRSP contribution reduces your income taxes to $103,233. A total savings of $17,391.

Interest paid on the loan over the year is $867

Net Savings is $16,524

Catch Up On Contributions

An RRSP loan can also be an effective strategy to catch up or maximize contributions. Currently, you should have two updated amounts on your MyCRA account:

2025 Deduction Limit

Unused RRSP Contributions Available to Deduct in 2025

The total of these two numbers is what you are able to contribute to your RRSP and deduct from your tax return this year.

Many individuals will inevitably experience years where they are unable to contribute this amount. If your goal is wealth accumulation, and financial independence, this is not optimal. Instead, what you want to do is maximize your contributions, especially early on in your investing journey. This allows compound interest to do its work.

Another scenario where an RRSP loan could be useful is in the case of the two programs offered through the RRSP which are the Home Buyers Plan (HBP), and Lifelong Learning Plan (LLP). These programs allow you to withdraw funds from your RRSP to pay for an education or a home purchase. Both involve a mandatory repayment period. In order to maximize your long term returns, you can use an RRSP loan to repay the full amount immediately, and gradually pay off the loan over time.

RRSP Loan In Practice

Joe is 23 years old, living in Ontario, and he currently earns a salary of $100,000 as a plumber. He has earned the same salary since 2023, but has never contributed to an RRSP. He should have a $32,000 RRSP deduction limit in 2025, which consists of:

