Get our free Debt vs Invest Calculator — click here to access it

Dividend Investing: Pros, Cons, and When It Makes Sense

Dividend investing explained—pros, cons, risks, and rewards to help you decide if it’s the right wealth-building strategy.

INVESTING FOR BEGINNERSDIVIDEND INVESTING

7/2/202522 min read

Introduction

In our last post, we went over the difference between dividend and total return investing. Both when used appropriately can be effective at growing your wealth. As we discussed, total return investing tends to outperform on most available timelines. However, that doesn’t mean that it is the best strategy for your situation. This post will explore the benefits and downsides of dividend investing so that you can decide for yourself if it is right for you.

Benefits of Dividend Investing

There are several reasons why dividend investing may be beneficial for investors.

Reliable Income Stream for Retirees

If you have consistently invested over your lifetime, eventually you will be faced with the dilemma of what to do with your investments in retirement. A commonly recommended strategy is what is known as the 4% rule. The 4% rule suggests that you can safely sell and withdraw 4% of your investments annually (plus adjusting for inflation). This percentage should allow you to live off your investments throughout your retirement years without significantly drawing down your principle.

Ex. If you retire with $1,000,000 invested in a low cost index ETF such as VOO, the 4% rule says that you can safely withdraw $40,000/year.

However, the challenge for many individuals is knowing when it is a safe time to sell their stocks.

If the market decreases by 10%, should you sell less of your holdings?

And, if the market goes up by 20%, should you sell more?

Although the answer to this question is you should continue to sell 4% of your holdings regardless of the state of the market. In reality though, it isn’t that easy to implement and stick to.

A dividend investing strategy is liked among retirees because it allows you to avoid the decision around the appropriate time to sell. Instead, you focus on finding a basket of stocks, or an ETF that provides a yield close to 4%. Then, you collect your annual income in the form of a dividend. Therefore, removing the need to sell.

Lower Volatility

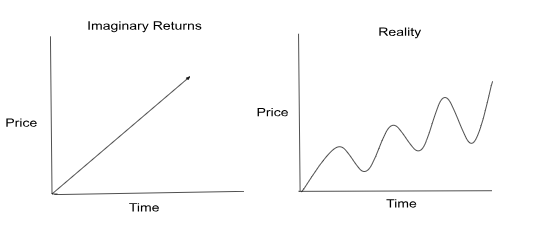

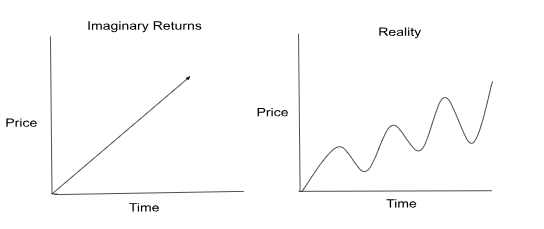

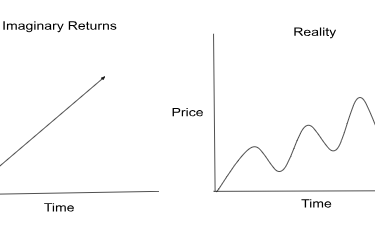

Volatility is a measurement of the amount of variance or change in price over time. In an ideal world, we would experience a linear progression in our investments. In this case, our investments would just increase gradually over time (ie. Image on left). Unfortunately, the price ends up looking more like a rollercoaster that moves above and below a growing average (ie. Image on Right).

A benefit of dividend investing is that you experience a shallower wave formation in your returns. In other words, they are less volatile and more stable over time. A research study by Frank Templeton compared a MSCI High Dividend Yield Fund with an MSCI Total Return Fund. The results showed that the high dividend fund experienced less volatility, and a lower maximum drawdown in price when measured over a 3 year period.

If you are less focused on maximizing your returns, and are looking for more stability in your portfolio, then dividend investing may fit that need.

Important Note: It is important to remember that stocks are still very volatile when compared to fixed income assets such as bonds, money market funds, or GIC’s.

