Old Age Security (OAS) in Canada 2025: Eligibility, Payments, and Clawback Explained

Learn about Old Age Security (OAS) in Canada for 2025, including eligibility, payments, deferral options, and the OAS clawback explained clearly.

INVESTING FOR BEGINNERSRETIREMENTOLD AGE SECURITYOAS

8/25/202523 min read

Introduction

OAS is one of the most important retirement programs in Canada, but it's also one of the most misunderstood. Many people approaching retirement have no idea how much they'll receive, when they're eligible, or what factors affect their payments. The rules around residency requirements, clawbacks, and payment calculations can seem overwhelming at first glance. This guide breaks down everything you need to know about OAS in 2025 - from basic eligibility to payment amounts to tax implications. Understanding these fundamentals is the first step toward making smart decisions about your retirement income.

What is Old Age Security (OAS)?

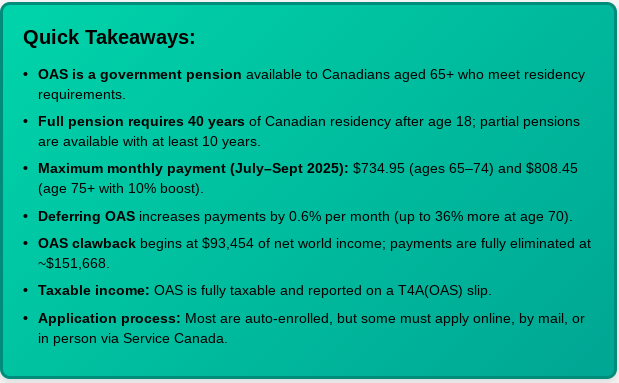

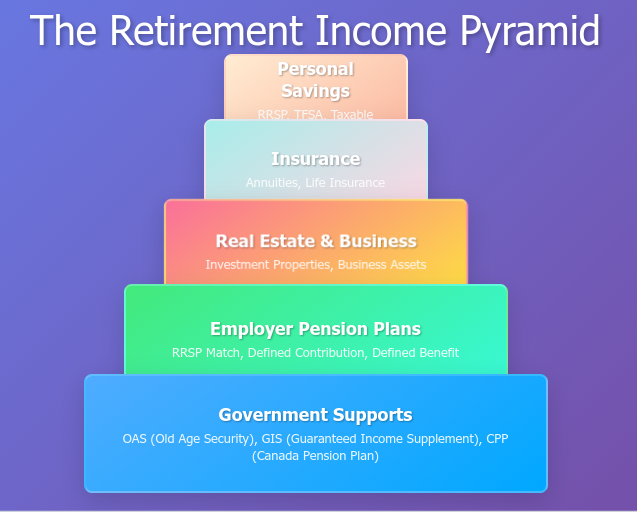

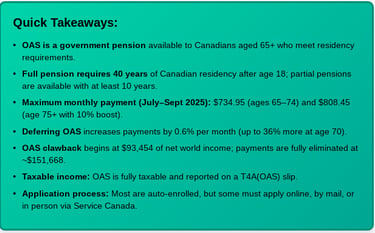

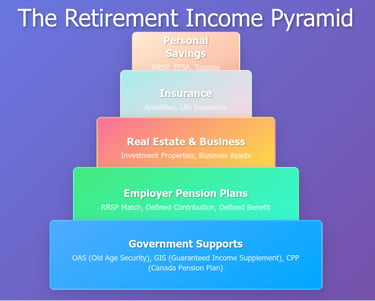

The Old Age Security (OAS) is a government pension that was created in order to assist seniors (age 65 or older) in meeting their basic income demands. The OAS is not meant to be an individuals only source of income in retirement. Instead it provides the foundation for what we like to call The Retirement Income Pyramid.

The OAS is funded by general tax revenue. You as a Canadian taxpayer contribute to the program indirectly by the taxes you pay throughout your daily life. The Canadian Pension Plan (CPP), on the other hand, is funded by a combination of employee, and employer contributions.

Unlike the CPP, you are not required to be employed in order to receive OAS payments. However, there are specific residency requirements that need to be met in order to be eligible for the program.

Eligibility Requirements

In order to be eligible for OAS, you need to meet the following criteria:

Be age 65 or older

Have lived in Canada for a minimum of 10 years after the age of 18

However, the 10 year minimum will only provide you with a partial OAS pension. In order to be eligible for the full pension you must have lived in Canada for 40 years after the age of 18.

