Complete Guide to Canada Pension Plan (CPP) 2025: Maximize Your Benefits & Contributions

Learn how to maximize your Canada Pension Plan (CPP) benefits in 2025. Complete guide covering contribution rates, benefit calculations, when to start payments (age 60-70), and strategies to optimize your retirement income. Check your CPP estimates today.

INVESTING FOR BEGINNERSCANADIAN PENSION PLANCPP

8/18/202525 min read

Introduction

The Canadian Pension Plan (CPP) was set up by the Government of Canada in an effort to provide all Canadians with an opportunity to receive income in retirement. The goal of which is to avoid leaving any retiree behind by providing a minimum basic income source. It is not meant to be an individuals only source of income, but rather, makes up a component within a three pronged system:

Government Programs (CPP, OAS, & GIS)

Employer Pension Programs

Individual Savings/Investments

How CPP Contributions Work

Overview

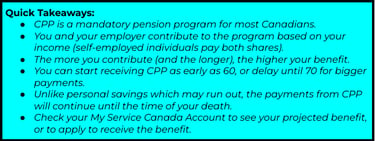

Every Canadian that is 18 years of age or older, and is earning an income of >$3,500/year is required to pay into the CPP. For employed individuals, the CPP will be remitted from their paycheck. Meanwhile, self-employed individuals will be required to pay the full annual amount on their tax return.

Note: The only exception is self-employed individuals that have incorporated. They have the option of receiving dividends, or a salary. In the case that they receive dividends, they will not be required to pay into the CPP. We will discuss more on this in a future blog post.

Basic Exemption

The first $3,500 of yearly earnings are exempt from contributions to CPP.

Contribution Rates

After the $3,500 minimum threshold, the contribution rates to CPP for 2025 are the following:

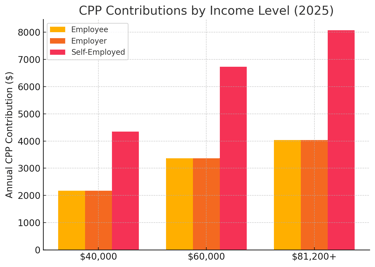

Employee: 5.95% of Gross Income

Employer contributes an additional 5.95%

Self-Employed: 11.9% of Gross Income

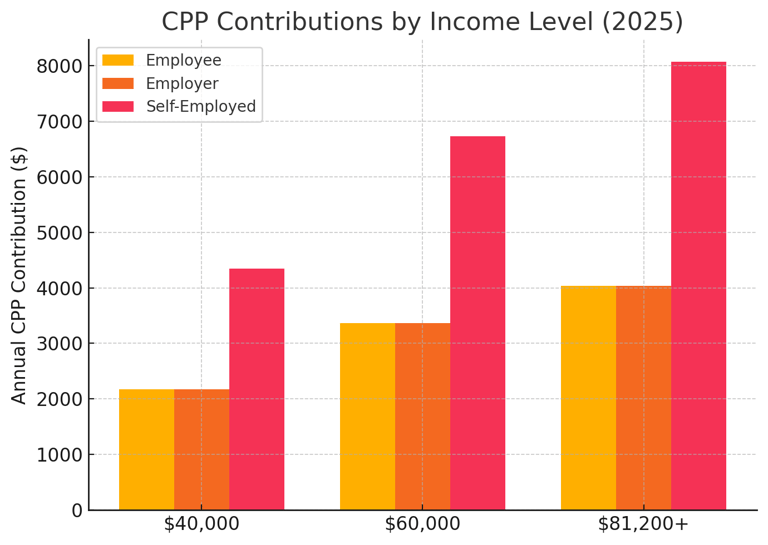

Ex. The CPP contributions of Cindy and Betty.

Cindy works as an administrative assistant earning a yearly salary of $60,000.

She will contribute $3,361.75, and her employer will contribute the remaining $3,361.75. A total contribution amount of $6,723.50.

Calculation: [$60,000 (Gross Income)- $3,500 (Basic Exemption)] x 0.0595 (5.95%) = $3,361.75

Betty is self-employed as a freelance writer, and she also earns $60,000 after deducting all her business expenses.

She will be required to pay the full $6,723.50 on her annual tax return, or 4 quarterly installments of $1,680.88.

Calculation: [$60,000 (Gross Income)- $3,500 (Basic Exemption)] x 0.119 (11.9%) = $6,723.50

Earnings Threshold

In order to deal with the rising cost of living, the maximum CPP contribution amount known as the maximum pensionable earnings (YMPE) increases each year. The amount of increase is determined by the Consumer Price Index (CPI) which measures the rate of inflation (ie. change in cost of living). In 2025, the YMPE is $71,300.

Enhanced CPP

In 2024, the CPP introduced an additional program known as CPP2. This program enables middle income Canadians earning above the YMPE to contribute more to the program, and as a result, earn more when they decide to withdraw.