Tax Benefits

Non-Registered Accounts (Canadian Dividends)

Another benefit of dividend investing is the tax implications. To dive deep on the subject you can refer to our blog post on how non-registered investments are taxed in Canada here. In brief, Canadian eligible dividends are taxed favourably relative to other investment types such as capital gains, and Interest Income. The same can’t be said for US & International dividends though, as they are subjected to a withholding tax.

If you are young, chances are that you have not maximized your registered accounts (like TFSA, RRSP, etc), and as such, this benefit isn’t important until you do so.

However, if you have maxed out your registered accounts and/or are over 65 years old, it is important you consult with a tax professional before deciding if dividends are right for you. There are a couple of reasons why:

The tax benefits occur until you earn approximately $114,750 of taxable income (as of 2025). After which point, they are taxed higher than capital gains, and become significantly less advantageous.

Canadian dividends are grossed up, which means they increase your taxable income. This can impact your ability to receive certain income tested benefits such as GIS, OAS, GST credits, & child benefits. A tax professional will help you determine if the tax benefits of the dividends is worth giving up the government support benefits.

Registered Retirement Savings Plan (US Dividends)

There is one other account that dividend investing could be tax advantageous, which is the RRSP. This applies specifically to dividends received from US listed companies. In all other accounts, any US dividends are subjected to a withholding tax of 15%. Like any tax, this reduces your returns. Over the long term, this amount could be significant. Fortunately, the RRSP is exempt from withholding tax on US dividends.

Provided this is the case, holding US dividend stocks in your RRSP would be beneficial. However, it is important to note that a smart investing approach involves you focusing on only the best companies…regardless of where they are located in the world.

Psychological Comfort

A common adage that is used amongst dividend investors says “you are being paid to wait”. This is at least partially true… especially during a bear market (usually when the market has gone down 20% or more).

The S&P 500 return since inception has been ~10%/year. The interesting thing is that by holding over this period, you would almost have never seen a 10% return in any given year. The variance ranged from -47.07% in 1931 to 46.59% in 1933. In recent memory, if you invested at the top of the market in October 2007, it would have taken until March 2013 to return to a new all-time high, and recoup your losses. That is almost 6 years of waiting.

A growth investor would have to wait this entire period until the market rebounded to get a return on their investment. However, a dividend investor would continue to receive some income throughout this period, while they waited for the market to rebound.

It is important to note this does not mean that the dividend investor makes more money. Rather their returns are more spread out over time.

Ex. Imagine John buys Apple at $10/share, and Mark buys CN Rail at $10/share in November 2000. Apple has no dividend, meanwhile, CN Rail pays out $0.50/share each year.

A market crash happens a week later, and both stocks fall by 50%. Now

John’s Apple stock is $5/share

Mark’s CN Rail stock is $5/share

Unfortunately, it takes until November 2005 (5 years later) for the market to recover. In this case, all things being equal, both stocks shouldn’t recover back to the same price point. Why? Because CN Rail paid out some of there earnings to their shareholders over the 5 years, and Apple didn’t. Instead the result look like this:

John’s Apple stock recovers to $10/share.

Mark’s CN Rail stock only recovers to $7.50/share.

This is because he received 5 payments of $0.50/share (ie. 2000, 2001, 2002, 2003, 2004) for a total of $2.50/share throughout the bear market.

If the thought of your stock portfolio dropping by 50% scares you, then maybe the stock market isn’t a good place to park your money. Instead, you should consider including more fixed income in your portfolio. However, a dividend focused strategy could be helpful psychologically to tolerate these downturns, as you continue to get paid throughout them.

Drawbacks of Dividend Investing

Dividends Are Not Guaranteed

“Nothing is certain except death and taxes”- Benjamin Franklin

A common mistake made amongst dividend investors is thinking that their dividends are guaranteed. This theory works...until it doesn’t.

Bad Times

When a company is doing well, they may choose to return some of their earnings to their shareholders in the form of a dividend. However, during tough financial times, companies will often remove and/or significantly decrease their dividend payout to save money. This could occur as a result of a recession, industry downturn or any other major disruption to their finances. Even stable mature companies are not exempt.

Ex. During the COVID-19 pandemic, several well-established companies including Disney, Boeing, and Ford cut their dividends. All of which previously had a strong dividend history. A report by S&P Global showed that there was a $42.5 Billion decrease in US dividend payments in Q2 2020 alone.