Partial OAS Pension Calculation

If you meet the minimum residency requirements of 10 years, but not the maximum of 40 years you’re pensionable benefits will be calculated using the following equation:

# of years of Canadian Residency x 2.5 (1/40th) = % OAS Maximum

Ex. Mandy lived in Toronto until the age of 18. She decided to go to school at Trinity College in Dublin for Economics. After which point she found a corporate job in Ireland where she worked until age 30. She then returned back to Toronto to live closer to family as she raised her kids. She retired at age 65, and collected her OAS. In this case she lived in Canada for a total of 35 years after age 18. She will receive 87.5% of the OAS maximum benefits.

35 Years x 2.5 = 87.5% of OAS Maximum

Living Abroad and Receiving Full OAS

In some cases you may be eligible to receive the full benefits from OAS despite living abroad. The two most common exceptions would be:

Living in a country with a social security agreement with Canada

Canadian Military or Government Service

There are currently 50 countries that have a social security agreement with Canada including USA, Australia, Germany, Japan, etc. For a comprehensive list of those countries you can go to the Government of Canada website here. These countries allow you to combine years of residency when calculating OAS payments. The purpose of this exemption is to avoid cases whereby someone paid into a social security program internationally but is unable to receive the benefits.

In the case of Canadian military or government service, your time internationally may count as Canadian residency. Additionally, your spouse or partner who lived with you outside of Canada may also have that period count as Canadian residency. However, you must meet the following criteria:

You have been employed by

Canadian Government

Canadian Armed Forces.

You must maintain ties to Canada while abroad

Paying Canadian income taxes

Keeping Canada bank accounts, property, or dependents in Canada.

How Much is OAS? (2025 Numbers)

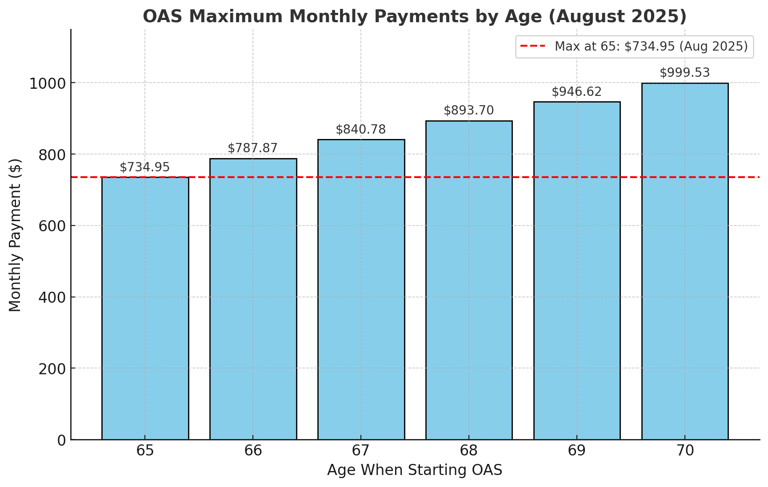

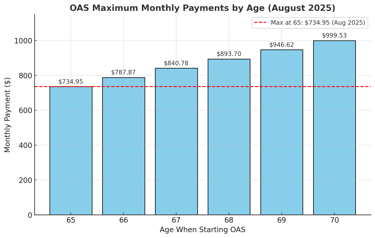

The maximum OAS payment for July-September 2025 is the following:

Age 65-74

$734.95/month or $8,795.40/year

0.6% increase for each month of deferral after age 65.

Both OAS and CPP are inflation adjusted according to the Consumer Price Index (CPI). The difference between the two programs though is that CPP adjustments are calculated annually. However, OAS is adjusted quarterly. So the maximum amounts noted above will change in October 2025. For more updated amounts you can go directly to the Government of Canada website here.

Example 1: John is age 65 and plans to start receiving his OAS payments in August 2025. He worked abroad as a pilot for most of his life. He only lived in Canada for a total of 20 years after his 18th birthday. Since the residency demands for OAS require 40 years of living in Canada, he only has 50% of the required residency time. His estimated monthly benefit should be the following:

Current Maximum OAS Benefit ($734.95) x 0.5 (50% of residency demands for maximum benefits) = $367.48

Example 2: Mark is age 65 and plans to start receiving OAS payments in August 2025. He served in the Canadian Armed Forces (CAF) as an aviation technician. He only lived in Canada for 30 years. However, he served abroad for the CAF for 10 years. During that time he owned a condo in Canada, and paid Canadian income taxes. He is eligible for the full benefit. His estimated monthly benefit is the following:

Current Maximum OAS Benefit ($734.95) x 1.0 (100% of residency demands for maximum benefits) = $734.95

Deferring OAS

The default age for starting to draw your OAS payments is age 65. Afterwards, you will be auto-enrolled into the program, and start receiving payments. However, you have the option of applying to defer your OAS payments. This can be performed on your My Service Canada Account.