2025 Deduction Limit: $18,000 (18% of 2024 income)

Unused RRSP Contributions Available to Deduct in 2025: $18,000

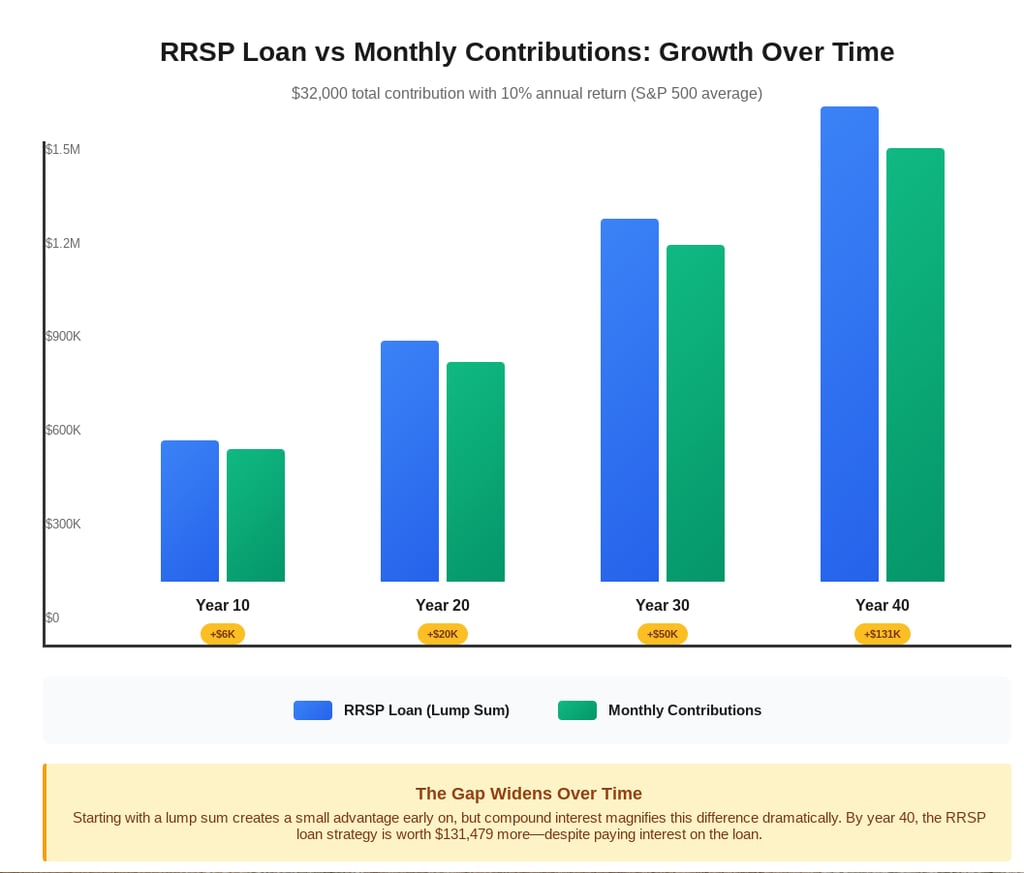

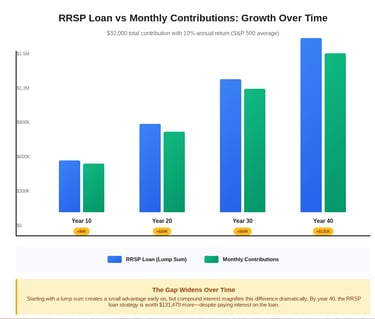

His goal is to contribute this $32,000 to his RRSP as soon as possible. He will be investing the funds into a S&P 500 ETF which earns an average of 10%/year. He has two options:

Option 1

Take out a $32,000 RRSP Loan today at 5% interest and repay it over the next 24 months.

Tax Savings (2025) = $9,699

Earnings (2025-2026) = $6,720

Interest Paid on Loan = ($1,655)

Compounded Growth of Initial Investment (40 years)= $1,448,296

Option 2

Contribute $1333.33 per month for the next 24 months.

Tax Savings (2025-2026)= $10,796

Earnings (2025-2026) = $3,205

Interest Paid on Loan = $0 (No loan)

Compounded Growth of Initial Investment (40 years) = $1,316,817

As you can see from this example, the RRSP loan is the better of the two options. The initial growth in the investment throughout 2025-2026 makes up for the cost of borrowing, and the less tax deductions you receive. However, what is even more important is there is >$100,000 difference in the long term compounded returns from using the loan option.

Business Loan

A business loan is used to facilitate the initiation, continued operations, or growth of a business.

Since many businesses are very capital intensive (ex. construction) most people will need to take out a loan to start. This borrowing process often continues throughout the first few years of many businesses until they are able to build up enough cash to operate through profits alone. As they continue to grow, they may run into growth barriers (ex. More employees, equipment demands, etc) that require more cash then they have on hand which is when a loan will become useful again. This process often continues throughout most businesses' lifespan.

However, a business loan, like other forms of debt, can only be categorized as good if the funds are used for the right purposes. More specifically, to increase the profits of the business. A good business loan adds capacity, and/or income.

Ex. You start a lawn maintenance business using a riding lawn mower, a pickup truck and a trailer. You service all of your clients yourself, but you are fully booked. You’ve hit a growth ceiling. You go to the bank and take out a $25,000 loan at 7% interest to finance expansion. You use the funds for the following:

New Commercial Grade Lawn Mower- $10,000

Utility Trailer- $5,000

Truck Down Payment- $5,000

Marketing (Flyers, website, local ads)- $2,000

Working Capital buffer (fuel, payroll)- $3,000

The Dark Side of a Business Loan

Not all business loans are created equal though. A bad business loan adds debts without improving the businesses earning power. This occurs when you use the loan to:

Buy luxury or non-essential items (ex. Top of the line truck)

Use it just to keep a non profitable business afloat

Fund personal expenses (ie. Pay off your credit car, or renovate your home).

However, it could also be a bad loan if you overestimated the demand of the business by expanding too fast, or if the interest rate on the loan is too high (ex. Pay day loans) that it eats into profits.

The Bottom Line: When Does Debt Make Sense?

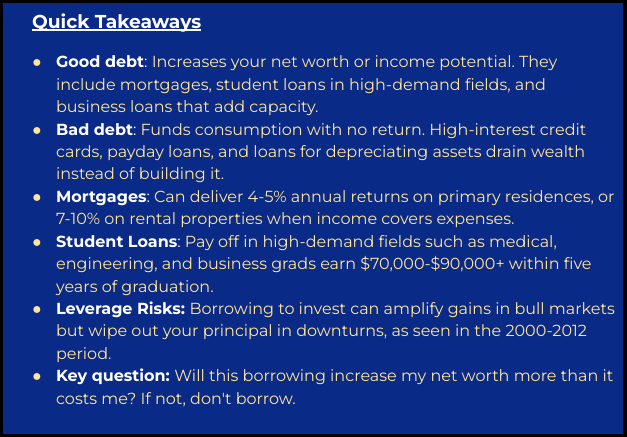

Good debt in Canada boils down to a simple test: Will this borrowing increase your net worth or earning potential more than it costs you?