Redirection of Funds

Unlike bond interest payments, dividends are not legally required. Rather, dividends are discretionary, and up to the board of directions. In fact, even if they have the ability to pay out a dividend, they may change their corporate strategy entirely. This could include redirecting the funds towards stock buybacks, research and development, or investment strategies.

Ex. Intel cut its dividend by 66% in 2023, ending a 29-year streak, redirecting its money to infrastructure investments. In this case its fabrication facilities to build semiconductors. This was necessary in order to survive in a highly competitive environment against companies like TSMC.

Misguided Solution

In order to mitigate this risk, intelligent dividend investors search for companies with a long history of dividend payments. Hence the birth of the categories of dividend growers:

Dividend Achievers- 5+ years of dividend growth

Dividend Aristocrats- 25+ years of dividend growth

Dividend Kings- 50+ years of dividend growth.

The problem is that this may create a false sense of conviction. A companies history of paying a dividend provides no guarantee of a continuation of that trend.

Ex. General Electrics (GE) was a mature company with over 100 years of dividend payments. Unfortunately, they suffered a fall from grace. Between the years 2009 and 2018, it cut its dividend several times, eventually reducing it to just $0.01/share. This is from a high in 2008 of $1.24/share.

In any of these cases, if your predicted return depended on a dividend that no longer existed, the investment failed to deliver.

Concentration Risk

The next significant downside to a divided only investing approach is the lack of diversification. Diversification is a strategy used in investing to reduce the volatility of your portfolio, and minimize the risk of ruin. In a stock only investing strategy, diversification provides you with exposure to a variety of different companies globally. Ultimately, when you diversify your portfolio, you are trying to avoid/reduce complete exposure to a few different type of risks:

Company Specific Risk

Sector/Industry Specific Risk

Country Specific Risk

A significant flaw with dividend only investing is that you limit your available investment options. Generally, dividend stocks tend to concentrated in only a few different sectors:

Energy

Utilities

Telecommunications

Healthcare/Pharmaceuticals

Consumer Staples

REITS

Due to the smaller size of the Canadian market, the options are even more limited with significantly less high dividend paying consumer staples, and healthcare stocks relative to US.

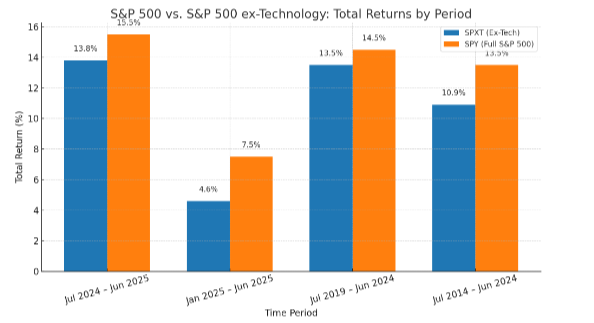

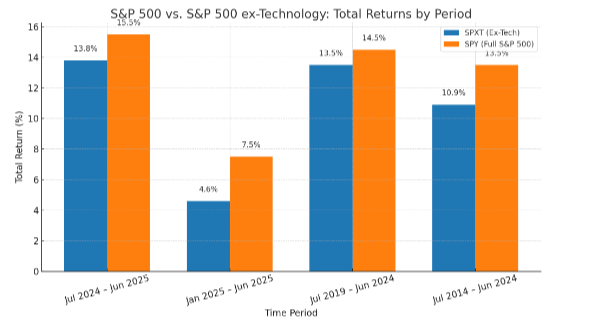

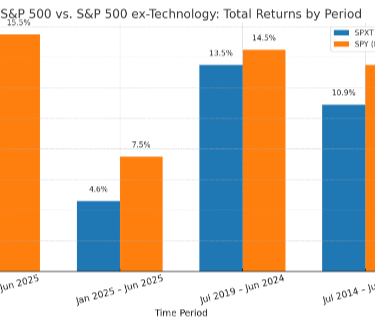

However, the most significant issue with this approach is the lack of exposure to technology. A significant amount of the gains in the S&P 500 in recent history can be attributed to the growth of the tech sector. Below is a chart comparing the S&P 500 with and without the inclusion of tech stocks. As you can see, over a 10 year period from July 2014- June 2024, the S&P500 produced a 13.5% annual rate of return (ARR). Meanwhile, when technology stocks alone are removed from this calculation, the ARR dropped down to 10.9%.