Why would you want to defer payments?

For every month that you defer your OAS payments after age 65 the payment will increase by 0.6%. This results in an annual increase of 7.2%. If you defer until the age of 70 it would result in a 36% increase in payments. This increase will be applied to all future payments until the time of your death. Unlike investments, this is a guaranteed increase in payment not susceptible to volatility.

Example: Fred has his 65th birthday in 6 months. He is debating whether or not to apply for a OAS deferral. If he does he plans to wait until age 70 to start drawing OAS. He has lived in Canada for over 40 years since his 18th birthday so he should qualify for the entire OAS benefit. If he starts receiving his payments at age 65 he will receive $734.95 + any quarterly inflation adjustments for the rest of his life. However, if he delays until age 70 he will receive $999.53 + quarterly inflation adjustments for the rest of his life.

$734.95 (OAS Maximum Benefit at Age 65) x 1.36 (36% Increase in Payments from deferral)= $999.53 (OAS Maximum Benefit at Age 70)

Payment Boost at Age 75

In July 2022, the federal government introduced a permanent boost to OAS payments of 10% for everyone aged 75 and older. This is applied regardless of whether you started receiving OAS payments at age 65, or deferred until age 70.

The maximum OAS payment for July-September 2025 is the following:

Age 75

No Deferral of OAS Payments from Age 65 to Age 70

$808.45/month or $9,701.40

Deferred OAS Payments until age 70

$1099.48/month or $13,193.80

Example: Jennifer had her 75th birthday this month.

She started receiving OAS payments at age 65.

She had only 35 years of Canadian residency prior to receiving her OAS payments.

Prior to her birthday she received OAS payments of $643.08/month.

Current Maximum OAS Benefit ($734.95) x 0.875 (87.5% of residency demands for maximum benefits) = $643.08

Now that she is age 75 she will receive an additional 10% boost in payments .

$643.08 (OAS Payment prior to Age 75) x 1.10 (10% boost in payment at age 75) = $707.39 (OAS Payment at Age 75 after the 10% boost)

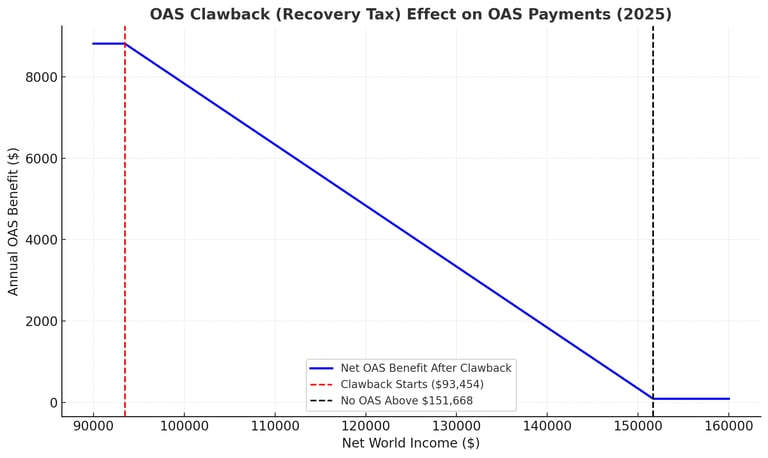

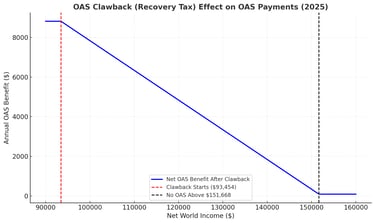

OAS Clawback (OAS Recovery Tax)

Unlike CPP, the OAS is subjected to something called a Recovery Tax, often referred to as a “OAS clawback”. This is an additional tax applied on high income seniors.

The purpose of the OAS clawback is to create income equity amongst retirees. The program is meant for those in most need of the funds which are low to middle income earners. Generally speaking high income earners don’t rely on the funds for survival so the payments are reduced after certain income thresholds.

Income Threshold

You will be subjected to an OAS clawback for every $1 you earn above $93,454 per year. It is important to note that the OAS is calculated based on an individuals net world income, not household income. So in theory, provided both you and your spouse make below the individual threshold you could earn a family income of $186,908.

What is included in net world income?