If you're taking out a mortgage to buy a home that will appreciate, a student loan for a high-demand career, or a business loan that generates more revenue than the interest costs, you're using debt strategically.

But if you're borrowing at high interest rates to fund consumption, or taking on debt without a clear path to a positive return, you're likely headed for financial trouble.

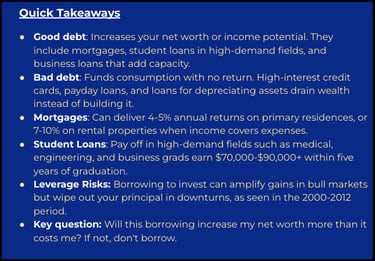

Key Takeaways

Good debt builds wealth: mortgages, student loans in high-earning fields, business loans that add capacity, investment loans used carefully

Bad debt funds consumption: high-interest credit cards, payday loans, car loans for depreciating assets

The interest rate matters: Your return must exceed your borrowing cost

Risk matters too: Leveraged investments amplify both gains and losses

Before taking on any debt, ask yourself:

What is this money being used for?

What is the expected return or benefit?

What is the true cost of borrowing (interest + fees)?

Can I afford the payments if things don't go as planned?

Most wealthy Canadians use debt strategically. The difference between them and those drowning in debt isn't whether they borrow. Rather it's what they borrow for and whether they can manage the risk.

Use debt as a tool, not a crutch. When used wisely, it can accelerate your path to financial independence. When misused, it can set you back for years.

Related Posts:

[Budgeting for Beginners: How to Take Control of Your Money]

[How Much Emergency Fund Do You Need in Canada (2025 Guide)]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

Canada Revenue Agency. (n.d.). CRA login services. Government of Canada. https://www.canada.ca/en/revenue-agency/services/e-services/cra-login-services.html

Ipsos. (n.d.). Six in ten Canadians who don't own a home have given up on owning. https://www.ipsos.com/en-ca/six-in-ten-canadians-who-dont-own-home-have-given-up-on-owning

Statistics Canada. (n.d.). Earnings and employment by field of study and level of highest certificate, diploma or degree, annual [Data table 98-10-0409-01]. https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=9810040901

The Canadian Real Estate Association. (n.d.). National price map. Canadian Housing Market Statistics. https://www.crea.ca/housing-market-stats/canadian-housing-market-stats/national-price-map/

Understanding Debt: The Basics

We've all heard the advice: stay out of debt at all costs. Credit cards are dangerous. Loans are traps. If you can't pay cash for it, you can't afford it.

But here's the reality: most Canadians who build significant wealth do it with borrowed money.

That might sound counterintuitive, but debt isn't inherently good or bad. It's a tool. And like any tool, it can either work for you or against you, depending on how you use it.

At its simplest, debt is money you owe to a lender. It occurs when you borrow money today with the intention of repaying it in the future, typically with interest. The vast majority of Canadians will take on some form of debt throughout their lifetime whether it's a mortgage, student loan, car loan, or credit card balance.

The key difference between good debt and bad debt comes down to one question: What are you using the borrowed money for?

When debt is used to purchase assets that have the potential to increase your net worth or boost your income potential, it can be a powerful wealth-building tool. Think of it less as "going into debt" and more as making a leveraged investment. A mortgage lets you buy a home that may appreciate in value. A student loan can give you access to a career that dramatically increases your earning power. A business loan might help you start an enterprise that generates income for decades.

Contrast this with using a high-interest payday loan to fund an all-inclusive trip to Cabo. That's consumer debt where you borrow money for purchases with minimal to no economic return. This is where debt starts falling into the "bad" category: you're left with the bill and the interest charges, but nothing that improves your financial position.