As you can see, the problem with dividend investing is not necessarily a selection problem (although it could also be this too), but rather a lack of available options. By limiting the pool of available options based on one criteria only, you can significantly drag down your long term returns.

Tax Implications

The next downside to dividend investing is the tax implications. These can be split into two categories: taxable accounts, and registered accounts. Both provide separate issues to consider.

Taxable Accounts (Taxed When Received)

As we discussed in our last post, there are two ways in which you can make money from a stocks:

The first is through price appreciation, capital gains.

The second in through income received in the form of dividends.

The problem with dividends is that you have no control over when you receive them, and they are taxed in the year they are received. You do not have the capacity to delay the payments of dividends in order to avoid a tax burden.

Capital gains, on the other hand, are only taxed when they are realized. Said another way, they are only taxed after you actually sell the stock and “realize” your gain. This provides significant flexibility in terms of when you are taxed. It allows you to delay taxation to a later year when your income is lower (ie. retirement, parental leave, unemployment).

For more information on how each of the assets are taxed, you can refer to this post here.

Registered Accounts

In all registered accounts, with the exception of the RRSP, all foreign dividends are subjected to a withholding tax. As we noted above, the US withholding tax is 15%. Since a well diversified dividend investing strategy will require some US holdings, this has the potential to eat into your long term returns over time.

Please note: This also applies to taxable accounts too. However, there is the ability to apply for a foreign tax credit to offset some of the losses.

Psychological Trap (Chasing Yield)

There is a term often used in investing which is know as “Chasing Yield”. This isn’t necessarily an issue with dividend investing per se, but rather how it is applied. An experienced investor should always look for a company in good financial standing. They should ask themselves questions such as:

Is the company making money, and growing profits over time?

Does the company have a manageable amount of debt? Can it be paid off in a reasonable amount of time using free cash flow, or near term profits?

Does the company actually have the money to pay this dividend?

How is this company paying this dividend? Is it from excess profits, are they cutting into their free cash, or even worse are they using debt?

Inexperienced dividend investors will evaluate a company solely based on its “Dividend Yield”. This often results in them purchasing stocks with outrageous yields, such as 7% or more. The problem is that these companies often fail the questions mentioned above. Many shouldn’t even be paying a dividend, let alone a high one. Instead, they pay a high dividend solely to attract investors, or avoid current investors from liquidating. Their survival depends on paying a high dividend, that they can’t afford.

Why do Inexperienced Investors fall into a Yield Trap?

The obvious answer is that they fail to look at the financial standing of said investment. However, there is another less obvious issue that is often ignored. It is that people assume a dividend is additive to your total return.

We hear from personal finance experts that stocks typically produce 7-10%/year. This assumes you invest in a low cost S&P 500 Index ETF. However, the second part is often ignored. Instead, the inexperienced investor buys a dividend stock yielding 6%/year. Their flawed mental math says 7%+6%=13% which is an amazing return. The problem is that this almost never happens. Lets assume the stock in question actually performs as well as the S&P 500 (~10%/year). Well at a 6% dividend yield you should assume a 4%/year growth in price.

Dividends are simply a method of distributing the return of capital over time. Instead of waiting to sell your stock to capture all of the returns, they are paid out to your in advance. By you taking the money earlier, the company has less money to invest in other areas of growth, thereby dragging down your returns.

Conclusion

Dividend investing offers psychological comfort and steady income, but comes with trade-offs like reduced diversification and potential tax inefficiencies. Total return investing often delivers stronger long-term growth and greater flexibility. The best approach depends on your goals, time horizon, and risk tolerance. For many investors, combining both strategies can offer a balanced path to wealth building.