The CRA defines net world income as your “Net Income Before Adjustments” on a tax return. It includes things like:

Employment Income

Pension Income (OAS, CPP, RRSP/RRIF withdrawals, private pensions, etc)

Rental Income

Business Income

Non-registered Investment Income (Interest, capital gains, dividends)

Capital Gains from secondary property

Worldwide Income

Since their are several types of income sources considered in this calculation tax planning is very important. By tax planning It helps you to avoid accidentally receiving an “OAS clawback” due to a poorly timed asset sale, or overlap between employment and OAS payments.

How is the OAS Clawback Calculated

The OAS clawback is not a strict cut-off point at the income threshold. Instead the payments are gradually reduced until you reach the upper threshold of $151,668 of yearly income. At which point you will no longer be eligible to receive any OAS payments.

For every $1 you receive above the minimum threshold of $93,454, you will be required to repay 15 cents (15%) for the OAS clawback.

Ex. Jennifer earns a net world income of $115,000 in 2025. This includes $90,000 salary from her job as a district manager, $15,000 of taxable interest income from investments, and $10,000 of rental income from her secondary property. Her OAS clawback will be $3,231.90 for the year 2025. This is the calculation:

Excess over minimum income threshold: $115,000 - $93,454 = $21,546

OAS Recovery Tax or clawback: $21,546 x 0.15 (15%) = $3,231.90

Does the OAS Clawback threshold increase if I defer until 70?

No, the OAS clawback threshold does not increase if you defer your OAS payments from age 65 to age 70.

However, if you recall earlier in this post there is a 10% OAS payment boost that occurs at age 75. After this is introduced the OAS clawback maximum threshold increases from $151,668 to $157,490.

OAS Clawback- Point of Contention

The “OAS clawback” is questionable at best, and it is often a point of contention amongst retirees.

In order to qualify for the OAS program you need 10+ years of Canadian residency. In many cases, individuals have lived in the country for 40 + years. One could argue that they have paid significantly into the tax system (ie. income taxes, sales taxes, property taxes, etc). Actually, all things being equal the higher income earner will have paid more into the tax system throughout their life than lower income individuals.

The marginal tax rate of an individual living in Ontario with a net world income of $93,454 is ~30%. The “OAS clawback” or recovery tax is an additional 15%. This means that a retiree is effectively being taxed at 45% for every $1 of earnings above this income threshold.

However, the program is meant to create equity, and prevent poverty in retirement. This is accomplished through raising the minimum income floor for those who need it. Like our tax system, the more you may the more you pay in. In this case the more you make, the more they take away.

How to Apply for OAS

Provided you are a Canadian Citizen, 65 years old, and meet the minimum requirements of 10 years of residency you should be automatically enrolled into receiving OAS payments.

Service Canada will send you a letter the month after you turn 64 telling you that you either that you will be auto-enrolled, or you need to apply. If you don’t receive a letter by age 64, you should contact Service Canada to confirm if you need to apply.

You can apply for OAS as early as 11 months before your 65th birthday. If you want to defer OAS (up to age 70), you should indicate that in your application. There are three ways to apply for OAS:

Online

On your My Service Canada Account (MSCA)

On your Dashboard there is an option for OAS

Within the OAS category there is a subsection titled apply for benefits.

This is the fastest and easiest option for most people.

Paper Application

Fill out Form ISP-3550 (Application for the Old Age Security Pension).

Mail the completed form and required documents to your nearest Service Canada Office.

In Person

Visit a Service Canada Centre and submit the application with any required documents.

Required Documents

In order to apply for OAS you will be asked to provide the following documents:

Proof of legal status in Canada

Birth Certificate, Canadian Passport, Citizenship Certificate, or Permanent Resident Card.

Social Insurance Number (SIN)

Details of your residence history in Canada after age 18

Processing Times

It is generally recommended that you apply for OAS as early as possible. The processing of applications may take several months, particularly for individuals with a complex residency history.

High Income and Application Considerations

OAS calculations are made based on your prior years net world income. If you recall the OAS recovery tax or “clawback” is applied on any income above $93,454 per year.

This creates an interesting dilemma for high income earners who are looking to retire on a lower income, and receive OAS benefits. Without proper planning your OAS benefits will be “clawed back” in the first year of retirement, due to your prior years income.

There are two ways to resolve this issue:

Defer OAS Start Time

You could delay your OAS start time until the following year, whereby your benefits will be calculated on your lower income avoiding the clawback entirely.

This gives you an additional 7.2% increase in OAS payments.