This program was introduced in response to a trend that has gradually occurred over time. This trend is a reduction in the amount of defined benefit pension plan programs. Data from Statistics Canada showed that private sector defined benefit (DB) pension plans shrunk from 26% in 1989 down to 9% in 2019. This is due primarily to a shift towards defined contribution (DC) pension programs. Although both can be effective, the income received from a DC program is less guaranteed, and more variable than a traditional DB program.

There are two tiers to CPP contributions:

Base CPP

Applies to income between $3,500 and $71,300 (YMPE).

Employees contribute 5.95% of gross income, self-employed contribute 11.9% of gross income, as was mentioned above.

Enhanced CPP

Applies to income between $71,300 and $81,200 (YAMPE).

Employees contribute 4% of gross income, self-employed contribute 8% of gross income.

Ex. The CPP Contributions of Brian and Lucy

Brian works as a junior accountant earning a yearly salary of $78,000.

His contributions will include:

Base CPP: $4,034.10

Calculation: [$71,300 (YMPE)- $3,500 (Basic Exemption)] x 0.0595 (5.95%) = $4,034.10

Enhanced CPP: $268

Calculation [$78,000 (Salary) - $71,300 (YMPE) = $6,700 x 0.04 (4%) = $268

Lucy is self-employed as a website designer, and she also earns $78,000 after deducting all her business expenses.

She will be required to pay the full $8,068.20 on the basic CPP, and $536 on the enhanced CPP for a total of $8,604.20 on her annual tax return. She can also pay in 4 quarterly installments of $2,151.05.

Maximum Contribution

The maximum amount of contributions an individual can make to CPP in 2025 is:

Employee

Base CPP: $4,034.10

CPP2 Enhancements: $396.00

Maximum CPP Contribution: $4430.10

Self Employed

Base CPP: $8068.20

CPP2 Enhancements: $792.00

Total CPP Contribution: $8860.20

How Much Will You Receive (Know Your Numbers)

You can find out how much your payments are projected to be by logging into your My Service Canada Account. If you haven’t already, you will need to set-up an account.

In order to set-up an account you will need to provide the following information:

SIN number

First and Last Name

Date of Birth

Banking Information

And security questions

All future logins will require you to input your banking information. You may also be prompted to re-submit the answers to your security questions. You can set-up a multi-factor identification using text, email or phone calls.

Once logged in. you will go to the section titled “Canada Pension Plan” on your dashboard. In this section you will find options such as

Apply for CPP

View your payments

View your contributions

And View benefit estimates.

The “view benefit estimates” section will provide you with an estimation of how much you will receive if you withdraw the funds at 60, 65, or 70 years of age. Please note that these estimates will change over time, particularly if you are young, and haven’t built up years of contribution.

How CPP Benefits Are Calculated

After logging into your My Service Canada website, and finding out your estimated benefits, you may ask the question of how are they calculated? Well this depends on two factors:

How many years have you contributed?

How much did you contribute during those years?

At a minimum, you are required to make only one contribution, in order to be eligible for some CPP retirement pension (albeit likely very small).

In order to receive the maximum CPP benefits, you would be required to contribute to the program for 39-40 years at the maximum contribution threshold. If you recall from above, in order to contribute the maximum for 2025, you would need to earn $81,200.

Based on these amounts, you would need to be earning this income at 25 years of age, and experience an inflation adjusted increase in your income annually until the age of 65, in order to receive the maximum CPP benefits.

Drop out Provisions

CPP does however provide certain “drop-out” provisions, so that lower-earning or zero-earning months don’t drag down your average pensionable earnings.

These are the following:

General Drop-Out

CPP drops out 17% of your lowest-earning months from age 18 until you start withdrawing CPP.

This works out to ~8 years in a 47 year contributory period (ie. Between 18-65).

This is automatically applied to their calculation of your CPP benefits.

Child-Rearing Provision

You can drop months with zero or low earnings while raising your children.

You must be the primary caregiver of a child under the age of 7.

Requires that are eligible for Canada Child Benefit during those years.

You must apply for this provision on your My Service Canada Account or by filling out the appropriate forms.

This is in addition to the general drop-out.

These provisions are helpful considering that many individuals will take several years before they reach their peak earning years. Additionally, due to rising costs of child care many individuals are required to reduce their working hours while raising their kids.

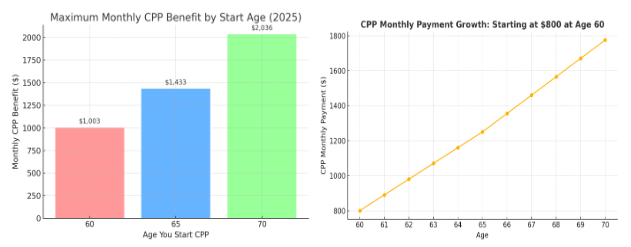

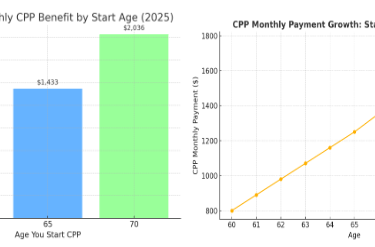

Maximum Benefit

Currently, the maximum monthly CPP payment at age 65 is ~$1,433 which results in an annual benefit of $17,197. The CPP is also inflation-indexed which means that it will increase in accordance with the consumer price index (CPI). Due to rising contribution thresholds, and the new enhanced CPP, younger individuals will be eligible to receive higher payments when they decide to start receiving CPP.