The difference matters. Good debt allows Canadians to purchase homes, get an education, and start businesses. All of which have the potential to improve your economic position and quality of life. Without access to borrowing, most of these opportunities would be out of reach for the average person.

In this article, we'll walk through what qualifies as good debt in the Canadian context, when it makes sense to borrow, and how to evaluate whether taking on debt will actually help you build wealth, or just dig you into a deeper hole.

What Is Good Debt?

Good debt is any form of borrowing that is projected to increase your net worth or income potential over time.

Unlike bad debt—which funds consumption with no economic return—good debt acts as leverage to purchase appreciating assets or income-generating opportunities. The key difference comes down to one question: What are you using the borrowed money for?

Types of Good Debt

The most common forms of good debt include:

Mortgage

Student Loan

Business Loan

Investment Loan

Mortgage

A home has utility beyond an investment opportunity. It provides Canadians with shelter, security, and a sense of independence. It represents a key life milestone for many young Canadians. A survey conducted by Ipsos found that 77% of Canadians agree that owning a home is the best investment a person can make. Contrary to this belief, smart renting decisions may allow you to build long term wealth faster than owning a home. However, it doesn’t fulfill this inherent need.

Purchasing a house by taking out a mortgage can be a good investment decision though. This is particularly true in Canada where house prices have gone through an extended bull market.

Another key feature of having a mortgage is that it acts as a “forced savings". Most people are better at paying off bills than setting money aside for investments. A mortgage acts as both a bill and an investment, while failure to pay means loss of a roof over your house. Pretty good incentives if you ask me.

Primary Residence

According to The Canadian Real Estate Association (CREA) the average house price in Canada as of August 2025 was $664,078. The minimum down payment to avoid paying CMHC insurance on this home would be $132,816 (or 20%) *. If you think that this is out of reach, then you are like most Canadians.

Now imagine you had to pay for the entire house at the time of purchase? That is what would be required if you couldn’t take out debt to pay for it. This is just one example of why borrowing is important.

When you purchase a house as your primary property, the only investment opportunity occurs as a result of capital appreciation (ie. increase in house cost). This is because you aren’t receiving any steady income flow from the home while you live in it. Even without regular income, this has worked out moderately well for Canadians in recent history. As of August 2015, 10 years prior, the average house price was only $430,536. This equates to a 54% total return or 4.43%/year return. Depending on which market you decided to live in, the returns could have been much higher (ex. Toronto vs North Bay).

* The actual minimum payment on this home would be 6.24% or $41,408. However, you will be required to pay CMHC which is an additional $24,907. The result of such a low down payment is that you increase your total borrowing cost on the house by an additional $100K+.

Rental Property

The potential investment returns of a mortgage loan increase significantly when you use the funds to purchase a rental property. Instead of relying on only price appreciation, you also have a steady flow of rental income. In a perfect world, the rental income should cover mortgage payments, property taxes, and maintenance costs. This means that your initial investment consists of only your down payment, and any start up costs. Your expenses are any taxes on rental income, and capital gains upon sale.

Because, in an ideal scenario, your regular expenses are covered by rental income alone, your returns should be calculated based on your initial investment costs. For example:

Initial Investment= $80,000

Purchase Price (2015)= $430,000

Equity Built from 2015- 2025 =$242,000

Built through payments made on your mortgage loan throughout the term.

Sale Price (2025)= $660,000

Capital Gains = $230,000

Total Returns = $472,000 (Capital Gains + Equity Built)

Rate of Return = 490% or 19.42%/year

Unfortunately, many people do not receive a return even close to this amount because their rental income does not fully cover the operational costs of the rental unit. Even well managed properties should only expect between a 7-10% annual return. As a stock investor at heart, this seems like an incredible amount of work and risk for a rather average return.

Student Loan

A student loan could also be considered a good source of debt when it provides you access to an education that meaningfully improves your earning potential. However, like any other good debt, the quality of the return matters. In the case of a student loan, the question becomes what are the employment opportunities and income levels associated with your program of study?