However, this only works if you have enough savings to manage without the OAS benefits.

Fill out Form T1213(OAS)- Request to Reduce Old Age Security Recovery Tax at Source.

This form allows you to estimate what your current years gross income will be. The CRA will base your clawback on this current year’s estimate.

Form must be submitted to the Canada Revenue Agency (CRA).

If approved, Service Canada will reduce or eliminate the clawback immediately instead of waiting until you file next year’s income tax return.

It is unlikely you will fill out the form prior to receiving your first OAS payment. Any recovery tax or “clawback” charged will be credited to you during your income tax return, provided your income was actually below the income threshold.

OAS Tax Treatment

Like CPP, OAS is taxable income.

Unlike CPP, OAS does not get tax withheld at source when you receive your check. Instead the default option is that you will get your full gross OAS payment each month. You will then owe tax when filing your income tax return.

You can apply to have taxes withheld from your OAS payments. In order to do so you will need to complete Form ISP3520 (Request for Voluntary Federal Income Tax Deductions). This form can be used to set an exact $ amount or % of gross pay that you would like to be withheld from both CPP and OAS. The form then must be mailed to Service Canada.

At the end of each year, prior to income tax filing, Service Canada will provide you with a T4A(OAS) slip. This should appear online in your My Service Canada Account. This will provide you with information such as:

Total OAS Pension received

Income Tax deducted

OAS Recovery Tax withheld

Recovery Tax- Automatically Withheld

The OAS recovery tax or “OAS clawback” will automatically be deducted from your OAS payments. The amount is determined by your prior year income tax assessment.

Conclusion

Now that you understand how OAS works, you can see why it's such a crucial piece of the retirement puzzle. The program affects millions of Canadians and will likely play a significant role in your retirement income planning. While the rules can seem complex, having this foundational knowledge puts you ahead of most people approaching retirement. In our next post, we'll dive into specific strategies for maximizing your OAS benefits and integrating them with your overall retirement plan. For now, make sure you understand your eligibility and start thinking about how OAS fits into your retirement timeline.

If you liked this post you may also like:

[RRSP Guide 2025: Canada's Powerful Retirement Savings Tool]

[Complete Guide to Canada Pension Plan (CPP) 2025: Maximize Your Benefits & Contributions]

[4 Financial Lessons Traveling Taught Me About Money and Happiness]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Canada Revenue Agency. (2025). Old Age Security (OAS) recovery tax (clawback). Government of Canada. https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/old-age-security-recovery-tax.html

Government of Canada. (2025). Old Age Security (OAS) pension: Overview. Government of Canada. https://www.canada.ca/en/services/benefits/publicpensions/cpp/old-age-security.html

Government of Canada. (2025). Application for the Old Age Security Pension (ISP-3550). Government of Canada. https://www.canada.ca/en/services/benefits/publicpensions/cpp/old-age-security/apply.html

Service Canada. (2025). Payment amounts for Old Age Security (OAS). Government of Canada. https://www.canada.ca/en/services/benefits/publicpensions/cpp/old-age-security/payments.html

Introduction

OAS is one of the most important retirement programs in Canada, but it's also one of the most misunderstood. Many people approaching retirement have no idea how much they'll receive, when they're eligible, or what factors affect their payments. The rules around residency requirements, clawbacks, and payment calculations can seem overwhelming at first glance. This guide breaks down everything you need to know about OAS in 2025 - from basic eligibility to payment amounts to tax implications. Understanding these fundamentals is the first step toward making smart decisions about your retirement income.

What is Old Age Security (OAS)?

The Old Age Security (OAS) is a government pension that was created in order to assist seniors (age 65 or older) in meeting their basic income demands. The OAS is not meant to be an individuals only source of income in retirement. Instead it provides the foundation for what we like to call The Retirement Income Pyramid.

The OAS is funded by general tax revenue. You as a Canadian taxpayer contribute to the program indirectly by the taxes you pay throughout your daily life. The Canadian Pension Plan (CPP), on the other hand, is funded by a combination of employee, and employer contributions.

Unlike the CPP, you are not required to be employed in order to receive OAS payments. However, there are specific residency requirements that need to be met in order to be eligible for the program.

Eligibility Requirements

In order to be eligible for OAS, you need to meet the following criteria:

Be age 65 or older

Have lived in Canada for a minimum of 10 years after the age of 18

However, the 10 year minimum will only provide you with a partial OAS pension. In order to be eligible for the full pension you must have lived in Canada for 40 years after the age of 18.