Beyond Retirement: CPP Survivor and Death Benefits

A concern that many retirees have regarding CPP is the notion that if you die, all the contributions you made throughout your life will have gone to waste. There are some flaws with this line of thought.

The first is the fact that the risk of reduced payout from early death is balanced by the potential of significant payout from a long life. If you somehow lived to 120 years old, the CPP will continue to pay you. The longer you live, the greater the chances that the payout is significantly higher than the sum total of all of your previous contributions.

The next issue is that it is not entirely true that all of the contributions you make will go to waste. In fact, there are certain benefits that your family members will be entitled to in the case of your death.

Death Benefit

The death benefit is a one time payment in order to help cover the costs of funeral expenses. Like CPP retirement benefits, it is calculated based on how much and how long the contributor paid into CPP. In order to be eligible the deceased will have had to make CPP contributions for at least 3 years. The maximum payment amount in 2025 is $2,500. The amount will be paid to the estate. If no estate exists it will be paid to one of the following:

Individual who paid for the funeral

Surviving spouse or common-law partner

Next of kin

Unfortunately, you will not be automatically enrolled into this program. There is an application process. This requires you to fill out a form called ISP1200- Application for a Canada Pension Plan Death Benefits. This form requires you to provide important information such as:

Proof of Death (Death certificate, funeral directors statement, etc).

SIN Number of Deceased

Date and Place of Death

Banking Information

Your Own SIN Number (and contact information if you are the applicant)

The form then can be submitted online via your My Service Canada Account if you are the executor of the estate.

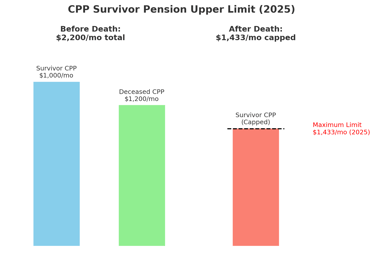

Survivors Pension (Spouse)

The “survivors pension” is paid out to a surviving partner. In order to qualify you must have been legally married, or in a common-law relationship at the time of death. Also, similar to the death benefit, the deceased must have contributed to the CPP for at least 3 years.

The amount received depends on your unique situation, however, here are some important numbers you should know:

If the surviving partner is under age 65 they will receive 37.5% of the deceased CPP retirement pension plus a flat-rate benefit.

The flat rate benefit is $232.18/month in 2025.

The maximum survivors benefit in 2025 is $721.48/month

If the surviving partner is age 65 or older, they will receive 60% of the deceased CPP retirement pension.

The maximum survivors benefit in 2025 is $1,008.30/month.

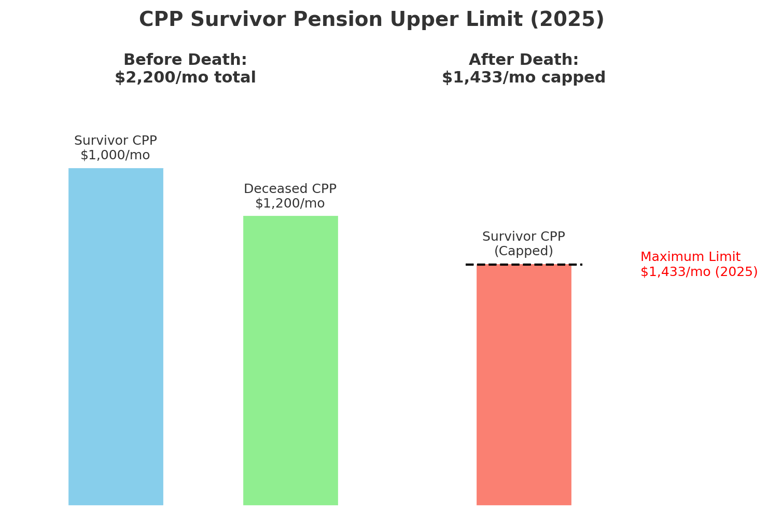

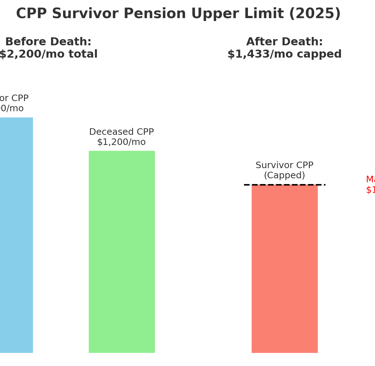

Upper Limit

There is one big caveat which is often a point of contention for many retirees. If the survivor is already receiving CPP retirement benefits themselves this limits the amount they could potentially receive from the deceased benefits. Currently, the total cannot exceed the maximum CPP retirement pension which is $1,433.00/month in 2025.