In fields such as the skilled trades, medicine, law, engineering, and business the results are more clear. According to Statistics Canada, these fields have the highest employment rates, and earrings within just a few years of graduation. Five years after finishing school, median employment income typically exceeds $90,000 for medical fields, $80,000 for engineering, and $70,000 for business and accounting graduates. These figures often continue to rise sharply over time.

In contrast, graduates in arts, humanities, and certain social sciences often earn less and take longer to see a financial return from their education. Median income for these fields can range from $40,000–$50,000 five years after graduation.

This doesn’t mean that an arts degree or similar program lacks value. Education can offer personal growth, communication skills, and adaptability that are valuable across careers. But from a purely investment-return perspective, it’s important to evaluate whether the cost of your education, and the debt required to finance it, aligns with the financial opportunities it’s likely to provide.

Investment Loan

An investment loan is when you borrow money in order to increase your returns in the stock market. Unlike a mortgage, which provides utility outside of investment returns (ie. place to lay your head at night), investment loans are intended solely to earn more money. The problem is like with all asset classes they can go up…or down. This means that the benefits you receive in a bull market could be tremendous. You could also experience massive losses in a bear market.

Risk Assessment

A normal process in investing is to evaluate risk. In recent memory, assets such as small to medium size tech stocks and cryptocurrencies would fit into the high risk category. Despite this, many people continue to invest into them…why? They have “recently” earned returns significantly above the market average. Between October 2015 and October 2025, Bitcoin has returned a 39,351% return. This is an annualized return of 82% per year.

To many individuals, the risk of investing in these assets is worth the reward. This may work when gambling your own money. However, when borrowing money from someone else (ie. bank) the risk increases significantly.

The amount of risk of an investment loan depends significantly on a variety of factors:

The expected rate of return of the asset

The relative safety or stability of the asset

The loan interest rate

Market Factors (economic, government, etc)

How Investment Loans Boost Your Returns

In simple terms, investment loans allow you to boost your returns by increasing your bet size. The historical average rate of return of the S&P 500 is ~10%/year. The current investment loan interest rate offered at most banks is between 5-7%. Depending on the bank you may be able to borrow up to 3x your initial investment.

Ex. You borrow 3:1 at a rate of 5% on $20,000 to invest in the S&P 500 today. The bank gives you an additional $60,000 to invest. In October 2026, you cash out and repay your loan. In this case, leverage increased your annual investment returns by >2x.

Leveraged Investment Returns

$80,000 x 10% (S&P 500 Return) = $8,000

Cost to Borrow

$60,000 x 5% (Interest Rate on Loan)= $3,000

Net 1 Year Returns

$5,000 or 25% of initial investment

The Downside of Investment Loans

The choice of borrowing money to invest appears great on the surface. Unfortunately, it isn’t all sunshine and rainbows. The reason why is simple, the market doesn’t always do what we want it to do.

Just because the S&P 500 produces these returns on average doesn’t mean that it will continue to do so. In fact there have been multiple periods throughout history where the average returns were significantly below 10%. Between 2000-2012 we experienced the Dot-com bust and the Global Financial Crisis. The average total return (including dividends) over this 12 year period was 1.7%/year. In real (inflation-adjusted) terms, that is a 0% return which is why this period is referred to as a “lost decade”. To show the consequences of borrowing during this time lets use the following example:

Ex. You borrow 3:1 at a rate of 9% on $20,000 to invest in the S&P 500 in 2000. Since it is 3:1 the bank gives you an additional $60,000 to invest. In 2012, 12 years later, you decide to cash out and repay your loan. In this case, you would have lost your entire principle investment to service the interest costs on the loan.

Leveraged Investment Returns

$80,000 x 1.7%/year compounded = $17,935.79

Cost to Borrow

$60,000 x 9% (Interest Rate on Loan) x 12 years compounded= $40,548.47

Net 12 Year Returns

($22,612.68) or -113% Return

As the late great Charlie Munger said “There are three ways to go broke: liquor, ladies, and leverage”.

Investment Loans for Fixed Income

You may think that the solution to the problem of risk would be to buy stable asset classes such treasury or high grade corporate bonds, money market funds, or GIC’s. Unfortunately, at current rates these asset classes will not provide a significant enough reward to offset the cost of borrowing. As we said above, you can get an investment loan at 5-7% interest. Most of these asset classes currently only yield in the 3-4% range. In order for fixed income to actually work the interest rate on the investment loan has to be less than the projected yield on the investment.