If you liked this post you may also like:

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Bennett, B. (2023, February 27). The Intel Dividend Cut: What It Means for Investors. The Motley Fool. https://www.fool.com/investing/2023/02/27/the-intel-dividend-cut-what-it-means-for-investors/

Franklin Templeton. (n.d.). Understanding volatility: How dividend stocks compare. Franklin Templeton Investments. (Implied from volatility comparison in dividend investing section; you may replace with exact study URL if needed.)

Investopedia. (n.d.). GE Dividends Slashed Over 90%. https://www.investopedia.com/news/ge-dividends-slashed-over-90/

ProShares. (2025). ProShares S&P 500 Ex-Technology ETF (SPXT) Performance. https://www.financecharts.com/etfs/SPXT/performance/total-return

ProShares. (2025). SPXT: Fund Overview & Historical Performance. https://www.proshares.com/our-etfs/strategic/spxt/

S&P Dow Jones Indices. (2020, July 2). S&P Dow Jones Indices Reports $42.5 Billion Decrease in U.S. Indicated Dividend Payments for Q2 2020 – Worst Quarter Since Q1 2009. https://www.spglobal.com/spdji/en/corporate-news/article/sp-dow-jones-indices-reports-425-billion-decrease-in-u-s-indicated-dividend-payments-for-q2-2020-worst-quarter-since-q1-2009/

SPDR. (2025). SPDR S&P 500 ETF Trust (SPY) Performance Summary. https://www.ssga.com/us/en/individual/etfs/funds/spdr-sp-500-etf-trust-spy

YCharts. (2025). S&P 500 12-Month Total Return. https://ycharts.com/indicators/sp_500_12_month_total_return

Introduction

In our last post, we went over the difference between dividend and total return investing. Both when used appropriately can be effective at growing your wealth. As we discussed, total return investing tends to outperform on most available timelines. However, that doesn’t mean that it is the best strategy for your situation. This post will explore the benefits and downsides of dividend investing so that you can decide for yourself if it is right for you.

Benefits of Dividend Investing

There are several reasons why dividend investing may be beneficial for investors.

Reliable Income Stream for Retirees

If you have consistently invested over your lifetime, eventually you will be faced with the dilemma of what to do with your investments in retirement. A commonly recommended strategy is what is known as the 4% rule. The 4% rule suggests that you can safely sell and withdraw 4% of your investments annually (plus adjusting for inflation). This percentage should allow you to live off your investments throughout your retirement years without significantly drawing down your principle.

Ex. If you retire with $1,000,000 invested in a low cost index ETF such as VOO, the 4% rule says that you can safely withdraw $40,000/year.

However, the challenge for many individuals is knowing when it is a safe time to sell their stocks.

If the market decreases by 10%, should you sell less of your holdings?

And, if the market goes up by 20%, should you sell more?

Although the answer to this question is you should continue to sell 4% of your holdings regardless of the state of the market. In reality though, it isn’t that easy to implement and stick to.

A dividend investing strategy is liked among retirees because it allows you to avoid the decision around the appropriate time to sell. Instead, you focus on finding a basket of stocks, or an ETF that provides a yield close to 4%. Then, you collect your annual income in the form of a dividend. Therefore, removing the need to sell.

Lower Volatility

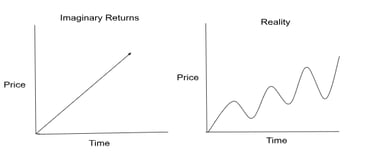

Volatility is a measurement of the amount of variance or change in price over time. In an ideal world, we would experience a linear progression in our investments. In this case, our investments would just increase gradually over time (ie. Image on left). Unfortunately, the price ends up looking more like a rollercoaster that moves above and below a growing average (ie. Image on Right).

A benefit of dividend investing is that you experience a shallower wave formation in your returns. In other words, they are less volatile and more stable over time. A research study by Frank Templeton compared a MSCI High Dividend Yield Fund with an MSCI Total Return Fund. The results showed that the high dividend fund experienced less volatility, and a lower maximum drawdown in price when measured over a 3 year period.

If you are less focused on maximizing your returns, and are looking for more stability in your portfolio, then dividend investing may fit that need.

Important Note: It is important to remember that stocks are still very volatile when compared to fixed income assets such as bonds, money market funds, or GIC’s.