Partial OAS Pension Calculation

If you meet the minimum residency requirements of 10 years, but not the maximum of 40 years you’re pensionable benefits will be calculated using the following equation:

# of years of Canadian Residency x 2.5 (1/40th) = % OAS Maximum

Ex. Mandy lived in Toronto until the age of 18. She decided to go to school at Trinity College in Dublin for Economics. After which point she found a corporate job in Ireland where she worked until age 30. She then returned back to Toronto to live closer to family as she raised her kids. She retired at age 65, and collected her OAS. In this case she lived in Canada for a total of 35 years after age 18. She will receive 87.5% of the OAS maximum benefits.

35 Years x 2.5 = 87.5% of OAS Maximum

Living Abroad and Receiving Full OAS

In some cases you may be eligible to receive the full benefits from OAS despite living abroad. The two most common exceptions would be:

Living in a country with a social security agreement with Canada

Canadian Military or Government Service

There are currently 50 countries that have a social security agreement with Canada including USA, Australia, Germany, Japan, etc. For a comprehensive list of those countries you can go to the Government of Canada website here. These countries allow you to combine years of residency when calculating OAS payments. The purpose of this exemption is to avoid cases whereby someone paid into a social security program internationally but is unable to receive the benefits.

In the case of Canadian military or government service, your time internationally may count as Canadian residency. Additionally, your spouse or partner who lived with you outside of Canada may also have that period count as Canadian residency. However, you must meet the following criteria:

You have been employed by

Canadian Government

Canadian Armed Forces.

You must maintain ties to Canada while abroad

Paying Canadian income taxes

Keeping Canada bank accounts, property, or dependents in Canada.

How Much is OAS? (2025 Numbers)

The maximum OAS payment for July-September 2025 is the following:

Age 65-74

$734.95/month or $8,795.40/year

0.6% increase for each month of deferral after age 65.

Both OAS and CPP are inflation adjusted according to the Consumer Price Index (CPI). The difference between the two programs though is that CPP adjustments are calculated annually. However, OAS is adjusted quarterly. So the maximum amounts noted above will change in October 2025. For more updated amounts you can go directly to the Government of Canada website here.

Example 1: John is age 65 and plans to start receiving his OAS payments in August 2025. He worked abroad as a pilot for most of his life. He only lived in Canada for a total of 20 years after his 18th birthday. Since the residency demands for OAS require 40 years of living in Canada, he only has 50% of the required residency time. His estimated monthly benefit should be the following:

Current Maximum OAS Benefit ($734.95) x 0.5 (50% of residency demands for maximum benefits) = $367.48

Example 2: Mark is age 65 and plans to start receiving OAS payments in August 2025. He served in the Canadian Armed Forces (CAF) as an aviation technician. He only lived in Canada for 30 years. However, he served abroad for the CAF for 10 years. During that time he owned a condo in Canada, and paid Canadian income taxes. He is eligible for the full benefit. His estimated monthly benefit is the following:

Current Maximum OAS Benefit ($734.95) x 1.0 (100% of residency demands for maximum benefits) = $734.95

Deferring OAS

The default age for starting to draw your OAS payments is age 65. Afterwards, you will be auto-enrolled into the program, and start receiving payments. However, you have the option of applying to defer your OAS payments. This can be performed on your My Service Canada Account.

Why would you want to defer payments?

For every month that you defer your OAS payments after age 65 the payment will increase by 0.6%. This results in an annual increase of 7.2%. If you defer until the age of 70 it would result in a 36% increase in payments. This increase will be applied to all future payments until the time of your death. Unlike investments, this is a guaranteed increase in payment not susceptible to volatility.

Example: Fred has his 65th birthday in 6 months. He is debating whether or not to apply for a OAS deferral. If he does he plans to wait until age 70 to start drawing OAS. He has lived in Canada for over 40 years since his 18th birthday so he should qualify for the entire OAS benefit. If he starts receiving his payments at age 65 he will receive $734.95 + any quarterly inflation adjustments for the rest of his life. However, if he delays until age 70 he will receive $999.53 + quarterly inflation adjustments for the rest of his life.

$734.95 (OAS Maximum Benefit at Age 65) x 1.36 (36% Increase in Payments from deferral)= $999.53 (OAS Maximum Benefit at Age 70)

Payment Boost at Age 75

In July 2022, the federal government introduced a permanent boost to OAS payments of 10% for everyone aged 75 and older. This is applied regardless of whether you started receiving OAS payments at age 65, or deferred until age 70.