The frustration is justified because the surviving partner is already receiving a significant discount relative to what they received prior to the individual's death. By placing an upper threshold on the total amount received someone could experience a significant reduction in income.

This is also problematic considering that many individuals are still holding onto debts later in life (ex.mortgage). Their expenses unfortunately don’t just magically decrease when their partner passes.

Survivors Pension (Dependent Children)

The survivors pension can also be paid to a dependent child. The eligibility for what is considered a dependent child is the following:

Under age 18, or

Under age 25 and attending full time post-secondary school

The maximum amount in 2025 paid out to each child is $281.72/month.

The amount will be paid to the parent/guardian of the child if they are under the age of 18, or directly to the child if they are age 18 or older (under age 25) and attending school.

Similar to the death benefit, you will not be automatically enrolled into the survivors pension. Instead, you are required to fill out the following form ISP1300- Survivors Pension and Child(ren)’s Benefits Application. The following information at a minimum will be required:

Proof of Death (see above)

SIN Number of Deceased

SIN Number of Wife or Common Law Partner

Birth Certificate of Child (Dependent Child Benefit)

Proof of Relationship

Marriage Certificate

Birth Certificate (Dependent Child Benefit)

Proof of Attendance at School (if Dependent Child is 18-25)

Banking Information for Direct Deposit

CPP is Taxable

The CPP is a taxable pension.

The default option is for the individual to receive their gross benefit. This means that there will be no income tax withheld on each check. Instead you will be required to pay any taxes owed on your income tax return in April.

However, you can ask Service Canada to withhold federal and provincial income tax from each monthly payment. In order to do so you will need to fill out a Form ISP3520- Request for Voluntary Federal Income Tax Deduction. On this form, you will select the percentage (%), or dollar amount ($) you wish to be deducted from each payment. The form will then need to be mailed to a Service Canada office in your respective province.

Prior to income tax in April, usually before the end of February, you will be provided with a T4A(P)- Statement of Canada Pension Plan Benefits. This will appear on your My Service Canada Account. If you only receive retirement benefits, the total amount received will appear in Box 20. Taxes withheld throughout the year will appear in Box 30 as a credit against your total taxes owed.

When to Take CPP: Early vs. Standard vs. Delayed

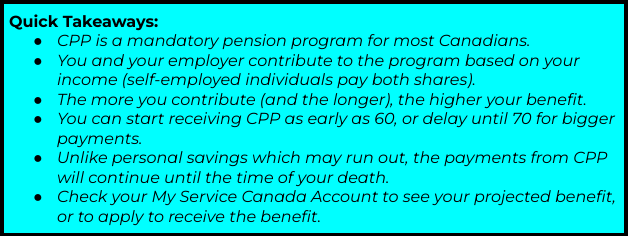

If you contributed to the CPP, you can start receiving payments as early as age 60.

Deciding when to start is complicated and depends on factors such as:

Employment Status

Income Sources in Retirement

Health Status

Life Expectancy & Family History

Tax Implications

Spousal/Partner Situation

Eligibility for other benefits

Because everyone’s circumstances are different, let’s first look strictly at the numbers.

How Payments Change by Age

It increases by 0.6% per month from 60-65 years of age.

This is a rate of return of 7.2%/year.

It increases by 0.7% per month from 65-70 years of age.

This is a rate of return of 8.4%/year.

The “Take it Early and Invest” Argument

A common belief among retirees is that it’s smarter to take CPP as soon as possible, and invest the money. This can sound appealing, but there are several pitfalls:

Tax Implications

If you are still working into your 60’s the CPP payments will be taxed at your higher employment tax rate.

This can be offset if you have an RRSP contribution room to shelter the income, though not everyone does.

Discipline Gap (Behaviour Risk)

Many people overestimate their ability to consistently save and invest the extra CPP income.

Without strong financial discipline, the money often gets spent instead of invested.

Market Risk

The S&P 500 has produced an average annual return of ~10% historically, which seems to outpace the guaranteed CPP increase.

However, markets are volatile. If you retire during a bear market, the value of your investments could be much lower than expected. Unfortunately, this may occur right when you need to start withdrawals.

CPP, by contrast, is guaranteed, inflation-protected, and lasts for life.

Death Risk

Another major concern amongst retirees is the potential risk of death.

Despite misinformation, your partner or child will receive the survivors benefit and pension regardless of whether or not you have started withdrawing CPP. Provided you contributed to the program they will be entitled to these benefits. However, you will lose out on prior years earnings if you choose to delay the benefits after age 60.

Your risk of an early death depends on a variety of factors including medical history, genetics, health behaviours, etc. With all of this considered, it is important to note the following:

The average life expectancy in Canada is 83 years of age.

Despite a minor drop during the COVID pandemic it has grown steadily from 68 years of age in 1950.

Statistics Canada projects life expectancy in 2068 to grow to 90 years of age for women, and 86.9 years of age for men.