Tax Benefits

Non-Registered Accounts (Canadian Dividends)

Another benefit of dividend investing is the tax implications. To dive deep on the subject you can refer to our blog post on how non-registered investments are taxed in Canada here. In brief, Canadian eligible dividends are taxed favourably relative to other investment types such as capital gains, and Interest Income. The same can’t be said for US & International dividends though, as they are subjected to a withholding tax.

If you are young, chances are that you have not maximized your registered accounts (like TFSA, RRSP, etc), and as such, this benefit isn’t important until you do so.

However, if you have maxed out your registered accounts and/or are over 65 years old, it is important you consult with a tax professional before deciding if dividends are right for you. There are a couple of reasons why:

The tax benefits occur until you earn approximately $114,750 of taxable income (as of 2025). After which point, they are taxed higher than capital gains, and become significantly less advantageous.

Canadian dividends are grossed up, which means they increase your taxable income. This can impact your ability to receive certain income tested benefits such as GIS, OAS, GST credits, & child benefits. A tax professional will help you determine if the tax benefits of the dividends is worth giving up the government support benefits.

Registered Retirement Savings Plan (US Dividends)

There is one other account that dividend investing could be tax advantageous, which is the RRSP. This applies specifically to dividends received from US listed companies. In all other accounts, any US dividends are subjected to a withholding tax of 15%. Like any tax, this reduces your returns. Over the long term, this amount could be significant. Fortunately, the RRSP is exempt from withholding tax on US dividends.

Provided this is the case, holding US dividend stocks in your RRSP would be beneficial. However, it is important to note that a smart investing approach involves you focusing on only the best companies…regardless of where they are located in the world.

Psychological Comfort

A common adage that is used amongst dividend investors says “you are being paid to wait”. This is at least partially true… especially during a bear market (usually when the market has gone down 20% or more).

The S&P 500 return since inception has been ~10%/year. The interesting thing is that by holding over this period, you would almost have never seen a 10% return in any given year. The variance ranged from -47.07% in 1931 to 46.59% in 1933. In recent memory, if you invested at the top of the market in October 2007, it would have taken until March 2013 to return to a new all-time high, and recoup your losses. That is almost 6 years of waiting.

A growth investor would have to wait this entire period until the market rebounded to get a return on their investment. However, a dividend investor would continue to receive some income throughout this period, while they waited for the market to rebound.

It is important to note this does not mean that the dividend investor makes more money. Rather their returns are more spread out over time.

Ex. Imagine John buys Apple at $10/share, and Mark buys CN Rail at $10/share in November 2000. Apple has no dividend, meanwhile, CN Rail pays out $0.50/share each year.

A market crash happens a week later, and both stocks fall by 50%. Now

John’s Apple stock is $5/share

Mark’s CN Rail stock is $5/share

Unfortunately, it takes until November 2005 (5 years later) for the market to recover. In this case, all things being equal, both stocks shouldn’t recover back to the same price point. Why? Because CN Rail paid out some of there earnings to their shareholders over the 5 years, and Apple didn’t. Instead the result look like this:

John’s Apple stock recovers to $10/share.

Mark’s CN Rail stock only recovers to $7.50/share.

This is because he received 5 payments of $0.50/share (ie. 2000, 2001, 2002, 2003, 2004) for a total of $2.50/share throughout the bear market.

If the thought of your stock portfolio dropping by 50% scares you, then maybe the stock market isn’t a good place to park your money. Instead, you should consider including more fixed income in your portfolio. However, a dividend focused strategy could be helpful psychologically to tolerate these downturns, as you continue to get paid throughout them.

Drawbacks of Dividend Investing

Dividends Are Not Guaranteed

“Nothing is certain except death and taxes”- Benjamin Franklin

A common mistake made amongst dividend investors is thinking that their dividends are guaranteed. This theory works...until it doesn’t.

Bad Times

When a company is doing well, they may choose to return some of their earnings to their shareholders in the form of a dividend. However, during tough financial times, companies will often remove and/or significantly decrease their dividend payout to save money. This could occur as a result of a recession, industry downturn or any other major disruption to their finances. Even stable mature companies are not exempt.