To achieve a significant enough return you will have to look to high yield (ie. junk) bonds, or private credit. Both of which could be as risky, or more so than stocks depending on the market conditions.

When Investment Loans Work to Perfection

In 2020, Warren Buffett’s Berkshire Hathaway made a major investment in Japan’s five largest trading houses, buying about 5% stakes in each. To finance this move, Berkshire issued yen-denominated bonds in Japan rather than using U.S. dollars. This allowed him to borrow at ultra-low interest rates, roughly 0.17% to 1%, depending on the bond maturity. This strategy let Buffett take advantage of Japan’s cheap borrowing costs while gaining exposure to strong, diversified global businesses that pay solid dividends.

RRSP Loan

An RRSP loan is a short term loan that is used to make a lump-sum RRSP contribution. It is a variation of an investment loan. However, it provides a few unique benefits:

Accelerates savings

Boosts tax refund

Helps you catch up on contributions

Tax Refund

Any contributions to an RRSP can be used to offset taxes in the year of the contribution. They can also be carried forward to future years.

Ex. If you earn $100,000 in 2025 but also contributed $10,000 to an RRSP then your taxable income decreases to $90,000.

An RRSP loan allows you to reduce your immediate tax burden after a high earning year (ex. Secondary Property Sale). Since Canada has a progressive tax system, your marginal tax rate increases the more you earn. This means that the benefits of an RRSP are better for high earning individuals (or during a high earning year).

Ex. Imagine you live in Ontario and earn $100,000 in 2025. However, you also sold a family cottage for a capital gain of $400,000. You will be required to pay $120,624 in income tax. In order to offset the immediate tax burden you could take out a $32,490 RRSP loan (maximum 2025 limit) at 5% which you intend to pay back within the year. In this example:

A $32,490 RRSP contribution reduces your income taxes to $103,233. A total savings of $17,391.

Interest paid on the loan over the year is $867

Net Savings is $16,524

Catch Up On Contributions

An RRSP loan can also be an effective strategy to catch up or maximize contributions. Currently, you should have two updated amounts on your MyCRA account:

2025 Deduction Limit

Unused RRSP Contributions Available to Deduct in 2025

The total of these two numbers is what you are able to contribute to your RRSP and deduct from your tax return this year.

Many individuals will inevitably experience years where they are unable to contribute this amount. If your goal is wealth accumulation, and financial independence, this is not optimal. Instead, what you want to do is maximize your contributions, especially early on in your investing journey. This allows compound interest to do its work.

Another scenario where an RRSP loan could be useful is in the case of the two programs offered through the RRSP which are the Home Buyers Plan (HBP), and Lifelong Learning Plan (LLP). These programs allow you to withdraw funds from your RRSP to pay for an education or a home purchase. Both involve a mandatory repayment period. In order to maximize your long term returns, you can use an RRSP loan to repay the full amount immediately, and gradually pay off the loan over time.

RRSP Loan In Practice

Joe is 23 years old, living in Ontario, and he currently earns a salary of $100,000 as a plumber. He has earned the same salary since 2023, but has never contributed to an RRSP. He should have a $32,000 RRSP deduction limit in 2025, which consists of:

2025 Deduction Limit: $18,000 (18% of 2024 income)

Unused RRSP Contributions Available to Deduct in 2025: $18,000

His goal is to contribute this $32,000 to his RRSP as soon as possible. He will be investing the funds into a S&P 500 ETF which earns an average of 10%/year. He has two options:

Option 1

Take out a $32,000 RRSP Loan today at 5% interest and repay it over the next 24 months.

Tax Savings (2025) = $9,699

Earnings (2025-2026) = $6,720

Interest Paid on Loan = ($1,655)

Compounded Growth of Initial Investment (40 years)= $1,448,296

Option 2

Contribute $1333.33 per month for the next 24 months.