Doesn’t account for any medical or scientific breakthroughs.

Summary

Based on this information, the answer will depend on where you fall on this spectrum when you turn 60 years of age:

Highest Return, High Risk (ie. Market Volatility)

Take CPP payments at 60, and invest in S&P500 index ETF.

High Return, Moderate Risk (ie. Death)

Wait until 70 years of age to take CPP Payments

Moderate Return, Low to Moderate Risk (ie. Death)

Wait until 65 years of age to take CPP payments

Low Return, Low Risk

Take the CPP payments at 60 years of age

Conclusion

The Canada Pension Plan is a cornerstone of retirement income for Canadians, providing inflation-protected, lifelong benefits. By understanding how contributions work, what factors affect your benefit amount, and when it might be best to start receiving payments, you can make more informed decisions that align with your financial goals. Whether you choose to take CPP early, at the standard age, or delay it for higher payments, the key is to plan ahead. Check your My Service Canada Account regularly, keep track of your contributions, and integrate CPP into your broader retirement strategy. Thoughtful planning today can help ensure a more secure and comfortable retirement tomorrow.

If you liked this post you may also like:

[RRSP Guide 2025: Canada's Powerful Retirement Savings Tool]

[4 Financial Lessons Traveling Taught Me About Money and Happiness]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Government of Canada. (2024, January 1). Canada Pension Plan – How much could you receive. https://www.canada.ca/en/services/benefits/publicpensions/cpp/retirement-income.html

Government of Canada. (2024, January 1). Canada Pension Plan – Contributions. https://www.canada.ca/en/services/benefits/publicpensions/cpp/contributions.html

Government of Canada. (2024, January 1). My Service Canada Account. https://www.canada.ca/en/employment-social-development/services/my-account.html

Government of Canada. (2024). Child-rearing provision – Canada Pension Plan. https://www.canada.ca/en/services/benefits/publicpensions/cpp/child-rearing.html

Government of Canada. (2024). Application for a Canada Pension Plan Death Benefit (ISP1200). https://www.canada.ca/en/services/benefits/publicpensions/cpp/apply.html

Government of Canada. (2024). Survivor’s pension and children’s benefits (ISP1300). https://www.canada.ca/en/services/benefits/publicpensions/cpp/survivor-pension.html

Government of Canada. (2024). Request for voluntary federal income tax deduction (ISP3520). https://www.canada.ca/en/services/benefits/publicpensions/cpp/tax.html

Statistics Canada. (2020, March 11). Pension plans in Canada, as of January 1, 2019. https://www150.statcan.gc.ca/n1/daily-quotidien/200311/dq200311a-eng.htm

Statistics Canada. (2022). Life tables, Canada, provinces and territories. https://www150.statcan.gc.ca/n1/pub/84-537-x/84-537-x2022001-eng.htm

Statistics Canada. (2019). Population projections for Canada, provinces and territories, 2018 to 2068. https://www150.statcan.gc.ca/n1/pub/91-520-x/91-520-x2019001-eng.htm

Introduction

The Canadian Pension Plan (CPP) was set up by the Government of Canada in an effort to provide all Canadians with an opportunity to receive income in retirement. The goal of which is to avoid leaving any retiree behind by providing a minimum basic income source. It is not meant to be an individuals only source of income, but rather, makes up a component within a three pronged system:

Government Programs (CPP, OAS, & GIS)

Employer Pension Programs

Individual Savings/Investments

How CPP Contributions Work

Overview

Every Canadian that is 18 years of age or older, and is earning an income of >$3,500/year is required to pay into the CPP. For employed individuals, the CPP will be remitted from their paycheck. Meanwhile, self-employed individuals will be required to pay the full annual amount on their tax return.

Note: The only exception is self-employed individuals that have incorporated. They have the option of receiving dividends, or a salary. In the case that they receive dividends, they will not be required to pay into the CPP. We will discuss more on this in a future blog post.

Basic Exemption

The first $3,500 of yearly earnings are exempt from contributions to CPP.

Contribution Rates

After the $3,500 minimum threshold, the contribution rates to CPP for 2025 are the following:

Employee: 5.95% of Gross Income

Employer contributes an additional 5.95%

Self-Employed: 11.9% of Gross Income

Ex. The CPP contributions of Cindy and Betty.

Cindy works as an administrative assistant earning a yearly salary of $60,000.

She will contribute $3,361.75, and her employer will contribute the remaining $3,361.75. A total contribution amount of $6,723.50.

Calculation: [$60,000 (Gross Income)- $3,500 (Basic Exemption)] x 0.0595 (5.95%) = $3,361.75

Betty is self-employed as a freelance writer, and she also earns $60,000 after deducting all her business expenses.

She will be required to pay the full $6,723.50 on her annual tax return, or 4 quarterly installments of $1,680.88.