The maximum OAS payment for July-September 2025 is the following:

Age 75

No Deferral of OAS Payments from Age 65 to Age 70

$808.45/month or $9,701.40

Deferred OAS Payments until age 70

$1099.48/month or $13,193.80

Example: Jennifer had her 75th birthday this month.

She started receiving OAS payments at age 65.

She had only 35 years of Canadian residency prior to receiving her OAS payments.

Prior to her birthday she received OAS payments of $643.08/month.

Current Maximum OAS Benefit ($734.95) x 0.875 (87.5% of residency demands for maximum benefits) = $643.08

Now that she is age 75 she will receive an additional 10% boost in payments .

$643.08 (OAS Payment prior to Age 75) x 1.10 (10% boost in payment at age 75) = $707.39 (OAS Payment at Age 75 after the 10% boost)

OAS Clawback (OAS Recovery Tax)

Unlike CPP, the OAS is subjected to something called a Recovery Tax, often referred to as a “OAS clawback”. This is an additional tax applied on high income seniors.

The purpose of the OAS clawback is to create income equity amongst retirees. The program is meant for those in most need of the funds which are low to middle income earners. Generally speaking high income earners don’t rely on the funds for survival so the payments are reduced after certain income thresholds.

Income Threshold

You will be subjected to an OAS clawback for every $1 you earn above $93,454 per year. It is important to note that the OAS is calculated based on an individuals net world income, not household income. So in theory, provided both you and your spouse make below the individual threshold you could earn a family income of $186,908.

What is included in net world income?

The CRA defines net world income as your “Net Income Before Adjustments” on a tax return. It includes things like:

Employment Income

Pension Income (OAS, CPP, RRSP/RRIF withdrawals, private pensions, etc)

Rental Income

Business Income

Non-registered Investment Income (Interest, capital gains, dividends)

Capital Gains from secondary property

Worldwide Income

Since their are several types of income sources considered in this calculation tax planning is very important. By tax planning It helps you to avoid accidentally receiving an “OAS clawback” due to a poorly timed asset sale, or overlap between employment and OAS payments.

How is the OAS Clawback Calculated

The OAS clawback is not a strict cut-off point at the income threshold. Instead the payments are gradually reduced until you reach the upper threshold of $151,668 of yearly income. At which point you will no longer be eligible to receive any OAS payments.

For every $1 you receive above the minimum threshold of $93,454, you will be required to repay 15 cents (15%) for the OAS clawback.

Ex. Jennifer earns a net world income of $115,000 in 2025. This includes $90,000 salary from her job as a district manager, $15,000 of taxable interest income from investments, and $10,000 of rental income from her secondary property. Her OAS clawback will be $3,231.90 for the year 2025. This is the calculation:

Excess over minimum income threshold: $115,000 - $93,454 = $21,546

OAS Recovery Tax or clawback: $21,546 x 0.15 (15%) = $3,231.90

Does the OAS Clawback threshold increase if I defer until 70?

No, the OAS clawback threshold does not increase if you defer your OAS payments from age 65 to age 70.

However, if you recall earlier in this post there is a 10% OAS payment boost that occurs at age 75. After this is introduced the OAS clawback maximum threshold increases from $151,668 to $157,490.

OAS Clawback- Point of Contention

The “OAS clawback” is questionable at best, and it is often a point of contention amongst retirees.

In order to qualify for the OAS program you need 10+ years of Canadian residency. In many cases, individuals have lived in the country for 40 + years. One could argue that they have paid significantly into the tax system (ie. income taxes, sales taxes, property taxes, etc). Actually, all things being equal the higher income earner will have paid more into the tax system throughout their life than lower income individuals.

The marginal tax rate of an individual living in Ontario with a net world income of $93,454 is ~30%. The “OAS clawback” or recovery tax is an additional 15%. This means that a retiree is effectively being taxed at 45% for every $1 of earnings above this income threshold.

However, the program is meant to create equity, and prevent poverty in retirement. This is accomplished through raising the minimum income floor for those who need it. Like our tax system, the more you may the more you pay in. In this case the more you make, the more they take away.

How to Apply for OAS

Provided you are a Canadian Citizen, 65 years old, and meet the minimum requirements of 10 years of residency you should be automatically enrolled into receiving OAS payments.

Service Canada will send you a letter the month after you turn 64 telling you that you either that you will be auto-enrolled, or you need to apply. If you don’t receive a letter by age 64, you should contact Service Canada to confirm if you need to apply.