Tax Savings (2025-2026)= $10,796

Earnings (2025-2026) = $3,205

Interest Paid on Loan = $0 (No loan)

Compounded Growth of Initial Investment (40 years) = $1,316,817

As you can see from this example, the RRSP loan is the better of the two options. The initial growth in the investment throughout 2025-2026 makes up for the cost of borrowing, and the less tax deductions you receive. However, what is even more important is there is >$100,000 difference in the long term compounded returns from using the loan option.

Business Loan

A business loan is used to facilitate the initiation, continued operations, or growth of a business.

Since many businesses are very capital intensive (ex. construction) most people will need to take out a loan to start. This borrowing process often continues throughout the first few years of many businesses until they are able to build up enough cash to operate through profits alone. As they continue to grow, they may run into growth barriers (ex. More employees, equipment demands, etc) that require more cash then they have on hand which is when a loan will become useful again. This process often continues throughout most businesses' lifespan.

However, a business loan, like other forms of debt, can only be categorized as good if the funds are used for the right purposes. More specifically, to increase the profits of the business. A good business loan adds capacity, and/or income.

Ex. You start a lawn maintenance business using a riding lawn mower, a pickup truck and a trailer. You service all of your clients yourself, but you are fully booked. You’ve hit a growth ceiling. You go to the bank and take out a $25,000 loan at 7% interest to finance expansion. You use the funds for the following:

New Commercial Grade Lawn Mower- $10,000

Utility Trailer- $5,000

Truck Down Payment- $5,000

Marketing (Flyers, website, local ads)- $2,000

Working Capital buffer (fuel, payroll)- $3,000

The Dark Side of a Business Loan

Not all business loans are created equal though. A bad business loan adds debts without improving the businesses earning power. This occurs when you use the loan to:

Buy luxury or non-essential items (ex. Top of the line truck)

Use it just to keep a non profitable business afloat

Fund personal expenses (ie. Pay off your credit car, or renovate your home).

However, it could also be a bad loan if you overestimated the demand of the business by expanding too fast, or if the interest rate on the loan is too high (ex. Pay day loans) that it eats into profits.

The Bottom Line: When Does Debt Make Sense?

Good debt in Canada boils down to a simple test: Will this borrowing increase your net worth or earning potential more than it costs you?

If you're taking out a mortgage to buy a home that will appreciate, a student loan for a high-demand career, or a business loan that generates more revenue than the interest costs, you're using debt strategically.

But if you're borrowing at high interest rates to fund consumption, or taking on debt without a clear path to a positive return, you're likely headed for financial trouble.

Key Takeaways

Good debt builds wealth: mortgages, student loans in high-earning fields, business loans that add capacity, investment loans used carefully

Bad debt funds consumption: high-interest credit cards, payday loans, car loans for depreciating assets

The interest rate matters: Your return must exceed your borrowing cost

Risk matters too: Leveraged investments amplify both gains and losses

Before taking on any debt, ask yourself:

What is this money being used for?

What is the expected return or benefit?

What is the true cost of borrowing (interest + fees)?

Can I afford the payments if things don't go as planned?

Most wealthy Canadians use debt strategically. The difference between them and those drowning in debt isn't whether they borrow. Rather it's what they borrow for and whether they can manage the risk.

Use debt as a tool, not a crutch. When used wisely, it can accelerate your path to financial independence. When misused, it can set you back for years.

Related Posts:

[Budgeting for Beginners: How to Take Control of Your Money]

[How Much Emergency Fund Do You Need in Canada (2025 Guide)]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions

Citations

Canada Revenue Agency. (n.d.). CRA login services. Government of Canada. https://www.canada.ca/en/revenue-agency/services/e-services/cra-login-services.html

Ipsos. (n.d.). Six in ten Canadians who don't own a home have given up on owning. https://www.ipsos.com/en-ca/six-in-ten-canadians-who-dont-own-home-have-given-up-on-owning

Statistics Canada. (n.d.). Earnings and employment by field of study and level of highest certificate, diploma or degree, annual [Data table 98-10-0409-01]. https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=9810040901

The Canadian Real Estate Association. (n.d.). National price map. Canadian Housing Market Statistics. https://www.crea.ca/housing-market-stats/canadian-housing-market-stats/national-price-map/