Calculation: [$60,000 (Gross Income)- $3,500 (Basic Exemption)] x 0.119 (11.9%) = $6,723.50

Earnings Threshold

In order to deal with the rising cost of living, the maximum CPP contribution amount known as the maximum pensionable earnings (YMPE) increases each year. The amount of increase is determined by the Consumer Price Index (CPI) which measures the rate of inflation (ie. change in cost of living). In 2025, the YMPE is $71,300.

Enhanced CPP

In 2024, the CPP introduced an additional program known as CPP2. This program enables middle income Canadians earning above the YMPE to contribute more to the program, and as a result, earn more when they decide to withdraw.

This program was introduced in response to a trend that has gradually occurred over time. This trend is a reduction in the amount of defined benefit pension plan programs. Data from Statistics Canada showed that private sector defined benefit (DB) pension plans shrunk from 26% in 1989 down to 9% in 2019. This is due primarily to a shift towards defined contribution (DC) pension programs. Although both can be effective, the income received from a DC program is less guaranteed, and more variable than a traditional DB program.

There are two tiers to CPP contributions:

Base CPP

Applies to income between $3,500 and $71,300 (YMPE).

Employees contribute 5.95% of gross income, self-employed contribute 11.9% of gross income, as was mentioned above.

Enhanced CPP

Applies to income between $71,300 and $81,200 (YAMPE).

Employees contribute 4% of gross income, self-employed contribute 8% of gross income.

Ex. The CPP Contributions of Brian and Lucy

Brian works as a junior accountant earning a yearly salary of $78,000.

His contributions will include:

Base CPP: $4,034.10

Calculation: [$71,300 (YMPE)- $3,500 (Basic Exemption)] x 0.0595 (5.95%) = $4,034.10

Enhanced CPP: $268

Calculation [$78,000 (Salary) - $71,300 (YMPE) = $6,700 x 0.04 (4%) = $268

Lucy is self-employed as a website designer, and she also earns $78,000 after deducting all her business expenses.

She will be required to pay the full $8,068.20 on the basic CPP, and $536 on the enhanced CPP for a total of $8,604.20 on her annual tax return. She can also pay in 4 quarterly installments of $2,151.05.

Maximum Contribution

The maximum amount of contributions an individual can make to CPP in 2025 is:

Employee

Base CPP: $4,034.10

CPP2 Enhancements: $396.00

Maximum CPP Contribution: $4430.10

Self Employed

Base CPP: $8068.20

CPP2 Enhancements: $792.00

Total CPP Contribution: $8860.20

How Much Will You Receive (Know Your Numbers)

You can find out how much your payments are projected to be by logging into your My Service Canada Account. If you haven’t already, you will need to set-up an account.

In order to set-up an account you will need to provide the following information:

SIN number

First and Last Name

Date of Birth

Banking Information

And security questions

All future logins will require you to input your banking information. You may also be prompted to re-submit the answers to your security questions. You can set-up a multi-factor identification using text, email or phone calls.

Once logged in. you will go to the section titled “Canada Pension Plan” on your dashboard. In this section you will find options such as

Apply for CPP

View your payments

View your contributions

And View benefit estimates.

The “view benefit estimates” section will provide you with an estimation of how much you will receive if you withdraw the funds at 60, 65, or 70 years of age. Please note that these estimates will change over time, particularly if you are young, and haven’t built up years of contribution.

How CPP Benefits Are Calculated

After logging into your My Service Canada website, and finding out your estimated benefits, you may ask the question of how are they calculated? Well this depends on two factors:

How many years have you contributed?

How much did you contribute during those years?

At a minimum, you are required to make only one contribution, in order to be eligible for some CPP retirement pension (albeit likely very small).

In order to receive the maximum CPP benefits, you would be required to contribute to the program for 39-40 years at the maximum contribution threshold. If you recall from above, in order to contribute the maximum for 2025, you would need to earn $81,200.

Based on these amounts, you would need to be earning this income at 25 years of age, and experience an inflation adjusted increase in your income annually until the age of 65, in order to receive the maximum CPP benefits.

Drop out Provisions

CPP does however provide certain “drop-out” provisions, so that lower-earning or zero-earning months don’t drag down your average pensionable earnings.

These are the following:

General Drop-Out

CPP drops out 17% of your lowest-earning months from age 18 until you start withdrawing CPP.

This works out to ~8 years in a 47 year contributory period (ie. Between 18-65).

This is automatically applied to their calculation of your CPP benefits.

Child-Rearing Provision

You can drop months with zero or low earnings while raising your children.

You must be the primary caregiver of a child under the age of 7.

Requires that are eligible for Canada Child Benefit during those years.

You must apply for this provision on your My Service Canada Account or by filling out the appropriate forms.

This is in addition to the general drop-out.

These provisions are helpful considering that many individuals will take several years before they reach their peak earning years. Additionally, due to rising costs of child care many individuals are required to reduce their working hours while raising their kids.

Maximum Benefit

Currently, the maximum monthly CPP payment at age 65 is ~$1,433 which results in an annual benefit of $17,197. The CPP is also inflation-indexed which means that it will increase in accordance with the consumer price index (CPI). Due to rising contribution thresholds, and the new enhanced CPP, younger individuals will be eligible to receive higher payments when they decide to start receiving CPP.