Ex. During the COVID-19 pandemic, several well-established companies including Disney, Boeing, and Ford cut their dividends. All of which previously had a strong dividend history. A report by S&P Global showed that there was a $42.5 Billion decrease in US dividend payments in Q2 2020 alone.

Redirection of Funds

Unlike bond interest payments, dividends are not legally required. Rather, dividends are discretionary, and up to the board of directions. In fact, even if they have the ability to pay out a dividend, they may change their corporate strategy entirely. This could include redirecting the funds towards stock buybacks, research and development, or investment strategies.

Ex. Intel cut its dividend by 66% in 2023, ending a 29-year streak, redirecting its money to infrastructure investments. In this case its fabrication facilities to build semiconductors. This was necessary in order to survive in a highly competitive environment against companies like TSMC.

Misguided Solution

In order to mitigate this risk, intelligent dividend investors search for companies with a long history of dividend payments. Hence the birth of the categories of dividend growers:

Dividend Achievers- 5+ years of dividend growth

Dividend Aristocrats- 25+ years of dividend growth

Dividend Kings- 50+ years of dividend growth.

The problem is that this may create a false sense of conviction. A companies history of paying a dividend provides no guarantee of a continuation of that trend.

Ex. General Electrics (GE) was a mature company with over 100 years of dividend payments. Unfortunately, they suffered a fall from grace. Between the years 2009 and 2018, it cut its dividend several times, eventually reducing it to just $0.01/share. This is from a high in 2008 of $1.24/share.

In any of these cases, if your predicted return depended on a dividend that no longer existed, the investment failed to deliver.

Concentration Risk

The next significant downside to a divided only investing approach is the lack of diversification. Diversification is a strategy used in investing to reduce the volatility of your portfolio, and minimize the risk of ruin. In a stock only investing strategy, diversification provides you with exposure to a variety of different companies globally. Ultimately, when you diversify your portfolio, you are trying to avoid/reduce complete exposure to a few different type of risks:

Company Specific Risk

Sector/Industry Specific Risk

Country Specific Risk

A significant flaw with dividend only investing is that you limit your available investment options. Generally, dividend stocks tend to concentrated in only a few different sectors:

Energy

Utilities

Telecommunications

Healthcare/Pharmaceuticals

Consumer Staples

REITS

Due to the smaller size of the Canadian market, the options are even more limited with significantly less high dividend paying consumer staples, and healthcare stocks relative to US.

However, the most significant issue with this approach is the lack of exposure to technology. A significant amount of the gains in the S&P 500 in recent history can be attributed to the growth of the tech sector. Below is a chart comparing the S&P 500 with and without the inclusion of tech stocks. As you can see, over a 10 year period from July 2014- June 2024, the S&P500 produced a 13.5% annual rate of return (ARR). Meanwhile, when technology stocks alone are removed from this calculation, the ARR dropped down to 10.9%.

As you can see, the problem with dividend investing is not necessarily a selection problem (although it could also be this too), but rather a lack of available options. By limiting the pool of available options based on one criteria only, you can significantly drag down your long term returns.

Tax Implications

The next downside to dividend investing is the tax implications. These can be split into two categories: taxable accounts, and registered accounts. Both provide separate issues to consider.

Taxable Accounts (Taxed When Received)

As we discussed in our last post, there are two ways in which you can make money from a stocks:

The first is through price appreciation, capital gains.

The second in through income received in the form of dividends.

The problem with dividends is that you have no control over when you receive them, and they are taxed in the year they are received. You do not have the capacity to delay the payments of dividends in order to avoid a tax burden.

Capital gains, on the other hand, are only taxed when they are realized. Said another way, they are only taxed after you actually sell the stock and “realize” your gain. This provides significant flexibility in terms of when you are taxed. It allows you to delay taxation to a later year when your income is lower (ie. retirement, parental leave, unemployment).

For more information on how each of the assets are taxed, you can refer to this post here.

Registered Accounts

In all registered accounts, with the exception of the RRSP, all foreign dividends are subjected to a withholding tax. As we noted above, the US withholding tax is 15%. Since a well diversified dividend investing strategy will require some US holdings, this has the potential to eat into your long term returns over time.