You can apply for OAS as early as 11 months before your 65th birthday. If you want to defer OAS (up to age 70), you should indicate that in your application. There are three ways to apply for OAS:

Online

On your My Service Canada Account (MSCA)

On your Dashboard there is an option for OAS

Within the OAS category there is a subsection titled apply for benefits.

This is the fastest and easiest option for most people.

Paper Application

Fill out Form ISP-3550 (Application for the Old Age Security Pension).

Mail the completed form and required documents to your nearest Service Canada Office.

In Person

Visit a Service Canada Centre and submit the application with any required documents.

Required Documents

In order to apply for OAS you will be asked to provide the following documents:

Proof of legal status in Canada

Birth Certificate, Canadian Passport, Citizenship Certificate, or Permanent Resident Card.

Social Insurance Number (SIN)

Details of your residence history in Canada after age 18

Processing Times

It is generally recommended that you apply for OAS as early as possible. The processing of applications may take several months, particularly for individuals with a complex residency history.

High Income and Application Considerations

OAS calculations are made based on your prior years net world income. If you recall the OAS recovery tax or “clawback” is applied on any income above $93,454 per year.

This creates an interesting dilemma for high income earners who are looking to retire on a lower income, and receive OAS benefits. Without proper planning your OAS benefits will be “clawed back” in the first year of retirement, due to your prior years income.

There are two ways to resolve this issue:

Defer OAS Start Time

You could delay your OAS start time until the following year, whereby your benefits will be calculated on your lower income avoiding the clawback entirely.

This gives you an additional 7.2% increase in OAS payments.

However, this only works if you have enough savings to manage without the OAS benefits.

Fill out Form T1213(OAS)- Request to Reduce Old Age Security Recovery Tax at Source.

This form allows you to estimate what your current years gross income will be. The CRA will base your clawback on this current year’s estimate.

Form must be submitted to the Canada Revenue Agency (CRA).

If approved, Service Canada will reduce or eliminate the clawback immediately instead of waiting until you file next year’s income tax return.

It is unlikely you will fill out the form prior to receiving your first OAS payment. Any recovery tax or “clawback” charged will be credited to you during your income tax return, provided your income was actually below the income threshold.

OAS Tax Treatment

Like CPP, OAS is taxable income.

Unlike CPP, OAS does not get tax withheld at source when you receive your check. Instead the default option is that you will get your full gross OAS payment each month. You will then owe tax when filing your income tax return.

You can apply to have taxes withheld from your OAS payments. In order to do so you will need to complete Form ISP3520 (Request for Voluntary Federal Income Tax Deductions). This form can be used to set an exact $ amount or % of gross pay that you would like to be withheld from both CPP and OAS. The form then must be mailed to Service Canada.

At the end of each year, prior to income tax filing, Service Canada will provide you with a T4A(OAS) slip. This should appear online in your My Service Canada Account. This will provide you with information such as:

Total OAS Pension received

Income Tax deducted

OAS Recovery Tax withheld

Recovery Tax- Automatically Withheld

The OAS recovery tax or “OAS clawback” will automatically be deducted from your OAS payments. The amount is determined by your prior year income tax assessment.

Conclusion

Now that you understand how OAS works, you can see why it's such a crucial piece of the retirement puzzle. The program affects millions of Canadians and will likely play a significant role in your retirement income planning. While the rules can seem complex, having this foundational knowledge puts you ahead of most people approaching retirement. In our next post, we'll dive into specific strategies for maximizing your OAS benefits and integrating them with your overall retirement plan. For now, make sure you understand your eligibility and start thinking about how OAS fits into your retirement timeline.

If you liked this post you may also like:

[RRSP Guide 2025: Canada's Powerful Retirement Savings Tool]

[Complete Guide to Canada Pension Plan (CPP) 2025: Maximize Your Benefits & Contributions]

[4 Financial Lessons Traveling Taught Me About Money and Happiness]

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Canada Revenue Agency. (2025). Old Age Security (OAS) recovery tax (clawback). Government of Canada. https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/old-age-security-recovery-tax.html

Government of Canada. (2025). Old Age Security (OAS) pension: Overview. Government of Canada. https://www.canada.ca/en/services/benefits/publicpensions/cpp/old-age-security.html

Government of Canada. (2025). Application for the Old Age Security Pension (ISP-3550). Government of Canada. https://www.canada.ca/en/services/benefits/publicpensions/cpp/old-age-security/apply.html

Service Canada. (2025). Payment amounts for Old Age Security (OAS). Government of Canada. https://www.canada.ca/en/services/benefits/publicpensions/cpp/old-age-security/payments.html