Beyond Retirement: CPP Survivor and Death Benefits

A concern that many retirees have regarding CPP is the notion that if you die, all the contributions you made throughout your life will have gone to waste. There are some flaws with this line of thought.

The first is the fact that the risk of reduced payout from early death is balanced by the potential of significant payout from a long life. If you somehow lived to 120 years old, the CPP will continue to pay you. The longer you live, the greater the chances that the payout is significantly higher than the sum total of all of your previous contributions.

The next issue is that it is not entirely true that all of the contributions you make will go to waste. In fact, there are certain benefits that your family members will be entitled to in the case of your death.

Death Benefit

The death benefit is a one time payment in order to help cover the costs of funeral expenses. Like CPP retirement benefits, it is calculated based on how much and how long the contributor paid into CPP. In order to be eligible the deceased will have had to make CPP contributions for at least 3 years. The maximum payment amount in 2025 is $2,500. The amount will be paid to the estate. If no estate exists it will be paid to one of the following:

Individual who paid for the funeral

Surviving spouse or common-law partner

Next of kin

Unfortunately, you will not be automatically enrolled into this program. There is an application process. This requires you to fill out a form called ISP1200- Application for a Canada Pension Plan Death Benefits. This form requires you to provide important information such as:

Proof of Death (Death certificate, funeral directors statement, etc).

SIN Number of Deceased

Date and Place of Death

Banking Information

Your Own SIN Number (and contact information if you are the applicant)

The form then can be submitted online via your My Service Canada Account if you are the executor of the estate.

Survivors Pension (Spouse)

The “survivors pension” is paid out to a surviving partner. In order to qualify you must have been legally married, or in a common-law relationship at the time of death. Also, similar to the death benefit, the deceased must have contributed to the CPP for at least 3 years.

The amount received depends on your unique situation, however, here are some important numbers you should know:

If the surviving partner is under age 65 they will receive 37.5% of the deceased CPP retirement pension plus a flat-rate benefit.

The flat rate benefit is $232.18/month in 2025.

The maximum survivors benefit in 2025 is $721.48/month

If the surviving partner is age 65 or older, they will receive 60% of the deceased CPP retirement pension.

The maximum survivors benefit in 2025 is $1,008.30/month.

Upper Limit

There is one big caveat which is often a point of contention for many retirees. If the survivor is already receiving CPP retirement benefits themselves this limits the amount they could potentially receive from the deceased benefits. Currently, the total cannot exceed the maximum CPP retirement pension which is $1,433.00/month in 2025.

The frustration is justified because the surviving partner is already receiving a significant discount relative to what they received prior to the individual's death. By placing an upper threshold on the total amount received someone could experience a significant reduction in income.

This is also problematic considering that many individuals are still holding onto debts later in life (ex.mortgage). Their expenses unfortunately don’t just magically decrease when their partner passes.

Survivors Pension (Dependent Children)

The survivors pension can also be paid to a dependent child. The eligibility for what is considered a dependent child is the following:

Under age 18, or

Under age 25 and attending full time post-secondary school

The maximum amount in 2025 paid out to each child is $281.72/month.

The amount will be paid to the parent/guardian of the child if they are under the age of 18, or directly to the child if they are age 18 or older (under age 25) and attending school.

Similar to the death benefit, you will not be automatically enrolled into the survivors pension. Instead, you are required to fill out the following form ISP1300- Survivors Pension and Child(ren)’s Benefits Application. The following information at a minimum will be required:

Proof of Death (see above)

SIN Number of Deceased

SIN Number of Wife or Common Law Partner

Birth Certificate of Child (Dependent Child Benefit)

Proof of Relationship

Marriage Certificate

Birth Certificate (Dependent Child Benefit)

Proof of Attendance at School (if Dependent Child is 18-25)

Banking Information for Direct Deposit

CPP is Taxable

The CPP is a taxable pension.

The default option is for the individual to receive their gross benefit. This means that there will be no income tax withheld on each check. Instead you will be required to pay any taxes owed on your income tax return in April.

However, you can ask Service Canada to withhold federal and provincial income tax from each monthly payment. In order to do so you will need to fill out a Form ISP3520- Request for Voluntary Federal Income Tax Deduction. On this form, you will select the percentage (%), or dollar amount ($) you wish to be deducted from each payment. The form will then need to be mailed to a Service Canada office in your respective province.

Prior to income tax in April, usually before the end of February, you will be provided with a T4A(P)- Statement of Canada Pension Plan Benefits. This will appear on your My Service Canada Account. If you only receive retirement benefits, the total amount received will appear in Box 20. Taxes withheld throughout the year will appear in Box 30 as a credit against your total taxes owed.

When to Take CPP: Early vs. Standard vs. Delayed

If you contributed to the CPP, you can start receiving payments as early as age 60.