Please note: This also applies to taxable accounts too. However, there is the ability to apply for a foreign tax credit to offset some of the losses.

Psychological Trap (Chasing Yield)

There is a term often used in investing which is know as “Chasing Yield”. This isn’t necessarily an issue with dividend investing per se, but rather how it is applied. An experienced investor should always look for a company in good financial standing. They should ask themselves questions such as:

Is the company making money, and growing profits over time?

Does the company have a manageable amount of debt? Can it be paid off in a reasonable amount of time using free cash flow, or near term profits?

Does the company actually have the money to pay this dividend?

How is this company paying this dividend? Is it from excess profits, are they cutting into their free cash, or even worse are they using debt?

Inexperienced dividend investors will evaluate a company solely based on its “Dividend Yield”. This often results in them purchasing stocks with outrageous yields, such as 7% or more. The problem is that these companies often fail the questions mentioned above. Many shouldn’t even be paying a dividend, let alone a high one. Instead, they pay a high dividend solely to attract investors, or avoid current investors from liquidating. Their survival depends on paying a high dividend, that they can’t afford.

Why do Inexperienced Investors fall into a Yield Trap?

The obvious answer is that they fail to look at the financial standing of said investment. However, there is another less obvious issue that is often ignored. It is that people assume a dividend is additive to your total return.

We hear from personal finance experts that stocks typically produce 7-10%/year. This assumes you invest in a low cost S&P 500 Index ETF. However, the second part is often ignored. Instead, the inexperienced investor buys a dividend stock yielding 6%/year. Their flawed mental math says 7%+6%=13% which is an amazing return. The problem is that this almost never happens. Lets assume the stock in question actually performs as well as the S&P 500 (~10%/year). Well at a 6% dividend yield you should assume a 4%/year growth in price.

Dividends are simply a method of distributing the return of capital over time. Instead of waiting to sell your stock to capture all of the returns, they are paid out to your in advance. By you taking the money earlier, the company has less money to invest in other areas of growth, thereby dragging down your returns.

Conclusion

Dividend investing offers psychological comfort and steady income, but comes with trade-offs like reduced diversification and potential tax inefficiencies. Total return investing often delivers stronger long-term growth and greater flexibility. The best approach depends on your goals, time horizon, and risk tolerance. For many investors, combining both strategies can offer a balanced path to wealth building.

If you liked this post you may also like:

Disclaimer: The information discussed in this blog is not financial advice, and is meant for educational purposes only. Please consult a personal financial expert before making any financial decisions.

Citations

Bennett, B. (2023, February 27). The Intel Dividend Cut: What It Means for Investors. The Motley Fool. https://www.fool.com/investing/2023/02/27/the-intel-dividend-cut-what-it-means-for-investors/

Franklin Templeton. (n.d.). Understanding volatility: How dividend stocks compare. Franklin Templeton Investments. (Implied from volatility comparison in dividend investing section; you may replace with exact study URL if needed.)

Investopedia. (n.d.). GE Dividends Slashed Over 90%. https://www.investopedia.com/news/ge-dividends-slashed-over-90/

ProShares. (2025). ProShares S&P 500 Ex-Technology ETF (SPXT) Performance. https://www.financecharts.com/etfs/SPXT/performance/total-return

ProShares. (2025). SPXT: Fund Overview & Historical Performance. https://www.proshares.com/our-etfs/strategic/spxt/

S&P Dow Jones Indices. (2020, July 2). S&P Dow Jones Indices Reports $42.5 Billion Decrease in U.S. Indicated Dividend Payments for Q2 2020 – Worst Quarter Since Q1 2009. https://www.spglobal.com/spdji/en/corporate-news/article/sp-dow-jones-indices-reports-425-billion-decrease-in-u-s-indicated-dividend-payments-for-q2-2020-worst-quarter-since-q1-2009/

SPDR. (2025). SPDR S&P 500 ETF Trust (SPY) Performance Summary. https://www.ssga.com/us/en/individual/etfs/funds/spdr-sp-500-etf-trust-spy

YCharts. (2025). S&P 500 12-Month Total Return. https://ycharts.com/indicators/sp_500_12_month_total_return