Deciding when to start is complicated and depends on factors such as:

Employment Status

Income Sources in Retirement

Health Status

Life Expectancy & Family History

Tax Implications

Spousal/Partner Situation

Eligibility for other benefits

Because everyone’s circumstances are different, let’s first look strictly at the numbers.

How Payments Change by Age

It increases by 0.6% per month from 60-65 years of age.

This is a rate of return of 7.2%/year.

It increases by 0.7% per month from 65-70 years of age.

This is a rate of return of 8.4%/year.

The “Take it Early and Invest” Argument

A common belief among retirees is that it’s smarter to take CPP as soon as possible, and invest the money. This can sound appealing, but there are several pitfalls:

Tax Implications

If you are still working into your 60’s the CPP payments will be taxed at your higher employment tax rate.

This can be offset if you have an RRSP contribution room to shelter the income, though not everyone does.

Discipline Gap (Behaviour Risk)

Many people overestimate their ability to consistently save and invest the extra CPP income.

Without strong financial discipline, the money often gets spent instead of invested.

Market Risk

The S&P 500 has produced an average annual return of ~10% historically, which seems to outpace the guaranteed CPP increase.

However, markets are volatile. If you retire during a bear market, the value of your investments could be much lower than expected. Unfortunately, this may occur right when you need to start withdrawals.

CPP, by contrast, is guaranteed, inflation-protected, and lasts for life.

Death Risk

Another major concern amongst retirees is the potential risk of death.

Despite misinformation, your partner or child will receive the survivors benefit and pension regardless of whether or not you have started withdrawing CPP. Provided you contributed to the program they will be entitled to these benefits. However, you will lose out on prior years earnings if you choose to delay the benefits after age 60.

Your risk of an early death depends on a variety of factors including medical history, genetics, health behaviours, etc. With all of this considered, it is important to note the following:

The average life expectancy in Canada is 83 years of age.

Despite a minor drop during the COVID pandemic it has grown steadily from 68 years of age in 1950.

Statistics Canada projects life expectancy in 2068 to grow to 90 years of age for women, and 86.9 years of age for men.

Doesn’t account for any medical or scientific breakthroughs.

Summary

Based on this information, the answer will depend on where you fall on this spectrum when you turn 60 years of age:

Highest Return, High Risk (ie. Market Volatility)

Take CPP payments at 60, and invest in S&P500 index ETF.

High Return, Moderate Risk (ie. Death)

Wait until 70 years of age to take CPP Payments

Moderate Return, Low to Moderate Risk (ie. Death)

Wait until 65 years of age to take CPP payments

Low Return, Low Risk

Take the CPP payments at 60 years of age

Conclusion

The Canada Pension Plan is a cornerstone of retirement income for Canadians, providing inflation-protected, lifelong benefits. By understanding how contributions work, what factors affect your benefit amount, and when it might be best to start receiving payments, you can make more informed decisions that align with your financial goals. Whether you choose to take CPP early, at the standard age, or delay it for higher payments, the key is to plan ahead. Check your My Service Canada Account regularly, keep track of your contributions, and integrate CPP into your broader retirement strategy. Thoughtful planning today can help ensure a more secure and comfortable retirement tomorrow.

If you liked this post you may also like:

[RRSP Guide 2025: Canada's Powerful Retirement Savings Tool]

[4 Financial Lessons Traveling Taught Me About Money and Happiness]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Government of Canada. (2024, January 1). Canada Pension Plan – How much could you receive. https://www.canada.ca/en/services/benefits/publicpensions/cpp/retirement-income.html

Government of Canada. (2024, January 1). Canada Pension Plan – Contributions. https://www.canada.ca/en/services/benefits/publicpensions/cpp/contributions.html

Government of Canada. (2024, January 1). My Service Canada Account. https://www.canada.ca/en/employment-social-development/services/my-account.html

Government of Canada. (2024). Child-rearing provision – Canada Pension Plan. https://www.canada.ca/en/services/benefits/publicpensions/cpp/child-rearing.html

Government of Canada. (2024). Application for a Canada Pension Plan Death Benefit (ISP1200). https://www.canada.ca/en/services/benefits/publicpensions/cpp/apply.html

Government of Canada. (2024). Survivor’s pension and children’s benefits (ISP1300). https://www.canada.ca/en/services/benefits/publicpensions/cpp/survivor-pension.html

Government of Canada. (2024). Request for voluntary federal income tax deduction (ISP3520). https://www.canada.ca/en/services/benefits/publicpensions/cpp/tax.html

Statistics Canada. (2020, March 11). Pension plans in Canada, as of January 1, 2019. https://www150.statcan.gc.ca/n1/daily-quotidien/200311/dq200311a-eng.htm

Statistics Canada. (2022). Life tables, Canada, provinces and territories. https://www150.statcan.gc.ca/n1/pub/84-537-x/84-537-x2022001-eng.htm

Statistics Canada. (2019). Population projections for Canada, provinces and territories, 2018 to 2068. https://www150.statcan.gc.ca/n1/pub/91-520-x/91-520-x2019001-eng.htm